SEC Moves to End Mandatory Quarterly Reporting After 50 Years

7 hrs ago

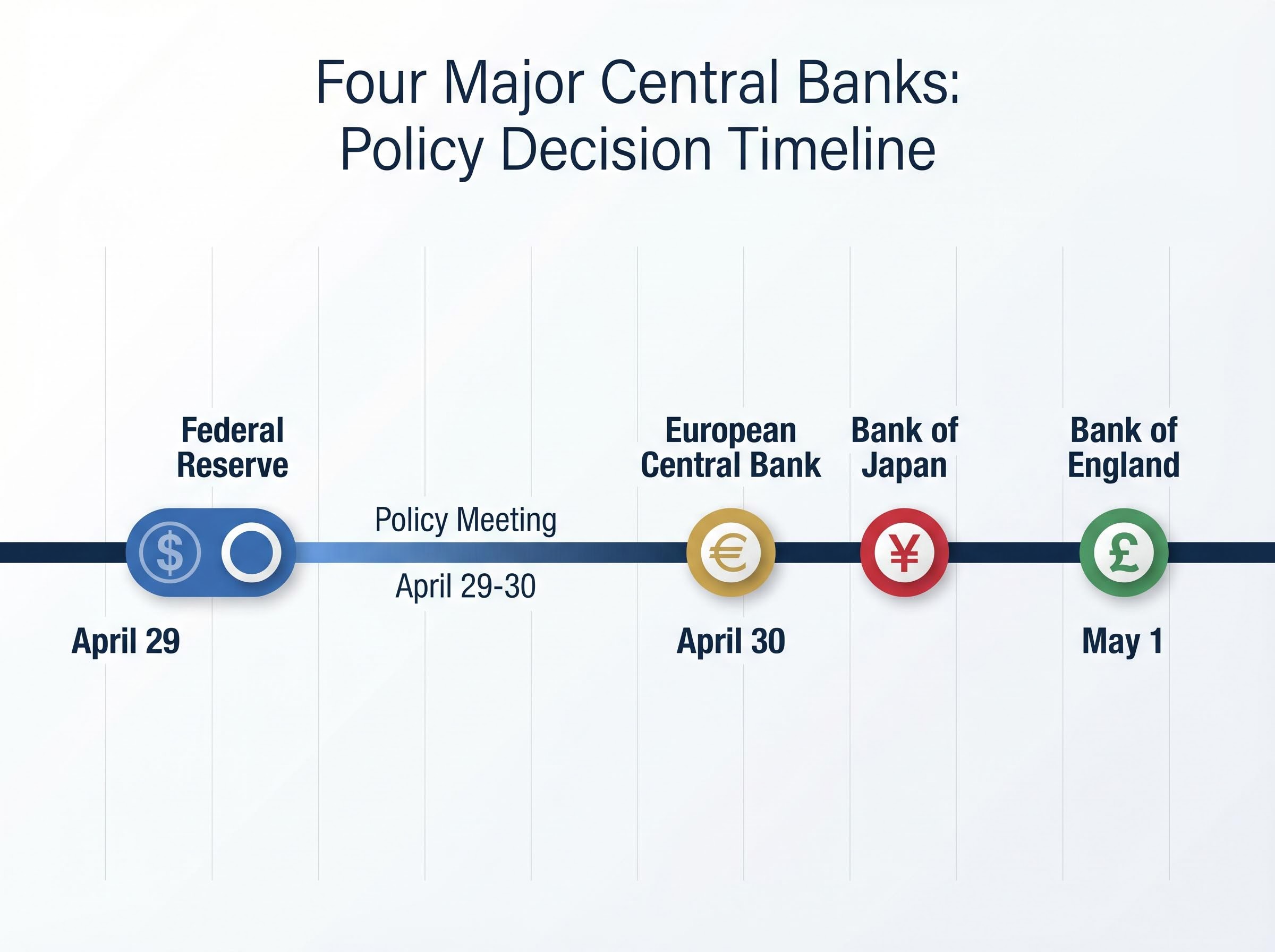

Four of the world’s most influential central banks will deliver monetary policy decisions in the coming week, each navigating the same question from starkly different starting positions: how do you fight inflation when a war is simultaneously destroying growth?

The Federal Reserve, European Central Bank, Bank of England, and Bank of Japan face policy announcements against a backdrop of U.S.-Iran tensions in the Strait of Hormuz, crude oil prices above $100 per barrel, and currency markets showing clear safe-haven rotations. The timing compresses what would normally be months of deliberation into a single, high-stakes week.

This analysis breaks down what each central bank is likely weighing, how their decisions interconnect, and what the collective policy direction signals for global markets in the months ahead.

Four major central banks announcing within days of each other creates amplified market sensitivity. Policy decisions normally absorb days of post-announcement analysis; when they arrive in a compressed window, each statement is interpreted not in isolation but as part of a coordinated signal about the global growth and inflation trade-off.

What makes the current backdrop different from prior clustered announcements is the geopolitical uncertainty. The Strait of Hormuz standoff, fragile ceasefires, and Iranian military demonstrations are forcing policymakers to weigh inflation against potential economic damage simultaneously. Energy cost pressures may discourage G10 rate hikes in coming months, according to Jane Foley, head of FX strategy at Rabobank.

The Strait of Hormuz closure has removed approximately 20 million barrels of petroleum liquids per day from global markets, representing 21% of worldwide consumption and creating the inflation pressure that now constrains every central bank decision this week.

Brent crude closed at $106.21 per barrel on 23 April 2026, with WTI at $96.77. The U.S. 10-Year Treasury yield sits at 4.332%, and the Dollar Index at 98.695, tracking weekly gains on safe-haven flows. Markets are pricing two conflicting risks at once: inflation persistence and growth contraction.

Central bank meeting schedule:

Jane Foley, Rabobank: “Energy cost pressures may discourage G10 rate hikes in coming months, as central banks weigh the risk of tightening into a supply-driven inflation shock that monetary policy cannot resolve.”

This is not a typical policy week. The clustering of decisions against an active geopolitical crisis means each announcement will be interpreted as a signal of whether central banks are prioritising inflation control or growth protection.

The Fed’s specific dilemma is visible in the currency markets. Strong dollar demand suggests markets trust the Fed’s resolve, but the same energy shock pressuring inflation is also a headwind to growth. Either choice carries visible costs.

The Federal Reserve’s dual mandate of maximum employment and stable prices creates the structural tension visible in this week’s policy dilemma, requiring the FOMC to balance inflation control against growth protection when both risks are elevated simultaneously.

Elevated energy-driven inflation argues for continued tightening. Yet further rate hikes risk tipping the economy into contraction at a moment when external shocks are already compressing growth forecasts. The dollar’s weekly strength reflects safe-haven positioning, which both validates Fed credibility and complicates export competitiveness for U.S. multinationals.

The euro trades at $1.1684, down roughly 0.7% on the week. Dollar Index gains alongside Treasury yield movements signal that markets expect the Fed to hold rates steady or continue tightening rather than pivot. Markets will parse any Fed language for signals on pause, hike, or dovish shift.

Markets now price a 73% probability of no Fed rate cuts in 2026, driven entirely by oil prices above $100 per barrel eliminating Fed rate cut expectations that had underpinned equity valuations at the start of the year.

Three scenarios markets are pricing:

Safe-haven flows into the dollar suggest markets expect the Fed to hold rates steady or continue tightening. The feedback loop is clear: dollar strength dampens imported inflation by making foreign goods cheaper, but it hurts U.S. multinationals competing abroad and pressures emerging market currencies tied to dollar-denominated debt.

For global investors, the Fed sets the tone. A hawkish stance could accelerate dollar strength and pressure emerging market currencies. A dovish tilt could spark risk-on rotation but raise questions about the Fed’s inflation commitment, potentially unsettling bond markets that have priced in terminal rate stability.

The European position differs from the Fed’s in one material respect: proximity to the energy shock. European economies are more directly exposed to energy supply disruptions, creating a more asymmetric risk profile where the cost of getting policy wrong is higher.

The ECB and BOE confront sharper trade-offs. EUROSTOXX 50 futures fell 0.65% on 23 April, and FTSE futures dropped 0.9%, reflecting investor caution ahead of policy announcements. Sterling trades near $1.3469 with a slight weekly loss, suggesting markets see the BOE as constrained rather than poised for aggressive action.

European inflation has been stickier than U.S. inflation, driven partly by energy costs and supply chain bottlenecks unique to the continent. Yet underlying growth in the eurozone remains weaker than in the U.S., limiting the ECB’s room to tighten without risking recession. The BOE faces a similar bind: UK inflation remains elevated, but household purchasing power has deteriorated sharply, and mortgage rate sensitivity is acute.

Key differences between ECB and BOE positioning:

“European central banks are navigating a crisis where the policy tools available address demand-side inflation, but the shock driving current price pressures is predominantly supply-side. That mismatch creates an unusually narrow path for credible forward guidance.”

European policy signals will affect everything from eurozone equity valuations to UK mortgage rates. A perceived policy misstep could accelerate capital outflows to dollar assets, compounding the currency pressure already visible in euro and sterling weakness.

The yen closed at 159.78 per dollar on 23 April 2026, tracking 0.7% weekly depreciation. The psychological threshold of 160 yen per dollar is widely viewed as the intervention trigger level, a line Japanese authorities have defended in prior currency crises.

Finance Minister Katayama issued an explicit warning about coordinated decisive measures with the United States if the yen continues to weaken. Golden Week holidays, running from late April into early May, immediately follow the BOJ meeting. Thin liquidity conditions during the holiday period could amplify intervention impact if authorities choose to act.

Carl Ang, senior portfolio manager at MFS Investment Management, noted that intervention during Golden Week would occur in conditions where even modest official purchases could move the currency sharply. The BOJ’s room to manoeuvre is constrained by its structural policy divergence from other G10 central banks.

Carl Ang, MFS Investment Management: “Golden Week presents unique conditions for currency intervention. Liquidity thins considerably, and the BOJ could achieve significant yen support with smaller-than-usual official purchases, making the timing strategically advantageous if authorities judge intervention necessary.”

Market consensus points to unchanged rates given yen weakness and external uncertainty. The BOJ’s divergence from other G10 central banks is a structural factor, not a meeting-by-meeting variable. Japan’s inflation readings remain below the sustained 2% target the BOJ has sought for decades, and domestic growth remains fragile.

The BOJ’s policy dilemma is the inverse of the Fed’s: while the Fed debates how much tightening is too much, the BOJ debates whether any tightening is feasible without destabilising a still-recovering economy. Currency intervention would address yen weakness without requiring a rate hike, preserving dovish policy whilst defending the 160 threshold.

For investors holding yen-denominated assets or exposed to Japanese exporters, the intervention calculus matters. A sharp yen rally triggered by coordinated intervention would compress carry trade returns and shift Asian equity flows.

The same energy shock is feeding inflation readings for all four central banks while simultaneously threatening their growth outlooks. There is no policy setting that resolves both at once.

The Strait of Hormuz standoff is the proximate cause of elevated crude prices. Iran demonstrated military control with commando boarding footage released on 18 April, and U.S. President Trump ordered mine-clearing operations in response. Brent trades at $106.21 per barrel, WTI at $96.77, both significantly above pre-crisis levels.

Energy-driven inflation is qualitatively different from demand-driven inflation. Tightening monetary policy does not increase oil supply. Central banks are being asked to solve a supply-side problem with demand-side tools, a mismatch that creates the unusually narrow policy path all four face this week.

The NBER research on central bank responses to supply shocks examines the trade-off between looking through temporary price pressures and acting to control inflation expectations, a tension that directly frames the policy choices facing all four central banks this week.

Vishnu Varathan, head of economics and strategy at Mizuho, characterised the market dynamic as taking bullish positions without genuine conviction that resolution is imminent. The path to de-escalation remains non-linear.

| Benchmark | Price (23 April 2026) | Weekly Move | Primary Driver |

|---|---|---|---|

| Brent Crude | $106.21 | +2.1% | Strait of Hormuz disruption, intervention risk |

| WTI Crude | $96.77 | +1.8% | U.S. naval positioning, supply constraint fears |

Vishnu Varathan, Mizuho: “Markets are taking bullish positions on oil, but the conviction that resolution is imminent remains low. The path to de-escalation is non-linear, and central banks are pricing that uncertainty into their forward guidance in real time.”

Understanding this mismatch helps investors interpret policy signals more accurately. If central banks collectively pause or soften guidance, it validates that growth fears are dominating. If they stay hawkish despite energy uncertainty, it signals inflation commitment is prioritised, with all the growth costs that entails.

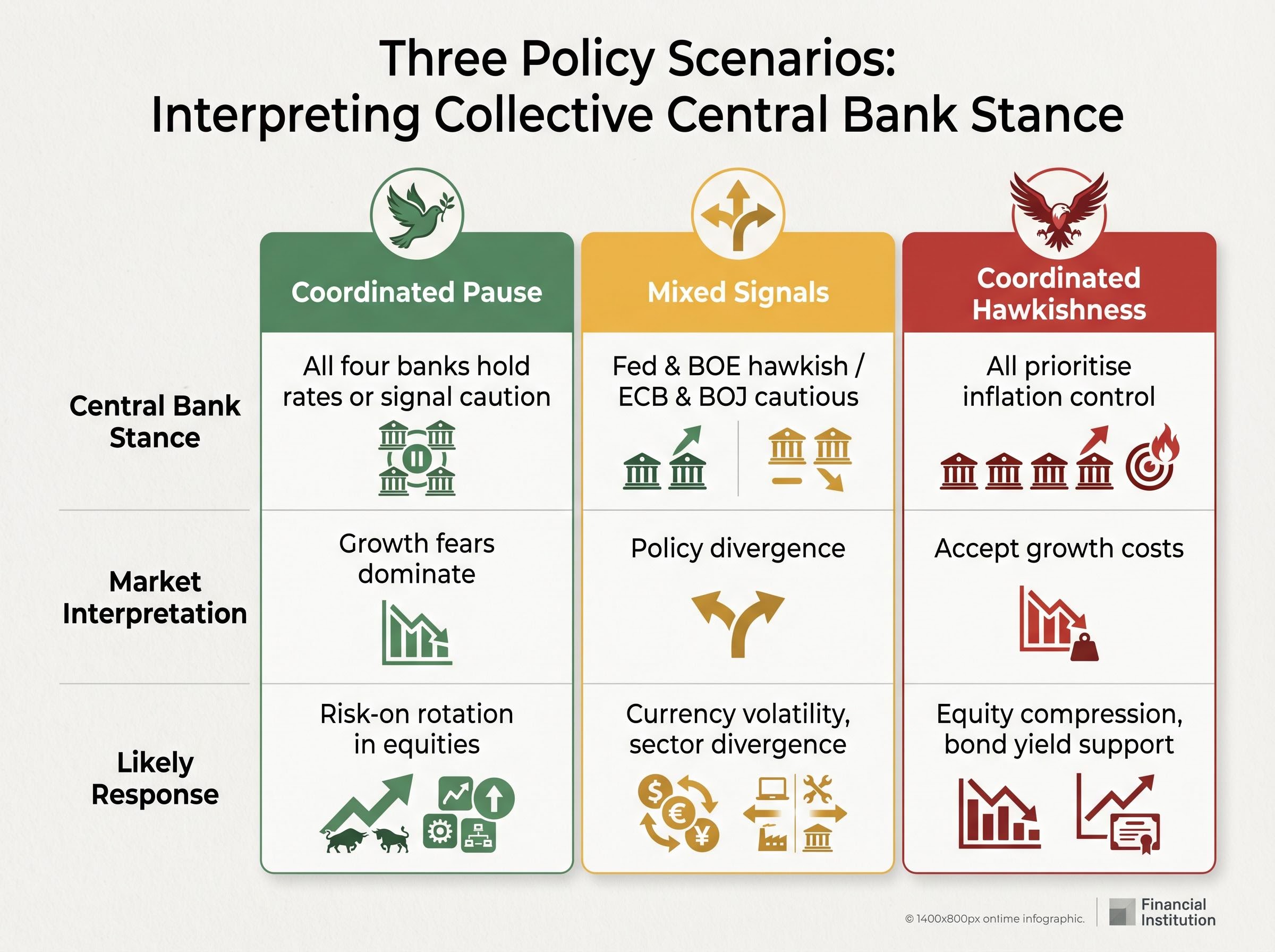

The forward-looking implications hinge on whether central banks collectively pause, diverge, or maintain hawkishness. Each path validates a different reading of the inflation-versus-growth debate.

A coordinated pause would signal that growth fears dominate. It would suggest central banks see the energy shock as large enough to compress activity regardless of policy stance, making further tightening counterproductive. Continued hawkishness, by contrast, would signal that inflation commitment is prioritised even at visible growth costs. Markets would interpret this as central banks willing to accept recession risk to anchor inflation expectations.

Divergence between central banks could drive currency volatility and sector rotation. A hawkish Fed paired with a dovish BOJ would widen yield differentials, strengthening the dollar further and pressuring yen-denominated assets. A cautious ECB alongside a firm BOE would create intra-European divergence, complicating eurozone equity positioning.

Treasury yields offer one gauge of market expectations. The 10-Year yield sits at 4.332%, the 30-Year at 4.92%. The VIX closed at 19.31, up 2.06%, reflecting elevated hedging demand. Gold remains flat at $4,691.60, suggesting safe-haven flows are muted despite uncertainty, possibly because real yields remain positive enough to compete with non-yielding assets.

Three interpretive scenarios for collective policy stance:

Core investor question: Does the collective policy stance this week validate that central banks see the energy shock as transitory and manageable, or as a structural threat that requires prioritising growth protection over inflation targets?

The coming week’s decisions will set the tone for Q2 and Q3 positioning. A coherent read of the collective policy stance is more valuable than parsing any single announcement in isolation. Investors should focus on the language around growth risks, the consistency of forward guidance across central banks, and whether the policy divergence widens or narrows.

For investors exploring how institutional portfolios are responding to the inflation-growth trade-off central banks now face, our dedicated guide to stagflation positioning and hard asset allocation strategies examines how Bridgewater, Berenberg, and other leading institutions have restructured portfolios around precious metals and inflation-protected assets in 2026.

The convergence of four major central bank decisions against an unresolved energy shock and active geopolitical standoff makes the coming week unusually consequential. Each policymaker faces the same inflation-versus-growth tension, but their starting positions, currency pressures, and domestic constraints differ materially.

The Fed navigates from a position of relative strength but with dollar appreciation complicating the picture. European central banks face sharper trade-offs due to energy exposure and weaker underlying growth. The BOJ’s intervention calculus operates independently of its rate decision, driven by yen threshold defence rather than inflation targeting.

Investors should monitor not just individual rate decisions but the collective language around growth risks and forward guidance. The policy stance that emerges will shape yield differentials, currency flows, and sector leadership through mid-year.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Central bank policy decisions are official announcements on interest rates and forward guidance that directly influence borrowing costs, currency values, equity valuations, and bond yields. When four major central banks announce within days of each other, as scheduled for late April and early May 2026, the collective signal can reshape global asset allocation in a compressed timeframe.

The Strait of Hormuz standoff has removed approximately 20 million barrels of petroleum liquids per day from global markets, pushing Brent crude to $106.21 per barrel and creating supply-driven inflation that monetary policy tools cannot directly resolve. This forces the Fed, ECB, Bank of England, and Bank of Japan to weigh tightening against the risk of deepening a growth contraction caused by energy costs.

Market consensus points to unchanged rates from the Bank of Japan, given yen weakness and external uncertainty. Authorities are instead focused on potential currency intervention to defend the psychological threshold of 160 yen per dollar, with Finance Minister Katayama warning of coordinated decisive measures if the yen continues to depreciate.

If all four major central banks hold rates steady or signal caution simultaneously, it would validate that growth fears are dominating policy thinking, which typically sparks risk-on rotation into equities and compresses bond yields. Investors should monitor the collective language around growth risks rather than parsing each individual rate decision in isolation.

Oil prices above $100 per barrel have eliminated the disinflationary conditions that underpinned earlier Fed rate cut expectations, with energy-driven inflation making it difficult for the FOMC to justify easing without risking an unanchoring of inflation expectations. This shift has materially repriced rate cut probabilities that had supported equity valuations at the start of the year.