When KKR, one of the world’s largest private equity firms, installed a retired four-star general as a full partner, it was not a symbolic appointment. General David H. Petraeus now serves as Partner, Chairman of the KKR Global Institute, and Chairman of KKR Middle East, with a mandate to map geopolitical risk directly onto investment decisions. That institutional choice is itself the signal: geopolitical analysis has moved from a periodic macro footnote to a permanent underwriting discipline.

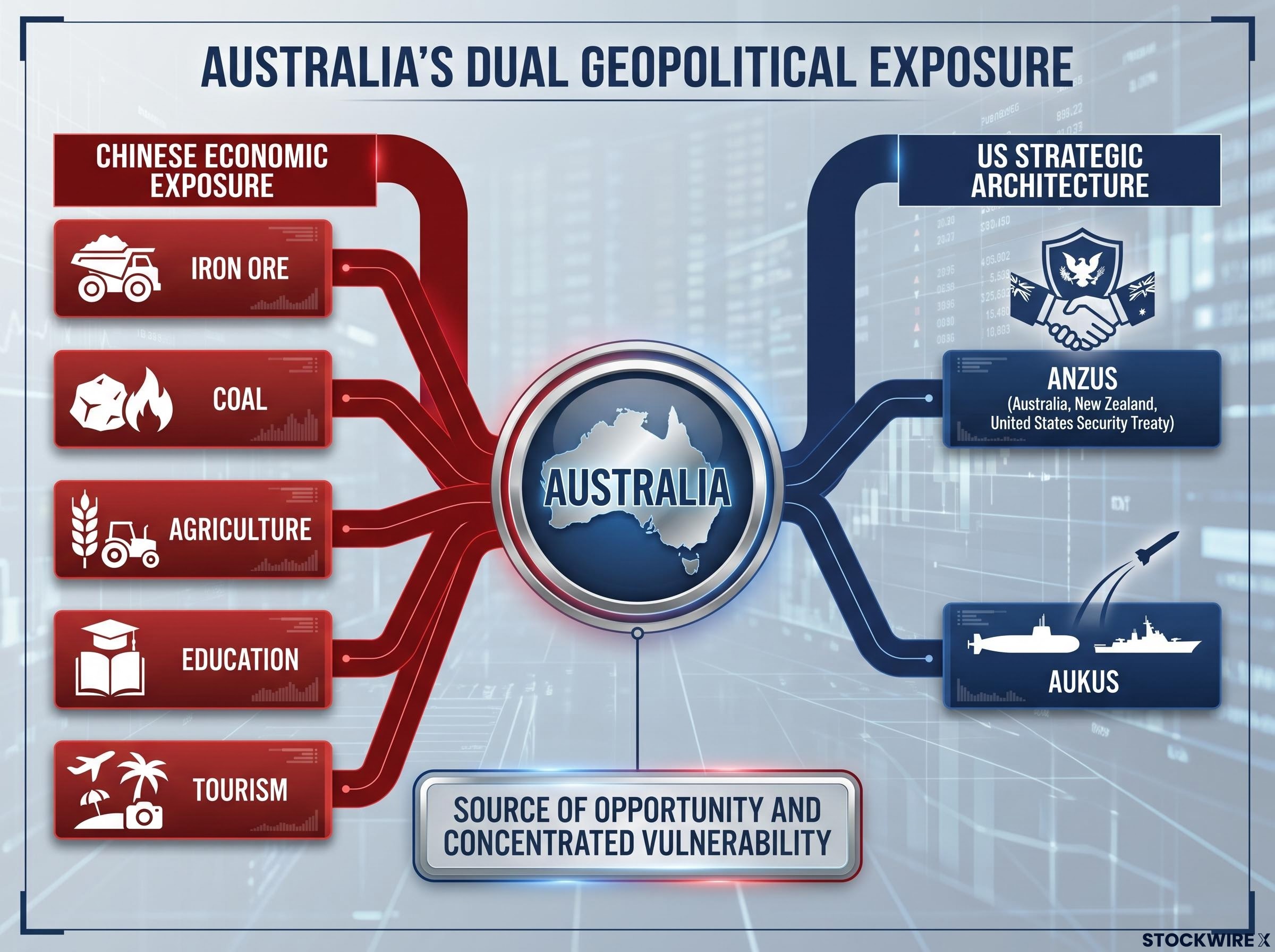

In a nabtrade interview with Tom Piotrowski published on 19 June 2026, Petraeus outlined a world where three fault lines, Ukraine-Russia, the Middle East, and the US-China relationship, are simultaneously active. For Australian investors, the implications are specific. Defence, energy, and critical minerals sit at the intersection of all three dynamics, and the combination of deep China economic exposure with firm US security alignment creates a form of geopolitical investment risk that few other markets carry with the same concentration. What follows is a map of how each fault line transmits into Australian portfolios, and a framework for acting on that analysis rather than treating it as background noise.

Why geopolitical risk has become a core part of the investment thesis, not a footnote

The KKR model is instructive precisely because of what it is not. Petraeus was not hired to write quarterly macro commentaries or to provide colour on earnings calls. He was embedded into the firm’s deal-level underwriting process, tasked with identifying how geopolitical conditions change the risk profile of specific assets and sectors.

That structural commitment reflects a broader shift. In a world where multiple geopolitical fault lines are active simultaneously, the range of possible outcomes for any given sector or country has widened materially. Sector and country selection carry more weight in 2026 than at any point in the past decade, because the tail risks are fatter and more correlated.

Sector and country selection carry more weight in 2026 than at any point in the past decade precisely because geoeconomic fragmentation is reshaping the return landscape across regional blocs, with five major economies committing hundreds of billions of dollars to competing industrial policies in semiconductors, batteries, and green technology.

“Geopolitical analysis is now part of the core investment thesis, not an afterthought.”

For Australian investors, this widening carries a particular edge. The Australian economy runs deep exposure to Chinese demand through iron ore, coal, agriculture, education, and tourism, while simultaneously locking into the US strategic architecture through ANZUS and AUKUS. That dual positioning is both a source of opportunity and a concentrated vulnerability. Investors who still treat geopolitical developments as context rather than thesis-level inputs are operating with an incomplete analytical framework.

When big ASX news breaks, our subscribers know first

The Middle East conflict, LNG security, and why Australia’s distance is a commercial asset

Middle Eastern instability transmits into global markets through a well-documented mechanism. Red Sea disruptions have periodically forced shipping to reroute around the Cape of Good Hope, adding material time and cost to global trade. Gulf energy producers operate in a region where security conditions can shift rapidly, and the combination of Iran’s posture, Houthi activity, and conflicts involving Israel has embedded a persistent geopolitical risk premium into oil and gas pricing.

The primary effect for global investors is higher volatility and a structural security premium rather than a clear directional call on energy prices. Higher-for-longer energy prices function as a drag on global growth and complicate central bank inflation management.

For Australia, however, the picture inverts.

As a major LNG exporter, Australia is directly tied into Asia’s search for secure, long-term gas supply. When Middle Eastern alternatives look less reliable, Asian buyers increase their valuation of contract-backed Australian LNG. This dynamic supports contracted producers and the terminal and pipeline infrastructure that connects them to market.

RBA analysis of Australian LNG contract structures confirms that the majority of Australia’s LNG exports to Japan, China, and South Korea are governed by long-term, oil-linked agreements, a contract architecture that insulates producers from spot-price volatility and reinforces the supply reliability premium Asian buyers assign to Australian cargoes.

| Attribute | Middle East energy exposure | Australian LNG positioning |

|---|---|---|

| Supply security | Subject to conflict disruption and chokepoint risk | Geographically distant from conflict zones; stable regulatory environment |

| Price volatility sensitivity | High; directly exposed to geopolitical risk premium | Moderate; long-term contracts buffer spot volatility |

| Contract structure | Mix of spot and contract; security concerns weigh on new commitments | Predominantly long-term, contract-backed supply agreements |

Australia’s geographic and political distance from the Middle Eastern conflict zone is itself a commercial asset, one that is quantifiable in the premium Asian buyers are willing to pay for supply reliability.

Gulf states’ ongoing military modernisation adds a further dimension. The Middle East is simultaneously a source of geopolitical risk and a significant downstream customer in the global defence supply chain, a dual character that investors should weigh when assessing sector exposures.

Ukraine and the permanent militarisation of defence investment

The investment case in Ukraine is not the war itself. It is what the war has done to defence procurement logic globally.

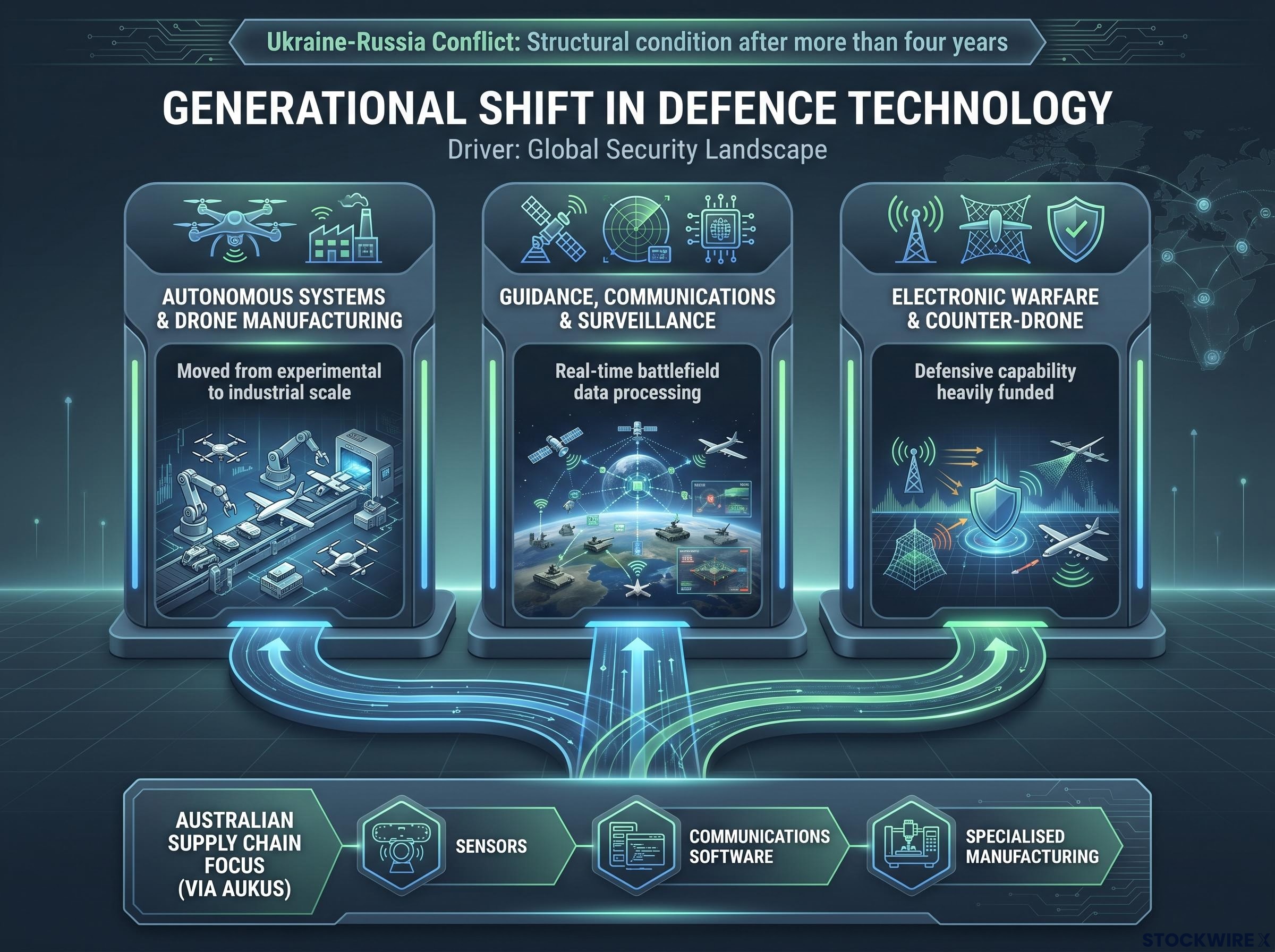

After more than four years of conflict with no near-term resolution in view, the Ukraine-Russia war has become a structural condition rather than a temporary shock. Frontlines move slowly, diplomatic solutions remain distant, and the market has repriced defence spending trajectories accordingly. The more consequential shift, however, is qualitative: the conflict has demonstrated that modern warfare is increasingly fought with technology-intensive systems rather than legacy platforms.

Ukraine’s extensive battlefield deployment of drones, unmanned vehicles, and electronic warfare has accelerated demand across three specific technology categories:

- Autonomous systems and drone manufacturing, where procurement volumes have moved from experimental to industrial scale

- Guidance, communications, and surveillance technologies, where real-time battlefield data processing has become a procurement priority

- Electronic warfare and counter-drone systems, where defensive capability is now as heavily funded as offensive platforms

This is not a temporary procurement spike. It represents a generational shift in how warfare is conducted and resourced, and the spending trajectory extends well beyond the immediate conflict.

What this means for Australian defence-exposed stocks

Australia’s connection to this spending shift runs through AUKUS, which channels allied defence procurement into Australian supply chains across sensors, communications software, and specialised manufacturing. The opportunity is real, but it is also precise. The growth sits in technology-intensive subsystems, not in the defence sector broadly. Investors concentrating in legacy platform manufacturers may find themselves in the wrong part of the defence complex.

Defence sector valuation has moved materially ahead of earnings reality, with ITA and XAR trading at forward P/E multiples roughly 10-20% above their own five-year averages and major names like Lockheed Martin at 25x versus 18x pre-2022 levels, a gap that management teams are not confirming through forward guidance.

Understanding how geopolitical fault lines transmit into markets

Before investors can act on geopolitical risk, they need to understand the mechanics by which distant conflicts become portfolio events. The US-China relationship offers the clearest current illustration of all three primary transmission channels operating simultaneously.

- Trade disruption: Tariffs, sanctions, and non-tariff barriers raise costs and uncertainty across global supply chains. For Australian exporters of iron ore, coal, and agricultural products, shifts in Chinese trade policy transmit quickly into corporate earnings and government revenues.

- Technology ecosystem fragmentation: Semiconductor controls, investment restrictions, and diverging technical standards are splitting technology ecosystems into partially separate Western and Chinese spheres. Australian companies with supply chains or customer bases spanning both ecosystems face increasing compliance complexity.

- Security-driven risk-off episodes: Tensions in the Taiwan Strait and South China Sea generate periodic bouts of risk aversion across global markets, hitting high-beta currencies and equity markets disproportionately.

Technology ecosystem fragmentation between the US and China has advanced well beyond export controls on individual chip categories; diverging technical standards, investment restrictions, and national-security law with bipartisan Congressional backing are creating structurally separate spheres that trade summit optimism cannot bridge, with Nvidia, TSMC, and ASML each carrying quantified revenue exposure to the divide.

These channels do not operate in isolation. A trade escalation can trigger a risk-off episode, which weakens the Australian dollar, which changes the return profile of every unhedged offshore holding in an Australian portfolio. Understanding these linkages converts vague geopolitical unease into a specific diagnostic the reader can trace through their own positions.

The Australian dollar as a geopolitical instrument

The AUD functions as a liquid proxy for China sentiment and global risk appetite, meaning it responds to US-China escalations with a speed and sensitivity that equity markets sometimes lag.

AUD weakness during geopolitical stress creates a dual effect. It cushions local-currency returns on unhedged offshore investments, making international equity holdings look stronger in Australian dollar terms. Simultaneously, it raises import costs and complicates the Reserve Bank of Australia’s inflation and rate decisions. Currency exposure in an Australian portfolio is therefore not a passive byproduct of asset allocation; it is itself a form of geopolitical expression.

Translating geopolitical analysis into portfolio decisions

The gap between understanding geopolitical risk and acting on it is where most investors lose the thread. Surface-level sector labels, “buy defence”, “buy energy”, “buy resources”, are insufficient in a geopolitically complex environment because meaningful distinctions exist within each sector.

| Sector | Sub-segment distinction | Geopolitical driver | Key risk |

|---|---|---|---|

| Defence | Legacy platforms vs. autonomous systems, cyber, and electronic warfare | Ukraine conflict accelerating technology-intensive procurement | Programme delays; budget reallocation between sub-segments |

| Energy | Contracted LNG (supply security premium) vs. spot-price sensitivity | Middle Eastern instability elevating Asian buyer demand for reliable supply | Contract renegotiation risk; transition policy shifts |

| Resources | Bulk commodities (Chinese construction demand) vs. critical minerals (allied reshoring) | US-China managed rivalry driving supply-chain diversification | Chinese demand slowdown; regulatory and permitting delays |

The practical methodology for integrating this analysis follows a sequence that mirrors the KKR underwriting approach:

- Map each major holding to a specific geopolitical fault line and identify which transmission channel (trade, technology, or security) is most relevant

- Stress-test revenue, cost, and financing assumptions under plausible conflict and policy scenarios

- Use that analysis to inform position sizing, diversification, and hedging choices rather than to generate qualitative commentary alone

- Price liquidity and optionality more highly; environments with elevated geopolitical risk favour liquid securities over illiquid positions, because sudden regime shifts can reprice assets rapidly

The investors best positioned to benefit from Australia’s structural advantages in LNG and critical minerals are those who also understand the policy and regulatory risks that are the mirror image of those same advantages.

Geopolitical risk is not going away, and that is precisely the investment opportunity

The simultaneous activation of multiple geopolitical stressors is not a temporary disruption to be waited out. It is the investment environment.

The US-China relationship has settled into a condition of managed rivalry, competitive but deeply entangled, that is likely to generate recurring episodes of market stress rather than resolve into a binary crisis or a stable equilibrium. Ukraine’s conflict has become a structural feature of global defence and commodity markets. Middle Eastern instability continues to shape energy pricing and shipping risk.

Australia enters this environment with genuine structural advantages. Its positions in LNG, critical minerals (lithium, nickel, cobalt, and rare earths), and its status as a trusted supplier with rule-of-law governance infrastructure are real and durable. These advantages are not self-executing, however. They require deliberate portfolio construction to capture, because the same geopolitical forces that create the opportunity can redirect it through policy shifts, regulatory changes, or alliance realignments.

The persistent complexity of the geopolitical environment is not a disruption to the investment thesis. It is the investment thesis, and it rewards the analytical work that most participants are unwilling to do.

The Petraeus-KKR model demonstrates that this analytical upgrade is already underway at the institutional level. The gap between investors who integrate geopolitical analysis into their underwriting and those who treat it as background noise will compound over time. For Australian investors sitting at the intersection of Chinese economic exposure and US strategic alignment, the case for closing that gap is as specific as it gets.

APRA’s geopolitical risk directive, issued on 17 June 2026 to every regulated bank, insurer, and superannuation fund overseeing $9.8 trillion in assets, confirms that the analytical upgrade Petraeus describes at the institutional investment level has a direct regulatory parallel in Australia, with preparedness now an enforceable supervisory obligation rather than voluntary guidance.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding geopolitical conditions and their market implications are speculative and subject to change based on evolving circumstances.