CSL Share Price: Real Turnaround or Relief Rally?

18 mins ago

Morningstar Investment Management Australia is buying Nike, Burberry, and Kering while all three are posting some of the weakest earnings of the past decade. Higher input costs, cautious US consumers, collapsing Chinese luxury demand, and tariff friction have converged to drive share prices down and keep them there.

That convergence is precisely the point. Ameya Hattangadi, Associate Portfolio Manager at Morningstar Investment Management Australia, frames it as the entry discipline the firm’s process is designed to exploit: rank global stocks by price relative to normalised (cycle-average) earnings, buy only those in the cheapest roughly 20% of the universe where the problems look temporary, and wait for mean reversion to do the heavy lifting.

Here is what the thesis actually rests on, where it is most vulnerable, and what Australian investors need to weigh before acting on it.

The logic is deliberately uncomfortable. Morningstar’s equity process does not screen for stocks with improving momentum or rising consensus estimates. It screens for the opposite: businesses where the gap between current earnings and what the franchise can earn in a normal environment is widest.

Right now, all four of the headwinds Hattangadi identifies are hitting consumer-facing multinationals simultaneously:

Each pressure alone would dent earnings. Together, they create the kind of trough that makes a stock look uninvestable on a trailing price-to-earnings (P/E) screen, which is the ratio of a company’s share price to its earnings per share and the most common quick measure of whether a stock is cheap or expensive.

As of Morningstar’s mid-2026 assessment, the US equity market’s forward P/E sits above both its five-year and ten-year historical averages, placing the broader market in expensive territory. These three stocks, by contrast, are priced as though their current earnings depression is permanent. Morningstar’s bet is that it is not.

A trailing P/E ratio tells you what the market is paying for what a company earned over the past twelve months. When those twelve months happen to capture a cyclical trough, the ratio is misleading. It either looks artificially high (because earnings are temporarily crushed) or it cannot be calculated at all (because the company is loss-making).

The P/E ratio limitations that make Burberry and Kering look uninvestable on conventional screens are the same ones that have historically concealed the best entry points in cyclically depressed franchises; free cash flow yield, EV/EBITDA, and normalised earnings each correct a specific blind spot that trailing P/E cannot see.

Normalised earnings strip out the trough. They estimate what a business can earn across a full cycle by using average margins and returns rather than the current depressed figures. The framework pushes investors toward names the market has abandoned, which is uncomfortable but historically where value has been found.

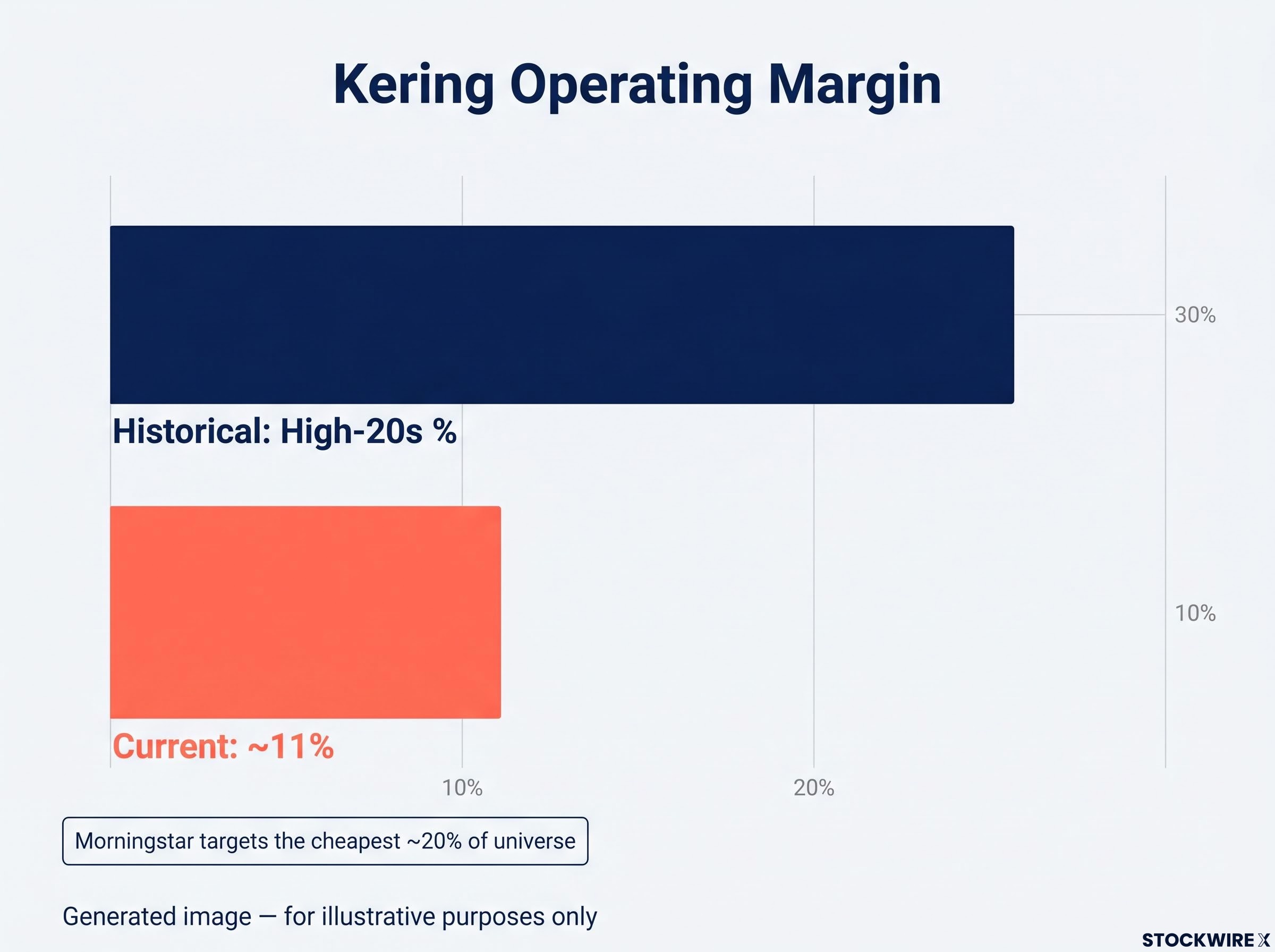

Kering’s current operating margin sits at approximately 11%. Its historical margins ran in the high-20s percentage range. That gap is the entire thesis in one number.

For a retail investor screening stocks on trailing P/E, Kering may look expensive or unrankable right now. Burberry posted negative free cash flow of negative £184 million and a roughly 20% revenue decline in its most recent first-half results. On conventional screens, these look like stocks to avoid. On a normalised-earnings screen, they look like franchises priced for a future far worse than the one Morningstar expects.

That optical illusion is what the normalised framework is designed to correct. And Morningstar’s selectivity bar is high: only the cheapest roughly 20% of its entire universe qualifies for consideration.

Each of these three businesses is dealing with a different version of the same problem: cyclically and operationally depressed earnings inside a franchise Morningstar believes retains long-term competitive strength.

| Company | Moat Rating | Star Rating | Key Turnaround Lever | Fair Value Signal |

|---|---|---|---|---|

| Burberry | Narrow | 5-star | Outerwear and scarves refocus (approximately 40-50% of revenue) | Approximately 80% upside to fair value estimate |

| Kering | Narrow | Not specified | ReconKering plan: more than double operating margin from 2025 levels | Fair value EUR 334/share (reduced from EUR 360) |

| Nike | Not specified | Not specified | Inventory clearance, direct-to-consumer recalibration | Not specified |

Burberry has suspended dividends and is resetting prices on commoditised lines (polo shirts, leather goods) to levels seen 18-24 months ago while selectively raising prices on its strongest categories. The high uncertainty rating is Morningstar’s own acknowledgement that executing a fashion turnaround in this macro environment is genuinely difficult.

Kering has launched its ReconKering plan targeting a return on capital above 20% and roughly 20% reduction in Gucci store space. The targets stretch to approximately 2028. Gucci’s quarterly sales are still declining double digits year-on-year, though the rate of decline has eased.

Nike retains dominant brand equity, athlete endorsements, and innovation capacity, but is working through an inventory overhang and margin pressure from input costs and softer North America and China demand.

All three cases share the same structural dependency. The turnaround at each company must actually gain traction for the normalised-earnings thesis to be validated. Without execution, the discount to fair value is simply a discount to a future that never arrives.

China is not one risk among many for this thesis. It is the single variable most likely to determine whether the path back to normalised earnings takes two years or six.

Morningstar’s research describes the decline in luxury spending as “widespread” and “especially harsh in China.”

Burberry and Kering derive significant revenue and margin from Chinese consumers, both domestically in China and through Chinese tourist spending abroad. The question is whether this spending decline is cyclical, driven by household confidence and property market stress, or structural, reflecting a lasting shift in how Chinese consumers relate to Western luxury brands. That question is not yet answered.

Gucci’s quarterly sales were still declining double digits year-on-year as of mid-2026, though the pace has moderated. If Chinese consumer confidence recovers, it would likely act as a meaningful catalyst for both Burberry and Kering. If it deteriorates further, Morningstar’s own research acknowledges the risk: what it currently views as cyclical earnings depression could prove closer to a structural reset at a lower profitability level.

That distinction matters directly to your position sizing. If you are considering these names, China is not background noise. It is the variable most likely to determine whether your investment thesis resolves in two years or gets pushed out to five or beyond.

Investors who want to stress-test the China recovery assumption before sizing these positions will find our deep-dive into China’s two-speed economy covers the structural property-consumption divergence, the first contraction in domestic consumer spending since late 2022, and the institutional positioning shifts that major banks are making in response.

Hattangadi has flagged a market-level dynamic that sits on top of all the stock-specific risks already discussed, and it applies to the next 90 days specifically.

Under normal conditions, analyst forecasts drift lower as a reporting period approaches, giving management teams a reduced target to clear and creating room for positive surprises. In the second quarter of 2026, that pattern reversed: rather than trimming their numbers ahead of the reporting season, analysts revised estimates upward, raising the bar companies must now clear.

That creates a binary setup with asymmetric consequences:

For investors in beaten-down consumer stocks, this dynamic matters even if the long-term recovery thesis is intact. Macro-driven selling does not distinguish neatly between cheap and expensive names. A broad de-rating in the coming weeks could deliver sharp mark-to-market losses on Nike, Burberry, or Kering regardless of their individual turnaround progress.

Morningstar’s thesis is coherent, specific, and evidence-based. It is also explicitly a multi-year position, not a multi-month trade. Kering’s ReconKering plan and Burberry’s turnaround targets stretch to approximately 2028. The distance between here and there is where the discomfort lives.

Australian investors can access these names through direct international equity holdings, global equity managed funds, or exchange-traded funds (ETFs) with consumer discretionary exposure. The route matters less than the question of whether you have the conviction and time horizon to hold through what could be a volatile interim.

International equity access for Australian investors spans direct foreign holdings, ASX-listed ETFs with consumer discretionary exposure, and global managed funds, each carrying different cost structures, currency treatment, and tax reporting obligations that affect the after-tax return on positions in Nike, Burberry, or Kering.

Three variables will determine whether this thesis is vindicated or extended:

The question worth asking is not whether Morningstar is right about these stocks over five years. It is whether you have the risk tolerance to hold through the volatility that is likely to accompany the wait.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Normalised earnings estimate what a business can earn across a full economic cycle by using average margins rather than current depressed figures. For stocks like Kering, whose operating margin has fallen to roughly 11% from historical highs in the high-20s percentage range, normalised earnings reveal a far more attractive valuation than a standard trailing price-to-earnings ratio would show.

Morningstar's process ranks global stocks by price relative to cycle-average earnings and buys only those in the cheapest roughly 20% of its universe where the headwinds appear temporary. Higher input costs, US consumer caution, collapsing Chinese luxury demand, and tariff friction have converged to create trough earnings that make these franchises look uninvestable on conventional screens, which is precisely the entry point the strategy targets.

China is the single variable most likely to determine whether the path back to normalised earnings takes two years or six. Both Burberry and Kering derive significant revenue from Chinese consumers, and it remains unresolved whether the current spending decline is cyclical or a structural reset at a permanently lower profitability level.

Australian investors can access these names through direct international equity holdings, global equity managed funds, or ASX-listed exchange-traded funds with consumer discretionary exposure, each carrying different cost structures, currency treatment, and tax reporting obligations that affect after-tax returns.

ReconKering is Kering's operational turnaround plan targeting a return on capital above 20%, a roughly 20% reduction in Gucci store space, and more than doubling operating margins from 2025 levels, with targets stretching to approximately 2028. Morningstar has set a fair value estimate of EUR 334 per share for Kering under this recovery scenario.