Barclays Flags Structural Bond Reset With 4.65% Yield Call

53 mins ago

Most investors expect bad news on results day. Confession season means the bad news is already arriving, weeks before the July-August reporting season, and this year the volume is unlike anything in recent memory.

It is late June 2026, and companies across nearly every ASX sector outside mining and energy have issued trading updates, guidance cuts, or profit warnings since early May. By late March 2026, a shared threshold had been crossed, with trading conditions turning across multiple sectors at roughly the same moment. UBS is expecting further downgrades, which means the wave is not yet over.

Here is what the pattern actually tells you: why so many ASX stocks are falling ahead of results, which sectors are absorbing the most damage and which are holding up, and how to use confession season as strategic preparation rather than a source of reactive anxiety. The difference between an investor who reads the confessions and one who merely reacts to them is the difference between preparation and surprise.

Confession season is the pre-earnings window when ASX-listed companies must update the market if results will materially miss prior guidance or consensus. Rather than waiting for results day, they disclose early through one of three mechanisms:

In a typical year, only a minority of companies issue these updates because most are tracking roughly in line with expectations. The 2026 season breaks that pattern. The sheer number of confessions, concentrated in May and June, signals something beyond individual company problems.

The obligation behind these disclosures is not voluntary. ASX Listing Rule 3.1 requires companies to disclose material information immediately once they become aware of it. A profit warning is a compliance action, not an editorial choice.

The obligation is not discretionary: continuous disclosure obligations require companies to act the moment material information is known internally, not after board sign-off or legal review, which is why a cluster of profit warnings in a short window reflects macro conditions landing simultaneously rather than companies choosing to confess.

That reframing matters. When you see five, ten, or fifteen companies confessing in a six-week window, you are not watching a parade of mismanagement. You are watching the macro environment land on multiple businesses at once, and the disclosure rules ensuring you hear about it in real time.

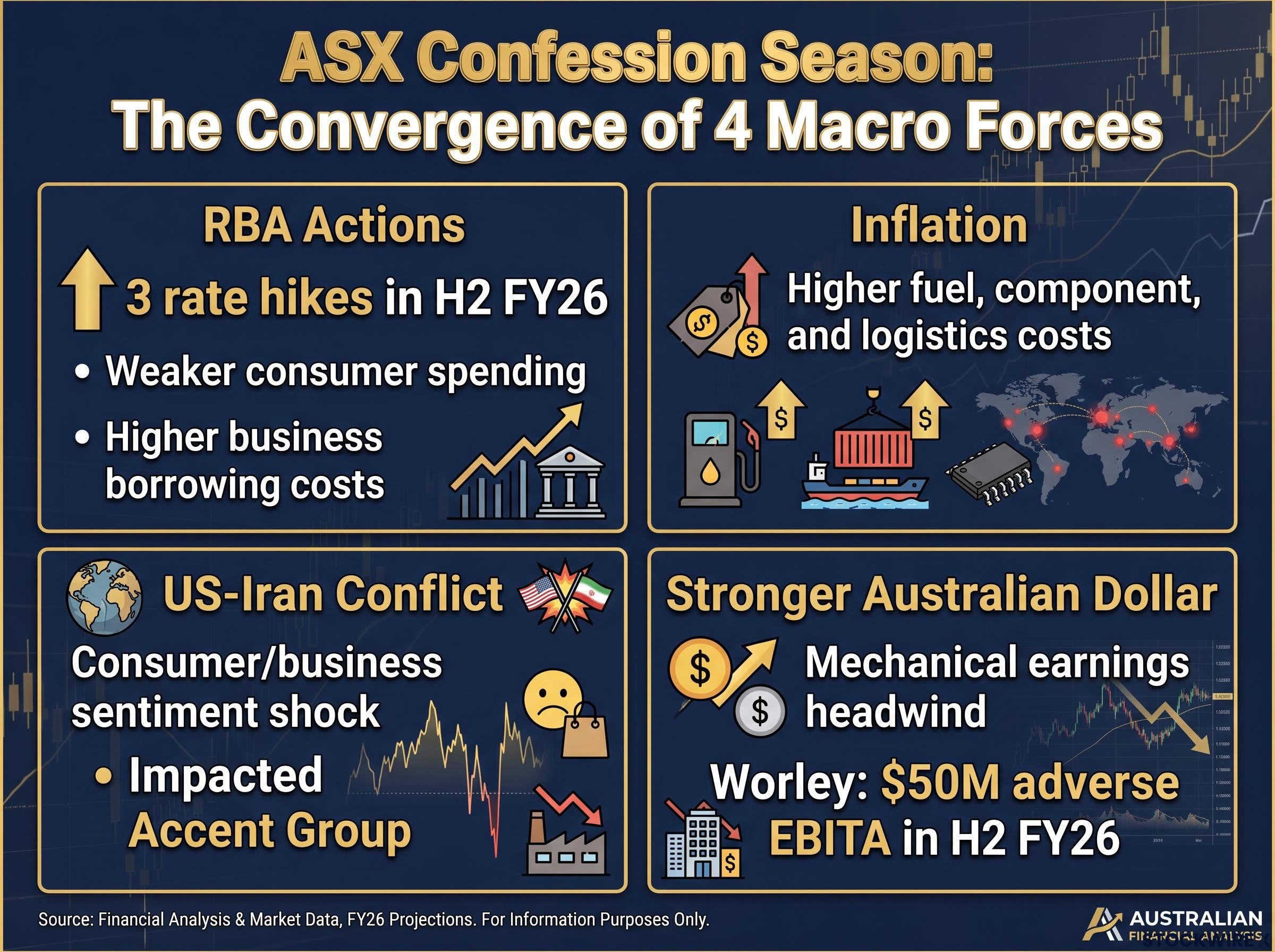

The four forces that shaped this confession season did not arrive independently. They converged in the same quarter, and the interaction between them is what made the damage broader and deeper than any single factor could explain.

The RBA raised the cash rate three times in the second half of FY26. Those hikes squeezed consumers from one direction, weakening discretionary spending capacity, and businesses from the other, raising borrowing costs. Then inflation re-accelerated, driven by higher fuel prices and component shortages that pushed input costs higher even where revenue was holding. Margins compressed before the top line softened.

The US-Iran conflict arrived as an unplanned external shock, hitting sentiment and supply chains simultaneously. In its 4 May 2026 update, Accent Group pointed to the geopolitical deterioration from late March as the direct cause of a sudden fall in both sales and gross margins, showing how rapidly shifts in consumer confidence can flow through to reported revenue. Meanwhile, a stronger Australian dollar created a mechanical earnings headwind for offshore earners. Worley disclosed that currency movements in H2 FY26 were expected to reduce its underlying EBITA by approximately $50 million, even as its operational performance remained solid.

The Strait of Hormuz selloff on 8 May 2026 illustrated the transmission speed of geopolitical shocks into Australian equities: a single overnight military exchange erased an estimated $100 billion in market capitalisation, with bond yield and oil price channels operating simultaneously and financials and real estate absorbing the sharpest sectoral damage.

No single factor is the cause. The convergence of all four in the same quarter is what makes 2026 structurally different from a typical softening year, and what tells you the pain is macro-driven rather than company-specific.

| Macro Force | Primary Transmission Channel | Most Directly Affected |

|---|---|---|

| Three RBA rate hikes (H2 FY26) | Weaker consumer spending, higher business borrowing costs | Discretionary retail, hospitality |

| Re-accelerating inflation | Higher fuel, component, and logistics costs squeezing margins | Consumer electronics retail (JB Hi-Fi) |

| US-Iran conflict | Consumer and business sentiment shock, supply-chain uncertainty | Leisure travel, sentiment-exposed retail (Accent Group) |

| Stronger Australian dollar | Mechanical earnings headwind on offshore revenues | Offshore earners (Worley: $50M adverse EBITA) |

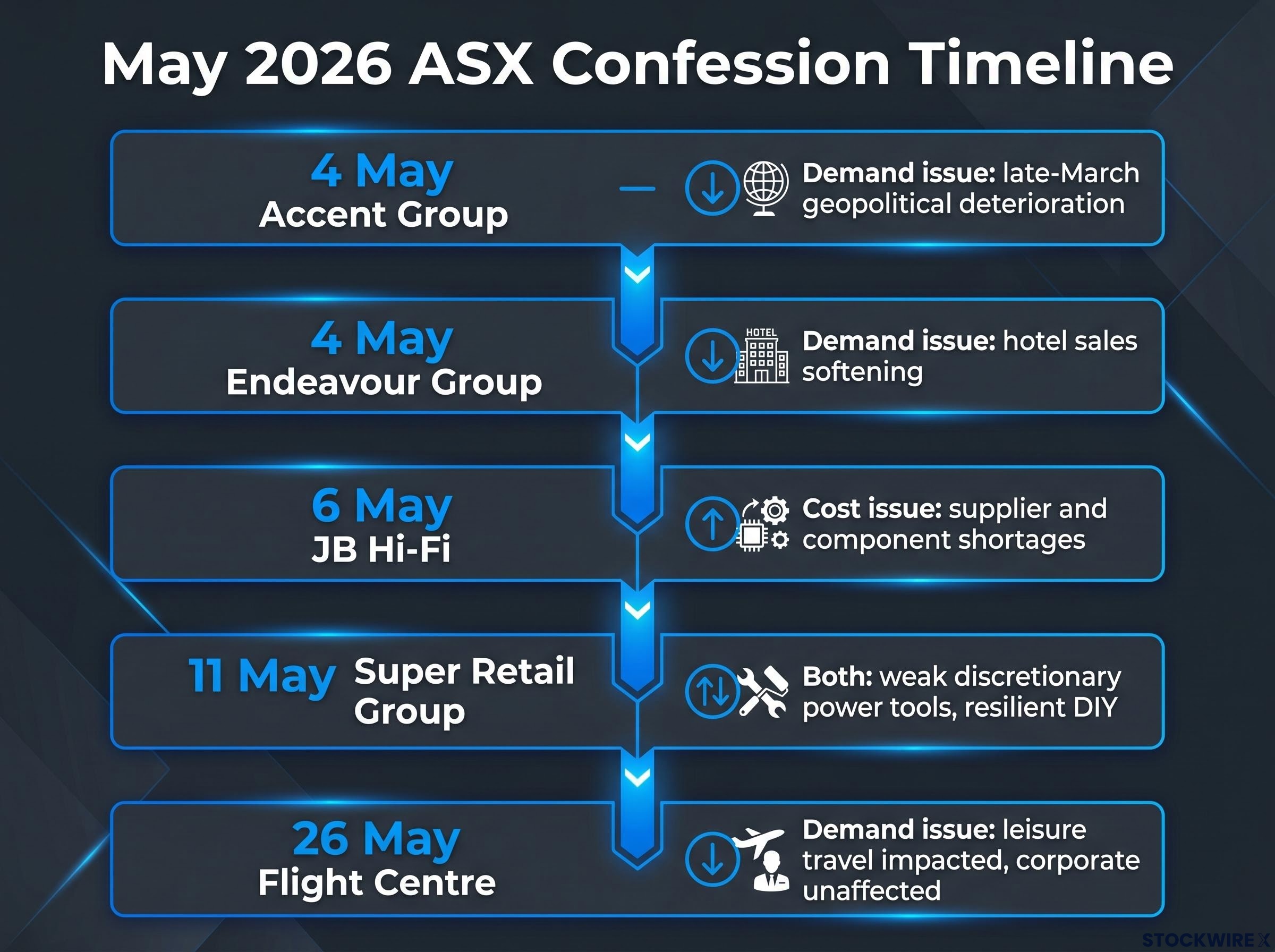

Five companies disclosed between 4 May and 26 May 2026. Individually, each is a data point. Together, they form a pattern that tells you something the individual disclosures cannot.

Accent Group (4 May) was meeting its guidance through to the end of March, when conditions shifted abruptly. A deterioration in trading through late March and into April, which the company linked to the geopolitical environment, drove both revenue lower and gross margins thinner.

Accent Group’s disclosure offered the most direct causal link in the current confession wave, with the company pinpointing the geopolitical escalation from late March as the specific trigger for its revenue and margin decline.

Endeavour Group (4 May) entered its third quarter with solid momentum, but revenue across its Hotels business began losing pace from March onward, with the slowdown touching food, bar, gaming, and accommodation lines. The pattern mirrors Accent Group’s timing precisely, but in a completely different sector.

JB Hi-Fi (6 May) told a different version of the same story, this time led by costs rather than demand. The company pointed to cost increases driven by supplier and component factors, alongside shortages limiting stock availability and a more competitive trading environment as the key pressures. Even a scale player with strong buying power could not offset sector-wide cost pressures.

Super Retail Group (11 May) entered the year with strong trading, but conditions in the Auto category began easing from March through April. The split within the segment is instructive: higher-ticket discretionary lines such as power tools came under pressure, while demand for maintenance, fuel-related, and DIY products provided a partial cushion. Consumers were choosing necessities over wants.

Flight Centre (26 May) reported that the current environment was weighing more heavily on its leisure travel business, while its corporate travel operations had not seen meaningful disruption at the time of the update. The leisure-versus-corporate split is one of the clearest behavioural signals in the current data.

| Company | Update Date | Core Issue | Sector | Key Detail |

|---|---|---|---|---|

| Accent Group | 4 May 2026 | Demand | Discretionary retail | Sharp late-March deterioration attributed to geopolitical tensions |

| Endeavour Group | 4 May 2026 | Demand | Hospitality | Hotel sales softening from March across all revenue streams |

| JB Hi-Fi | 6 May 2026 | Cost | Electronics retail | Supplier-driven costs, component shortages, reduced availability |

| Super Retail Group | 11 May 2026 | Both | Specialty retail | Discretionary categories weak; maintenance products resilient |

| Flight Centre | 26 May 2026 | Demand | Travel | Leisure travel impacted; corporate travel largely unaffected |

Late March 2026 was not a coincidence across five independent companies. It was the moment when macro conditions crossed a threshold that changed consumer and business behaviour simultaneously. That pattern gives you an evidence base for evaluating whether further downgrades in adjacent sectors are likely.

The damage is not uniform, and the dividing line is coherent enough to be useful.

The sectors taking concentrated pain share one trait: sensitivity to consumer confidence and discretionary spending decisions.

Breadth deterioration widened through late May 2026, with 27 ASX 200 constituents hitting fresh 52-week lows in the week ending 22 May, up from 22 two weeks earlier, and Consumer Discretionary recording 8 new lows across travel, retail, education, and automotive sub-categories simultaneously, a pattern consistent with systemic pressure rather than isolated stock-picking failures.

The relatively resilient categories share a different trait: they are either needs-driven, business-funded, or insulated from consumer sentiment entirely.

The margin damage in the current environment is worse than headline revenue trends suggest. Companies are simultaneously facing higher input costs (fuel, components, logistics) and weaker top-line performance. This dual squeeze is most acute in discretionary retail and hospitality, and it is the reason profit guidance cuts have been proportionally larger than sales guidance cuts.

The consumer behaviour pattern, maintaining necessities while cutting discretionary items, is coherent and likely to persist until rate settings change. That tells you the resilient sub-categories are structurally more defensible at this point in the cycle, not just temporarily holding up.

Confession season rewards analytical discipline, not speed of reaction. The framework for interpreting each new disclosure rests on four disciplines:

For most companies confessing in 2026, the macro cycle is the cause, not individual management failure. The disciplined investor’s edge is distinguishing which businesses will recover when the cycle turns and which have underlying problems the macro has simply exposed.

UBS expects further downgrades across the market, which means confession season is not yet complete. The July-August full-year results season is the next formal disclosure milestone where the full picture emerges.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The confession season preview maps onto July-August, but the detailed numbers, segment revenue, gross margin, operating cost lines, and cash flow, will reveal whether the damage is contained or more severe than the trading updates implied. The gap between a profit warning in May and a full-year result in August is the investor’s analytical window.

Resources and energy insulation means the ASX 200 index-level outcome will be buffered, even if the consumer-facing cohort delivers material earnings misses. The headline index number and the underlying sector story will tell different tales.

The equity risk premium on the ASX 200 sat at approximately 80 basis points as of May 2026, a historically thin buffer that means proportionally moderate earnings misses from the consumer-facing cohort can produce outsized index-level reactions, because the valuation multiple was already pricing in near-perfect earnings delivery before confession season began.

The variables that determine whether current headwinds ease or persist are all still in motion:

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The investor who uses the next six to eight weeks to map which holdings carry cyclical risk versus structural risk is entering reporting season with a genuine informational advantage over those reacting in real time.

ASX confession season 2026 is exceptional in breadth and timing, but the weight of evidence points to cyclical macro forces as the primary driver, not systemic business model failure across the consumer-facing ASX.

The discipline is to use confession season intelligence to build a clearer picture of which holdings carry cyclical risk and which carry structural risk before July-August results arrive. The macro variables driving the current wave, rate settings, geopolitical stability, FX movements, and the inflation trajectory, are all conditions that shift over the medium term.

The investor who has done the analytical groundwork during confession season is positioned to act decisively when they do.

ASX confession season is the pre-earnings window, typically running from May to June, when listed companies must issue trading updates, guidance cuts, or profit warnings if their results will materially miss prior guidance or consensus. The obligation is not voluntary: ASX Listing Rule 3.1 requires immediate disclosure once material information is known internally.

Four macro forces converged in the same quarter: three RBA rate hikes in H2 FY26 that squeezed consumers and raised business borrowing costs, re-accelerating inflation driving up input costs, the US-Iran conflict shocking consumer sentiment and supply chains, and a stronger Australian dollar creating a mechanical earnings headwind for offshore earners. Companies including Accent Group, Endeavour Group, JB Hi-Fi, Super Retail Group, and Flight Centre all pinpointed late March 2026 as the moment conditions shifted.

Discretionary retail, hospitality and leisure, and leisure travel are absorbing the most concentrated damage, with Consumer Discretionary recording 8 new 52-week lows in a single week in May 2026. Resources and energy are largely insulated, and UBS has noted that almost all ASX sectors outside mining and energy are in downgrade mode.

The key discipline is distinguishing cyclical pain from structural damage: a broken competitive position does not resolve when the macro cycle turns, but temporarily suppressed consumer confidence does. Market reactions to profit warnings can overshoot, potentially creating entry points in fundamentally sound businesses where the underlying problem is cyclical rather than structural.

As of late June 2026, UBS is expecting further downgrades, which means the confession wave is not yet complete. The July-August full-year reporting season is the next formal disclosure milestone, where detailed segment revenue, gross margin, and cash-flow data will confirm whether the damage disclosed in May and June trading updates is contained or more severe.