ASX 200 Enters June 2026 With Stretched Valuations and Upside Risk

10 hrs ago

Australian investors are navigating one of the most complex macro environments in recent memory. Armed conflict stretching across multiple months, a sustained disruption to a critical global energy supply route, persistent inflation, and decelerating growth have converged to create conditions where the standard growth-tilted portfolio faces pressure from multiple directions simultaneously. In this environment, defensive sector allocations are not a novelty; they are a deliberate portfolio construction choice that becomes more consequential when risk factors compound rather than alternate. Consumer staples exchange-traded funds (ETFs) represent one of the few sector-level vehicles with a historical record of absorbing these conditions rather than amplifying them. The iShares Global Consumer Staples ETF (ASX: IXI) sits squarely in that category. What follows is a detailed assessment of what IXI owns, how it is built, what it has returned, what it costs, and whether it earns a place in a defensive Australian portfolio in the current environment.

The defensive case for consumer staples in 2026 does not rest on a single risk factor. It rests on four converging simultaneously, each reinforcing the others:

What makes this combination particularly hostile to conventional portfolios is that growth equities and fixed income face headwinds at the same time. Growth stocks suffer when rate expectations stay elevated; bonds suffer when inflation erodes real returns. The standard diversification playbook, where bonds offset equity drawdowns, loses effectiveness.

The breakdown of conventional safe haven assets during supply-driven stagflation is a direct consequence of bonds and equities facing simultaneous headwinds: when inflation erodes real bond returns at the same time that elevated rate expectations compress equity multiples, the negative stock-bond correlation that underpinned decades of portfolio construction effectively disappears.

Professional Australian commentary from outlets including Livewire Markets, Morningstar Australia, and the Australian Financial Review has consistently treated global consumer staples as inflation-resilient defensive allocations within this context. The reasoning is structural, not speculative: staples companies derive their defensive quality from pricing power and demand inelasticity, not simply from low volatility. That distinction matters when evaluating whether a defensive allocation is a short-term hedge or a durable portfolio construction choice.

Consumer staples are the goods people buy regardless of whether the economy is expanding or contracting. Food, beverages, household cleaning products, personal care items, alcohol, and tobacco all fall into this category. Demand for these products is structurally inelastic: consumers may delay purchasing a new car or cancel a holiday, but they do not stop buying groceries, toothpaste, or laundry detergent.

The contrast with cyclical sectors is instructive:

This distinction is what separates a defensive allocation from simply holding a low-volatility stock. Staples companies do not just fall less during downturns. They maintain revenue and, in many cases, grow earnings through pricing adjustments while cyclical peers face volume declines.

The logic of defensive investing is asymmetric: the mathematics of drawdown recovery mean a 50% loss requires a 100% subsequent gain to break even, which is why sectors with structural demand inelasticity attract capital during periods of elevated uncertainty even when their prospective returns look modest against growth alternatives.

When input costs rise, staples companies pass those increases through to consumers. Woolworths and Coles, as Australian examples, have demonstrated this repeatedly during the recent high-inflation period, adjusting shelf prices to protect margins without triggering meaningful volume loss.

This pricing power is not unlimited. Extreme or prolonged inflation can eventually compress volumes as consumers trade down to private-label alternatives or reduce basket sizes. The mechanism works within a range, and understanding that range is part of evaluating staples exposure honestly.

Historically, consumer staples have outperformed broader equity indices during prior high-inflation and recessionary periods. The same demand inelasticity that delivers this outperformance also limits upside during bull markets, when investors chase growth and cyclical leverage. That trade-off is the honest cost of the defensive quality.

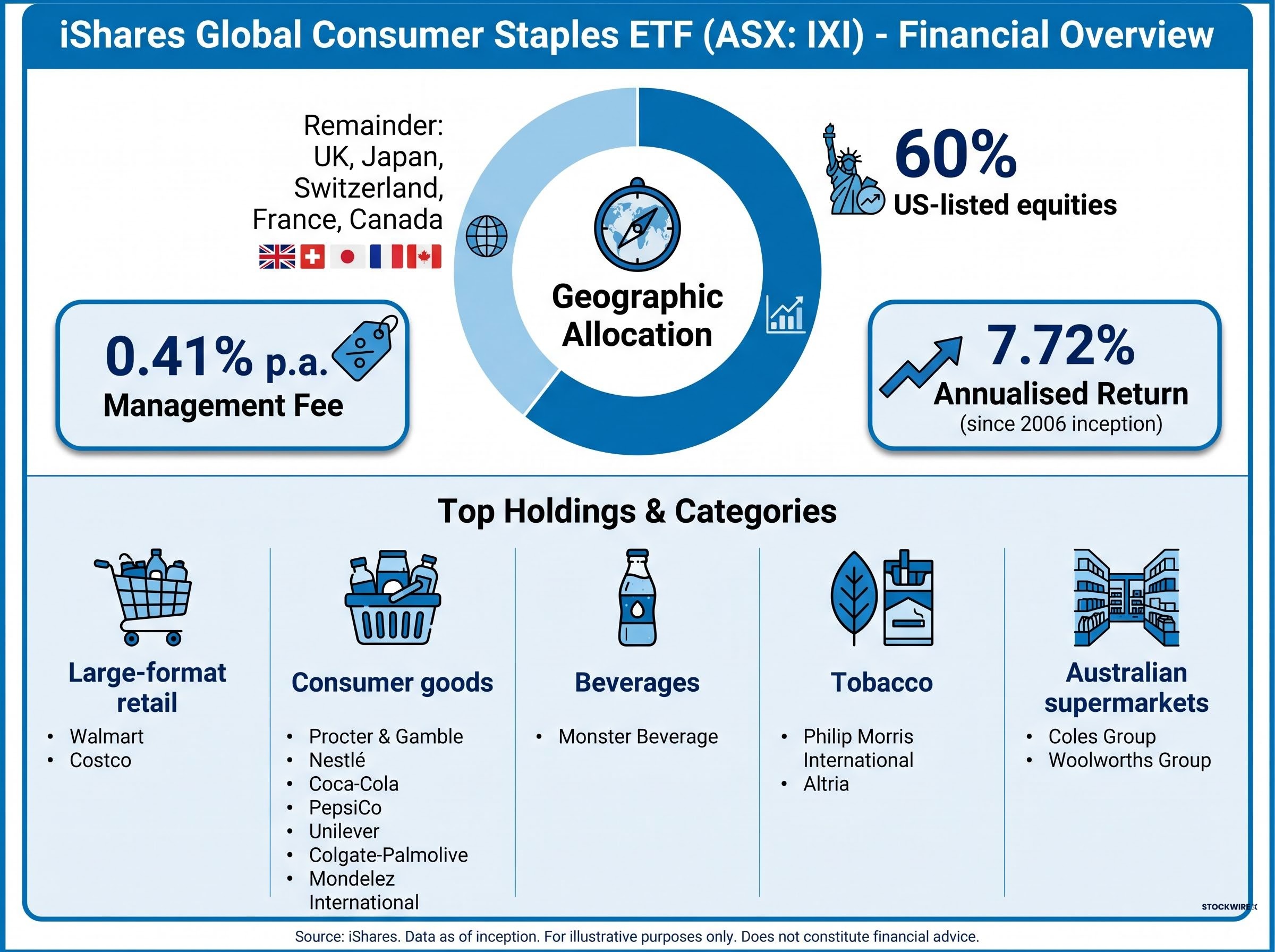

IXI is a CHESS-listed ETF that holds shares in leading global producers, distributors, and retailers of consumer staples products. Its geographic allocation is weighted approximately 60% toward US-listed equities, with the remainder distributed across the United Kingdom, Japan, Switzerland, France, Canada, and other markets.

The portfolio spans five distinct holding categories, each contributing a different dimension of the defensive profile:

| Category | Key Holdings | Geography |

|---|---|---|

| Large-format retail | Walmart, Costco | US |

| Consumer goods multinationals | Procter & Gamble, Nestlé, Coca-Cola, PepsiCo, Unilever, Colgate-Palmolive, Mondelez International | US, Switzerland, UK |

| Beverages | Monster Beverage | US |

| Tobacco | Philip Morris International, Altria | US |

| Australian supermarkets | Coles Group (ASX: COL), Woolworths Group (ASX: WOW) | Australia |

The inclusion of Coles and Woolworths alongside Walmart and Procter & Gamble illustrates how the fund layers global diversification over names Australian investors already know. The geographic spread means no single national economy’s consumer spending cycle dominates the return profile.

Management fee: 0.41% p.a. This fee is based on the most recent publicly available iShares product materials. Investors should verify the current fee against the latest iShares product disclosure statement (PDS) and any ASX announcements from BlackRock, as the most recent verifiable versions in public search results are pre-2025.

Annualised average return: 7.72% from inception in 2006 through to 30 April (reference year should be confirmed against the latest iShares performance disclosure).

That long-run figure anchors the performance picture, but it does not tell the full story. Over the past two to three years, global consumer staples have directionally underperformed broader equity indices, including the S&P 500, as risk appetite shifted and AI and technology mega-caps drove headline index returns. The rotation away from defensives during this period was well documented in late-2024 and early-2025 commentary from Reuters, the Financial Times, and Bloomberg.

For a 2026 buyer, that underperformance cycle carries three analytical implications:

Precise 2025-2026 return spreads between global consumer staples and the S&P 500 or ASX 200 require a data terminal or the latest iShares performance disclosures and cannot be quoted from available public search results. Current NAV, unit price, and assets under management (AUM) figures should be sourced from the latest iShares fact sheet or ASX product summary.

The underperformance does not invalidate the defensive thesis. It resets the entry price. For investors allocating to IXI as a defensive sleeve rather than a growth engine, the valuation context in 2026 is more favourable than it was when staples traded at peak multiples.

IXI fits most naturally in three investor profiles. Self-managed super fund (SMSF) holders seeking defensive income exposure will find the combination of demand-inelastic holdings and dividend yield relevant to pension-phase or near-pension portfolios. Investors de-risking later in the accumulation phase can use it to reduce portfolio beta without abandoning equity exposure entirely. And those with growth-heavy allocations, particularly concentrated in technology or resources, can deploy IXI as a low-correlation defensive sleeve.

The fund is less suited to early-accumulation investors with decades of runway who would sacrifice long-term compounding by allocating to a sector that structurally lags during bull markets. It is also less appropriate for investors who already hold significant direct positions in Coles (ASX: COL) or Woolworths (ASX: WOW), as the overlap would effectively double their defensive exposure in Australian supermarkets.

Two data points contextualise the Australian holdings. Coles holds approximately 28% of Australian food and grocery retail market share; Woolworths holds approximately 36%, according to Morningstar Australia. That duopoly structure underpins the non-cyclical demand thesis. Woolworths recently delivered a 12% single-day share price rally following upgraded guidance, highlighting earnings resilience within the defensive category. Morningstar Australia currently frames Coles as underperforming Woolworths operationally while remaining entrenched in the duopoly structure, a nuance for investors assessing the relative strength of IXI’s Australian component.

The AUD’s move from approximately 0.6777 in January 2026 to around 0.7153 by mid-to-late April 2026 created a measurable performance gap between hedged and unhedged international ETF strategies, with hedged products outperforming on a year-to-date basis, a dynamic that is directly relevant to evaluating whether IXI’s unhedged US equity exposure enhances or dilutes the defensive objective for a given investor.

The ASX product page for IXI provides access to the current Product Disclosure Statement dated March 2026, which is the authoritative source for verifying the management fee, fund structure, and any updates BlackRock has filed since earlier publicly searchable disclosures.

IXI offers genuine portfolio resilience through demand-inelastic holdings, geographic diversification across six or more national markets, a 19-year return track record averaging 7.72% annualised, and a fee structure that is competitive for global sector exposure. The income and diversification benefits complement the defensive objective rather than substituting for it.

The honest limits are equally clear. Consumer staples are not recession-proof in an absolute sense. Pricing power has a ceiling under severe demand compression, and the recent underperformance cycle against growth indices represents a real opportunity cost for younger, longer-horizon investors who would have been better served by broader market exposure over that specific period.

The 2026 environment is one where those trade-offs tilt more favourably toward a defensive allocation than usual. The convergence of geopolitical, inflationary, and growth-slowdown pressures creates conditions where the downside protection staples offer is more likely to be tested, and more likely to prove its worth.

All current product data, including the management fee, NAV, and performance figures, should be verified against the latest iShares disclosure before making any allocation decision.

For investors wanting to understand the structural context that makes a defensive sector sleeve like IXI more relevant now than it was five years ago, our full explainer on portfolio resilience beyond the 60/40 framework examines how the stock-bond correlation has turned persistently positive during inflation shocks in 2022, 2025, and 2026, and walks through a three-tier adaptive portfolio structure that individual investors can use as a practical alternative.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The iShares Global Consumer Staples ETF (ASX: IXI) is a CHESS-listed ETF that holds shares in leading global producers, distributors, and retailers of consumer staples products, with approximately 60% allocated to US-listed equities and the remainder spread across the UK, Japan, Switzerland, France, Canada, and other markets.

The management fee for IXI is 0.41% per annum based on the most recent publicly available iShares product materials, though investors should verify this figure against the latest iShares Product Disclosure Statement and any ASX announcements from BlackRock before making an allocation decision.

IXI holds major consumer staples names including Walmart, Costco, Procter and Gamble, Nestle, Coca-Cola, PepsiCo, Unilever, Colgate-Palmolive, Philip Morris International, Altria, and Australian supermarkets Coles Group (ASX: COL) and Woolworths Group (ASX: WOW).

IXI has delivered an annualised average return of 7.72% from its inception in 2006 through to 30 April, though over the past two to three years global consumer staples have directionally underperformed broader equity indices as risk appetite shifted toward technology and AI mega-caps.

Because approximately 60% of IXI's portfolio is in US-listed equities and the fund is unhedged, movements in the AUD/USD exchange rate will directly influence returns for Australian investors, meaning a rising Australian dollar can reduce the value of offshore gains when converted back to AUD.