What a Random ASX Backtest Reveals About Managing Market Risk

2 hrs ago

A hedge fund founded by a former OpenAI researcher who publicly argues that artificial general intelligence arrives by 2027 has just disclosed roughly $8 billion in bearish bets against the most prominent AI chip stocks on the market. The fund is Situational Awareness LP. The founder is Leopold Aschenbrenner. And the portfolio he has built does not look like what most people would expect from someone who believes superintelligence is imminent.

The fund’s first 13F filing with the Securities and Exchange Commission (SEC), a mandatory quarterly disclosure of U.S. equity holdings, covers positions as of 31 March 2026. It reveals a portfolio structured across two opposing poles: heavy put option exposure targeting the semiconductor complex on one side, and concentrated long positions in power generation, flash storage, and data-centre infrastructure on the other. Reading the positions together, this is not a straightforward bet against AI. It reads as a conviction call that value within the AI trade is rotating away from chip designers toward the physical layer that enables large-scale AI deployment.

If you currently hold Nvidia, AMD, Broadcom, TSMC, or any of the names that have defined the AI trade for the past two years, what follows is a concrete, position-level counter-thesis worth examining: what Aschenbrenner is shorting, what he is buying, why the logic is internally consistent, and what it means for how you think about your own exposure.

Leopold Aschenbrenner is 24 years old. He departed OpenAI in 2024, published a roughly 165-page essay titled Situational Awareness: The Decade Ahead arguing that AGI is likely by 2027-2030, and founded Situational Awareness LP in late 2024 to invest in AI infrastructure. Approximately 15 months later, the fund filed its first 13F.

The scale of this operation matters before you look at any individual position:

Any figure above $13.7 billion should be treated as a speculative estimate incorporating leverage or subsequent capital rounds, not confirmed regulatory data. What is confirmed is that a $13.7 billion fund run by a former OpenAI researcher with a published framework for AI’s trajectory has placed enormous, specific bets. This is not retail speculation dressed as institutional conviction. The positions that follow carry the weight of both scale and insider-level AI knowledge.

Start with the broadest expression. Situational Awareness LP holds approximately $2.0 billion in put options against the VanEck Semiconductor ETF (SMH), a position that captures the entire chip sector in a single trade. That alone is one of the largest disclosed bearish semiconductor positions in any recent 13F.

Then narrow the lens. Nvidia puts sit at approximately $1.5 billion in notional exposure. Oracle and Broadcom each carry roughly $1.0 billion in put notional. AMD follows at approximately $969 million. Micron at $584 million. TSMC at approximately $500-535 million. ASML at approximately $494 million. Intel at approximately $159 million.

| Position | Direction | Approximate Notional |

|---|---|---|

| SMH (VanEck Semiconductor ETF) | Put | ~$2.0B |

| NVDA (Nvidia) | Put | ~$1.5B |

| ORCL (Oracle) | Put | ~$1.0B |

| AVGO (Broadcom) | Put | ~$1.0B |

| AMD | Put | ~$969M |

| MU (Micron) | Put | ~$584M |

| TSM (Taiwan Semiconductor) | Put | ~$500-535M |

| ASML | Put | ~$494M |

| INTC (Intel) | Put | ~$159M |

| Total Semi/AI Put Notional | Put | ~$8.0-8.7B |

Total bearish notional across the semiconductor complex: approximately $8.0-8.7 billion.

The sequence matters. This is not a bet against one company’s execution. The positions span chip designers (Nvidia, AMD), foundries (TSMC), memory (Micron), lithography equipment (ASML), networking and custom silicon (Broadcom), and legacy CPU vendors (Intel). The entire supply chain is being targeted. These positions were newly scaled in Q1 2026, not legacy hedges carried forward from an earlier quarter.

One analytical caveat is worth flagging: large put positions can serve as directional shorts, tail hedges, or components of more complex option structures. The 13F does not provide full trade detail. What is clear is the direction and scale of conviction.

Aschenbrenner is not the only high-profile investor expressing bearish conviction on the semiconductor complex at scale; Michael Burry disclosed SOXX puts with a January 2027 expiration targeting a roughly 37% decline from May 2026 levels, a position that independently corroborates the view that chip valuations have moved well ahead of underlying earnings fundamentals.

If you are currently overweight Nvidia, AMD, or TSMC, the breadth of this short book should prompt a direct question: if a fund with deep AI knowledge believes the entire chip design and fabrication layer is richly valued, what would have to be true for that view to be wrong, and is that condition visible in your own thesis?

Before examining the long book, it is worth understanding the limits of the data source. A 13F filing is a quarterly SEC disclosure required of institutional investment managers with over $100 million in U.S. equity assets. It is filed within 45 days of each quarter’s end.

This filing was accepted by EDGAR on 15 May 2026 and covers positions as of 31 March 2026. That is roughly three months before this article’s publication in July 2026, meaning positions may have changed materially in the interim.

If you understand these limitations, you will extract the right kind of signal from the filing: directional conviction and thesis logic, not a precise recipe for replication.

13F filing divergences across Berkshire, Pershing Square, and Baupost on the same stocks in Q1 2026 illustrate the core interpretive challenge: the same regulatory snapshot can support opposite conclusions depending on which dimensions of the filing a reader prioritises, a structural limitation that applies equally to reading the Situational Awareness positions.

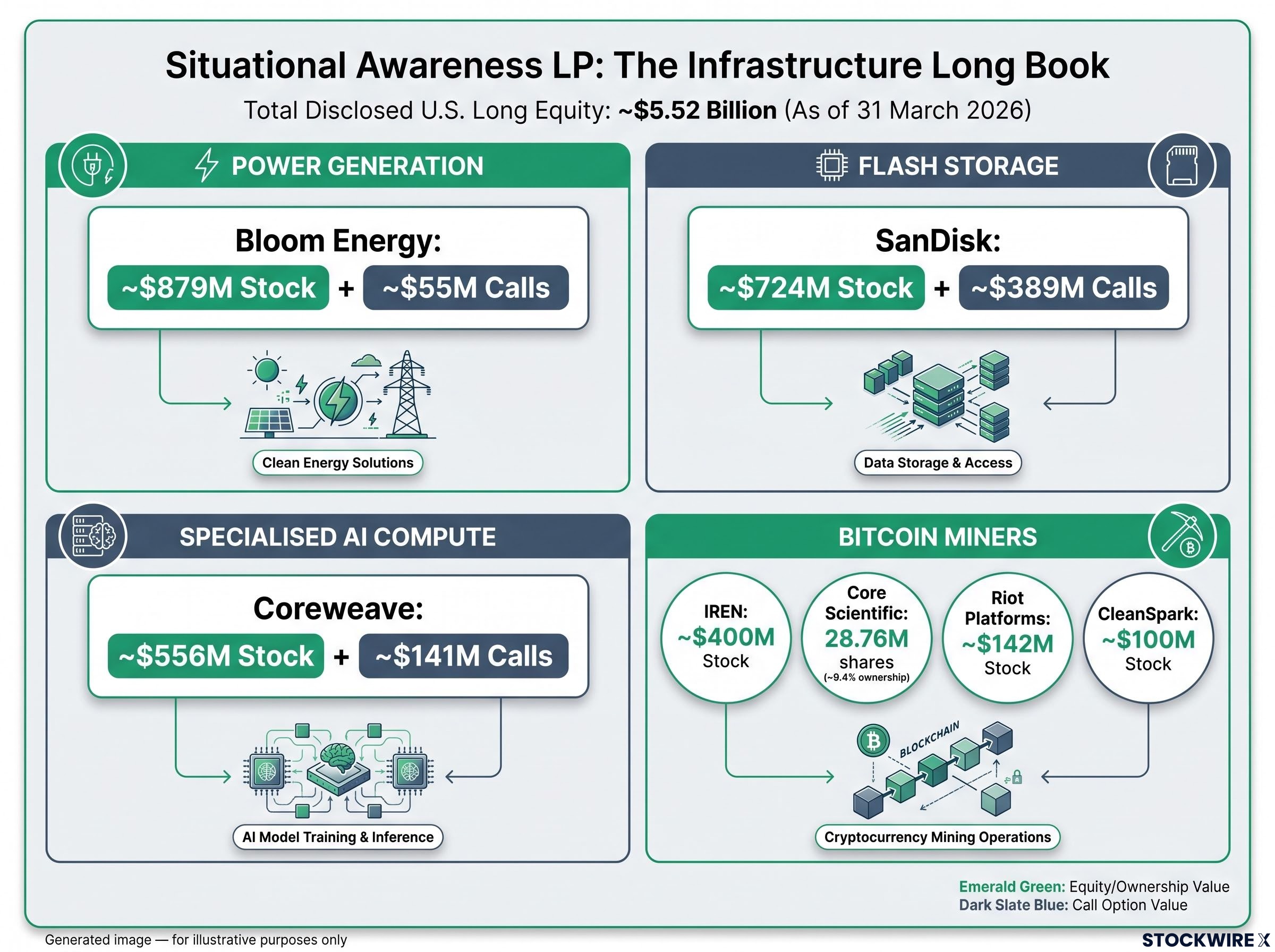

The other side of the portfolio tells you where Aschenbrenner believes value is migrating. The long book clusters into four categories: power generation, flash storage, specialised AI compute, and Bitcoin miners held as infrastructure assets.

Bloom Energy (BE) is the single largest disclosed long position: approximately $934 million combined in stock (~$879M) and calls (~$55M).

Bloom Energy manufactures solid-oxide fuel cells for on-site power generation, technology that can reduce data-centre dependence on strained electrical grids. This is the clearest power-access bet in the portfolio.

Power grid constraints have moved from a background risk to the primary operational bottleneck: data centres are projected to consume 9% of U.S. domestic electricity by 2030, up from 4% in 2023, a trajectory that makes on-site generation assets such as Bloom Energy’s solid-oxide fuel cells structurally attractive to operators who cannot wait years for grid interconnection approvals.

| Company | Ticker | Position Type | Approximate Value |

|---|---|---|---|

| Bloom Energy | BE | Stock + Calls | ~$879M + ~$55M |

| SanDisk | SNDK | Stock + Calls | ~$724M + ~$389M |

| Coreweave | CRWV | Stock + Calls | ~$556M + ~$141M |

| IREN (Iris Energy) | IREN | Stock | ~$400M |

| Core Scientific | CORZ | Stock (~9.4% ownership) | 28.76M shares |

| Riot Platforms | RIOT | Stock | ~$142M |

| CleanSpark | CLSK | Stock | ~$100M |

SanDisk is the flash storage play: approximately $724 million in stock plus $389 million in calls. The fund holds SanDisk calls alongside Micron puts, a pointed distinction. It is not blanket bearish on memory; it is selective, favouring flash-heavy storage over DRAM-focused exposures.

Coreweave carries approximately $556 million in stock plus $141 million in calls. Rather than holding chip intellectual property, the fund has taken a position in the company that actually deploys GPU capacity to AI customers, effectively owning the compute infrastructure layer rather than the underlying chip design.

The Bitcoin miner positions may seem counterintuitive in an AI portfolio, but the logic is specific. Core Scientific (approximately 9.4% ownership), IREN (~$400M), Riot Platforms (~$142M), and CleanSpark (~$100M) each operate large, power-dense facilities with established grid access. Rather than being valued solely as Bitcoin mining operations, those same physical sites can be redirected toward AI and high-performance compute workloads, making them a form of repurposable infrastructure with optionality across energy-intensive use cases.

If you have no current exposure to power generation, flash storage, or data-centre-adjacent infrastructure, this long book surfaces a specific set of names a well-informed institutional buyer has chosen to hold at scale. That is a starting point for your own research, not a buy list.

Step back from the individual positions and the portfolio resolves into a single coherent argument. Aschenbrenner is not betting against AI demand. His published work argues for rapid progress toward AGI by 2027-2030, implying sustained or accelerating need for compute. The portfolio, however, reflects a view that where value accrues within the AI build-out is changing, with the semiconductor complex no longer the primary site of scarcity or upside.

The thesis operates on four pillars:

Goldman Sachs Prime Brokerage data on hedge fund tech exposure adds quantitative weight to this pillar: aggregate institutional exposure to global IT equities reached an all-time high for the week ending 25 May 2026, with semiconductors and AI-linked software drawing the strongest inflows, meaning the contrarian case requires betting against a positioning trend that remains near its historical extreme.

This framing matters because it redefines what “being long AI” means. Whether purchasing chip IP still represents the strongest available expression of AI exposure is a genuinely open question if the point of scarcity has shifted toward physical deployment infrastructure. That is the question this portfolio places in front of you.

Two limitations deserve direct acknowledgement. First, the snapshot date is 31 March 2026, now roughly three months in the past as of July 2026. The portfolio could look materially different today. External research suggests that certain positions, including the Oracle puts, may remain open, but there is no comprehensive post-filing update available to confirm the current state of the book. Second, the 13F captures only a portion of the fund’s true risk exposure. Swap-based shorts, off-exchange derivatives, and structured positions are all omitted. What appears here is a partial view of a larger, more complex portfolio.

What the filing does establish is a high-information, high-conviction thesis: the AI infrastructure layer is underpriced relative to the chip design layer. That thesis is expressed at institutional scale by someone with deep, firsthand AI knowledge. It is not speculation passed around informally. It is the disclosed positioning of a $13.7 billion fund, recorded in a regulatory filing.

The structural view it embodies, that AI value is rotating from chip IP to physical infrastructure, will either prove out or fail over the 2026-2027 period. That gives you a concrete framework to test against incoming data.

Before the next earnings cycle for semiconductor names, bring these questions to your own portfolio:

You should not leave this analysis with a trade to copy. You should leave it asking a more precise question: within the AI build-out, are you positioned in the layer that is attracting institutional selling pressure, or in the layer that is attracting institutional buying?

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. The positions discussed are derived from a quarterly filing and may not reflect the fund’s current holdings.

—

Situational Awareness LP is a hedge fund founded in late 2024 by Leopold Aschenbrenner, a 24-year-old former OpenAI researcher who argues AGI will arrive by 2027-2030. The fund raised approximately $13.7 billion for its debut vehicle.

The fund holds put options across the entire semiconductor supply chain, including approximately $1.5 billion against Nvidia, $1.0 billion each against Oracle and Broadcom, $969 million against AMD, $584 million against Micron, $500-535 million against TSMC, $494 million against ASML, and $2.0 billion against the VanEck Semiconductor ETF (SMH).

The fund's largest long position is Bloom Energy at approximately $934 million, followed by SanDisk at roughly $1.1 billion combined in stock and calls, Coreweave at approximately $697 million, and Bitcoin miners including Core Scientific, IREN, Riot Platforms, and CleanSpark, held as repurposable power-dense infrastructure assets.

A 13F is a quarterly SEC disclosure showing long U.S. equity and listed options positions as of the quarter-end date, filed within 45 days. It does not capture swap-based shorts, off-exchange derivatives, or non-U.S. securities, meaning the Situational Awareness 13F shows only a partial view of the fund's true risk exposure.

Aschenbrenner's thesis is not a bet against AI demand but an infrastructure arbitrage: he argues the bottleneck has shifted from GPU supply to physical inputs such as electricity, land, and data-centre capacity, meaning chip valuations already embed the old narrative while power and storage assets remain underpriced relative to where AI value is now accruing.