How Geopolitical Risk Is Repricing Oil, Inflation and Bonds at Once

28 mins ago

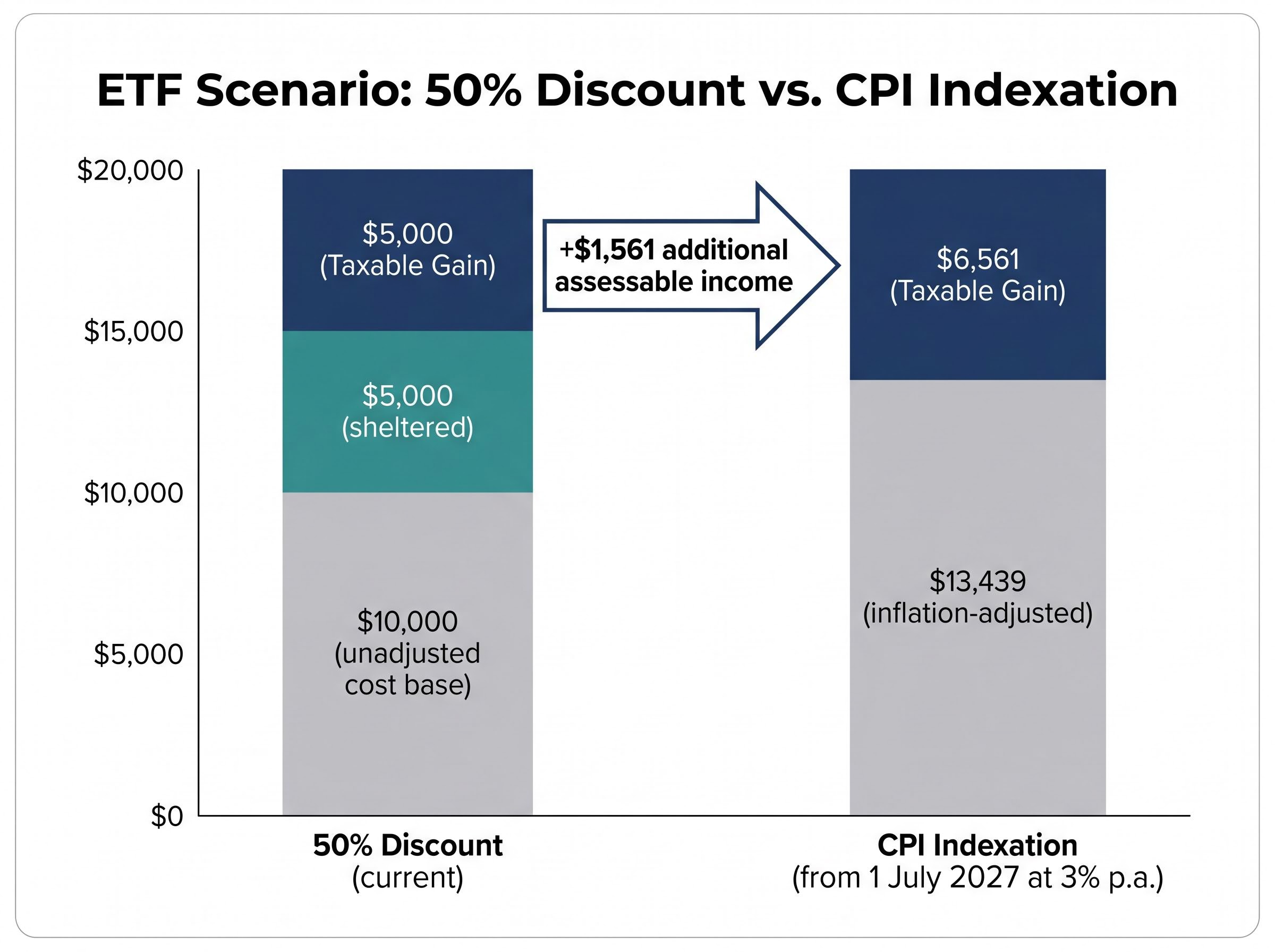

Australia’s capital gains tax changes, confirmed in the 12 May 2026 Federal Budget, replace a system investors have used for 26 years with one the country abandoned in 1999. Under the reinstated CPI indexation model taking effect 1 July 2027, a $10,000 ETF investment sold a decade later for $20,000 would produce a taxable gain of approximately $6,561, compared with $5,000 under the outgoing 50% discount. The difference is not dramatic. But it moves in a consistent direction, and it touches every asset class differently.

This article does not revisit the mechanics in exhaustive detail. It examines what the Budget means for where Australians should be directing capital: established property versus equities, income-oriented ASX stocks versus high-growth international assets, and super versus non-super structures. The case for each has shifted at the margin. What follows works through how, and by how much.

The 50% CGT discount worked by halving the nominal gain. An asset bought for $10,000 and sold for $20,000 produced a $10,000 nominal gain, of which $5,000 was assessable. The calculation was simple and identical regardless of how long the asset was held beyond 12 months.

CPI indexation works differently. It adjusts the original cost base for inflation, then taxes the entire remaining gain. Only the inflation component is sheltered; everything above it is fully assessable.

The formula is straightforward: the CPI at the quarter of sale divided by the CPI at the quarter of purchase, multiplied by the original cost base.

The ATO indexation methodology for CGT cost bases confirms that the adjusted cost base is calculated by multiplying the original cost by the CPI ratio between the acquisition quarter and the disposal quarter, with each asset parcel indexed separately from its own acquisition date.

Consider shares bought for $10,000 in the March 2020 quarter (CPI 114.1), sold in a hypothetical June 2030 quarter (CPI 145.0) for $25,000. The inflation-adjusted cost base becomes $12,710. The taxable gain is $12,290, the full distance between the adjusted base and the sale price.

The following table illustrates the comparison using the ETF scenario:

| Scenario | Cost Base | Taxable Gain | Tax Outcome |

|---|---|---|---|

| 50% Discount (current) | $10,000 (unadjusted) | $5,000 | Half the nominal gain assessed |

| CPI Indexation (from 1 July 2027) | $13,439 (inflation-adjusted at 3% p.a.) | $6,561 | Full real gain assessed |

The difference, approximately $1,561 in additional assessable income on a $10,000 position, is modest in isolation. Across a diversified portfolio held for a decade or longer, it compounds.

Newly constructed residential dwellings receive a carve-out: investors in new builds can elect between the 50% discount and CPI indexation. Established properties and all shares receive indexation only from 1 July 2027.

One dimension of the Budget not covered in this analysis is the end of the pre-1985 asset exemption, which removes a four-decade CGT-free status for assets acquired before September 1985 and replaces it with a deemed cost base equal to market value at 1 July 2027, creating material valuation risk for holders of long-standing family properties and farms.

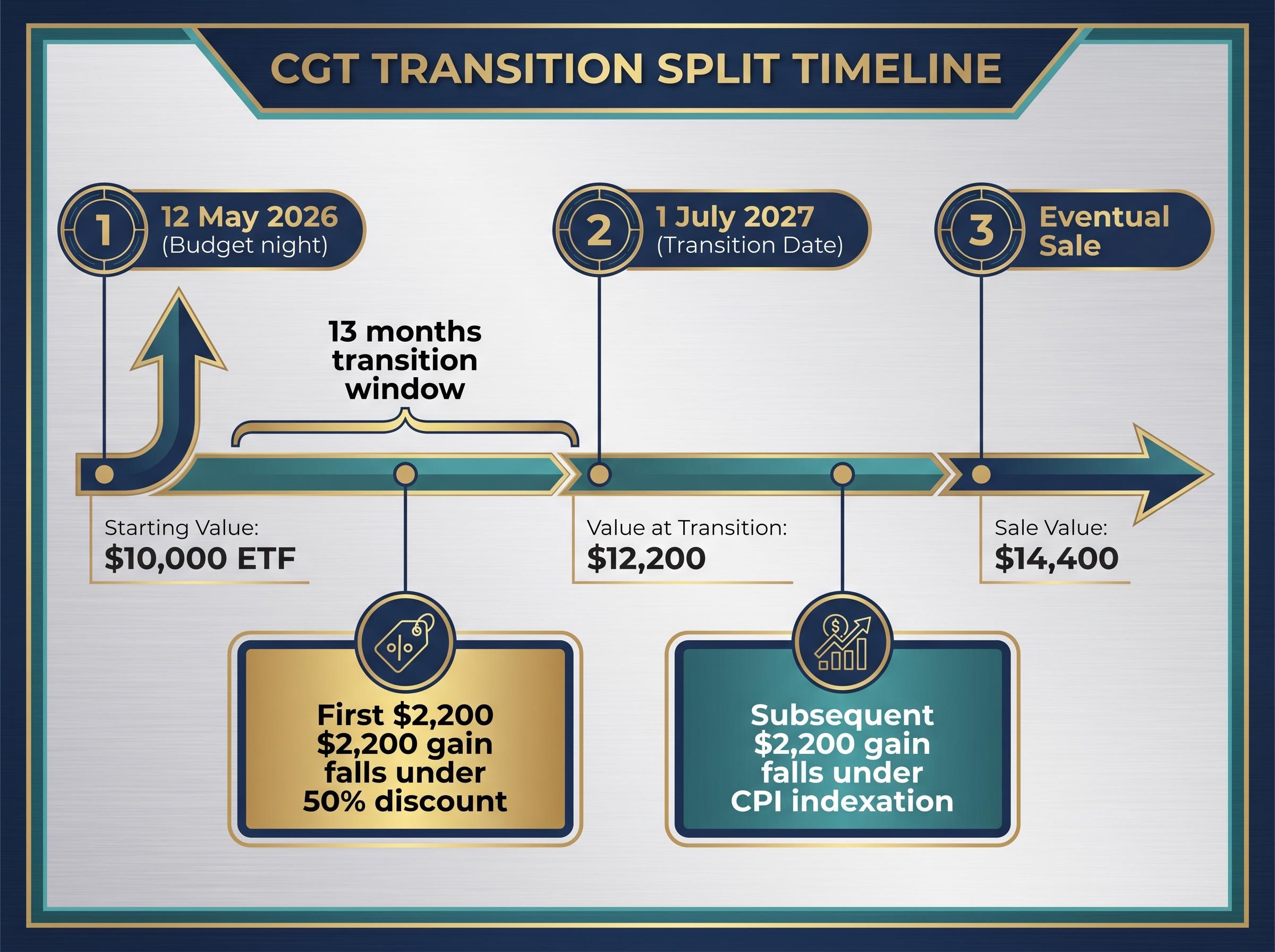

The market value on 1 July 2027 serves as the dividing line between the two regimes. Gains accrued before that date retain eligibility for the 50% discount. Gains accruing after that date are subject to CPI indexation.

For the $10,000 ETF that has grown to $12,200 by the transition date and is eventually sold at $14,400, the first $2,200 of gain falls under the discount system and the subsequent $2,200 under indexation. Investors can obtain a formal valuation or use an ATO-approved apportionment formula; however, ATO guidance tools are anticipated but not yet released as of mid-May 2026.

The Budget removed two of established property’s structural advantages simultaneously. Negative gearing has been curtailed, reducing the annual tax benefit of holding a loss-making investment property. The 50% CGT discount has been abolished for established dwellings, removing the other half of the tax arbitrage that supported leveraged property investment for more than two decades.

The double adjustment matters because these two mechanisms operated as a pair: negative gearing reduced the annual carrying cost, and the CGT discount magnified the after-tax gain on eventual sale. With both trimmed, the after-tax return profile of established residential property has compressed from two directions at once.

Equities face only one of these changes. The CGT discount is gone, but equities retain several structural features that property does not:

The new-build carve-out (election between 50% discount and indexation) is a deliberate policy signal favouring housing supply. It does not extend to established property or to shares. The pre-Budget Senate Committee on CGT had identified established housing as a primary target of the discount reform.

Rob Wilson, Director of Investment Strategy at Selfwealth, observed that equities now offer characteristics unavailable in established property, including liquidity, flexibility, and comparatively lower policy risk following this Budget.

The indexation system shelters only the inflation component of a gain. This creates an asymmetry that depends on how far an asset’s growth rate exceeds the inflation rate.

An asset that appreciates at roughly the rate of inflation, say 3% annually, generates almost no taxable gain under indexation. In certain scenarios, particularly elevated inflation environments, such an asset may produce a smaller tax liability under indexation than under the old 50% discount.

High-growth equities sit at the opposite end. A global technology stock that compounds at 12-15% annually in a 3% inflation environment sees only a small fraction of its gain sheltered. Most of the appreciation sits above the inflation-adjusted cost base and is fully assessable. Investors with a very low original cost base are most exposed, because adjusting a small base for inflation still leaves the overwhelming majority of the gain taxable.

| Asset Type | Growth Rate | Inflation | Taxable Gain (Indexation) | Position vs Old Discount |

|---|---|---|---|---|

| High-growth global equity | 12% p.a. | 3% | Large (minimal shelter) | Worse off |

| Income ASX stock (franked) | 5% p.a. | 3% | Moderate (partial shelter) | Broadly neutral; franking intact |

| Inflation-tracking asset | 3% p.a. | 3% | Minimal | Better off in some scenarios |

The imputation system itself is entirely unaffected by the Budget. Fully franked dividends continue to carry tax credits that offset the investor’s personal tax liability, exactly as before.

What has changed is the comparison. The CGT treatment of growth assets has become less favourable, which means the relative position of franked dividend income has improved without any alteration to dividend taxation itself. This is a shift in the comparison, not a windfall for income investors.

According to Selfwealth analysis, domestically listed equities paying fully franked dividends retain a structural tax advantage through the unchanged imputation system. Rob Wilson, writing in coverage published by Bloomberg and the Australian Financial Review, has cautioned against portfolio restructuring based solely on this change.

A well-known planning strategy allowed investors to time the sale of growth assets to coincide with low-income years, typically in early retirement or career breaks, to minimise the effective CGT rate by leveraging a lower marginal tax bracket.

The 30% minimum tax floor on real (CPI-adjusted) capital gains, effective from 1 July 2027, eliminates this approach. Regardless of the investor’s total income in the year of sale, the tax rate on real capital gains cannot fall below 30% for most non-super investors. The hard lower bound applies irrespective of whether the investor has no other assessable income in that year.

Superannuation funds, including self-managed super funds (SMSFs), retain their existing CGT treatment entirely. This makes the super environment comparatively more attractive for long-held growth assets, particularly for investors who previously planned to hold appreciation outside super and time disposals around low-income periods.

Pension-phase earnings in superannuation are taxed at 0% under current legislation, a structural advantage that exists entirely outside the CGT framework and compounds meaningfully over multi-decade accumulation periods; for investors on a 37% marginal rate, the difference in tax treatment on identical underlying portfolios can exceed $230,000 over 25 years without any difference in investment returns.

Three investor categories are most directly affected:

The announced changes still require parliamentary passage, and final details may be revised during the legislative drafting process. Investors should seek professional guidance before acting on this change.

CPI indexation applies identically to domestic and international equities. There is no differential CGT treatment based on where a stock is listed, which means the Budget has not introduced a new tax-based reason to favour ASX-listed equities over offshore holdings or vice versa.

The case for international diversification remains what it was before the Budget: a risk and return argument. The ASX is concentrated in financials and resources, and investors seeking exposure to global technology, healthcare innovation, and consumer platforms must look offshore. Reducing concentration risk in a single national market is a portfolio construction principle that the CGT changes do not alter.

ASX concentration in financials and resources means that domestic-heavy portfolios are structurally exposed to Australian bank cycles and commodity prices rather than the technology-led sectors that drove global equity outperformance over the past decade, a distinction that matters when assessing whether the marginal CGT cost of holding international growth equities is justified by the diversification benefit.

The one nuance worth noting is that international growth equities appreciating well above inflation are incrementally more exposed to the indexation shift than domestically listed income stocks paying franked dividends. This is a real but marginal cost consideration within a diversified portfolio, not a reason to abandon international exposure.

The primary arguments for maintaining international holdings that are unaffected by the Budget include:

According to Selfwealth analysis, the case for international diversification is not materially altered by this Budget.

The period between Budget night (12 May 2026) and 1 July 2027 provides approximately 13 months of transition. That is adequate time for deliberate modelling and professional consultation, not a deadline that demands immediate portfolio changes.

Tax settings inform the margin of an allocation decision. They do not replace the fundamentals: risk tolerance, expected returns, liquidity requirements, and investment time horizon continue to drive portfolio construction. The complexity of the new indexation calculation, particularly for investors with multiple share parcels, dividend reinvestment plan (DRP) accumulations, or properties with various capitalised costs (each asset parcel indexed separately from its acquisition quarter), makes professional guidance practically necessary.

Four practical steps for the transition period:

For investors wanting to move beyond the four steps outlined here into a full action checklist, our comprehensive walkthrough of CGT transition planning covers grandfathering mechanics for existing holdings, contribution maximisation strategies using unused concessional cap space, and a sequenced approach to cost-base modelling across share parcels, DRP accumulations, and investment properties.

Rob Wilson of Selfwealth has emphasised that the one-year transition window provides adequate time to model individual positions and consult advisers rather than react prematurely. The implementing legislation has not yet passed, and ATO calculation tools remain pending.

The CGT overhaul moves the relative attractiveness of income stocks, established property, and growth equities at the margin. It does not overturn the fundamental logic of diversified, return-focused asset allocation.

Three directional shifts are confirmed by the analysis. First, equities have gained ground over established property as a capital accumulation vehicle, given the simultaneous loss of both negative gearing benefits and the CGT discount. Second, income-oriented ASX stocks paying franked dividends have become incrementally more attractive relative to high-growth international assets, though the magnitude is contextual. Third, superannuation has become more appealing for long-held growth assets relative to non-super structures, given the 30% minimum tax floor outside super.

The implementing legislation has not yet passed, and ATO guidance tools remain pending. These factors make professional consultation during the transition window not optional but necessary.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. The policy measures discussed are subject to parliamentary passage, and final legislative details may differ from the Budget announcements described here.

Investors can use the worked examples in this article as a starting framework for modelling their own positions, and should engage a financial adviser or tax accountant before the 1 July 2027 transition date.

From 1 July 2027, Australia's 50% CGT discount is replaced by CPI indexation, meaning only the inflation component of a gain is sheltered and the full real gain above the inflation-adjusted cost base is assessable. The change was confirmed in the 12 May 2026 Federal Budget and applies to established property and all shares.

Under CPI indexation, the original cost base is adjusted for inflation before the taxable gain is calculated, whereas the 50% discount simply halved the nominal gain. On a $10,000 investment sold for $20,000 after a decade, the taxable gain is approximately $6,561 under indexation compared with $5,000 under the old discount, a difference of around $1,561 in additional assessable income.

Gains accrued before 1 July 2027 retain eligibility for the 50% discount, while gains accruing after that date are subject to CPI indexation. Investors will need to establish the market value of their holdings on that date, either through a formal valuation or an ATO-approved apportionment formula, though ATO guidance tools were still pending as of mid-May 2026.

The 30% minimum tax floor on real capital gains, effective from 1 July 2027, means the CGT rate cannot fall below 30% for most non-super investors regardless of their total income in the year of sale, eliminating the strategy of timing asset disposals to coincide with career breaks or early retirement to access a lower marginal tax bracket.

Yes, superannuation has become comparatively more attractive for long-held growth assets because the 30% minimum tax floor applies outside super but not within it. Pension-phase super earnings are taxed at 0% under current legislation, and for investors on a 37% marginal rate the difference in tax treatment on identical portfolios can exceed $230,000 over 25 years.