ASX 200 Enters June 2026 With Stretched Valuations and Upside Risk

10 hrs ago

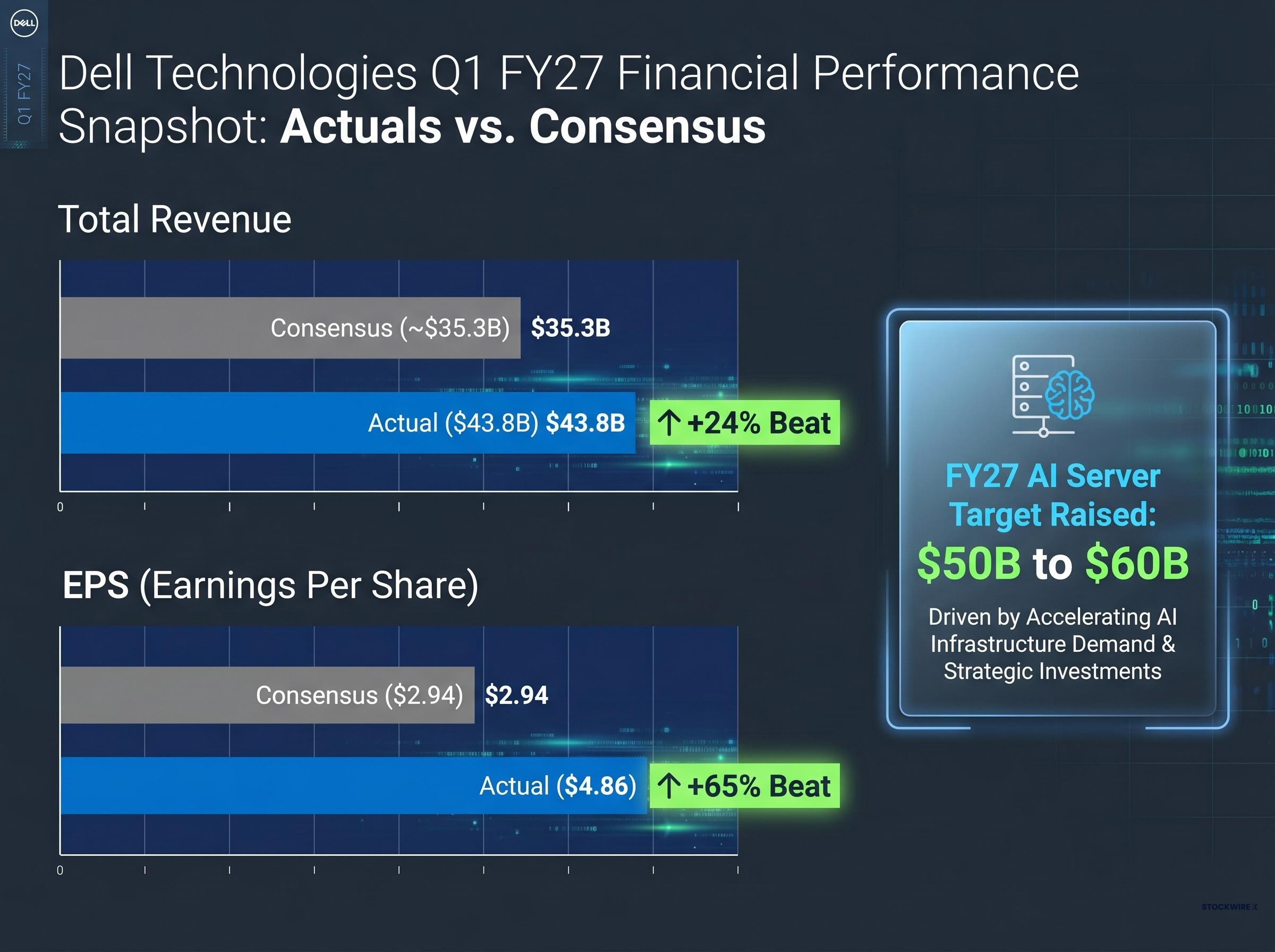

On 28 May 2026, Dell Technologies reported $43.8 billion in quarterly revenue, an 88% surge from the same period a year earlier and 24% above analyst consensus estimates. The stock rose 32.7% in the following session. That single earnings release landed as the Philadelphia Semiconductor Index (SOX) tracked toward its strongest quarter on record, as downside hedging costs across the chip sector fell to their lowest level since early 2025, and as AI infrastructure spending commitments from the world’s largest cloud operators continued to expand. The signal from Dell’s quarter is unusually clear. What investors should do with it is less straightforward.

What follows is an examination of what Dell’s numbers reveal about the pace and durability of the AI infrastructure buildout, how to read the broader semiconductor market indicators alongside them, and what framework investors can apply to distinguish genuine demand signals from cycle risk.

A 65% earnings-per-share beat at a company with a $43.8 billion revenue quarter is not a forecasting error. It is a signal that the consensus model itself was not calibrated to the speed at which AI infrastructure procurement is moving. When the gap between what analysts expected and what a company delivered is this wide, the problem is not the company’s quarter; it is the assumptions underpinning every AI-adjacent estimate in the market.

“$4.86 actual versus $2.94 consensus, a 65% beat at one of the world’s largest technology hardware companies.”

| Metric | Consensus Estimate | Q1 FY27 Actual | Beat |

|---|---|---|---|

| Total Revenue | ~$35.3B | $43.8B | ~24% |

| Non-GAAP Diluted EPS | $2.94 | $4.86 | ~65% |

| AI Server Revenue | N/A | $16.1B | N/A |

Management raised its full-year FY27 AI server revenue target from $50 billion to $60 billion. Given the order-to-revenue conversion already visible in the quarter, that revised target looks more like a conservative floor than an aspirational stretch.

The distinction between recognised revenue and order bookings tells investors where the demand pipeline actually sits. Dell recognised $16.1 billion in AI server revenue during Q1 FY27, but booked $24.4 billion in AI-related orders. The $8.3 billion gap between those two figures is not a vanity metric. It is contracted future revenue, already committed by customers, waiting to convert. That backlog functions as a leading indicator of quarters to come, and its scale suggests the current run rate has room to accelerate before it plateaus.

The SOX closed at 12,829.38 on 29 May 2026. That number sits within a quarterly trajectory that, according to Bloomberg and the Financial Times, is on track to be the strongest on record. The question is what that trajectory tells investors about risk rather than just about returns.

The session that followed Dell’s earnings release was itself a market event: all four major US benchmarks closed at simultaneous record highs on 29 May 2026, with Snowflake’s 34% product revenue growth providing a second enterprise AI data point that reinforced rather than contradicted the demand signal Dell had just delivered.

Four indicators, taken together, paint a picture of a market that is simultaneously very confident and largely unprotected:

The cost of protecting against a selloff in chip stocks fell to its lowest level since early 2025, according to Bloomberg data.

The decline in hedging costs alongside elevated bullish options positioning suggests that downside protection is being abandoned precisely when exposure is at its highest. The short-squeeze dynamic, where heavily shorted names rally as bears are forced to cover, indicates that momentum rather than fundamental repricing is driving marginal prices on the sector’s weaker names. For investors considering new positions, the AI infrastructure trade has moved from early-adopter conviction to consensus, and that shift changes the risk profile even if the underlying demand remains genuine.

AI infrastructure investment refers to the physical and systems layer, including servers, networking equipment, memory chips, and data centre capacity, that must be in place before AI workloads can operate at commercial scale. Without this layer, the software models that generate headlines have nowhere to run.

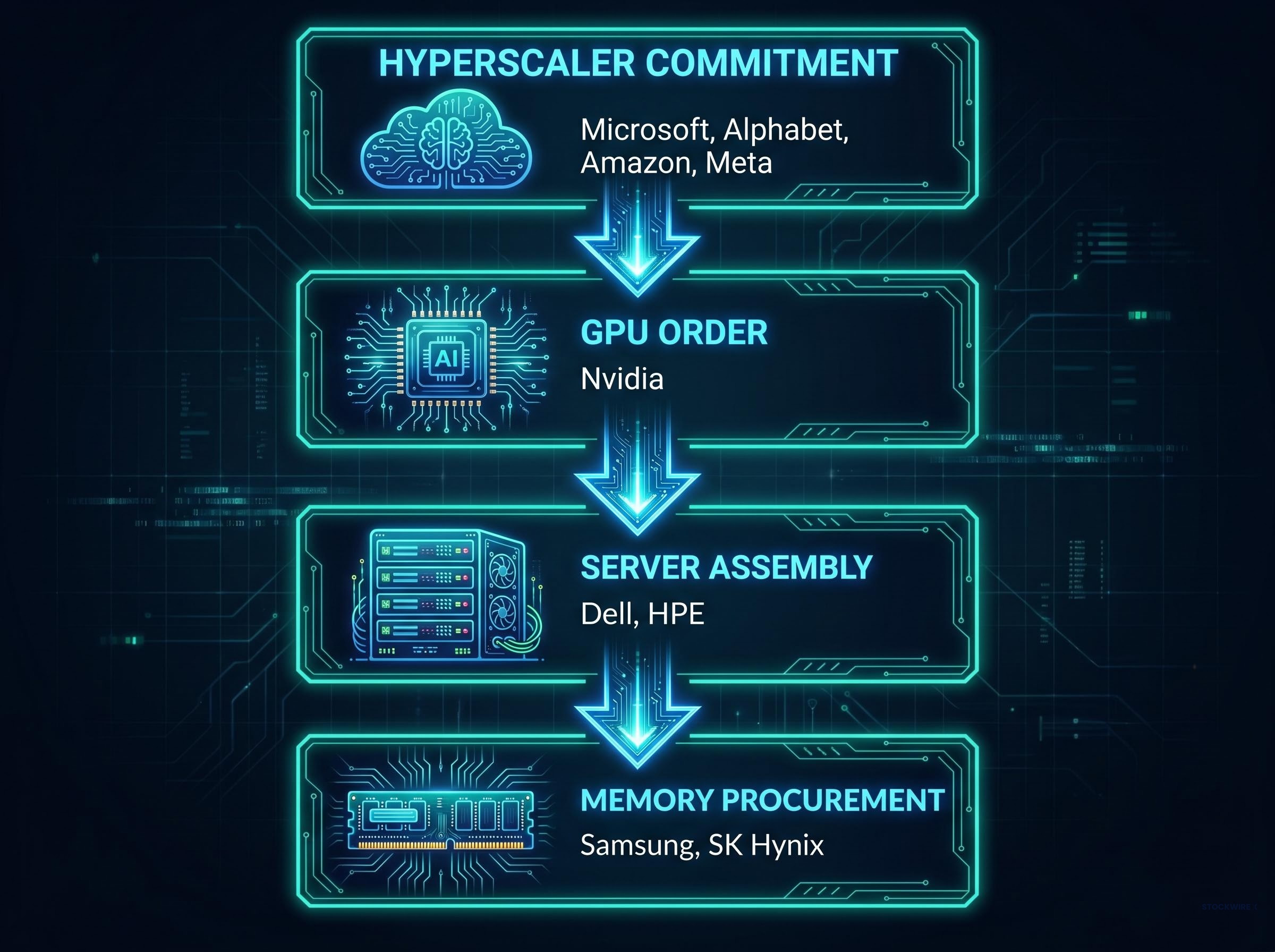

The procurement chain that connects a hyperscaler’s compute ambition to a server on Dell’s order books follows a specific sequence:

Training a large AI model is a capital-intensive but infrequent event; a company builds or rents a cluster, trains the model, and the peak compute demand subsides. Inference, the process of running a trained model to serve predictions to users, is continuous and scales with adoption. Every new user, every new application built on a foundation model, adds incremental inference compute demand.

This distinction matters because it creates a more sustained capex requirement than prior infrastructure cycles. The 1990s telecom fibre rollout, for example, was largely a one-time physical buildout. AI inference demand, by contrast, grows as adoption grows. Analysts watching utilisation rates alongside capex commitments are measuring the right variable: not just how much is being built, but how much of what has been built is being consumed.

The scale of hyperscaler capex commitments, with Amazon, Microsoft, Alphabet, and Meta collectively spending $130 billion in Q1 2026 alone against a full-year 2026 combined guidance of approximately $725 billion, is the upstream force that converts Dell’s order backlog from a company-specific metric into a sector-wide demand signal.

The demand case rests on specifics that are difficult to dismiss. $24.4 billion in order bookings from a hardware company in a single quarter is not speculative sentiment. Those are purchase orders, signed by counterparties, with delivery timelines attached. Dell’s guidance raise from $50 billion to $60 billion in FY27 AI server revenue is management telling the market that the forward pipeline supports a higher baseline.

The counterweight is not that AI demand is fabricated. It is that the current price of AI infrastructure exposure may already discount several years of growth, leaving limited margin for execution shortfalls, capex pauses, or utilisation disappointments.

The semiconductor bubble narrative has attracted rigorous pushback from institutional analysts, with Bank of America’s Savita Subramanian citing record free cash flow yields, earnings revisions above 20%, and active long-only overweight positioning at roughly half the 2017 cycle peak as three data points that collectively undercut the speculative excess characterisation.

Chip sector bubble risk analysis circulating in late May 2026 points to HBM memory as the clearest flashpoint: names with the highest concentration of AI-driven demand have also attracted the most crowded positioning, meaning any revision to hyperscaler capex timelines would be amplified through a simultaneous unwind of momentum trades built on top of the underlying fundamental case.

| Demand Signal | Risk Indicator |

|---|---|

| $24.4B in AI order bookings (Q1 FY27) | SOX on track for strongest quarter on record |

| $16.1B in recognised AI server revenue | Downside hedging costs at lowest since early 2025 |

| FY27 AI server target raised to $60B | Most-shorted names up as much as 30% |

| All four major hyperscalers confirming rising AI capex | Elevated bullish options positioning across chip sector |

The core risk is not that AI demand is speculative. It is that the current price of AI infrastructure exposure may already reflect several years of growth, leaving little room for any shortfall in execution or spending pace.

The gap between $16.1 billion in recognised revenue and $24.4 billion in bookings also carries a realisation risk. That backlog needs to convert. If hyperscaler capex budgets tighten or delivery timelines extend, the recognised revenue figure in future quarters may not match the implied pace of the current backlog. For investors already holding AI infrastructure positions, the honest assessment is that a portion of their return now reflects momentum dynamics rather than incremental fundamental insight.

Rather than arriving at a single verdict on whether AI infrastructure stocks are overvalued or undervalued, investors can apply a three-dimensional evaluation lens to individual positions:

Applying all three to Dell: demand durability appears strong on the basis of a $24.4 billion backlog and a raised $60 billion FY27 target. Positioning risk is elevated given the broader semiconductor index trajectory. Cycle position is mid-chain; Dell assembles what Nvidia and memory suppliers provide, capturing volume but not necessarily the bottleneck premium.

The most important forward-looking data for this thesis arrives quarterly. When Microsoft, Alphabet, Amazon, and Meta report earnings, investors should monitor three specific variables: the direction of capex guidance revisions (still rising, flattening, or pulling back), management commentary on AI workload utilisation rates, and any language suggesting infrastructure overcapacity or delayed deployment timelines. A single quarter where two or more hyperscalers signal a capex pause would materially alter the demand assumptions underpinning the entire procurement chain.

Dell’s $43.8 billion revenue quarter and $60 billion FY27 AI server guidance are the clearest real-world evidence to date that AI infrastructure demand is large, accelerating, and backed by contracted orders rather than projections. The thesis is not in question. What is in question is whether the current price of that thesis, reflected in a SOX approaching its strongest quarter ever, leaves room for investors entering new positions to generate returns that compensate for the cycle and positioning risks now embedded in valuations.

In a market where the AI infrastructure thesis is consensus, the investor question is not whether demand is real. It is where the next mispricing sits.

The answer may lie in parts of the procurement chain that have not yet reached record valuations: memory suppliers navigating concentration-driven selling, networking equipment providers enabling data centre interconnects, and power infrastructure companies supporting the energy demands of inference-scale compute. For investors who have already captured the most visible part of the AI buildout, the differentiated opportunity increasingly sits one layer deeper in the supply chain.

The AI infrastructure supply chain one layer deeper than Dell and Nvidia includes power generation names like Bloom Energy, which reported 130% revenue growth in Q1 2026 and reached profitability after roughly 25 years of losses, and optical networking suppliers like Lumentum, which posted 90% revenue growth and identified co-packaged optics as a forward growth catalyst, two categories that have materially outpaced the Nasdaq-100 year-to-date.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AI infrastructure investment refers to the physical and systems layer, including servers, networking equipment, memory chips, and data centre capacity, required to run AI workloads at commercial scale. It matters for stock markets because the scale of procurement from major cloud operators is directly driving revenue growth at hardware companies like Dell and chip suppliers like Nvidia.

Dell reported $43.8 billion in quarterly revenue, 24% above analyst consensus estimates, and non-GAAP diluted EPS of $4.86 against a $2.94 consensus, a 65% beat. The company also booked $24.4 billion in AI-related orders during the quarter and raised its full-year FY27 AI server revenue target from $50 billion to $60 billion.

AI training is a capital-intensive but infrequent event where compute demand subsides once a model is built, while AI inference is continuous and scales with every new user or application built on a foundation model. Inference demand creates a more sustained capex requirement than prior infrastructure cycles, which strengthens the long-term case for hardware suppliers.

Investors can examine order backlogs as a verification mechanism: Dell's $24.4 billion in AI order bookings represents contracted future revenue rather than speculative sentiment. However, the article notes that collapsing hedging costs, near-record SOX levels, and heavy short squeezes in chip names indicate that momentum is also playing a significant role in marginal pricing.

The article identifies memory suppliers, optical networking providers, and power infrastructure companies as categories that have not yet reached the same valuation levels as the most visible AI names. Examples cited include Bloom Energy, which reported 130% revenue growth in Q1 2026, and Lumentum, which posted 90% revenue growth driven by optical networking demand.