The Global X Hydrogen ETF (ASX: HGEN) has returned approximately 83% year to date through mid-May 2026, a figure that places it among the highest-performing exchange-traded funds on the ASX this year. The broader Australian market has delivered nothing close. Nor have most thematic ETFs: ERTH gained roughly 24% over the prior 12 months, and HVLU rose more than 22% year to date, both strong results that still trail HGEN by a wide margin.

What makes the number more striking is where it started. The hydrogen sector collapsed 60-70% from its 2021 highs, wiping out early investors and sending several pure-play names toward going-concern warnings. The 2026 rally is not a fresh breakout; it is a recovery from one of the deepest drawdowns in thematic ETF history, powered by a convergence of policy commitments, operational milestones at key holdings, and a weaker Australian dollar.

This analysis examines what HGEN actually holds, what has driven the surge, which policy and company developments underpin it, and what Australian investors should weigh before treating the fund as a portfolio position rather than a headline.

From 2021 crash to 2026 comeback: HGEN’s extraordinary recovery in context

The hydrogen sector peaked in early 2021 on a wave of net-zero pledges, speculative capital, and ambitious government roadmaps. What followed was severe. According to ETF Stream, hydrogen ETFs suffered drawdowns of 60-70% from those peaks as electrolyser orders stalled, cost projections disappointed, and capital rotated elsewhere. Investors who held through the trough absorbed years of negative returns before any recovery materialised.

HGEN’s 83% year-to-date gain through mid-May 2026 needs to be read against that backdrop. This is a high-beta rebound from a historically deep drawdown, not the steady compounding of a diversified equity fund.

ASX thematic ETF returns in April 2026 illustrated the same dynamic playing out across HGEN’s full year-to-date run: leveraged and concentrated funds posted headline numbers that obscured the policy qualifications and valuation risks sitting beneath them, including a domestic federal budget that halved key hydrogen programme spending even as the international narrative remained bullish.

The fund has also outperformed its offshore hydrogen ETF peers by a considerable margin:

- HGEN (ASX): approximately +83% YTD (mid-May 2026)

- Global X HYDR (NASDAQ): approximately +60-65% YTD (to 30 April 2026)

- Defiance HDRO (NYSE Arca): approximately +55-60% YTD (to 30 April 2026)

- L&G Hydrogen Economy UCITS ETF: approximately +50-55% YTD (to 30 April 2026)

The 15-25 percentage point gap between HGEN and its peers reflects two factors beyond stock selection: AUD weakness has amplified the fund’s Australian dollar returns relative to the underlying USD-denominated portfolio, and index construction differences mean HGEN carries heavier weightings in names that rallied hardest.

“After such a violent rebound, the risk is that expectations for orders and subsidies outrun what’s actually contracted.” — Local broker commentary, Australian Financial Review, 19 May 2026

When big ASX news breaks, our subscribers know first

What HGEN actually holds: fund mechanics and portfolio construction

Index, fees, and fund size

HGEN tracks the Solactive Global Hydrogen ESG Index, a rules-based index that screens for companies involved in hydrogen production, equipment manufacturing, fuel cells, and electrolysers, with an ESG overlay. The fund charges a management expense ratio (MER) of 0.69% per annum, as stated in the Product Disclosure Statement (PDS) dated 15 April 2025. Total fund size sits at approximately A$55-60 million as of mid-May 2026, making it a relatively small fund by ASX ETF standards.

The Global X HGEN fund overview confirms the 0.69% management fee and the Solactive Global Hydrogen ESG Index as the benchmark, providing Australian investors with the primary reference point for verifying fund mechanics and accessing the current Product Disclosure Statement.

Portfolio concentration: who the fund is actually betting on

The holdings tell a concentrated story. Bloom Energy alone represents approximately 18.75% of the fund, nearly one-fifth of total assets in a single solid oxide fuel cell manufacturer. Plug Power follows at roughly 9.8-10.4%. The top 10 holdings typically comprise more than half of fund assets, a concentration level the PDS explicitly flags as a risk factor.

ETF concentration risk is not uniformly distributed across the ASX fund universe; a passive broad-market fund holding 500 names carries fundamentally different single-stock exposure than a thematic fund where one holding represents nearly 19% of assets, and that structural difference shapes how investors should size each type of position within a portfolio.

| Company | Approx. Weighting | Country | Sub-sector |

|---|---|---|---|

| Bloom Energy | ~18.75% | United States | Fuel cell |

| Plug Power | ~9.8-10.4% | United States | Electrolyser / fuel cell |

| Doosan Fuel Cell | ~8.9% | South Korea | Fuel cell |

| Kaori Heat Treatment | ~7.9% | Japan | Electrolyser components |

| Nel ASA | Single-digit % | Norway | Electrolyser |

| Ballard Power Systems | Single-digit % | Canada | Fuel cell |

| ITM Power | Single-digit % | United Kingdom | Electrolyser |

| FuelCell Energy | Low single-digit % | United States | Fuel cell |

| Air Liquide | Low single-digit % | France | Industrial gas |

| Linde | Low single-digit % | Germany | Industrial gas |

Geographically, the United States represents the dominant weighting at roughly 45-50% of the portfolio, with Japan, the United Kingdom, Norway, South Korea, France, Germany, and Canada each contributing single-digit allocations. Australian investors buying HGEN are taking on unhedged cross-currency exposure across multiple developed markets.

The policy engine: why government spending is reshaping hydrogen economics in 2026

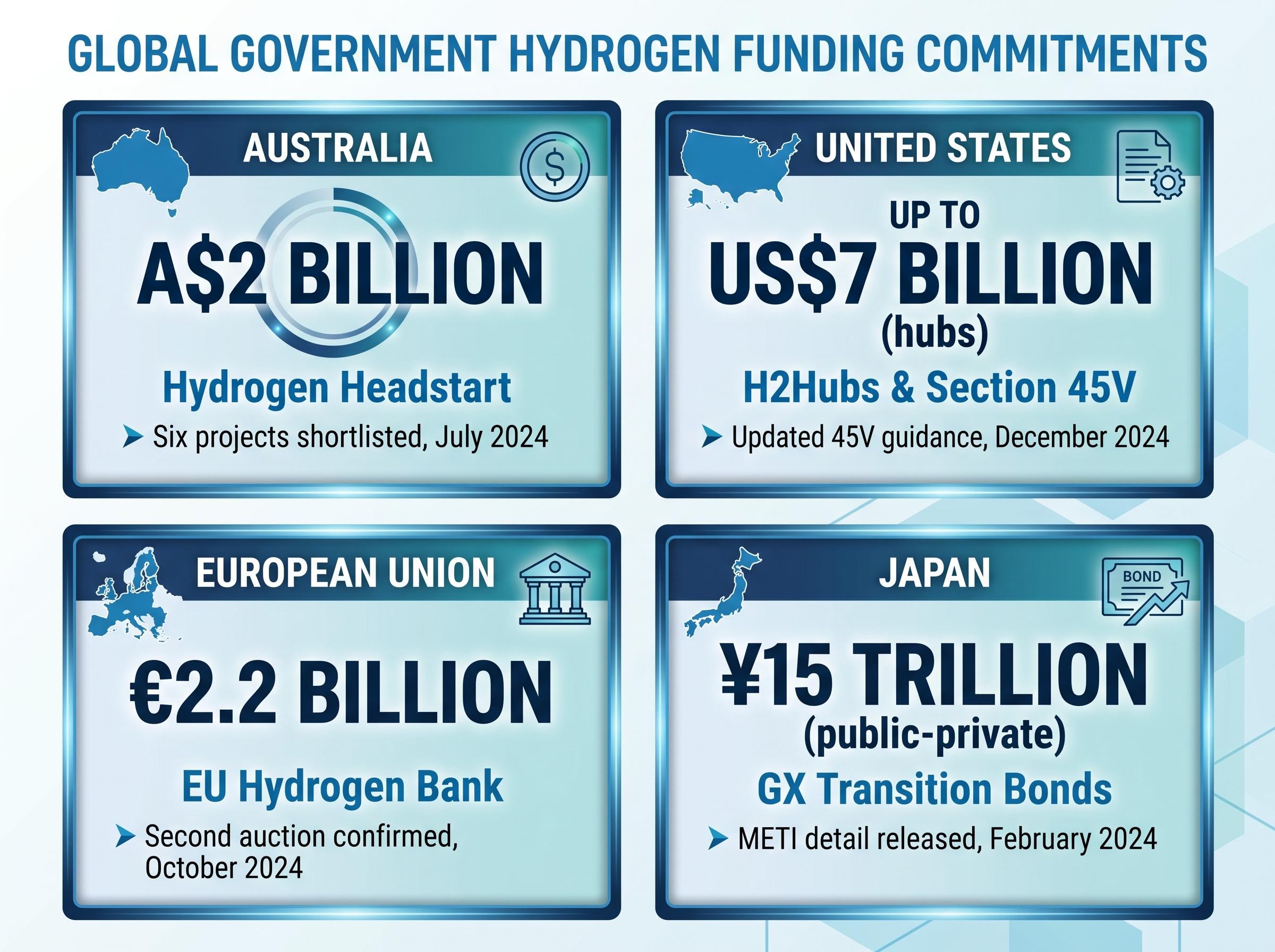

The 2026 re-rating is not sentiment alone. Governments across four major jurisdictions have moved from roadmaps to committed capital, and the scale of that commitment has changed the investment arithmetic for the companies HGEN holds.

| Country / Region | Programme | Amount Committed | Key Development |

|---|---|---|---|

| Australia | Hydrogen Headstart | A$2 billion | Six projects shortlisted, July 2024 |

| United States | H2Hubs / Section 45V | Up to US$7 billion (hubs) | Updated 45V guidance, December 2024 |

| European Union | EU Hydrogen Bank | €2.2 billion (second auction) | Second auction confirmed, October 2024 |

| Japan | GX Transition Bonds | ¥15 trillion (public-private target) | METI detail released, February 2024 |

For Australian investors specifically, the domestic policy stack has deepened:

- ARENA shortlisted six projects under Hydrogen Headstart in July 2024, representing up to 1.8 GW of electrolyser capacity and billions in potential private co-investment.

- The 2025-26 Federal Budget confirmed additional tax incentives under the Future Made in Australia framework, improving bankability for export-oriented hydrogen projects.

- Queensland and Western Australia have both updated state-level strategies, with infrastructure funding and land allocation for large-scale hubs in Gladstone, Townsville, and the Pilbara.

The policy effect flows directly into HGEN’s portfolio. The US Department of Energy’s conditional loan commitment of up to US$1.5 billion to Plug Power, the fund’s second-largest holding, is one example. Bloomberg reported in January 2025 that the updated Section 45V guidance “unlocks long-term subsidy visibility” for compliant projects, a shift that underpins final investment decisions across the hydrogen value chain.

Green hydrogen 101: what the technology actually does and why commercialisation is the hard part

Green, blue, and grey: the hydrogen spectrum that shapes the ETF’s mandate

Hydrogen is an energy carrier, not a primary energy source. It stores and transports energy produced elsewhere, which means the method of production determines its environmental profile. Three categories matter:

- Green hydrogen: Produced by splitting water into hydrogen and oxygen using an electrolyser powered by renewable electricity. Zero direct carbon emissions.

- Blue hydrogen: Produced from natural gas with carbon capture and storage applied to the emissions. Lower carbon intensity than grey, but not zero.

- Grey hydrogen: Produced from natural gas without carbon capture. This accounts for the vast majority of global hydrogen production today and carries a substantial emissions footprint.

The Solactive index that HGEN tracks focuses on companies involved in green hydrogen production, fuel cell technology, and electrolyser manufacturing, meaning the fund is positioned around the highest-cost, lowest-emission end of the spectrum.

Why the cost gap still matters for investors in 2026

Green hydrogen remains approximately two to three times the cost of hydrogen produced from unabated fossil fuels in most regions, according to the International Energy Agency’s Global Hydrogen Review released in September 2024. Electrolyser costs have declined, but not fast enough to close the gap without sustained policy support.

Morningstar’s March 2025 research concluded that widespread commercial adoption of green hydrogen in heavy industry, including steel, chemicals, and heavy transport, is more a 2030s development than a 2020s one. Bloomberg Intelligence noted in February 2025 that electrolyser utilisation factors remain uncertain, with project delays from permitting, grid interconnection, and policy clarity capable of pushing out revenue recognition by several years.

Most of HGEN’s pure-play holdings remain pre-profit. The ETF is pricing in a future state, one where green hydrogen achieves cost parity and industrial adoption scales, that has not yet arrived.

What Australian investors need to weigh before buying HGEN

An 83% year-to-date return creates its own risk profile. Three categories deserve specific attention from Australian investors considering a position at current levels:

- Concentration and liquidity risk: The top 10 holdings represent more than half of fund assets, and many constituents are small- and mid-cap names. Morningstar has warned that hydrogen ETFs “tend to cluster into a handful of names,” amplifying single-stock and thematic risk. Liquidity in underlying securities may tighten in stressed conditions.

- Valuation and earnings risk: Goldman Sachs noted in June 2024 that many hydrogen equipment names still traded at high revenue multiples relative to near-term order books, exposing investors to downside if contracted orders or policy incentives disappoint. Most pure-play holdings remain EBITDA-negative.

- Currency risk: AUD weakness has amplified HGEN’s Australian dollar return relative to the underlying USD-denominated portfolio. A reversal in the AUD/USD exchange rate would compress returns even if underlying holdings held steady, creating two-way currency exposure that investors may not have priced in.

“Hydrogen equities may offer optionality on a policy-backed decarbonisation theme, but with high volatility and execution risk.” — Morgan Stanley energy transition report, January 2026

That framing captures the position honestly. After an 83% run, an Australian investor is not entering a discounted opportunity; they are entering a high-momentum, high-volatility thematic position after a significant re-rating, where the risk of a sharp reversal is as structurally present as the policy tailwinds.

Thematic ETF sizing recommendations from advisers consistently land at 10-15% of a portfolio as a satellite allocation, a ceiling that carries particular weight after a sector has already delivered an 83% run, since deploying a full strategic position into a high-momentum thematic after the re-rating has occurred is precisely the scenario where the behaviour gap between reported returns and investor-experienced returns widens most sharply.

Momentum or mispricing? The case for and against hydrogen as a durable investment theme

Signs of genuine progress at the company level

The bull case is not pure speculation. Several of HGEN’s largest holdings have delivered operational milestones that would have seemed unlikely two years ago.

Bloom Energy reported positive operating cash flow for FY 2024 and narrowing net losses, driven by solid oxide fuel cell deployments. Nel ASA outlined a restructuring plan targeting EBITDA break-even by 2027, with a focus on large-scale electrolyser manufacturing. Plug Power recorded record electrolyser shipments in FY 2024 and secured the DOE’s conditional loan commitment of up to US$1.5 billion, with management guiding toward break-even by 2027. The industrial gas majors, Air Liquide and Linde, have committed real capital to hydrogen infrastructure projects, including EU Hydrogen Bank-supported developments.

The structural risks that persist after the rally

The bear case carries equal specificity. Goldman Sachs upgraded several hydrogen names from Sell to Neutral in June 2024 but maintained caution on near-term profitability, noting that valuations remained stretched relative to contracted order books. The IEA’s cost data shows green hydrogen at two to three times the cost of fossil-fuel alternatives. Bloomberg Intelligence has flagged project delays as a persistent risk to revenue recognition. The AFR broker warning from 19 May 2026 summarised the concern directly: expectations may be outrunning contracted reality.

| Bull Case: Key Evidence | Bear Case: Key Evidence |

|---|---|

| Bloom Energy positive operating cash flow, FY 2024 | Green hydrogen 2-3x cost of fossil-fuel hydrogen (IEA, 2024) |

| Nel ASA restructuring targets EBITDA break-even by 2027 | Goldman Sachs: high revenue multiples vs. near-term order books |

| Plug Power record electrolyser shipments; US$1.5B DOE loan | Bloomberg Intelligence: project delays push out revenue recognition |

| Air Liquide and Linde committing capital to hydrogen infrastructure | Most pure-play holdings remain EBITDA-negative |

| Multi-jurisdictional policy commitments exceeding A$30B combined | AFR broker: “expectations may outrun what’s actually contracted” |

Within the broader 2026 ASX thematic ETF space, neither ERTH (approximately +24% over 12 months) nor HVLU (more than +22% YTD) has come close to HGEN’s pace. That gap reinforces the fund’s character: this is a high-beta, high-conviction thematic position, not a core allocation.

ASX satellite allocations across cybersecurity, robotics, and gaming thematic ETFs have shown in 2026 that thematic performance dispersion is not just a feature of hydrogen exposure; RBTZ returned approximately 19.6% over one year while ESPO fell more than 15%, a reminder that sector selection within a satellite portfolio carries as much consequence as the decision to use thematic funds at all.

The hydrogen investment thesis in 2026 is compelling, contested, and not for the faint-hearted

HGEN’s 83% year-to-date return reflects a genuine policy and sentiment re-rating across the hydrogen sector. Governments in Australia, the United States, the European Union, and Japan have moved from aspirational targets to committed capital, and several of the fund’s largest holdings have reached operational milestones that mark real progress toward financial sustainability.

The structural challenges that caused the 2021-2023 collapse have not been resolved, however. They have been partially offset. Green hydrogen remains materially more expensive than fossil-fuel alternatives, commercialisation timelines extend into the 2030s, and the fund’s concentrated portfolio amplifies both upside and downside. AUD weakness has boosted returns for Australian investors, but that currency tailwind reverses if the dollar strengthens.

HGEN suits a specific investor profile: those with a long time horizon, genuine conviction in the hydrogen decarbonisation pathway, high tolerance for volatility, and the discipline to size a thematic position appropriately within a diversified portfolio. For that investor, the fund offers direct exposure to a policy-backed structural trend. For everyone else, the 83% number is best understood as evidence of what hydrogen equities can do, in both directions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.