Why Broadcom and Nvidia Rose While Global Markets Fell

1 hr ago

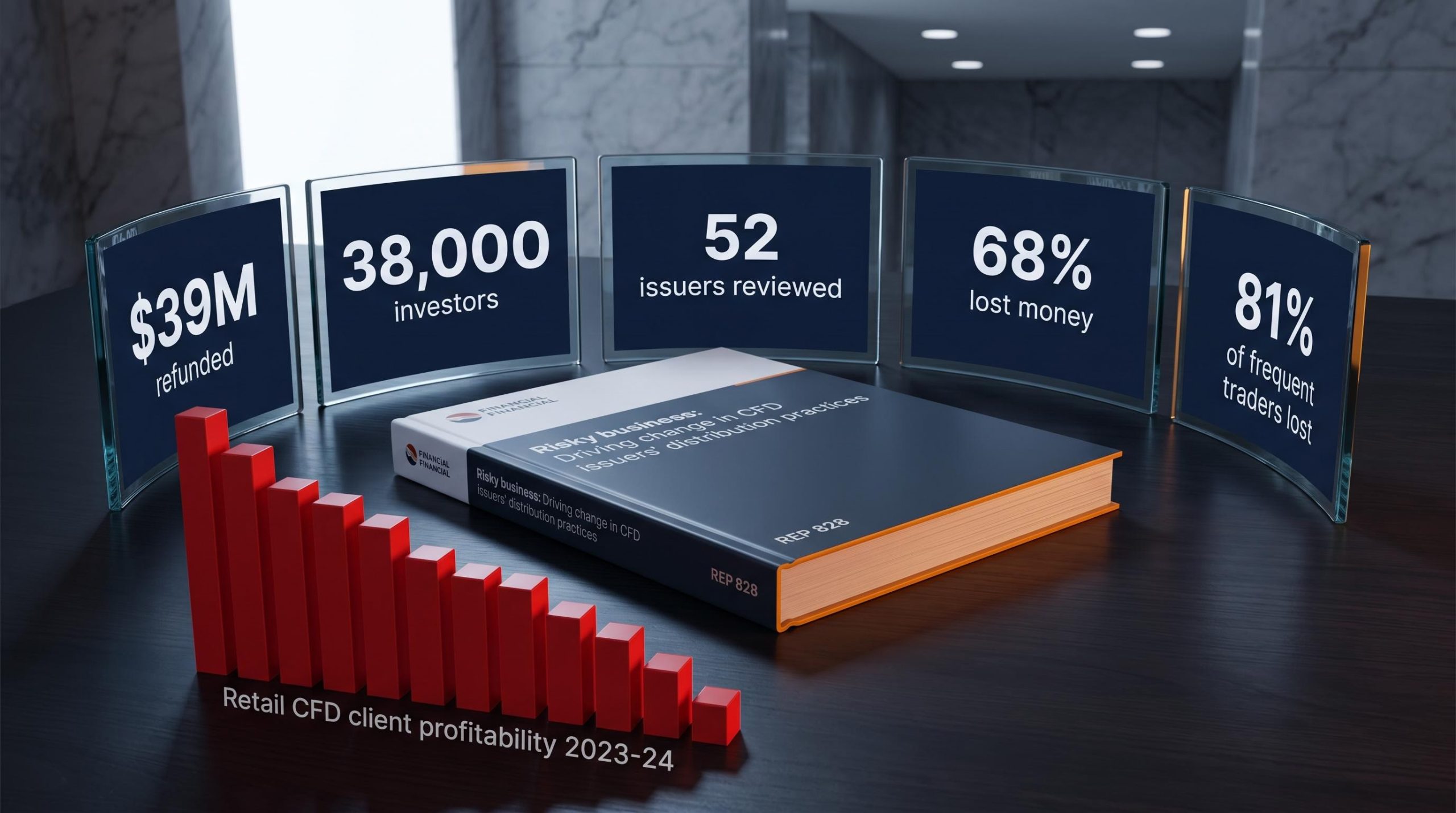

A refund pool exceeding $39 million was distributed across more than 38,000 retail investors as ASIC’s sector-wide review swept through all 52 licensed CFD issuers. That is not an enforcement action against a rogue operator. It is a whole-of-sector indictment, and ASIC delivered it in a single report.

ASIC released REP 828, titled Risky business: Driving change in CFD issuers’ distribution practices, on 20 January 2026 following a 14-month sector-wide review. The findings go beyond historical cleanup. They reveal that contract-for-difference (CFD) distribution in Australia was structurally failing retail clients at the product design, onboarding, and monitoring levels simultaneously, and that a consultation on the future of the Product Intervention Order (PIO) is already underway in 2026.

Here is what the review actually found, why the margin discount issue drove the majority of refunds, and what the new compliance standard means for anyone who trades, or is considering trading, leveraged products in Australia.

Between October 2024 and December 2025, ASIC assessed every one of Australia’s 52 licensed CFD issuers. This was not a targeted probe triggered by a whistleblower or a single firm’s collapse. It was a deliberate, whole-of-sector test of whether compliance with the Design and Distribution Obligations (DDO), the framework requiring issuers to define who a product is suitable for and distribute accordingly, and the PIO had actually taken hold since both came into force in 2021.

The answer was clear: almost every issuer required remediation in at least one area. The headline figure tells you the scale.

Across the review, refunds totalling over A$39 million were returned to more than 38,000 retail investors who had been affected by non-compliant practices.

The fact that remediation was required across virtually the entire sector tells you these were not outlier failures. Any retail investor who held CFDs during this period had material exposure to practices that ASIC has now confirmed were harmful.

CFDs are complex, leveraged, over-the-counter (OTC) derivatives. As instruments, they let retail clients take positions on the price movements of shares, currencies, and commodities without taking ownership of those assets. The leverage means a small move in the underlying price can produce a large percentage gain or loss on your position. Financing costs and fees can erode or eliminate profits even on trades that are directionally correct.

That structure alone creates elevated risk. The profitability data confirms it.

Financial leverage for Australian investors spans a range of instruments beyond CFDs, from margin lending on ASX equities to exchange-traded options and MINI Warrants, each carrying cost structures and stop-loss mechanisms that produce different loss profiles but share the same amplification dynamic that drove the sector-wide retail losses ASIC documented in REP 828.

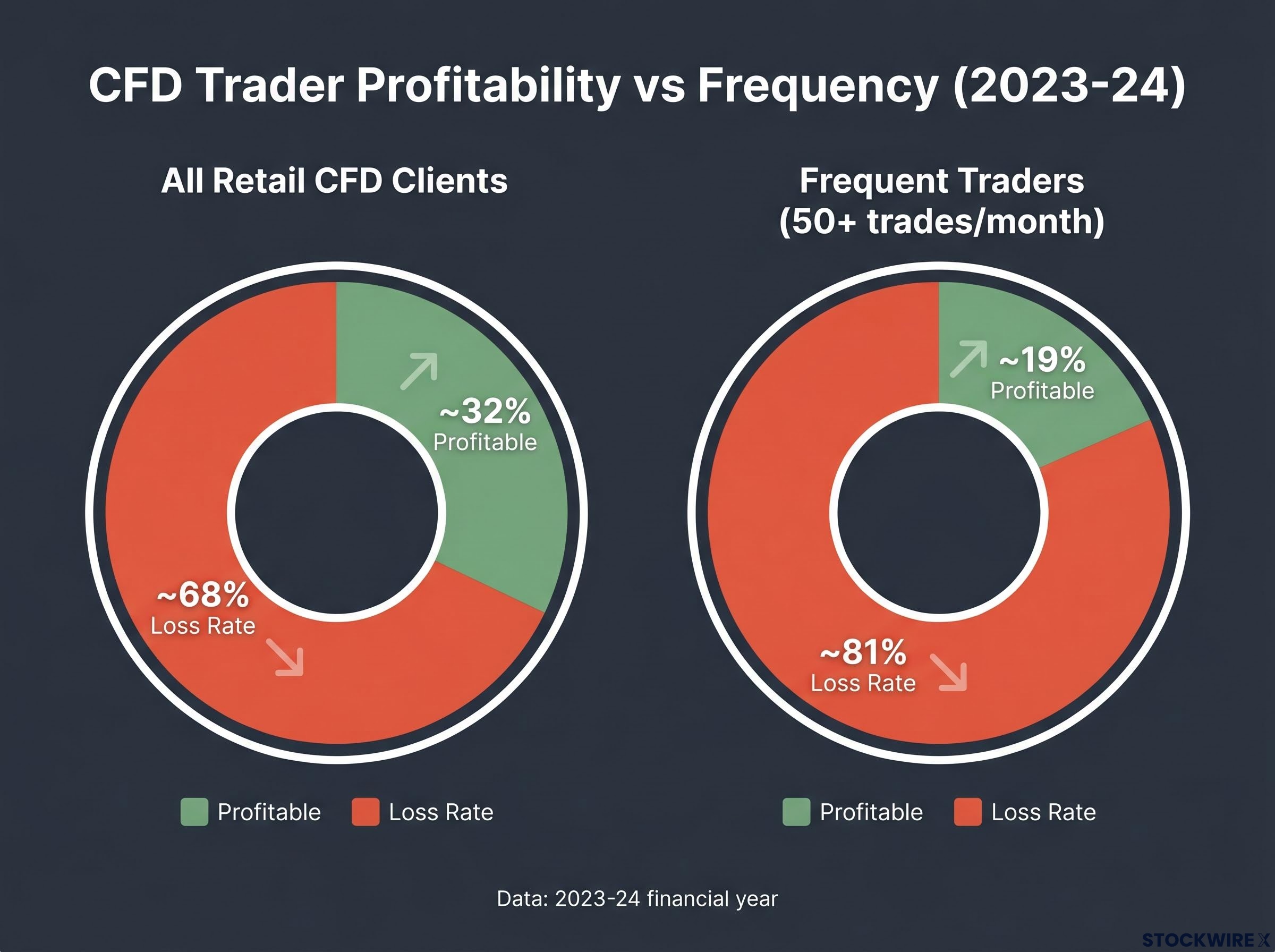

In the 2023-24 financial year, approximately 68% of retail CFD clients lost money, with aggregate net losses of approximately A$458 million, including A$73 million in fees. Only 32% of retail clients were profitable after fees.

The counterintuitive finding sits with the most active traders. Among frequent traders, those placing 50 or more trades per month, profitability fell to approximately 19%. Roughly four in five of the most engaged retail CFD traders were losing money.

| Investor Cohort | Profitable Clients (%) | Loss Rate (%) |

|---|---|---|

| All retail CFD clients (2023-24) | ~32% | ~68% |

| All retail clients after fees | ~32% | ~68% |

| Frequent traders (50+ trades/month) | ~19% | ~81% |

That frequency-profitability inversion matters. Increased engagement with CFDs does not improve outcomes the way it might with other investment products. It is precisely this dynamic that makes regulatory gatekeeping at the onboarding stage so consequential: if the product’s economics work against most participants regardless of activity, then who gets in the door is the variable regulators can actually influence.

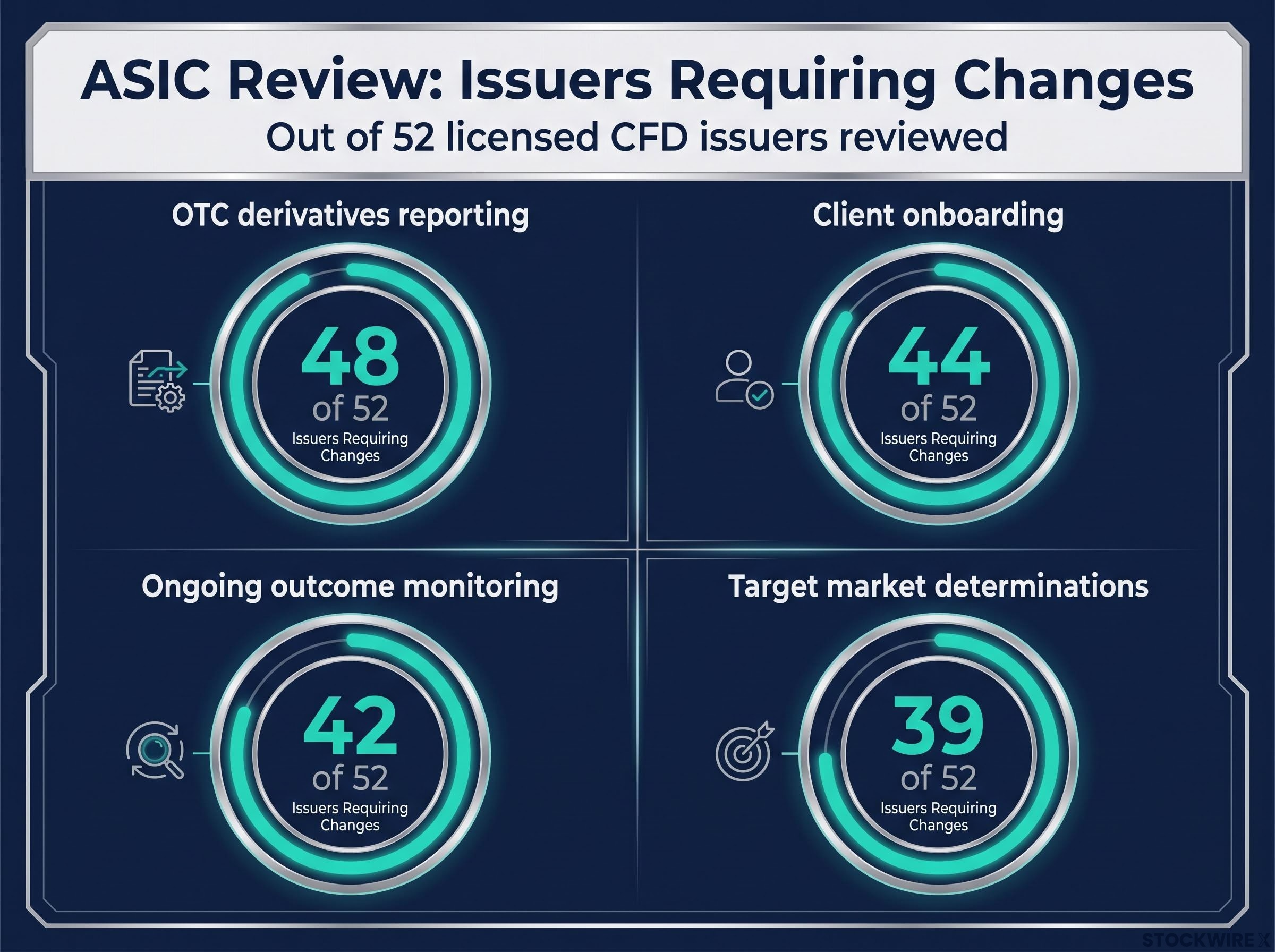

REP 828 identifies widespread weaknesses in four areas, and the failures reinforce each other. A too-broad target market makes onboarding screening weaker. Weak onboarding feeds a client base whose outcomes are never monitored. And corrupted transaction data means ASIC’s own surveillance cannot catch the patterns that would trigger intervention.

| Compliance Area | Core Deficiency Found | Issuers That Made Changes |

|---|---|---|

| Target market determinations | Markets defined too broadly; omitted criteria on financial objectives, circumstances, or trading experience | 39 of 52 |

| Client onboarding | Knowledge questionnaires did not reliably test understanding of leverage, margin calls, and loss scenarios | 44 of 52 |

| OTC derivatives reporting | Over 70 million erroneous reports, including missing fields and incorrect counterparty data | 48 of 52 |

| Ongoing outcome monitoring | Most issuers did little to no tracking of persistent loss patterns or consumer harm indicators | 42 of 52 |

DDO commenced in October 2021. Five years later, 39 issuers still needed to tighten their target market determinations. 44 had to improve their onboarding questionnaires. The gap between the regulation’s intent and its implementation was sector-wide.

Retail client misclassification, where issuers incorrectly designate retail investors as wholesale clients to remove DDO and PIO protections, represents a parallel enforcement track to the distribution failures REP 828 identified: the Federal Court’s $10 million penalty against Binance Australia Derivatives in March 2026 confirmed that classification errors carry the same enforcement weight as onboarding and target market failures.

The 70 million erroneous OTC derivatives reports are not an administrative footnote. ASIC uses this data as a frontline surveillance tool to detect risk concentrations and misconduct patterns across the sector. Corrupted data limits that capability directly.

Following the review, 48 issuers implemented changes to their reporting processes and systems. Reportable situations lodged by issuers rose 127% year-on-year. That increase signals something more durable than a process fix: it suggests the review shifted issuer willingness to surface problems, not just their systems for catching them.

The single practice that caused the most financial harm was also the most structurally revealing. Here is how it worked:

The result: a product feature marketed as a benefit was systematically extracting costs from clients who had no path to profitability on those positions. More than half the sector, over 26 of 52 issuers, contravened the PIO through this practice. ASIC classified it as a breach, not merely a poor practice.

28 issuers refunded over $36 million specifically related to margin discount practices, representing the majority of the total nearly $40 million refunded across the review.

The margin discount finding illustrates why ASIC moved to outcome-based supervision. A practice can involve no explicit deception, appear risk-reducing on its face, and still systematically disadvantage retail clients at scale. Disclosure alone would never surface this kind of structural harm. Outcome data did.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. CFDs and other leveraged derivatives are complex instruments that carry a high risk of rapid loss.

ASIC has signalled four post-review compliance expectations that collectively reset the operating environment for CFD distribution:

The PIO is due to expire on 23 May 2027. ASIC’s consultation on its future, planned for 2026, is ongoing as of mid-2026. Given the findings in REP 828, ASIC has left the door open to remaking or tightening conditions.

For you as a retail investor, the practical takeaway is that these improvements raise the floor on product design and distribution, but they do not alter the fundamental loss statistics. 68% of retail clients still lost money in 2023-24, and that number reflects the product’s structure, not just its distribution.

REP 828 explicitly frames its findings as relevant beyond CFDs. The regulatory logic ASIC demonstrated, DDO with genuine enforcement, outcome-based monitoring, and onboarding that functions as a real gatekeeper, applies to any complex, leveraged retail product.

The product categories facing analogous scrutiny include:

ASIC’s stated position in REP 828 is that products must be assessed on actual consumer outcomes, not compliance paperwork. Marketing scrutiny is increasing, particularly where product benefits are emphasised over risks, or where the underlying asset is promoted more prominently than the derivative itself.

The B-book dealing model, in which the issuer takes the opposite side of every retail trade and profits directly from client losses, represents the most extreme version of the structural misalignment REP 828 identified across the sector; the Federal Court’s record $300.2 million penalty against Union Standard International Group and its authorised representatives confirmed that a business model built on retail losses is not merely harmful practice but legally actionable misconduct.

The review’s scope, 52 issuers over 14 months, demonstrates ASIC’s capacity and willingness to run whole-of-sector assessments. For anyone invested in or distributing complex leveraged products beyond CFDs, outcome data (who is consistently losing, at what rate, and whether the issuer is responding) is now an enforceable compliance obligation, not an optional governance enhancement.

For investors exploring how DDO and wholesale client classification rules apply to leveraged crypto products, our full explainer on crypto derivatives regulation in Australia covers the Binance and Kraken enforcement outcomes and the 2026 Digital Assets Framework Act, showing how the same regulatory logic ASIC applied to CFDs is being extended across the broader derivatives sector.

The review produced concrete results. Refunds totalling close to $40 million reached more than 38,000 real people. Compliance standards across all four failure areas have been raised. The regulatory floor is measurably higher than it was before October 2024.

What changed:

What did not change:

The 2023-24 loss data was gathered during a period when the PIO was already in force. That tells you regulatory protections constrain how harmful distribution can be, but they cannot fundamentally alter the economics of a leveraged derivative product for most retail participants. The PIO consultation is ongoing in 2026, and ASIC has left the door open to tightening conditions further. Regulation is a backstop against harmful product features and distribution, not a guarantee against loss. The distinction matters.

Past performance does not guarantee future results. These statements are based on regulatory findings and historical data, and are subject to change based on market developments and regulatory outcomes.

ASIC's 14-month review of all 52 licensed CFD issuers found systemic failures across target market determinations, client onboarding, OTC derivatives reporting, and ongoing outcome monitoring, resulting in nearly $40 million in refunds to more than 38,000 retail investors.

The Product Intervention Order (PIO) is an ASIC regulatory instrument that sets mandatory conditions on how CFDs can be distributed to retail clients in Australia, including leverage limits and loss protection measures; it has been in force since 2021 and is currently under consultation ahead of its scheduled expiry on 23 May 2027.

In the 2023-24 financial year, approximately 68% of retail CFD clients in Australia lost money, with aggregate net losses of around A$458 million including A$73 million in fees; among the most active traders placing 50 or more trades per month, the loss rate rose to approximately 81%.

More than 26 of 52 issuers offered reduced margin requirements on hedged positions, a practice that appeared risk-reducing but systematically extracted funding costs from clients who had no path to profitability on those positions; 28 issuers refunded over $36 million specifically related to this practice.

The review raised the compliance floor across the sector, with tighter target market definitions, upgraded onboarding at 44 issuers, and new outcome monitoring frameworks, but the underlying loss statistics remain unchanged: regulation constrains harmful distribution practices but cannot alter the economics of leveraged derivatives for most retail participants.