Lululemon Plunges 12% on CEO Pick Amid Activist Investor Battle

2 hrs ago

For the past 24 months, Etsy faced a relentless contraction cycle that thoroughly tested the patience of its institutional and retail investors. That downward trajectory abruptly ended on 29 April 2026, when the digital marketplace reported a striking reversal of fortune before the opening bell.

The company’s first quarter 2026 financial results arrive against a backdrop of a slowly stabilising United States retail environment. These numbers also surface just weeks ahead of a major corporate restructuring that will permanently reshape the company’s operational footprint.

This breakdown of the latest Etsy earnings report analyses the top-line beat and the mechanics driving this renewed growth. It also examines what management’s upgraded transaction outlook means for the platform’s trajectory through the remainder of the year.

Wall Street analysts anticipated another sluggish quarter, but the core numbers delivered unexpected momentum. The company reported first-quarter revenue of $631.3 million, decisively beating consensus estimates of $617.1 million.

Earnings Per Share (EPS) reached $0.89, easily outpacing the projected $0.62. This top-line beat was driven by a 5.5% year-on-year increase in Gross Merchandise Sales (GMS), which hit $2.5 billion.

The specific segment breakdowns provided in Etsy’s official Form 8-K filing confirm that both domestic and international transaction volumes contributed to this renewed growth trajectory.

All reported metrics explicitly exclude the Depop subsidiary to provide a clear view of the core business. This return to growth contrasts sharply with the persistent contractions seen throughout late 2025, where consolidated GMS had previously dropped 14% from its 2021 peak.

| Metric | Q1 2026 Actual | Analyst Consensus |

|---|---|---|

| Revenue | $631.3 million | $617.1 million |

| Earnings Per Share (EPS) | $0.89 | $0.62 |

| Gross Merchandise Sales (GMS) | $2.5 billion | Contraction Expected |

The platform’s active buyer base hit 87.6 million, marking a critical transition from previous quarters. While this represents a slight 1% year-on-year decline, it reflects a positive sequential quarter-on-quarter growth that validates recent strategic user acquisition initiatives.

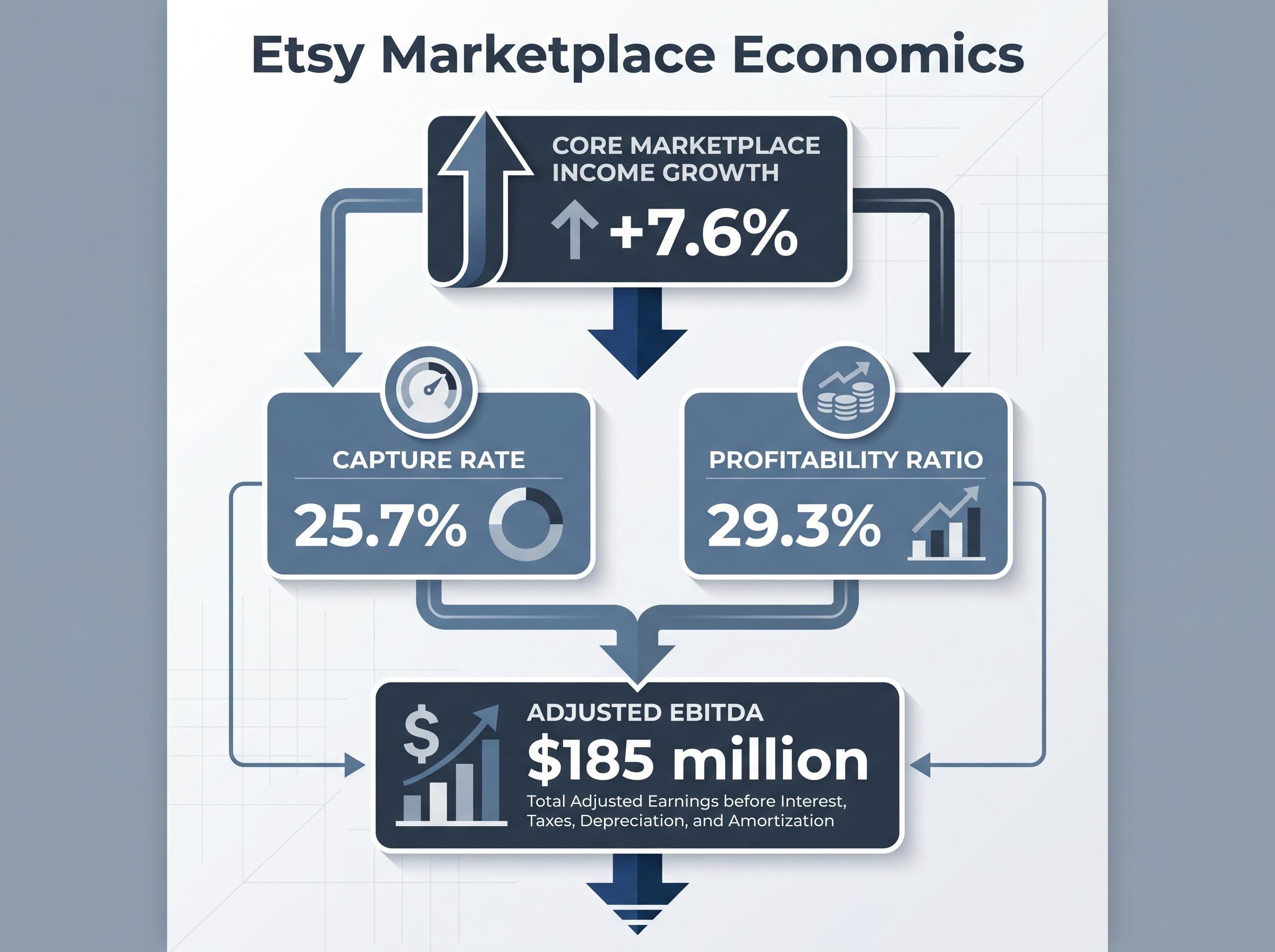

Merchant counts also increased, accompanied by a rise in the average spend per user across the ecosystem. According to company data, core marketplace income rose by 7.6%, signalling that existing buyers are transacting more frequently despite broader economic pressures.

For retail investors, this unvarnished data provides concrete evidence that turnaround efforts are gaining tangible traction.

Assessing digital marketplace health requires looking beyond raw user numbers to understand how platform activity translates into corporate revenue. Transaction volume acts as the true engine of profitability, which makes the mechanics of platform fees critical for investors to grasp.

According to company data, the platform’s anticipated capture rate sits near 25.7%, meaning the company retains just over a quarter of the value of every transaction processed on its servers. This dynamic conversion helped push the profitability ratio to 29.3%, generating $185 million in adjusted EBITDA for the quarter.

To contextualise this performance, baseline US e-commerce growth ran at 5.6% in the fourth quarter of 2025. The company’s current metrics suggest it is finally matching the broader domestic retail pace after trailing it for nearly two years.

The latest US Census Bureau retail data establishes this comparative baseline, demonstrating how the overall consumer transition to digital marketplaces has steadied following previous volatility.

To demystify these marketplace economics, investors should track three distinct metrics.

Gross Merchandise Sales (GMS): The total dollar value of all goods sold across the platform, representing overall ecosystem activity rather than direct corporate revenue. Core Marketplace Income: The actual corporate revenue generated from listing fees, transaction cuts, and integrated payments. * Capture Rate: The precise percentage of GMS that the company successfully converts into corporate revenue.

The operational growth recorded in the first quarter tells only half the story, as management prepares for a massive structural shift. All reported opening quarter metrics explicitly exclude Depop operations to ensure analytical clarity.

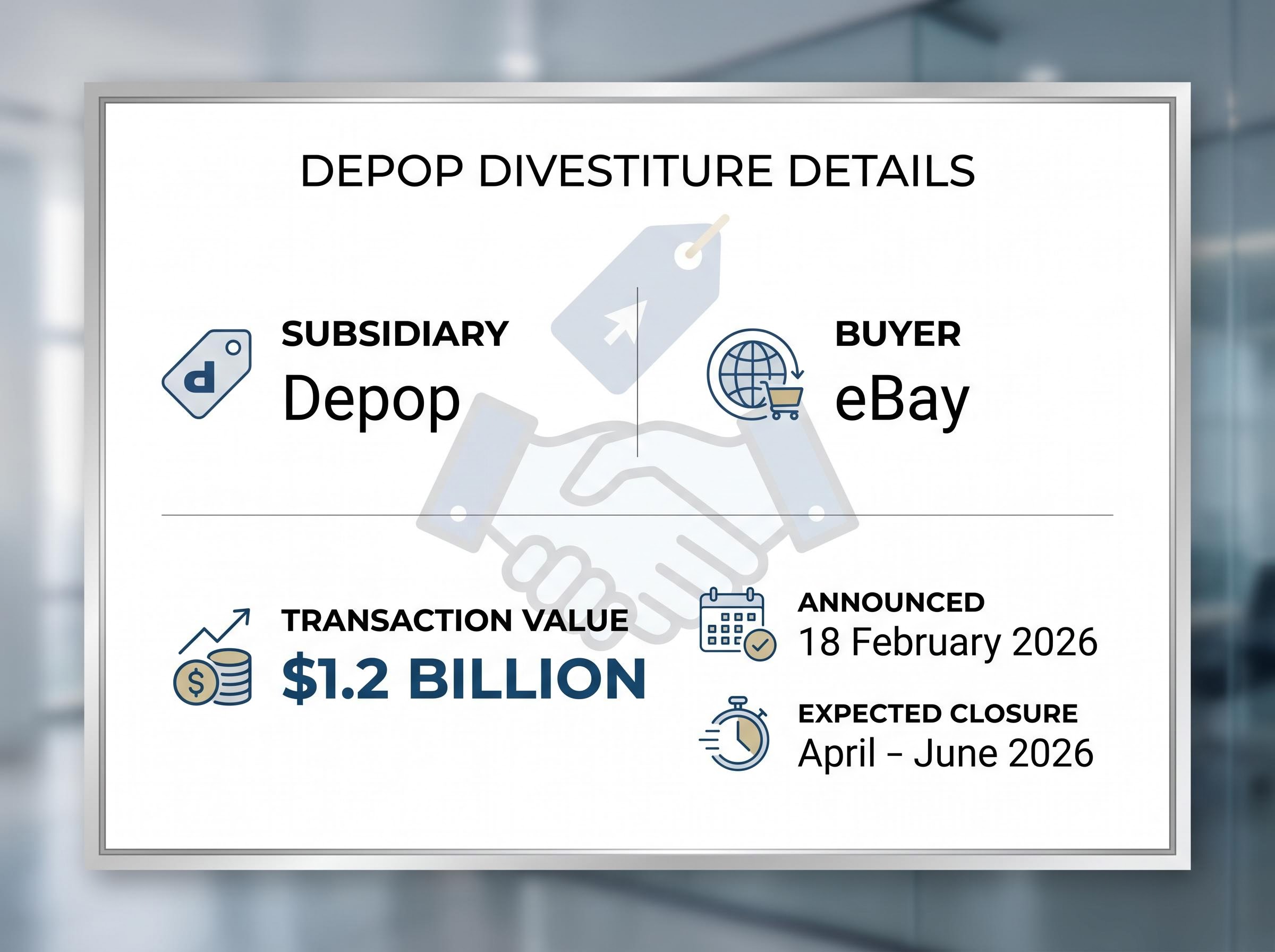

The company announced the sale of this fashion subsidiary to eBay for $1.2 billion on 18 February 2026. This transaction received unanimous board approval and is expected to close between April and June 2026.

The divestiture will strip away subsidiary distractions, allowing management to focus entirely on the primary marketplace. It also guarantees a massive capital influx that could fund future strategic acquisitions or shareholder returns.

Strategic Intent Commentary “Offloading the Depop subsidiary streamlines operational focus and equips the balance sheet with significant capital to reinvest directly into the core marketplace ecosystem.”

With a successful first quarter secured, the focus now shifts to the specific benchmarks Wall Street expects the company to hit next. Management has provided upward revisions for the coming months, projecting second-quarter 2026 GMS.

This target represents a 3% to 5% annual gain, a clear signal that the executive team believes the worst of the contraction is over. Quarterly adjusted profitability is expected to land, while full-year profitability estimates hold steady.

Ahead of the morning webcast, the stock closed at $62.16 on 28 April, and analyst rating updates will likely follow the management call. Investors monitoring the stock should watch the following sequence of catalysts over the coming months.

The resulting immediate equity valuation increase reflects growing institutional confidence that the executive team has successfully stabilized the platform’s core operational metrics after an extended period of contraction.

The first quarter successfully halted a prolonged contraction, proving that the primary platform can still generate organic growth. However, the true test for management will be maintaining this low single-digit expansion through the remainder of 2026 without the Depop subsidiary padding the numbers.

The company’s ability to boost merchant counts and increase average buyer spend highlights the underlying resilience of the US digital consumer. If these capture rates remain stable, the platform is well-positioned to capitalise on any further stabilisation in the broader domestic retail sector.

For investors analyzing the macroeconomic headwinds facing the broader e-commerce sector, our detailed coverage of US recession risk explores how rapid household savings depletion and plunging sentiment metrics threaten to disrupt domestic retail expenditure patterns.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Etsy's Q1 2026 turnaround was driven by a 5.5% year-on-year increase in Gross Merchandise Sales, exceeding revenue and EPS estimates due to improved transaction volumes. The company also saw increased merchant counts and average spend per user across its core marketplace.

The Depop divestiture for $1.2 billion will streamline Etsy's operational focus on its core marketplace and provide significant capital for future strategic initiatives or shareholder returns. This move aims to remove subsidiary distractions and enhance efficiency.

Etsy's management projects Q2 2026 Gross Merchandise Sales to achieve a 3% to 5% annual gain, targeting $2.48 billion to $2.53 billion. The company also expects to maintain full-year profitability estimates, with sustained 28% to 30% margins.

For an e-commerce platform, the capture rate is the percentage of the total Gross Merchandise Sales that the company successfully converts into its own corporate revenue. Etsy's anticipated capture rate sits near 25.7%, indicating how much value it retains from transactions.