$39 Million in CFD Refunds and 68% of Traders Still Losing

57 mins ago

While global equity indices posted losses exceeding 2% on 9 July 2026, two semiconductor stocks moved sharply higher on news that had nothing to do with the broader market and everything to do with their own specific situations.

That divergence is the signal worth examining.

The semiconductor sector is not behaving as a monolith. Company-specific catalysts are now driving meaningful performance gaps within the space, and the AI infrastructure spending cycle is creating structural conditions where those gaps can persist. For investors deciding how to position in chips, the question is no longer simply whether to own the sector, but how to own it.

This analysis breaks down what actually moved Broadcom and Nvidia on 9 July, what those catalysts mean structurally, and how to think about the concentrated versus diversified allocation decision in a sector where individual stories are increasingly running their own race.

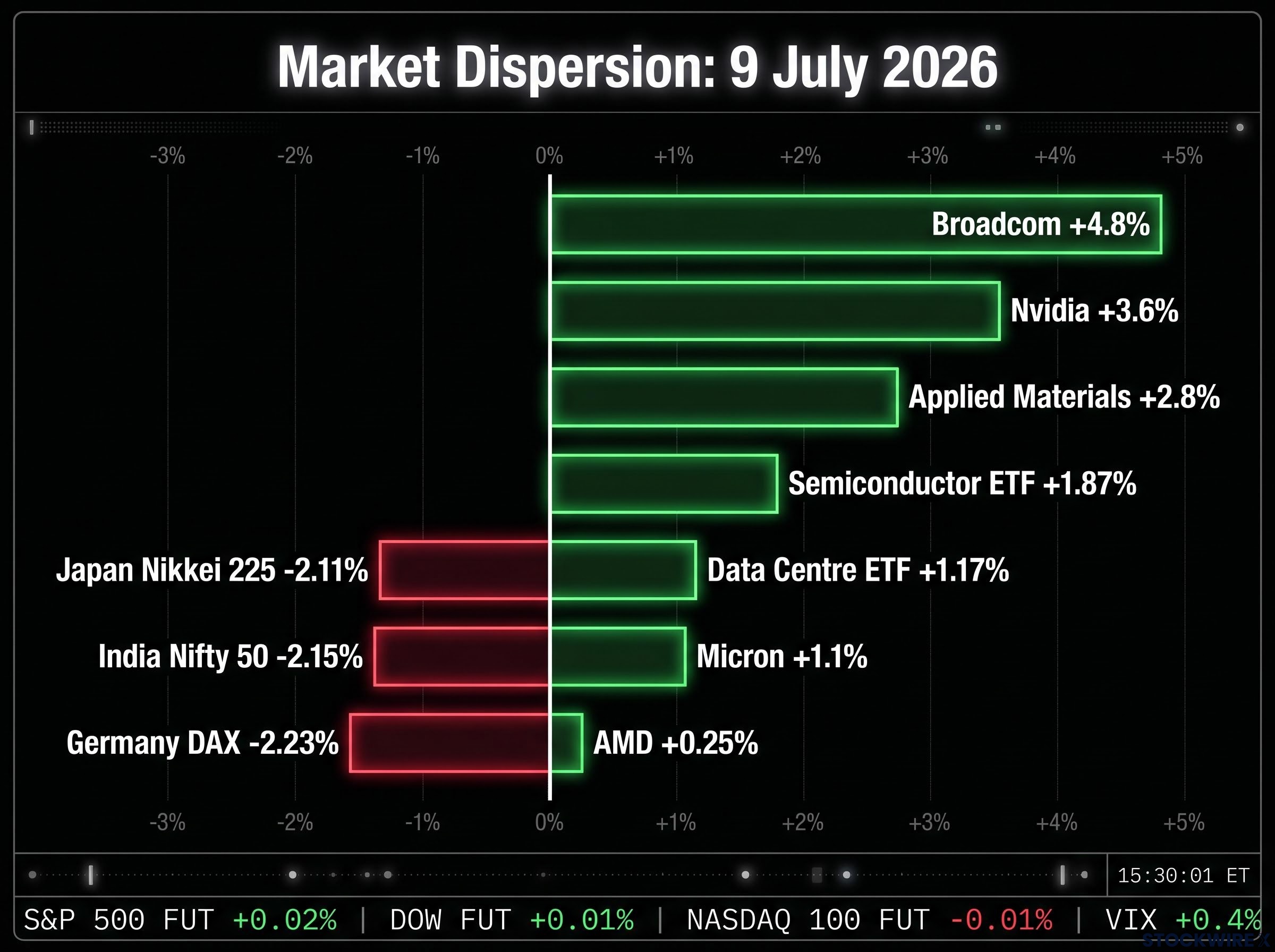

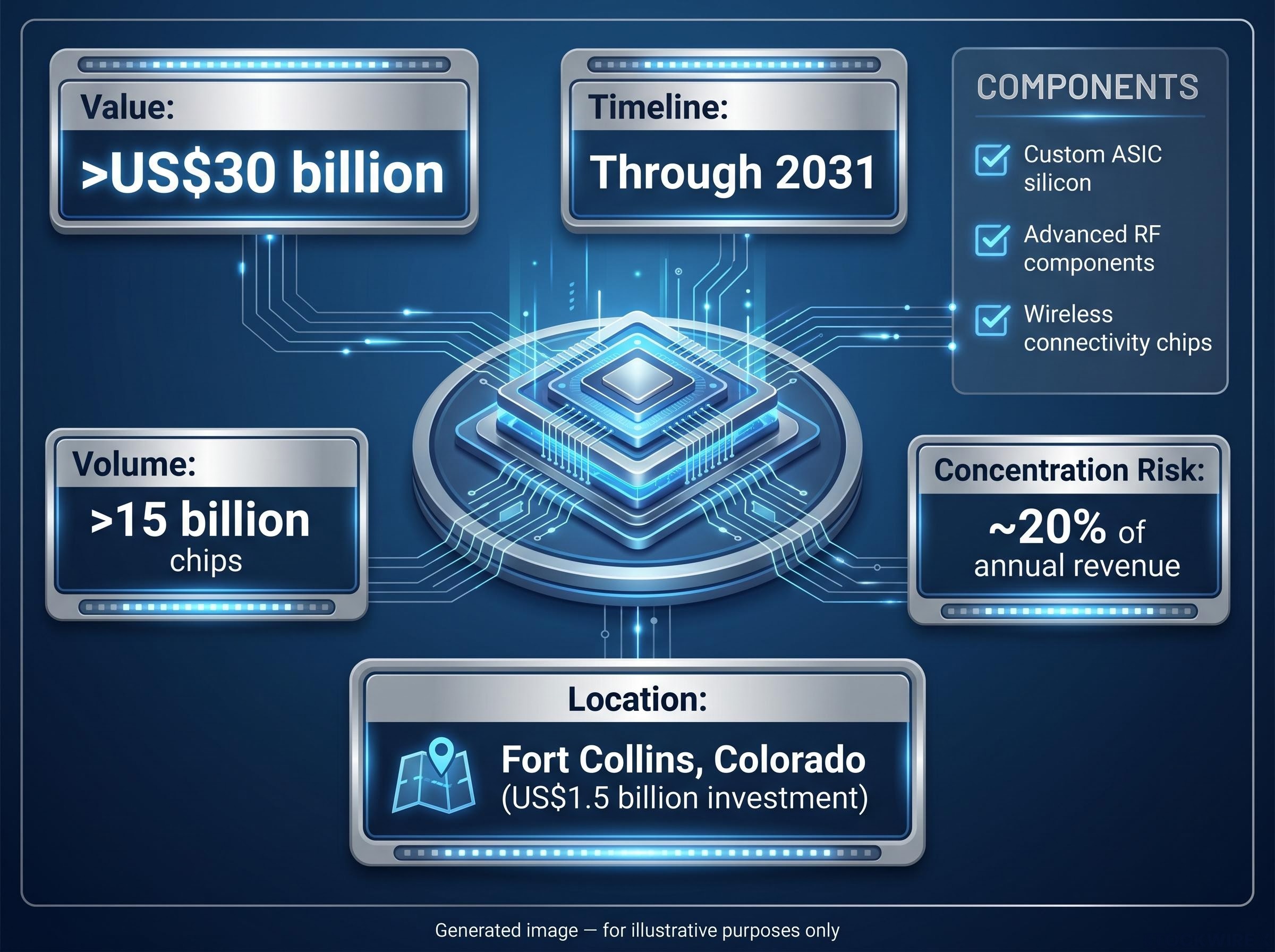

Broadcom rose 4.8% on the session. The catalyst was a new, expanded chip supply arrangement with Apple covering a commitment exceeding US$30 billion through 2031, with domestic production of more than 15 billion chips set out under the terms. This is a contractually defined commitment, not a forecast.

Apple deal value: exceeds US$30 billion through 2031, covering more than 15 billion chips manufactured domestically.

Nvidia gained 3.6%. The catalyst was renewed attention on the H200 AI accelerator’s potential in China, where approximately ten firms, including Alibaba, Tencent, ByteDance, Lenovo, and Foxconn, have received US government approval to purchase the chip. But here is the distinction that matters: as of mid-May 2026, no shipments had been confirmed. Beijing separately issued pause-order guidance in January 2026, instructing certain firms to hold off while domestic alternatives are prepared.

Both moves occurred while major international benchmarks were falling:

These gains were not market-lifted. They were catalyst-driven. And the contrast in catalyst quality, a signed multi-billion-dollar contract versus an unexecuted regulatory approval, tells you something important about the confidence interval attached to each stock’s move.

The headline number is large enough. But what the deal provides beyond revenue is where the valuation case sits.

The agreement runs through 2031 and encompasses custom ASIC silicon (application-specific integrated circuits, chips designed for a single customer’s exact requirements), advanced radio-frequency components, and wireless connectivity chips across multiple Apple product generations. Production is anchored at Broadcom’s Fort Collins, Colorado facility, which is receiving approximately US$1.5 billion in investment as part of the arrangement.

That Fort Collins anchor is not a geographic footnote. Under the CHIPS and Science Act, the US government is directing substantial capital incentives toward domestic semiconductor manufacturing. Companies with US-based fabrication are structurally advantaged in the current policy environment, and Apple has characterised this deal as part of a broader programme of hundreds of billions of dollars in domestic manufacturing commitment.

Apple’s strategy of using domestic chip manufacturing as a policy anchor extends beyond its Broadcom arrangement; its collaboration with Intel on 18A process node silicon for non-flagship devices, confirmed in June 2026, reflects a broader push to distribute US-based production across multiple foundry partners as CHIPS Act incentives reshape the economics of onshore fabrication.

For investors who have avoided chipmakers because of their boom-bust revenue patterns, a contract of this duration and scale compresses the cyclicality that makes semiconductor earnings unpredictable. It provides multi-year earnings visibility, which supports higher valuation multiples and reduces holding-period risk.

The contract components include:

| Bullish case | Risk case |

|---|---|

| Multi-year earnings visibility through 2031 | Valuation premium already priced into shares |

| US manufacturing alignment with CHIPS Act incentives | Apple represents ~20% of annual revenue |

| Implicit endorsement of Broadcom’s ASIC and RF capabilities | Contract renegotiation or expiry risk at 2031 |

Apple accounts for approximately 20% of Broadcom’s recent annual sales. A contract of this scale with a single customer is simultaneously a powerful earnings stabiliser and a genuine tail risk. If Apple were to shift suppliers, renegotiate terms materially at expiry, or reduce order volumes mid-contract, the revenue impact would be immediate and significant. This is not a theoretical concern. It is a 20% dependency that investors need to price consciously, not ignore because the headline number is attractive.

The factual sequence is straightforward. US approvals were granted to approximately ten Chinese firms, including several of the country’s largest technology companies. Nvidia’s H200 is its second-most-advanced AI accelerator, and Chinese demand for it is real.

Then the complications arrive. As of mid-May 2026, no shipments had been confirmed. Separately, in January 2026, Chinese authorities instructed certain local technology firms to pause H200 orders while preparing policies designed to mandate greater reliance on domestic AI accelerators.

US approvals and Beijing pause-order guidance are operating simultaneously, not sequentially. That two-sided policy dynamic is the environment investors are pricing.

The precise mechanism creating the gap between US approvals and actual H200 deliveries is a dual-approval deadlock: US Commerce clearance is necessary but not sufficient, because Beijing must independently issue its own approval before shipments can proceed, and as of late May 2026, that second approval had not been granted to any of the ten cleared Chinese firms.

This is not a simple bullish catalyst. It is not a simple bearish one either. US approvals signal that Washington sees value in allowing controlled chip access. Chinese demand interest confirms Nvidia’s technical desirability even under export controls. But Beijing’s own policy intervention creates friction that may prevent approvals from converting into shipments for months, or longer.

The 3.6% session gain priced in potential China demand. Investors are currently paying for a catalyst that has not cleared regulatory friction on either side of the Pacific, and that distinction should inform position sizing.

To convert this from a sentiment signal into a confirmed revenue catalyst, watch for:

Until Nvidia reports confirmed H200 shipments in its geographic revenue breakdown, the China catalyst should be treated as potential, not confirmed.

The semiconductor sector ETF (tracking the PHLX Semiconductor Sector Index) rose 1.87% to 562.03 on 9 July. The Data Centre and Digital Infrastructure ETF gained 1.17% to 28.59. Both advanced while broader international indices fell.

On a day when Broadcom returned 4.8%, owning the semiconductor ETF meant capturing less than half of that gain. That is the precise trade-off investors accept in exchange for reduced single-company risk.

Other semiconductor names on the session provided context for how the broader basket performed:

The ETF is not a consolation prize for investors unwilling to pick stocks. Over the medium term, semiconductor ETFs have recorded strong one-year and ten-year annualised returns through mid-2026, reflecting outsized contributions from AI accelerator and infrastructure companies. For investors who believe AI infrastructure spending is a multi-year cycle but lack conviction in any single company’s execution, the ETF provides a structurally sound entry point.

For investors concerned that a day like 9 July simply confirms an already-stretched sector, semiconductor valuation fundamentals tell a more nuanced story: Bank of America analysis from May 2026 identified record free cash flow yields, earnings revisions exceeding 20%, and active long-only overweight positions at roughly half the 2017 cycle peak, each pointing away from the speculative-bubble framing that dominates commentary.

| Vehicle | 9 July return | Primary catalyst | Primary risk |

|---|---|---|---|

| Broadcom | +4.8% | Apple supply contract (>US$30B through 2031) | Apple concentration (~20% of revenue) |

| Nvidia | +3.6% | China H200 demand and US approvals | Export-control and policy execution uncertainty |

| Semiconductor ETF | +1.87% | Broad AI infrastructure cycle exposure | Diluted upside on single-name catalysts |

The core allocation question is not whether semiconductors belong in a portfolio. It is whether your conviction is in the sector’s structural trajectory or in a specific company’s catalyst. The answer determines the vehicle.

The company-specific catalysts that moved Broadcom and Nvidia on 9 July did not emerge from nowhere. They sit on top of a structural foundation that explains both why they happened and why more like them are likely.

Three forces are driving this:

According to Reuters, the KOSPI fell into bear market territory on 9 July as chipmaker stocks experienced heightened volatility and capital rotated across Asia away from the semiconductor sector toward less expensive technology alternatives. The Hang Seng, by contrast, rose 2.99%.

The divergence between US AI-levered chip names and Korean memory and foundry suppliers on the same session is a live demonstration that the structural AI tailwind is not sector-wide. It rewards specific positions in the value chain. AI accelerators and custom silicon (the space Broadcom and Nvidia occupy) are capturing the spending. Memory and commodity foundry exposure, which semiconductor ETFs still embed, carries distinct cyclical and policy pressures. Investors need to know which position they actually own within any sector vehicle.

The 9 July session provided a proof point. Converting it into an investment thesis requires monitoring specific data points, not the general news flow.

In priority order:

US approval does not equal shipped revenue. That distinction matters for how investors should size any Nvidia position tied to the China thesis.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding shipments, contract implementation, and policy developments are subject to change based on market conditions and regulatory actions.

The numbers from a single session tell a clear story. Broadcom gained 4.8%. Nvidia gained 3.6%. The semiconductor ETF captured 1.87%. Major international indices lost more than 2%. The spread between the best single name and the sector vehicle was nearly three percentage points, on one day, driven by catalysts that had nothing to do with each other.

That dispersion is not noise. It is the structural condition of a sector where AI capital spending is concentrating returns in specific companies at specific points in the value chain. For investors with high conviction in a particular catalyst, whether that is Broadcom’s contractually locked revenue visibility or Nvidia’s eventual China volumes, concentrated positions capture the upside that diversified vehicles dilute. For investors who want the AI infrastructure tailwind without company-specific execution risk, the ETF remains sound, with the understanding that it captures roughly half the upside on the best days.

Both approaches carry risk. Broadcom carries a 20% customer concentration. Nvidia carries an unconfirmed China catalyst. The ETF carries exposure to memory and foundry names that are not benefiting from the same structural forces.

The question is not whether to own semiconductors. It is how to own them, and with what level of conviction in which specific story. 9 July made that question impossible to avoid.

Investors seeking a structured framework for acting on the allocation question the 9 July session raises will find our full explainer on navigating the semiconductor cycle, which maps the five-indicator timing framework for capturing peak-cycle gains without holding premium multiples into the 2027-2029 supply wave that TSMC and Samsung capital budgets have already locked in.

—

A semiconductor ETF tracks a basket of chipmakers across the value chain, including memory, foundry, and AI accelerator names, providing diversified exposure to the sector. Owning individual stocks lets investors target specific catalysts, as demonstrated on 9 July 2026 when Broadcom returned 4.8% while the semiconductor ETF captured only 1.87% of that move.

Broadcom rose 4.8% after confirming a new supply arrangement with Apple valued at more than US$30 billion through 2031, covering custom ASIC silicon, RF components, and wireless connectivity chips manufactured at its Fort Collins, Colorado facility.

Markets priced in the potential of approximately ten approved Chinese buyers, including Alibaba, Tencent, and ByteDance, accessing Nvidia's H200 accelerator, but the gain reflects sentiment rather than confirmed revenue because Beijing separately issued pause-order guidance in January 2026 and no shipments had been confirmed as of mid-May 2026.

Customer concentration risk refers to the revenue exposure a chipmaker carries to a single buyer; Broadcom's case is a clear example, with Apple accounting for approximately 20% of annual sales, meaning any shift in Apple's supplier strategy or order volumes would have an immediate and significant revenue impact.

The CHIPS Act directs substantial US government capital incentives toward domestic fabrication, structurally advantaging companies with US-based production; Broadcom's US$1.5 billion Fort Collins investment, underwritten by Apple's commitment, is a direct product of this policy environment and positions the company favourably for ongoing reshoring incentives.