Barclays Flags Structural Bond Reset With 4.65% Yield Call

59 mins ago

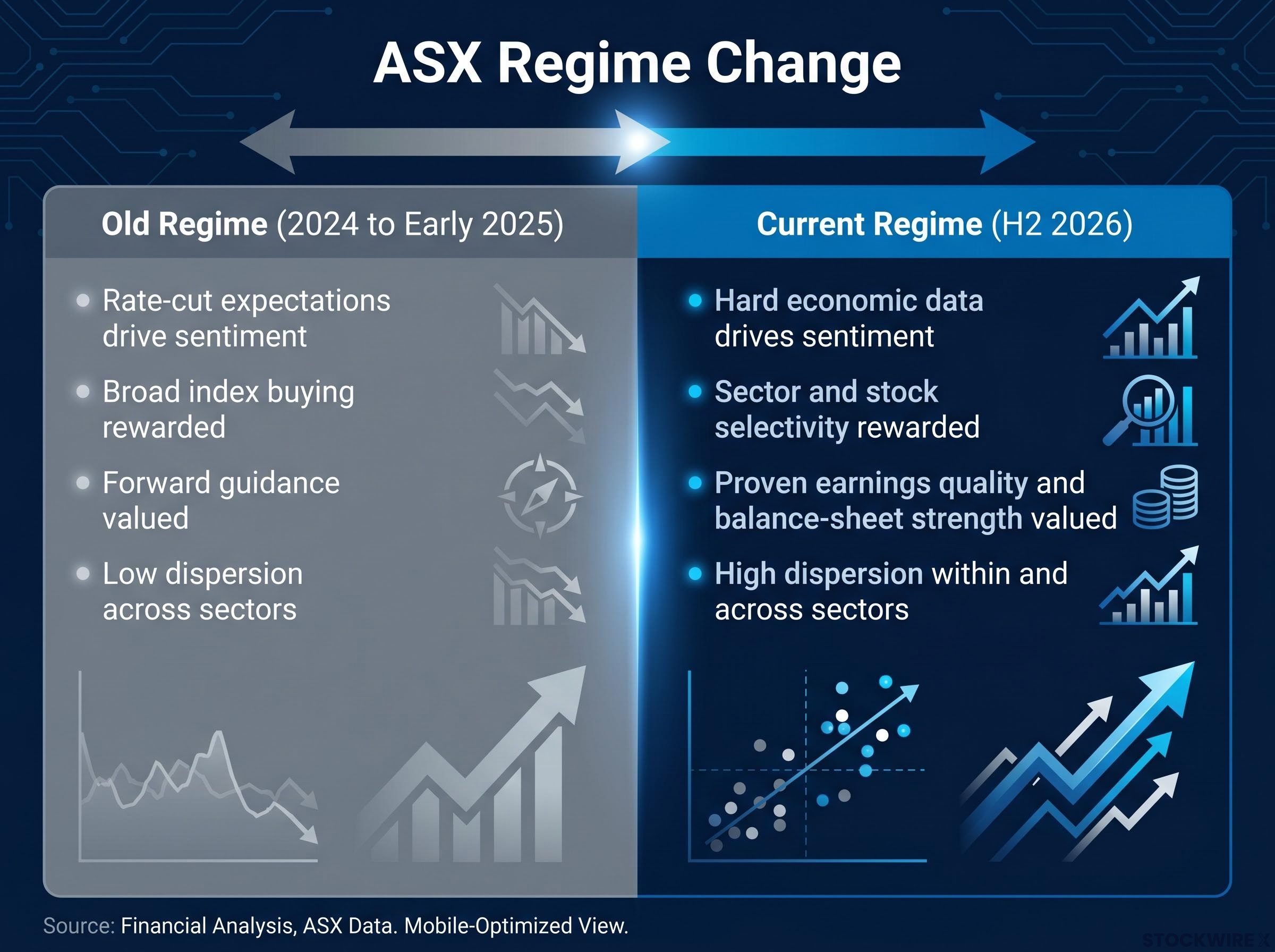

The rate-cut narrative that carried Australian equities through 2024 and into early 2025 is no longer available as a tailwind. That single fact reshapes how every sector on the ASX should be assessed for the second half of 2026.

This is not a bear market call. It is a regime change argument. The market has moved from pricing optimistic forward guidance to demanding hard evidence: visible disinflation, earnings resilience, and household financial stability. For investors who have not repositioned, the stakes are real, because the conditions that rewarded passive index exposure no longer apply.

This analysis tells you which sectors have the structural conditions to hold up and which face genuine headwinds, so you can assess whether your current exposure still fits the environment. Think of it as a practical reassessment tool covering the macro shift, the relative winners, the pressure zones, the resources question, and what evidence-based positioning actually looks like on the ASX right now.

Through 2024 and into early 2025, buying the index and waiting for rate cuts was a rational strategy. Monetary easing expectations underpinned sentiment. Risk-on positioning worked because the market was willing to pay up for the anticipated policy turn.

That trade has expired. The ASX now sits in an uncomfortable middle ground: rates still elevated, inflation sticky (particularly in services), and a labour market softening only gradually. This combination suppresses consumer demand and stresses leveraged balance sheets without triggering the aggressive RBA cuts that would resolve the tension.

Australia’s inflation surge reached 4.6% year-on-year in March 2026, driven by a 32.8% fuel price spike, a 25.4% electricity price surge, and accelerating construction costs, with the RBA’s own projections placing headline inflation above the 2-3% target band until end-2027.

A Vantage Markets senior analyst characterised the H2 2026 environment on 25 June 2026 as one where markets price hard economic evidence rather than forward-looking easing narratives. The market now requires three conditions to be clearly established before it will pay up: a sustained downward trend in inflation, demonstrated resilience in corporate earnings, and evidence that households are absorbing the financial squeeze without buckling.

Markets now price demonstrated, consistent economic data rather than hopeful forward guidance. The shift from narrative to evidence is not temporary noise; it is the regime.

Two scenarios define the range of plausible outcomes. On the constructive path, a steady decline in inflation allows the ASX to make incremental progress, supported by earnings delivery, dividend income, and pockets of sector strength. On the more difficult path, inflation that refuses to fall, bond yields that keep climbing, and weakening global risk appetite combine to force the market back into defensive mode. The absence of a clearly positive scenario in either case is precisely why broad index exposure has stopped being an adequate strategy.

The ASX sector rotation already underway as of June 2026 illustrates the dispersion argument concretely: beneath a near-flat ASX 200 close on 2 June, institutional capital rotated sharply out of domestic bank dividends and rate-sensitive defensives into globally exposed technology, base metals, and gold equities, with the Information Technology sub-index gaining 4.71% in a single session.

| Old Regime (2024 to Early 2025) | Current Regime (H2 2026) |

|---|---|

| Rate-cut expectations drive sentiment | Hard economic data drives sentiment |

| Broad index buying rewarded | Sector and stock selectivity rewarded |

| Forward guidance valued | Proven earnings quality and balance-sheet strength valued |

| Low dispersion across sectors | High dispersion within and across sectors |

What this means for you: the regime shift is not a temporary disruption waiting to revert. It is a durable change in what the market rewards, and your investment approach needs to reflect it. Every sector call that follows depends on understanding this shift first.

Banks and defensives are not exciting opportunities in H2 2026. They are the most structurally logical positions in a high-rate, slow-growth environment, and the distinction matters because the case for each comes with a clearly defined expiry condition.

The mechanism is straightforward. Sustained high rates support net interest margins, the difference between what banks earn on loans and pay on deposits. That margin support translates into relative earnings stability, provided the economic slowdown is gradual rather than sharp.

The risk is equally straightforward. According to Vantage Markets analysis, while the elevated rate environment continues to support bank earnings, the same conditions are creating a mounting burden for households, weighing on mortgage serviceability and limiting the scope for new credit growth. If household stress tips from manageable to acute, rising arrears and deteriorating loan book quality would undermine the earnings stability that justifies holding bank positions.

The indicators to watch: arrears data and household savings trends. These are the leading signals that tell you whether the banking thesis is holding or breaking down.

Healthcare names with solid domestic earnings, regulated utilities, and long-term infrastructure offer something scarce in this environment: earnings predictability that does not depend on a favourable macro turn.

The vulnerability is bond yield sensitivity. If yields rise further, the discount-rate effect compresses valuations on these long-duration assets even when underlying earnings are stable. Valuation discipline is not optional here; paying up for quality defensives in a rising yield environment can still deliver capital losses.

Key characteristics of relative winners in each category:

The relative-winner label is conditional. Before positioning around banks or defensives as portfolio anchors, you need to understand what data points would invalidate each thesis and monitor them actively.

The headwinds facing consumer stocks and property-linked equities are not a function of one bad quarter. They reflect structural conditions that will persist as long as household balance sheets remain stressed.

Australian households face a cumulative squeeze from three directions: elevated mortgage costs that have not eased despite rate-pause rhetoric, pandemic savings that have been substantially eroded, and living costs that continue to outpace felt wage gains. That triple pressure suppresses discretionary spending in a way that affects different business models very differently.

The most exposed consumer names share specific characteristics: highly leveraged, fixed-cost-heavy, reliant on stretched mortgage-holder customers, and operating with weak pricing power. Discretionary retail, travel and leisure, and casual dining sit squarely in this zone. Some business models, however, remain more defensible:

A-REITs (Australian Real Estate Investment Trusts, listed property funds) face a related but distinct set of headwinds. Sticky inflation keeps the risk skewed toward yield upside and valuation compression, and structural issues compound the rate sensitivity.

| A-REIT Sub-sector | Key Headwind | Outlook Characterisation |

|---|---|---|

| Office | Structural hybrid-work demand reduction | Persistent vacancy pressure; selective only |

| Retail | Ongoing e-commerce disruption | Footfall erosion continues; asset quality matters |

| Industrial/Logistics | Often priced richly after the reflation trade | Better fundamentals, but valuation discipline required |

For investors holding consumer or A-REIT exposure, the question is not whether conditions improve next quarter. It is whether the specific business models in your portfolio can withstand an extended period of household balance-sheet stress. Making differentiated assessments at the individual stock level is more productive than blanket sector exits.

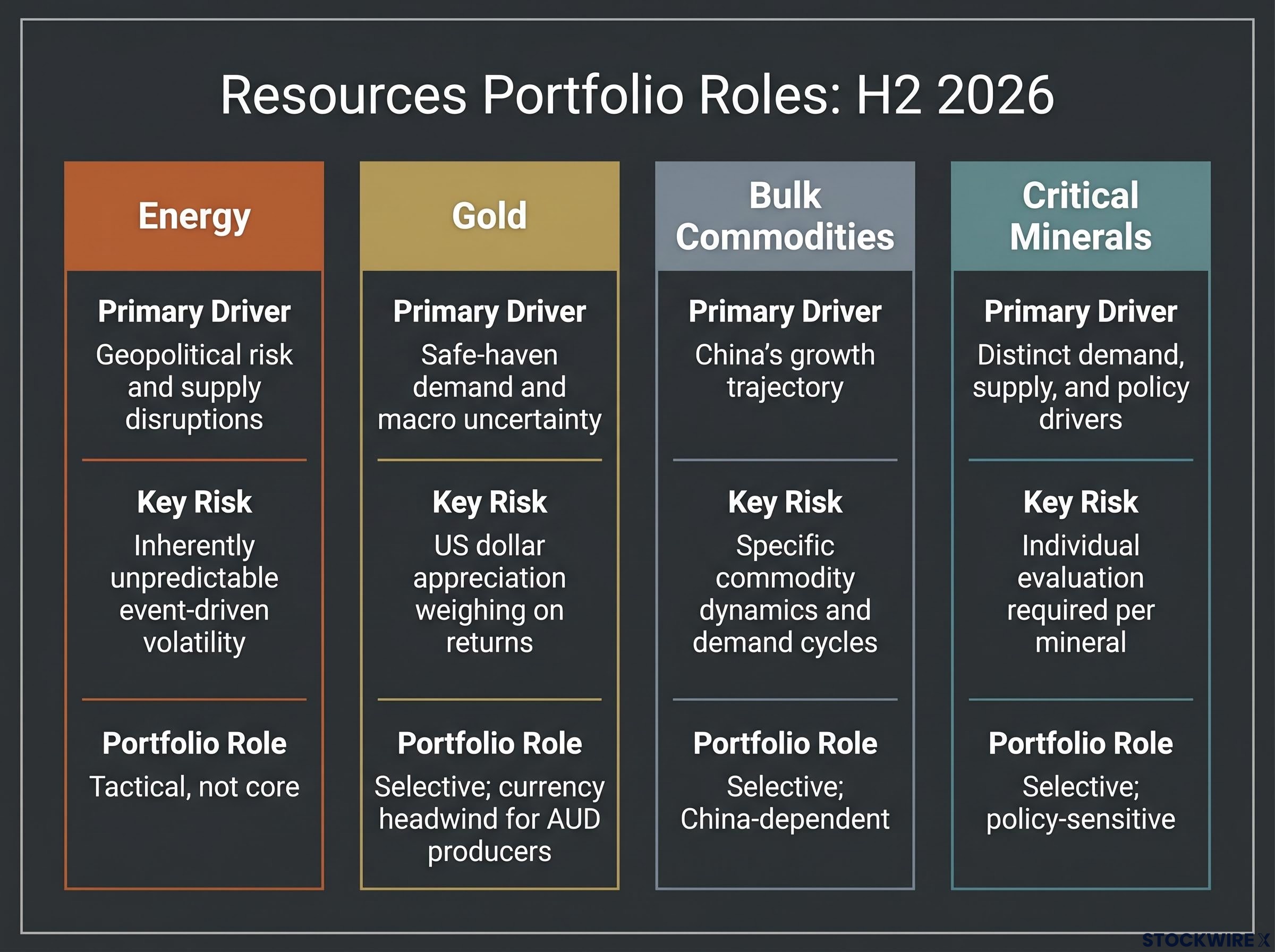

The research is explicit on this point: resources require bottom-up analysis rather than thematic basket exposure in H2 2026. The reason is that treating resources as a single category blends uncorrelated risks without providing the diversification benefit investors typically expect.

Each sub-sector has a different primary driver, a different risk profile, and a different role in portfolio construction.

| Sub-sector | Primary Driver | Key Risk | Portfolio Role (H2 2026) |

|---|---|---|---|

| Energy | Geopolitical risk and supply disruptions | Inherently unpredictable event-driven volatility | Tactical, not core |

| Gold | Safe-haven demand and macro uncertainty | US dollar appreciation weighing on returns | Selective; currency headwind for AUD producers |

| Bulk Commodities | China’s growth trajectory | Specific commodity dynamics and demand cycles | Selective; China-dependent |

| Critical Minerals | Distinct demand, supply, and policy drivers | Individual evaluation required per mineral | Selective; policy-sensitive |

According to Vantage Markets analysis, energy’s performance is anchored to geopolitical developments and supply-side shocks that are by nature difficult to forecast, which means it functions better as a tactical allocation than a core holding. Gold is contending with a firm US dollar; Australian producers, despite their costs being denominated in AUD, still face headwinds when the greenback appreciates against the commodities they sell. Bulk commodity returns hinge heavily on the direction of China’s economic activity. Critical minerals operate under a separate set of demand, supply, and policy variables that make each mineral its own distinct investment case.

An undifferentiated resources ETF or basket in H2 2026 does not give you broad commodity exposure. It gives you a mixture of geopolitical event risk, US dollar sensitivity, China cycle exposure, and policy-driven critical minerals plays, with no single macro call that validates all four simultaneously.

The actionable insight here is granularity. Knowing which resources sub-sector aligns with your specific macro view is considerably more valuable than knowing whether you are broadly bullish or bearish on resources.

Within the resources sub-sectors, lithium and critical minerals illustrate the stock-picker dynamic most clearly: in the week ending 1 May 2026, Liontown Resources gained 412.6%, Pilbara Minerals 314.86%, and Mineral Resources 209.42% from their 52-week lows, all while 22 ASX 200 constituents simultaneously hit fresh annual lows, confirming that undifferentiated exposure would have captured both extremes.

Moving from sector views to a positioning framework is where this analysis becomes something you can act on. Evidence-based investing in the H2 2026 context means prioritising proven earnings quality and balance-sheet strength over macro narratives, and tracking hard data rather than forward guidance.

Four categories of data now drive sector outcomes more than any macro narrative:

Each indicator connects back to the sector views. Rising arrears weaken the banking case. Sticky inflation prints extend the pressure on consumers and A-REITs. Deteriorating global sentiment affects resources sub-sectors unevenly, which is why the stock-picker’s market characterisation matters.

The five practical positioning principles drawn from the research:

This is not about making one big call. It is about building a portfolio that reflects the regime as it currently operates, and updating it as the data evolves.

The sector map for H2 2026 breaks into three distinct groupings:

The central challenge for Australian investors right now is this: broad optimism no longer provides lift. The market rewards proven earnings quality, balance-sheet strength, and sector-level differentiation, not thematic bets on a macro turn that may not arrive. Higher volatility and greater dispersion within and across sectors is a persistent feature of this environment, not a temporary aberration.

Investors still positioned for index-level gains from macro tailwinds are carrying risk they may not have priced. The adjustment required is not tactical trimming. It is a genuine update in what you expect to drive returns.

Looking ahead, two paths remain open. Where inflation retreats steadily, the ASX has room to advance through earnings delivery and dividend income. Where inflation proves stubborn, bond yields push higher, or global conditions deteriorate, the market will rotate back toward defensives sharply. Both paths are live possibilities, and that uncertainty is the strongest argument for selective, evidence-based positioning rather than a single directional bet.

Investors still assessing whether selective positioning outperforms passive exposure will find our full explainer on ASX stock performance versus the index details the 15-year dataset showing only 36% of the 210 largest ASX companies beat the ASX 300, and examines how cap-weighted index construction mechanically reduces exposure to deteriorating companies over time.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.

The ASX in H2 2026 is a regime where markets reward proven earnings quality and balance-sheet strength rather than rate-cut expectations. Broad index exposure has stopped being an adequate strategy as high dispersion across sectors means sector and stock selectivity now drives returns.

Banks and quality defensives such as healthcare, utilities, and infrastructure are the relative anchors in H2 2026, as sustained high rates support bank net interest margins and defensives offer earnings predictability independent of macro sentiment, though both come with clearly defined conditions that could invalidate the thesis.

Australian households face a triple squeeze from elevated mortgage costs, eroded pandemic savings, and living costs outpacing wage gains, which suppresses discretionary spending and keeps the risk skewed toward valuation compression for A-REITs through ongoing bond yield sensitivity.

Resources require bottom-up, stock-by-stock analysis rather than thematic basket exposure, because each sub-sector (energy, gold, bulk commodities, and critical minerals) has a different primary driver and risk profile, meaning no single macro call validates all four simultaneously.

The four indicators that matter most are inflation prints, RBA communications, household arrears and savings trends, and global risk sentiment, because each connects directly to the sector theses: rising arrears weaken the banking case, sticky inflation extends pressure on consumers and A-REITs, and deteriorating global sentiment hits resources sub-sectors unevenly.