Space Economy Set to Triple: an Analytical Framework for Investors

25 mins ago

Despite Westminster’s anticipation of a sudden £300 million infrastructure injection this week, the reality of the AstraZeneca UK investment strategy remains firmly anchored in domestic reduction. The pharmaceutical firm has maintained its previously announced pullbacks, casting a shadow over the government’s recently finalised United States and United Kingdom pricing agreement. This stark contrast highlights the growing disconnect between domestic policy ambition and multinational capital allocation.

Against the backdrop of sweeping April 2026 Medicines and Healthcare products Regulatory Agency (MHRA) reforms, political leaders had hoped to see a reinstatement of abandoned projects. Instead, corporate capital continues to flow heavily towards international markets.

This analysis breaks down the true state of domestic research facilities and the political positioning attempting to secure them. It examines what the latest first-quarter financial results reveal about the company’s broader global trajectory, separating political optimism from hard capital commitments.

An examination of domestic infrastructure reveals a stark geographical reality for British life sciences. While rumours circulated regarding a £300 million domestic package announced this week, corporate capital remains largely frozen across key regional research hubs. The expected reinstatement of these projects has not materialised, leaving local economies to absorb the lost infrastructural upgrades.

A review of the three primary development sites clarifies the current state of corporate capital deployment.

Macclesfield: Speculation regarding a £100 million advanced digital testing facility remains entirely unconfirmed, with no active corporate plans in place. Cambridge: The broader £200 million expansion of the life sciences campus remains paused, delaying 1,000 anticipated employment opportunities, though standalone construction on the Rosalind Franklin Building continues independently. * Speke: The previously abandoned £450 million immunisation production plant in Merseyside remains permanently cancelled following reduced government incentive offers.

Readers tracking corporate capital flows can see a clear pattern of domestic restraint. The lack of revitalisation in these hubs underscores the severity of the ongoing industry friction.

Domestic regulatory speed dictates corporate willingness to build local infrastructure. When a government accelerates therapeutic valuation and patient accessibility, pharmaceutical companies can forecast faster returns, making local manufacturing plants commercially viable. This fundamental relationship drove the government’s coordinated political effort to repair the domestic operating climate.

Policymakers implemented sweeping changes to the MHRA effective April 28, 2026. These reforms establish new targets to accelerate patient access to new medicines by up to six months. Concurrently, the publication of the bilateral US-UK agreement on pharmaceutical pricing on April 2, 2026, committed the National Health Service (NHS) to material medicine pricing increases.

The official US-UK pharmaceutical partnership details outline specific changes to medicine access alongside a crucial cap on the VPAG rebate, demonstrating the exact financial concessions the government is willing to make to retain life sciences capital.

Government Strategy Direction The new regulatory framework aims to position British life sciences as a pillar of economic strength, directly addressing the reimbursement frameworks that previously deterred infrastructure development.

Despite the authorisation of novel medical treatments by regulatory authorities since the start of 2026, AstraZeneca leadership maintains threats to halt further investments over ongoing NHS pricing rows.

The new clinical trial processes remove administrative bottlenecks that traditionally delayed medicine approvals. By streamlining data review phases, regulatory bodies can issue decisions significantly faster.

Faster patient access directly improves the commercial viability of domestic research centres. When treatments reach the market six months earlier, the extended patent exclusivity period generates substantial revenue, theoretically justifying the enormous upfront capital required for physical infrastructure.

The latest earnings reports demonstrate that global commercial momentum easily finances corporate expansion, regardless of domestic infrastructure friction. Released on April 29, 2026, the first-quarter data from major pharmaceutical players illustrates profound corporate strength driven by specialised therapeutic divisions. The figures reveal a sector heavily reliant on international market penetration rather than local government incentives.

AstraZeneca delivered a strong performance, posting a first-quarter revenue of $15.29 billion and comfortably beating market expectations of $14.74 billion. Analysts reacted positively to the print, noting that the expansion was heavily driven by expansion in the company’s oncology division and growth in uncommon medical conditions. This global success provides the financial flexibility to bypass unfavourable domestic operating environments.

Meanwhile, GSK presented a more mixed commercial picture. Overall commercial receipts landed at £7.6 billion (approximately $10.10 billion), missing the $10.42 billion expectation target. However, the company’s core operating profit reached £2.65 billion, representing a 10% year-over-year increase.

Specific product lines anchored this profitability. According to company data, the company’s oncology segment, featuring the therapeutic treatment Jemperli, surged by 28%, while the Shingrix product line surpassed £1 billion in returns.

| Company | Total Revenue (Q1 2026) | Expectation Target | Key Growth Driver |

|---|---|---|---|

| AstraZeneca | $15.29 billion | $14.74 billion | Oncology and pipeline momentum |

| GSK | £7.6 billion ($10.10 billion) | $10.42 billion | Specialty medicines portfolio |

Investors tracking these two primary British pharmaceutical firms can see a clear divergence in quarterly delivery. Both entities continue to demonstrate the profitability of focusing on high-margin disease categories over regional facility expansion.

For investors wanting to explore how emerging cancer treatments navigate clinical approval, our detailed coverage of targeted oncology regulatory pathways examines recent FDA feedback on first-in-human trial designs for radioligand therapies.

While the UK government views the newly implemented regulatory reforms as a domestic policy victory, multinational capital allocation tells a different story. The scale of domestic investment propositions is completely overshadowed by massive international expansions. Corporate spokespeople have openly noted an ongoing reassessment of European investment needs, reflecting deep industry frustration with the region’s commercial viability.

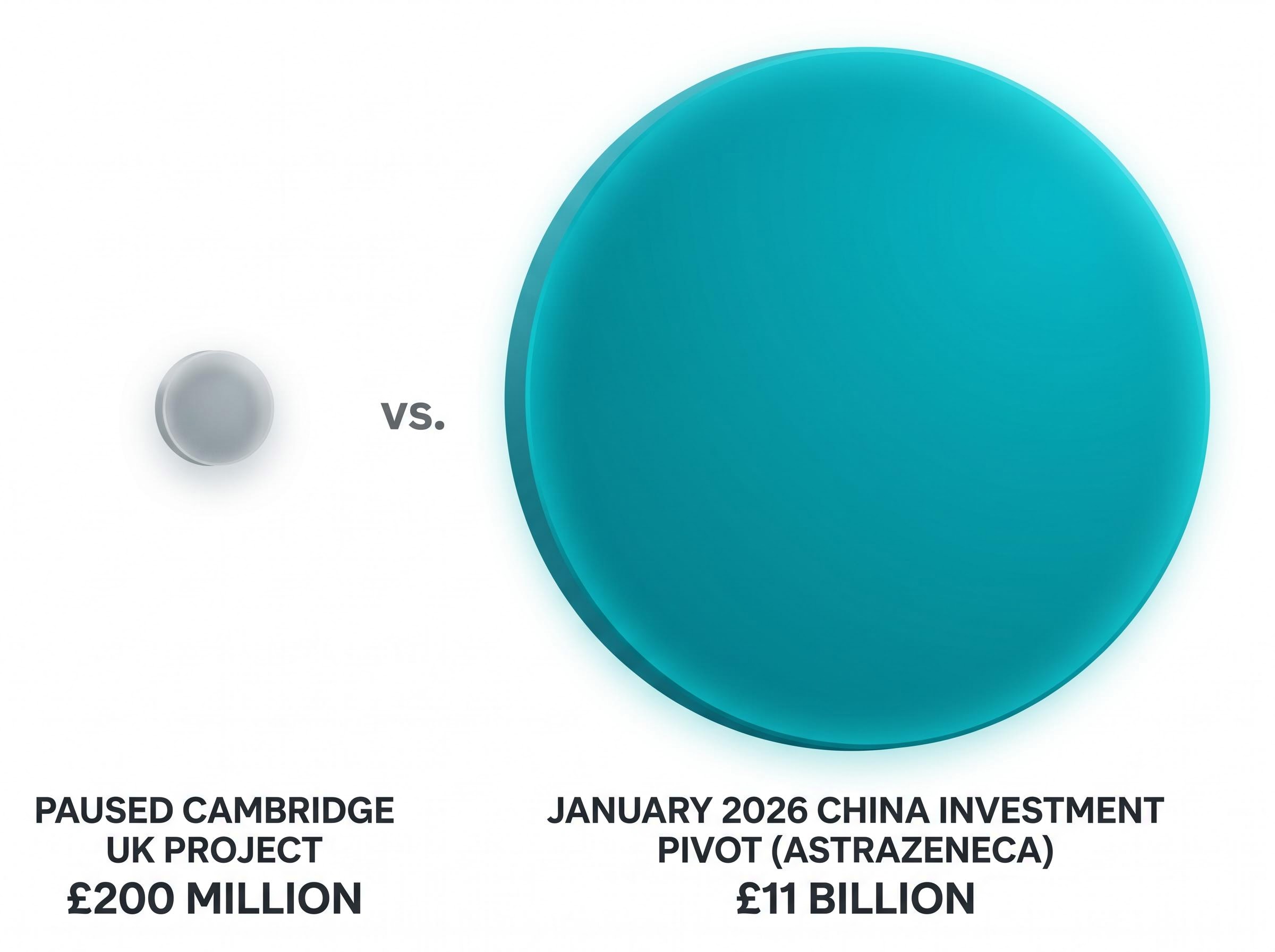

This reality was cemented in January 2026, when AstraZeneca announced a massive £11 billion investment pivot toward China. The sheer size of this capital deployment illustrates the true competitive environment for life sciences funding. When compared to the paused £200 million Cambridge project, the Asian expansion highlights how quickly corporate leadership will redirect funds toward more welcoming regulatory and pricing structures.

The sheer scale of this £11 billion investment in China effectively dwarfs the paused domestic projects in Merseyside and Cambridge, showcasing the immediate financial consequences of regional market friction.

The global operating environment remains complex, with domestic competitors facing distinct market headwinds abroad. Complex political and social factors, specifically immunisation hesitancy under the Donald Trump administration, continually impact the uptake of preventative products for GSK in the United States.

These international market pressures directly influence corporate reliance on emerging markets. When traditional Western jurisdictions present regulatory friction or pricing resistance, major pharmaceutical firms inevitably accelerate their capital deployment into Asian and alternative global hubs.

The intersection of first-quarter financial success and the newly active MHRA reforms defines the current state of the sector. Despite the government’s accelerated clinical trial processes, the continued absence of a £300 million infrastructure reversal underscores the lingering vulnerabilities in the domestic market. The permanent cancellation of the £450 million Merseyside facility remains a stark reminder of how rapidly corporate capital can exit.

When global regulatory bodies facilitate rapid phase III trial enrolment, pharmaceutical companies can reach commercialisation faster, making the choice of jurisdiction a critical competitive advantage.

Looking forward, the sector will likely demand substantially firmer policy guarantees regarding NHS pricing structures before committing to future manufacturing plants. Until those commercial frameworks align with international competitors, global revenue growth will continue to finance overseas expansion rather than local infrastructure.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AstraZeneca's previously announced UK projects, including facilities in Macclesfield, Cambridge, and Speke, remain unconfirmed, paused, or permanently cancelled despite government anticipation of new investments.

The April 2026 MHRA reforms aim to accelerate patient access to new medicines by up to six months and increase NHS medicine pricing, intending to make domestic manufacturing more commercially viable for pharmaceutical firms.

AstraZeneca's strong Q1 2026 revenue of $15.29 billion, driven by oncology, indicates robust global commercial momentum that allows the company to prioritize international expansions, such as its £11 billion investment in China, over some domestic UK projects.

AstraZeneca is prioritizing international markets, notably China, due to what it perceives as more welcoming regulatory and pricing structures compared to ongoing NHS pricing rows and domestic operating environment friction in the UK.