June US Inflation Report Hits as Fed Sits 9-9 on Rate Hikes

3 hrs ago

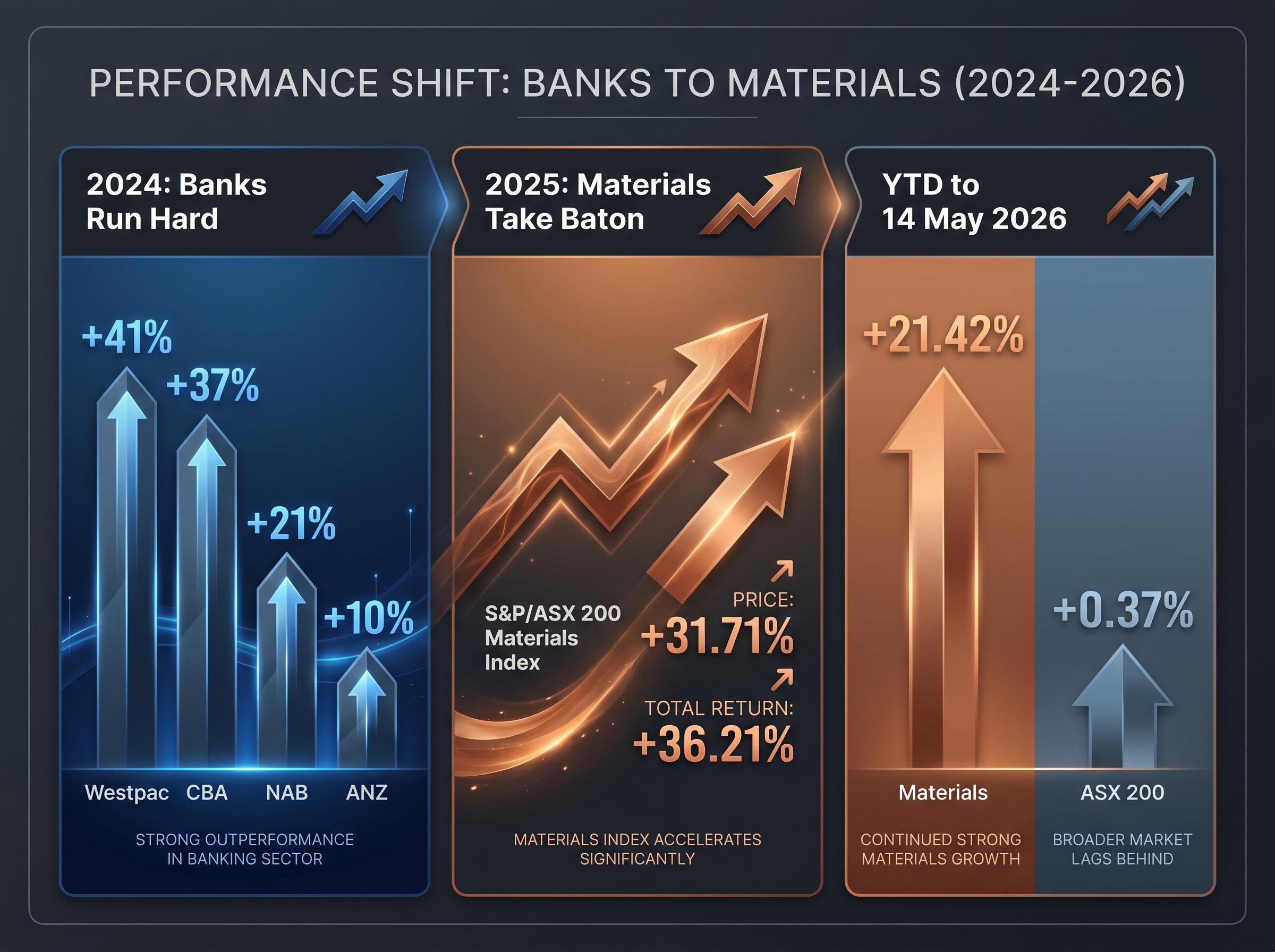

BHP has overtaken Commonwealth Bank (CBA) as the largest company on the ASX by market capitalisation, a symbolic shift that reflects something more fundamental than a single week’s price movement. As of mid-May 2026, the S&P/ASX 200 Materials index is up 21.42% for the year while the broader ASX 200 sits at just +0.37% YTD. That spread points directly at underperforming bank stocks. The rotation from banks to miners is no longer a thesis being debated; it is happening in real time, and Australian retail investors are asking whether their portfolios are positioned on the right side of it.

What follows walks through the valuation gap between ASX banks and miners, the commodity price momentum driving the shift, the 2026 Federal Budget sector implications, and an allocation framework that connects all four, so readers can weigh these sectors with sharper context.

The current spread between banks and miners did not appear overnight. It built across three distinct periods, each reinforcing the next.

The major banks delivered strong returns in 2024. Westpac led with a +41% gain, followed by CBA at +37%, NAB at +21%, and ANZ at +10%, according to Firstlinks data published in January 2025. Performance at those levels, particularly for CBA and Westpac, stretched valuations and compressed the expected return runway ahead.

The S&P/ASX 200 Materials Index returned +31.71% on price and +36.21% on a total return basis in 2025, making it the best-performing ASX 200 sector that year, according to Motley Fool analysis. That momentum has accelerated into 2026. As of 14 May 2026, the Materials index is up +21.42% YTD against the ASX 200’s +0.37%, a gap of more than 21 percentage points.

The table below frames the divergence across all three periods.

| Period | Banks (proxy) | Materials | Spread |

|---|---|---|---|

| 2024 | CBA +37%, WBC +41% | Modest relative to banks | Banks outperformed |

| 2025 (full year) | Lagged broader market | +31.71% (price), +36.21% (total return) | Materials led |

| YTD 2026 (to 14 May) | ASX 200 overall: +0.37% | +21.42% | ~21 percentage points |

This is not a sudden flip. It is a multi-stage reversal with a clear internal logic: banks stretched, miners repriced, and the spread widened.

The current divergence follows a pattern consistent with prior ASX market cycle lessons: sectors that lead one phase of the cycle tend to enter the next phase stretched on valuation, creating the conditions for rotation rather than continuation, a dynamic that played out clearly when Information Technology surged 52% and Materials fell 13% across the 2024 recovery.

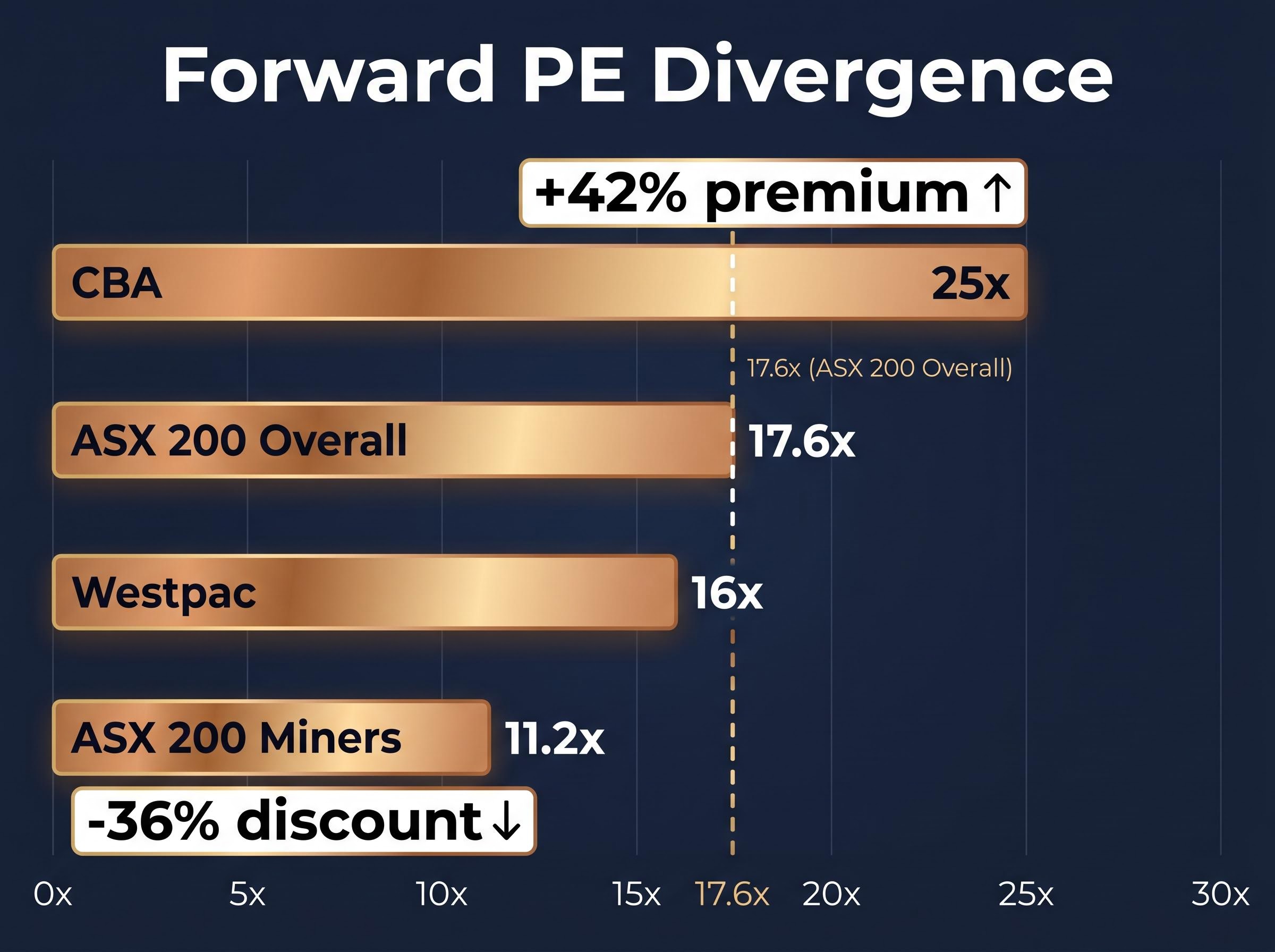

The performance divergence becomes sharper when viewed through forward earnings multiples. CBA trades at approximately 25x forward earnings (trailing 27x). Westpac sits at roughly 16x. The ASX 200 overall trades at 17.6x.

ASX 200 miners, by contrast, trade at a forward PE of 11.2x, according to Firstlinks analysis.

| Entity | Forward PE | Discount/premium to ASX 200 |

|---|---|---|

| CBA | ~25x | +42% premium |

| WBC | ~16x | -9% discount |

| ASX 200 Miners | ~11.2x | -36% discount |

| ASX 200 Overall | ~17.6x | Benchmark |

Miners trade at a 36% discount to the ASX 200 and a 37% discount to the Financials sector on a forward PE basis.

Valuation alone is not a catalyst. Cheap stocks can stay cheap. But when valuation compression coincides with positive commodity price momentum, as it does now, the asymmetry shifts toward the discounted sector. Firstlinks commentary has flagged this gap as likely to narrow.

The rotation thesis carries more weight when the commodities that drive miner earnings are moving in the right direction. All three of the major base metals tracked below have trended higher through April and into May.

Iron ore’s one-month gain of +7.82% from mid-April to mid-May represents the headline momentum signal for diversified miners with significant iron ore exposure.

The simultaneous upward movement across iron ore, copper, and nickel matters for companies like BHP and Rio Tinto with multi-commodity portfolios. It reduces single-commodity concentration risk for investors allocating to the sector and strengthens the aggregate earnings outlook.

The copper demand outlook extends well beyond current spot price momentum, with S&P Global projecting global consumption to rise from 28 million metric tonnes in 2025 to 42 million metric tonnes by 2040 as renewables, electric vehicles, and AI data centre buildouts each add structural incremental demand, a trajectory that strengthens the medium-term earnings case for diversified miners with significant copper exposure.

Before reading the valuation gap as a buy signal, it is worth understanding why miners have historically traded cheaper than banks on the ASX.

Mining companies are inherently cyclical. Their earnings are directly tied to commodity prices set on international exchanges, meaning revenue can swing sharply from one reporting period to the next depending on iron ore, copper, or nickel spot prices. Capital expenditure cycles amplify this: a mine expansion committed at $120-per-tonne iron ore looks very different at $80.

Banks, by contrast, operate as regulated oligopolies with sticky deposit franchises, predictable net interest margin income, and consistent dividend histories. Income-oriented investors have historically paid a premium multiple for that stability.

The PE discount for miners is therefore partly structural (reflecting genuine earnings volatility) and partly cyclical (reflecting where commodity prices sit at any given moment relative to expectations).

The conditions that historically narrow the bank-miner valuation gap include:

All three conditions are present in the current environment. Morgan Stanley’s model portfolio reflects this assessment, holding banks at a -5.63% underweight relative to the ASX 200’s 24% index weight, with only 18.5% allocated to the sector, according to LivewireMarkets (note: these figures are indicative, sourced from a page that could not be independently verified at the time of writing).

The gap may be narrowing, but Firstlinks framing is appropriate here: convergence remains a thesis, not a certainty.

The 2026-27 Federal Budget, announced on 12 May 2026, added a policy layer to a rotation already underway. The asymmetry between how the Budget treated each sector is notable.

| Sector | Key Budget measures | Likely earnings impact |

|---|---|---|

| Mining | Skilled migration reforms (faster assessments for migrant trades workers), accelerated occupational licensing, “Budget backs mining for national resilience” framing | Positive |

| Banking / Financial | No confirmed bank levy or APRA capital changes; potential implications for housing and mortgage policy | Neutral to uncertain |

Labour supply has been a structural constraint on Australian mining output for years. The skilled migration reforms and accelerated licensing measures are materially relevant to sector earnings potential rather than symbolic, because they address a bottleneck that has limited production scaling. The Minerals Council of Australia framed the Budget as one that “backs mining for national resilience.”

The Minerals Council of Australia budget response confirmed that the 2026-27 Federal Budget includes faster skills assessments for migrant trades workers and accelerated occupational licensing, measures the MCA framed as directly addressing the severe skills shortage that has constrained Australian mining output and production scaling.

On the banking side, no confirmed changes to bank levies or APRA capital requirements appeared in available Budget summaries from budget.gov.au. The fiscal settings carry potential implications for housing and mortgage policy that could affect net interest margins, but the direction remains unclear.

One sector received explicit policy support. The other received uncertainty. Federal Budget policy rarely moves share prices in isolation, but when it reinforces existing sector momentum, it can extend the duration of that momentum.

The 2026-27 Federal Budget tax reforms extend beyond sector-specific labour and production measures, with the $77 billion package restructuring capital gains tax, restricting negative gearing to new builds, and introducing a 30% minimum tax on discretionary trust distributions, each of which alters the after-tax return profile for Australian investors holding equities or property alongside their mining sector exposure.

Every thread covered in this analysis points in the same direction. Banks are expensive on forward earnings, face uncertain earnings tailwinds, and are underperforming. Miners are cheap at 11.2x forward PE, commodity prices are rising across iron ore, copper, and nickel simultaneously, and the Federal Budget explicitly supports the sector’s labour and production capacity.

The bull case for miners:

The risks that require conviction:

Investors currently overweight banks relative to the ASX 200 index may want to assess whether that position still reflects their view on earnings trajectory, given CBA at 25x forward earnings and the sector’s YTD underperformance.

For investors considering ETF-based implementation of a bank-to-miner reallocation, our full explainer on thematic ETF risks during sector rotation examines how technology-themed ETFs delivered up to 25% drawdowns in 2026 while resources ETFs returned triple digits, and why the behaviour gap between reported fund returns and actual investor returns is widest in thematic products, with ARK Innovation as the most cited case study.

BHP overtaking CBA as the ASX’s largest company by market capitalisation in mid-May 2026 is not a reason to chase, but it is a data point on where institutional capital has already moved.

The weight of evidence, valuation, commodity momentum, Budget policy, and market cap leadership, has shifted in the same direction. The question for Australian investors is no longer whether a rotation from banks to miners is occurring. It is whether their current sector weights reflect where earnings momentum is pointing.

What would change the thesis is straightforward: a sustained reversal in commodity prices, or a material re-acceleration in bank earnings growth driven by credit expansion or wider net interest margins. Until one of those conditions emerges, the data continues to favour the discounted sector.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

As of mid-2026, ASX 200 miners trade at approximately 11.2x forward earnings, representing a 36% discount to the ASX 200 overall (17.6x) and a 37% discount to the Financials sector. CBA alone trades at around 25x forward earnings, a 42% premium to the broader index.

The S&P/ASX 200 Materials index is up 21.42% year to date as of 14 May 2026 against the ASX 200's 0.37%, driven by rising iron ore, copper, and nickel prices, stretched bank valuations following strong 2024 returns, and Federal Budget reforms that directly support mining labour supply and production capacity.

The 2026-27 Federal Budget, announced on 12 May 2026, introduced faster skills assessments for migrant trades workers and accelerated occupational licensing, measures the Minerals Council of Australia framed as directly addressing the severe skills shortage constraining Australian mining output and production scaling.

Iron ore rose approximately 7.82% from mid-April to mid-May 2026, moving from around $103.34 USD per tonne to $111.42 USD per tonne, while copper climbed from $13,445 USD per tonne to $13,872 USD per tonne and nickel also trended higher over the same period.

The key risks include a sustained reversal in commodity prices, which are set on international markets and can move quickly, and a potential re-acceleration in bank earnings if interest rate cut timing shifts or credit growth surprises to the upside.