Citi’s decision to begin modelling Google’s custom AI chip sales as a separate revenue category within its cloud forecasts represents a notable analytical development. That single modelling decision, buried in a proprietary research note dated 16 July 2026, says something significant about how far AI commercialisation has actually travelled.

The timing is deliberate. These revised estimates land weeks before Alphabet and Amazon report Q2 2026 results, making Citi’s projections live market intelligence rather than long-range speculation. And the methodology behind the numbers matters as much as the numbers themselves: the bank has moved from treating AI infrastructure as a sunk cost absorbed into cloud operations to recognising it as a distinct commercial activity with attributable, forecastable revenue.

Here is what the data actually projects, why the analytical method behind those projections carries its own signal, and what the trajectory of AI cloud revenue tells you about where the AI spending cycle stands right now. Think of this as a lens for reading the next round of hyperscaler earnings, not a data dump.

Citi’s GCP estimates and what $190 billion implies about Google’s cloud ambition

Citi’s revised Google Cloud Platform (GCP) estimates, the cloud computing services Alphabet sells to businesses, are not incremental adjustments. They represent a fundamental re-sizing of the opportunity Citi believes AI is creating inside Google’s cloud business.

The headline numbers, drawn from Citi’s proprietary research note:

- Q2 2026 GCP year-over-year growth estimate: 68.5%

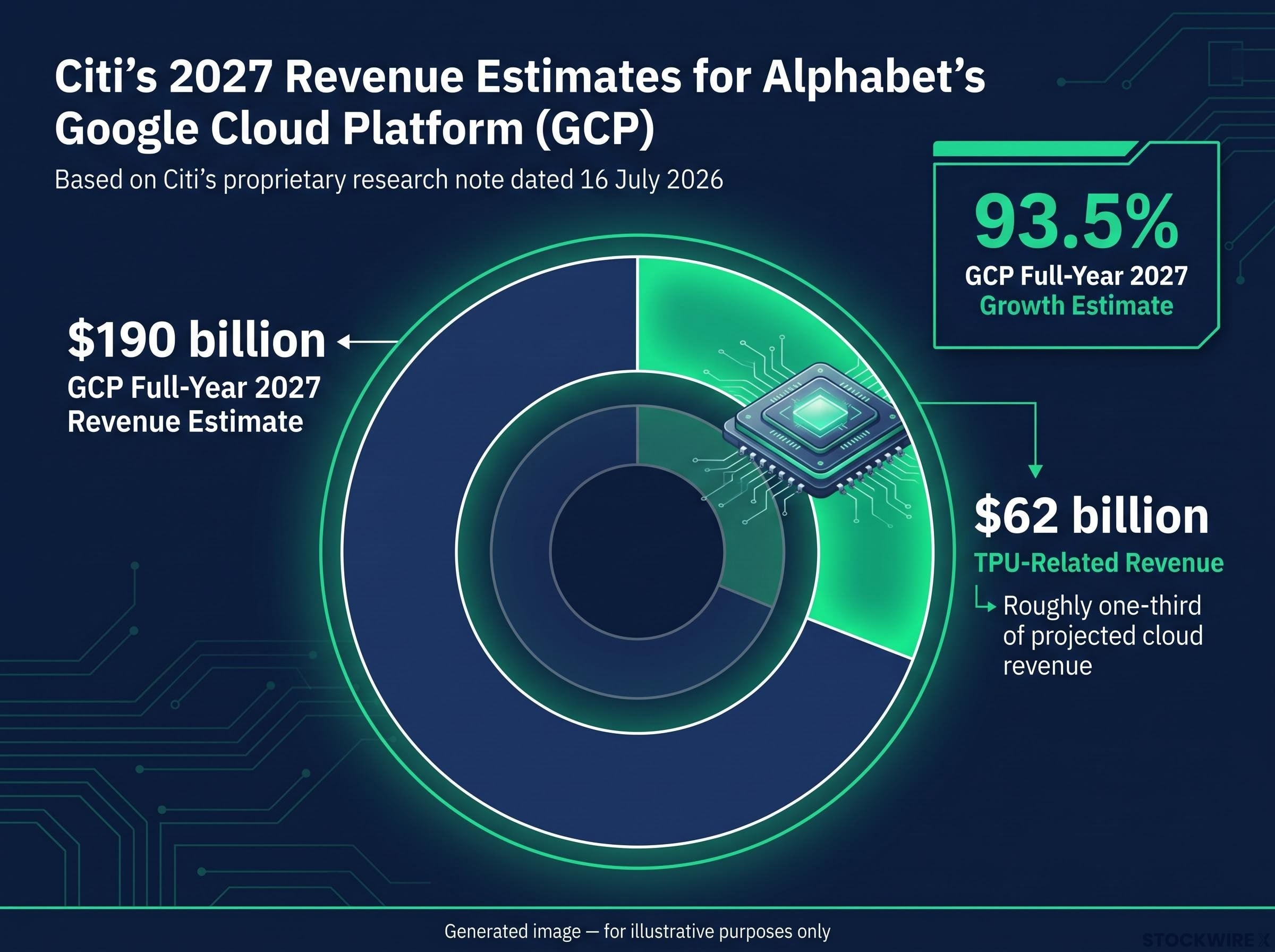

- Full-year 2027 GCP growth estimate: 93.5%

- Full-year 2027 GCP revenue estimate: $190 billion

These are pre-earnings projections. As of 16 July 2026, Q2 2026 results had not yet been reported, meaning Citi issued these figures as forward estimates, not post-result commentary.

The scale of the upward revision is the story within the story. A 93.5% annual growth rate approaching $190 billion in revenue means Citi is not modelling GCP as a mature cloud business defending market share. It is modelling a platform in mid-acceleration. That growth rate presupposes an AI adoption trajectory where enterprise demand is not just growing but compounding at a pace that few cloud businesses have sustained at anything close to this revenue base. For investors trying to size the AI revenue opportunity at Alphabet ahead of Q2 reporting, these estimates represent the most precise publicly available analyst benchmark, and their magnitude signals that prior models were materially underestimating AI-driven demand.

Alphabet’s cloud backlog exceeded $460 billion in Q1 2026, a forward revenue pipeline that gives structural context to Citi’s 2027 growth estimates and helps explain why the 93.5% GCP growth projection is anchored in contracted demand rather than speculative extrapolation.

When big ASX news breaks, our subscribers know first

The TPU revenue line that changes how analysts read Alphabet’s AI business

The number that matters most in Citi’s revised model is not the $190 billion total. It is the $62 billion in TPU-related revenue embedded inside it.

TPUs, or Tensor Processing Units, are Alphabet’s custom-designed AI chips, purpose-built for machine learning workloads. Historically, analyst models folded Google’s TPU operations into broader infrastructure costs rather than attributing them any commercial revenue value. Citi’s updated approach breaks that convention, separating TPU sales into a distinct revenue line and quantifying them explicitly for the first time.

The commercial logic behind custom AI chips, lower per-inference costs, improved energy efficiency, and reduced dependence on a single external supplier, explains why Alphabet invested years in TPU development before those chips generated any externally recognised revenue line.

Citi’s revised modelling approach treats Alphabet’s TPU operations as a standalone external revenue stream rather than a cost absorbed by the broader cloud business, a judgement that AI chip sales have reached sufficient commercial scale to justify dedicated attribution in analyst frameworks.

That $62 billion figure represents roughly one-third of Citi’s total $190 billion GCP revenue estimate for 2027. One-third of projected cloud revenue, in other words, now comes from selling AI chip capacity rather than traditional cloud computing services.

The practical implication for how Alphabet is valued is significant. If TPU revenue becomes a tracked line item in standard analyst models, AI chip sales, not just AI-driven cloud consumption, become a material factor in how the company’s financials are interpreted. The analytical frame shifts from “Google has an AI strategy” to “Google has an AI revenue stream” with specific, trackable metrics. That distinction changes the conversation at earnings time.

What AWS’s growth path to 40% tells investors about AI compute demand

Amazon Web Services tells a different growth story from GCP, but the structural signal is similar: AI compute demand is accelerating, not plateauing.

Citi’s AWS estimates follow a clear trajectory of building momentum:

| Period | Citi Growth Estimate | Driver Note |

|---|---|---|

| Q2 2026 | 32.5% YoY | Growing AI adoption across enterprise customers |

| Full-year 2026 | 33.5% | Sustained demand as AI workloads scale |

| Full-year 2027 | 40% | Expanded compute capacity coming online |

The acceleration from 33.5% to 40% matters more than it might appear at first glance. AWS already operates at a scale where each percentage point of growth represents billions in incremental revenue. Citi points to two specific drivers behind the projected step-up: rising AI adoption across the customer base and new compute capacity coming online, with the implication that the additional infrastructure Amazon has been building is finding immediate demand rather than lying unused.

What that tells you about the demand picture is instructive. An acceleration at this scale implies AWS is working through a meaningful demand backlog, one where customers wanted AI compute capacity that was not yet available. As capacity expands, the revenue follows. For investors with Amazon exposure, Citi’s 40% estimate for 2027 positions AWS as an AI infrastructure business in an expansion phase, not approaching a ceiling, and that distinction has direct implications for how the segment’s earnings contribution should be modelled.

From cost centre to revenue line: the structural shift in how AI is being modelled

Citi’s decision to break out TPU revenue inside GCP did not happen in isolation. It reflects a broader shift in how sell-side analysts are treating AI across the entire cloud sector, a shift already well advanced in coverage of other major platforms.

The evolution follows three observable stages:

- AI as internal capex. Infrastructure spending on AI chips, data centres, and model training treated purely as a cost. No revenue attribution in analyst models.

- AI as tracked revenue category in emerging cloud coverage. Analysts begin modelling AI-specific revenue lines in coverage of platforms where the data is available, particularly in international cloud markets.

- AI as primary growth driver with standalone line items in major hyperscaler models. The Citi GCP treatment, where TPU revenue is separated and quantified, represents this stage for US hyperscaler coverage.

The most concrete evidence for this transition comes from Alibaba Cloud coverage, where the shift is already well-documented.

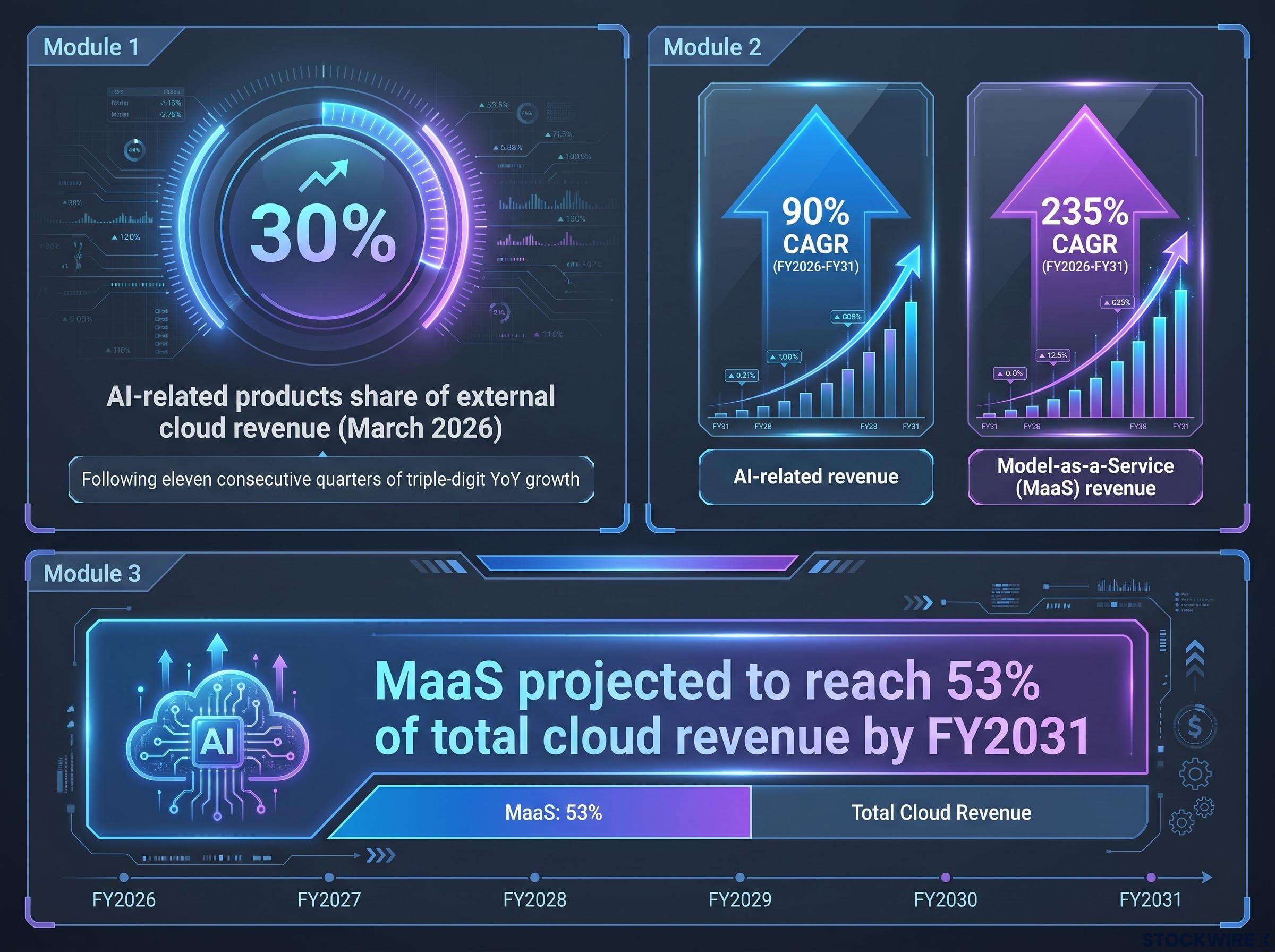

Alibaba Cloud’s AI-related products delivered triple-digit year-over-year growth for eleven consecutive quarters through March 2026, reaching 30% of external cloud revenue.

Citi’s own projections for Alibaba Cloud illustrate the endpoint of this trajectory: AI-related revenue growing at a 90% compound annual growth rate (CAGR, the average annual growth rate over a multi-year period) from FY2026 to FY2031, with Model-as-a-Service (MaaS) revenue, where customers pay for access to AI models via API calls rather than building their own, projected at a 235% CAGR over the same period, reaching 53% of total cloud revenue by FY2031.

These are not just corroborating data points. They show that AI-native revenue lines at scale are already being modelled and tracked with precision in major analyst coverage. Citi’s GCP methodology is catching up to established practice, not pioneering it in isolation. For investors, the takeaway is practical: platforms that can demonstrate AI revenue as a distinct, growing line item will be valued differently from those where AI remains purely a cost story. Knowing which stage each platform occupies in this transition helps you anticipate which metrics will carry analytical weight in future earnings cycles.

The next major ASX story will hit our subscribers first

Near-term earnings setup: why Citi expects all three hyperscalers to beat consensus

The structural story is one thing. The near-term trading setup is another, and Citi’s view on both is bullish.

For Q2 2026 results, Citi’s position is that Alphabet, Amazon, and Microsoft will each come in ahead of both revenue and earnings consensus. That call is grounded in primary market intelligence rather than extrapolation from prior quarters.

The evidence base Citi draws on spans three distinct inputs:

- Attendance and conversations at the Cannes advertising festival in June 2026, which gave Citi direct visibility into current spending intentions among major advertising buyers

- A dedicated call with an advertising sector specialist, adding qualitative depth on where demand trends are heading

- An overall digital advertising environment that Citi judges to have strengthened considerably relative to earlier in 2026, pointing to a more supportive macro backdrop heading into summer

Channel checks from industry gatherings are a standard and well-regarded pre-earnings methodology in sell-side research. Citi is not guessing; it is reporting what its on-the-ground contacts are telling it about spending conditions.

Q3 guidance as a secondary signal

Beyond Q2 results, Citi notes that the stronger advertising and e-commerce backdrop could carry into Q3 2026, with the potential to underpin positive guidance from all three companies. That is a secondary signal worth watching: if all three hyperscalers beat on Q2 and guide positively for Q3, it would suggest the advertising recovery is durable rather than seasonal.

For investors following this earnings cycle, the setup is specific: Citi has made a clear call that all three companies beat, with guidance also potentially constructive. Understanding the evidential basis for that call helps you assess its credibility rather than treating it as generic optimism.

What the growth curve actually means for the AI investment cycle

Step back from the individual platform stories and a structural picture emerges. The hyperscaler growth numbers Citi is modelling are, in effect, a demand signal for the entire AI infrastructure spending cycle. Investors who track AI from the revenue side gain a different vantage point from those tracking it from the capex side alone.

Hyperscaler capex commitments of approximately $725 billion for full-year 2026 represent the supply-side infrastructure investment that Citi’s demand-side revenue projections must be read against; the question of whether AI revenue is scaling fast enough to justify that spending level is the central tension beneath all three growth estimates.

| Platform | Citi 2027 Growth Estimate | Primary AI Driver (per Citi) |

|---|---|---|

| Google Cloud Platform | 93.5% | TPU chip commercialisation plus AI compute demand |

| Amazon Web Services | 40% | AI adoption plus expanded compute capacity |

| Alibaba Cloud | 90% AI revenue CAGR | MaaS and AI computing power |

The spread between GCP’s 93.5% and AWS’s 40% is itself informative. It tells you that AI chip commercialisation, the TPU story, is compressing timelines at Google in a way that pure compute-capacity expansion at Amazon is not yet doing. The platforms are not on identical trajectories, and the investment implications of each differ. Google’s AI revenue story is being shaped by chip commercialisation; Amazon’s is being shaped by infrastructure capacity and availability.

A meaningful tension sits beneath these projections. Some analysts are comfortable with the growth curves Citi and others are now modelling. Broader market participants remain sceptical that growth above 40% CAGR can sustain at this scale. Alibaba Cloud’s trajectory, with AI-related products already at 30% of external revenue in the March 2026 quarter and on a path toward majority share, provides a live benchmark for what the growth curve looks like in practice. But whether the US hyperscalers follow the same arc remains the open question.

AI monetisation risks of the kind BCA Research has documented, specifically the structural tension between capital intensity and commoditised output, represent the bearish counterweight to Citi’s projections and give investors a framework for assessing how much of the growth curve to discount.

The signals worth watching to assess whether these growth curves are tracking as modelled:

- Whether Q2 2026 earnings beats come in at or above Citi’s specific estimates, not just consensus

- The tone of Q3 2026 guidance, particularly on AI-specific demand language

- Whether management teams begin disclosing AI-specific revenue metrics voluntarily, a sign that the numbers are strong enough to show

The question for investors is no longer whether AI is driving cloud revenue growth. The data supports that clearly. The question is whether the acceleration can sustain at the rates now being modelled, and what happens to hyperscaler valuations if it does.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These projections are based on Citi’s proprietary estimates and are subject to change based on market developments and company performance.