What kind of investment returns 148% in 12 months, and what should an Australian investor do with that information today? The Global X Semiconductor ETF (ASX: SEMI) has delivered precisely that figure over the year to 30 May 2026, turning a sector-specific bet on the global chip supply chain into one of the most striking performances available on the ASX. The fund now sits at the intersection of two forces reshaping capital markets: the AI infrastructure build-out and the geopolitical race for semiconductor self-sufficiency. What follows is an assessment of what drove that return, how the fund is constructed, what the industry data actually says, and what the genuine risks are for an investor considering entry at current levels.

What a 148% return actually tells you about ASX: SEMI

A 148% gain over 12 months is not a normal equity return. The long-run average annual return for the ASX 200 sits in the range of 8-10%, which means SEMI delivered roughly 15 years of average market performance in a single year. That figure deserves respect and scrutiny in equal measure.

Performance snapshot: ASX: SEMI returned approximately 148% over the 12 months to 30 May 2026, with assets under management reaching A$1.001 billion as of 28 May 2026 and shares outstanding at 24,688,204. The AUM milestone signals that capital conviction has followed price appreciation.

The analytical tension is straightforward. A return of this magnitude is simultaneously evidence that a structural thesis has played out and a reason to question how much upside remains at the current entry price. The fund’s AUM crossing the A$1 billion threshold confirms that institutional and retail capital alike have recognised the semiconductor opportunity; the question is whether that recognition is now fully reflected in the price.

The sections that follow assess whether the thesis is still intact, not simply whether the number looks good.

When big ASX news breaks, our subscribers know first

The semiconductor supercycle: why chips became the new oil

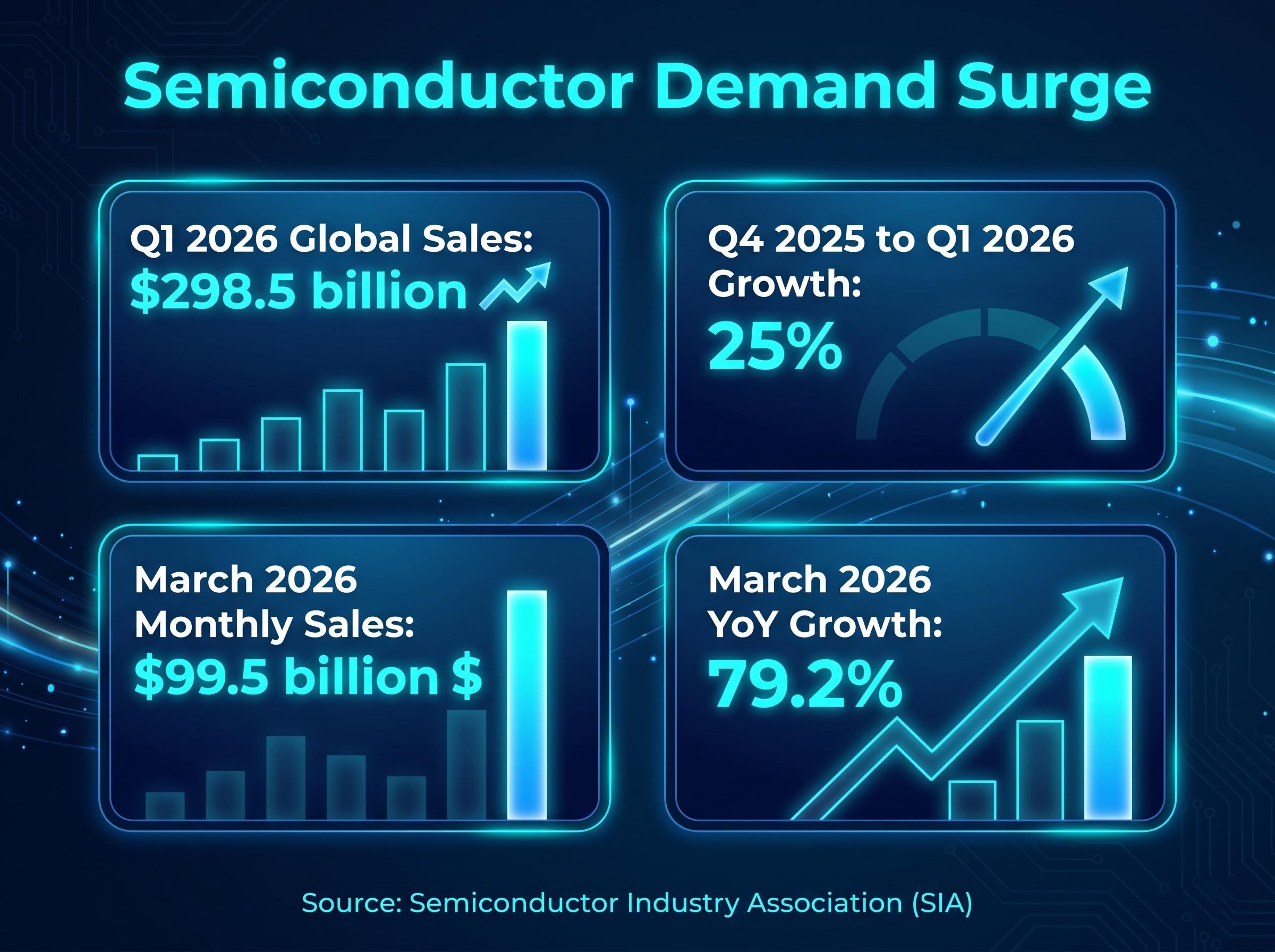

The demand data that underpins SEMI’s return is not speculative. According to the Semiconductor Industry Association (SIA), global semiconductor sales reached $298.5 billion in Q1 2026, a 25% increase from Q4 2025. March 2026 monthly sales hit $99.5 billion, representing 79.2% year-over-year growth.

These are not marginal gains. They reflect a demand environment where AI training clusters, data centre expansion, and consumer electronics refresh cycles are pulling on supply simultaneously.

The WSTS global semiconductor sales data for Q1 2026 confirms the $298.5 billion figure cited by the Semiconductor Industry Association, with year-on-year growth of 79.2% and a quarterly gain of 25.0% reflecting simultaneous demand pressure from AI infrastructure, data centre build-out, and consumer electronics refresh cycles.

| Metric | Period | Figure |

|---|---|---|

| Global semiconductor sales | Q1 2026 | $298.5 billion |

| Quarter-on-quarter sales growth | Q4 2025 to Q1 2026 | 25% |

| Monthly sales | March 2026 | $99.5 billion |

| Year-over-year monthly growth | March 2026 | 79.2% |

Deloitte’s 2026 Global Semiconductor Industry Outlook, published in February 2026, characterised the current environment as one of soaring sales alongside a strengthened emphasis on risk mitigation. That pairing matters: even industry analysts acknowledge that the boom carries complexity, not just momentum.

The current AI infrastructure investment cycle, which sees hyperscalers directing approximately 75% of combined capex toward physical hardware and data centre construction, represents the demand foundation beneath every holding in SEMI’s 30-stock portfolio; without that sustained capital commitment, the semiconductor supercycle thesis loses its primary engine.

From cyclical commodity to strategic infrastructure

Semiconductors have undergone a reclassification in how governments and corporations treat them. The U.S. International Trade Commission describes the industry as strategic infrastructure, and major economies have moved to expand domestic production capacity. This is no longer a supply-and-demand story governed purely by inventory cycles.

For investors, this reclassification carries a specific implication: it reduces the probability of a pure demand-driven collapse of the kind that ended prior semiconductor cycles. Policy tailwinds and national security priorities now provide a structural floor beneath the industry that did not exist a decade ago. That does not eliminate risk, but it changes the character of the risk an investor is taking.

Deloitte’s 2026 semiconductor industry outlook projects annual sales reaching $975 billion by end of 2026, a scale that supports the structural reclassification of chips from cyclical commodity to essential national infrastructure and helps explain why policy-driven capital flows have accompanied the demand surge.

Inside the fund: how ASX: SEMI builds its 30-stock exposure

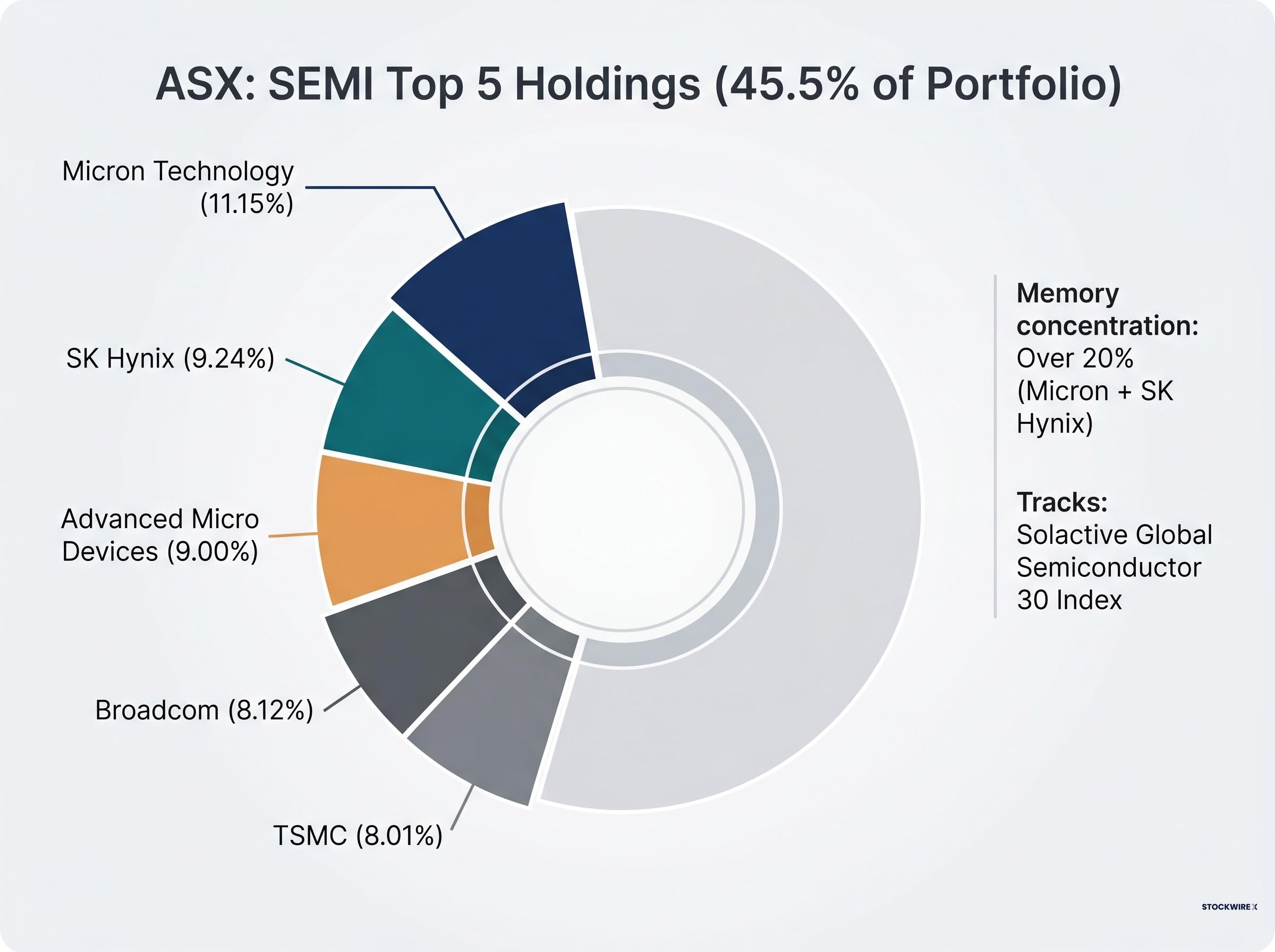

SEMI tracks the Solactive Global Semiconductor 30 Index, which holds 30 of the largest global semiconductor companies spanning chip design, manufacturing, and equipment. The portfolio covers the full supply chain, but its construction creates meaningful concentration at the top.

| Company | Sector role | Weighting |

|---|---|---|

| Micron Technology | Memory | 11.15% |

| SK Hynix | Memory | 9.24% |

| Advanced Micro Devices (AMD) | Design (CPU/GPU) | 9.00% |

| Broadcom | Design (networking/custom silicon) | 8.12% |

| Taiwan Semiconductor Manufacturing Co. (TSMC) | Foundry | 8.01% |

The top five holdings account for approximately 45.5% of the fund. An 11.15% position in Micron and a 9.24% position in SK Hynix mean that memory chip pricing dynamics alone could move the fund materially in either direction. An investor buying SEMI is not making a generic semiconductor bet; they are making a memory-heavy, design-concentrated wager with foundry exposure through TSMC.

The cost and income profile provides additional context for a sizing decision:

- Management expense ratio (MER): 0.45%

- 12-month distribution yield: 4.07% (as of 30 April 2026)

- AUM: A$1.001 billion (as of 28 May 2026)

The 4.07% yield adds a partial income component, though the return story is overwhelmingly capital appreciation. The AUM figure confirms sufficient liquidity for retail and institutional participation.

The concentration question: what a 30-stock portfolio really means for risk

A 148% return attracts capital. It also carries forward specific risks that an investor entering at current levels needs to weigh honestly.

The fund’s concentration is the most immediate concern. With five holdings each carrying between 8% and 11.15% of the portfolio, a significant drawdown in even one or two names would materially affect fund performance. This is diversification within a single sector, which is categorically different from broad portfolio diversification.

The specific risk factors worth sitting with:

- Concentration risk: Approximately 45.5% of the fund sits in five positions. Memory chip names (Micron, SK Hynix) alone represent over 20% of the portfolio.

- Post-rally valuation entry: Entering after a 148% run means buying at prices that already reflect substantial growth expectations. The remaining upside must come from the thesis continuing to exceed what the market has already priced.

- Single-sector exposure: All 30 holdings are semiconductor companies. A sector-wide headwind, whether regulatory, cyclical, or geopolitical, would affect every position simultaneously.

- Currency risk: Australian investors hold a fund denominated in USD-exposed assets. Currency movements between the Australian dollar and the US dollar add a layer of return variability independent of semiconductor fundamentals.

A Morningstar-identified capex-to-revenue lag of 18-24 months represents the central counterargument to an immediate entry thesis, because the hyperscaler spending that is currently lifting semiconductor valuations has not yet produced the revenue flows that would justify those valuations on a forward earnings basis.

Industry caution signal: Deloitte’s 2026 Global Semiconductor Industry Outlook pairs its characterisation of soaring sales with a strengthened emphasis on risk mitigation, a framing that suggests even industry-level analysis recognises the current environment demands discipline alongside conviction.

The MER of 0.45% is not prohibitive, but it represents an ongoing cost that compounds through periods of volatility. Holding through a drawdown means paying for the privilege of waiting for recovery.

Who should actually consider ASX: SEMI at current levels

The question is not whether semiconductors matter. The Q1 2026 sales data answered that. The question is whether this specific fund, at this specific price, fits a specific investor’s portfolio.

Investors for whom ASX: SEMI fits the thesis

- Long-horizon investors (five years or more) who want diversified exposure to the semiconductor supply chain without the single-stock risk of owning Micron or TSMC directly.

- Investors seeking AI-adjacent infrastructure exposure who are underweight technology in their current portfolio and want a single instrument covering design, manufacturing, and equipment.

- Those comfortable with sector-specific volatility who understand that a 148% gain over 12 months implies the possibility of significant drawdowns in subsequent periods.

- Income-supplemented growth seekers who value the 4.07% distribution yield as a partial return component alongside capital appreciation potential.

Investors who should think carefully before entering

- Short-horizon investors who may need to exit within 12-18 months, where a post-rally correction could lock in losses.

- Those already concentrated in technology equities, for whom adding SEMI would compound sector-specific risk rather than diversify it.

- Investors sensitive to entry-point risk who are uncomfortable buying an asset that has nearly tripled in price over the preceding year.

- Those seeking broad portfolio diversification, since a 30-stock fund within a single sector does not replace a multi-sector allocation strategy.

The fund’s AUM of A$1.001 billion provides a liquidity signal: daily trading volumes are sufficient for retail-sized positions without meaningful price impact. The Solactive index’s 30-stock global scope offers supply-chain breadth that single-stock selection cannot match, but it remains a concentrated sector bet by design.

Investors weighing whether to add SEMI or to complement it with broader AI exposure will find our dedicated guide to GXAI versus SEMI useful; it compares the two funds across supply-chain scope, holdings overlap, and return profile, and examines how AINF fits as a third layer for investors wanting infrastructure exposure alongside the semiconductor supply chain.

The semiconductor thesis is intact, but the easy money is gone

The structural case for semiconductors is supported by verifiable data. Q1 2026 sales of $298.5 billion, quarterly growth of 25%, and year-over-year monthly growth of 79.2% confirm that demand is accelerating, not plateauing. Governments have reclassified chips as strategic infrastructure. AI capital expenditure continues to expand.

The entry-cost reality is equally clear. A 148% 12-month return means the market has already priced substantial growth expectations into the fund. AUM crossing A$1 billion confirms broad investor recognition of the thesis. What remains is the question of whether ongoing structural tailwinds can deliver returns above what is now embedded in the price.

The semiconductor bubble narrative has attracted serious analytical scrutiny, with Bank of America’s Savita Subramanian publishing a note in May 2026 citing record free cash flow yields, upward earnings revisions exceeding 20%, and positioning levels at roughly half the 2017 cycle peak as evidence that the sector’s valuation is supported by fundamentals rather than speculative excess.

The core tension: Strong structural fundamentals, confirmed by Q1 2026 industry data and government reclassification of semiconductors as strategic infrastructure, meeting an elevated entry price after a 148% run. The opportunity is real; the margin for error at current levels is narrower than it was 12 months ago.

Deloitte’s emphasis on risk mitigation alongside growth captures the industry’s own recognition that this boom has matured. For an Australian investor, the decision is not whether to believe in semiconductors. It is what sized, long-horizon position fits their portfolio at a price that already reflects considerable conviction.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.