Why a 57,000 Jobs Miss Sent Equity Futures Higher

48 mins ago

Three of Australia’s four largest banks went sideways or backwards in June, a month when the Reserve Bank of Australia (RBA) finally paused its rate hike cycle and gave the sector the one thing it had been asking for: breathing room. The S&P/ASX 200 returned roughly 0.5% for the month. NAB was the only major bank to beat it. CBA, ANZ, and Westpac all fell short, with Westpac dropping 2.2%.

That gap between what the month delivered and what investors expected tells you something has shifted in how the market reads the bank story. The rate hike cycle that once fuelled margin expansion has become a ceiling. And the Federal Budget’s negative gearing changes, announced on 12 May 2026, have introduced a second pressure point, one that reaches directly into the housing credit engine underpinning all four balance sheets.

What follows here maps out the specific forces behind the June numbers and what they signal for the second half of the year. If you hold ASX bank shares or are considering a position, this is about whether the underperformance is temporary noise or something more structural, and what to watch heading into August reporting season.

The numbers themselves are straightforward. What makes them worth examining is the context around them.

| Bank | May Close | June 30 Close | June Return |

|---|---|---|---|

| NAB | $37.33 | $37.86 | +1.4% |

| ANZ | $35.20 | $35.35 | +0.4% |

| CBA | $165.02 | $164.62 | -0.2% |

| Westpac | $36.00 | $35.21 | -2.2% |

Against the ASX 200’s 0.5% return, only NAB outperformed. ANZ finished the month in positive territory but its gain fell short of the benchmark. CBA slipped 0.2%, a small move in absolute terms but notable for a stock trading at such a premium valuation; even marginal negative returns at that price level suggest buyers are stepping back. Share price data sourced via Motley Fool Australia reporting.

Westpac’s 2.2% decline made it the clear standout underperformer for the month, falling more than four times the distance of the next-weakest result.

Not one of the four banks put out any price-sensitive announcements during the month. No earnings updates, no capital raises, no management changes. The absence of company-specific news is the point: when three out of four major banks trail the index in a month with no idiosyncratic catalysts, macro sentiment, not corporate execution, is doing the driving. That distinction matters for how you read the sector from here.

On the surface, the RBA’s decision to hold the cash rate at 4.35% on 16 June 2026 looked like the event the banking sector had been waiting for. After three hikes earlier in the year, a pause should have been a relief.

The three consecutive RBA hikes from February through May 2026 added 75 basis points to borrowing costs, compressing household repayment capacity well before the June hold arrived and leaving banks with a loan book already under incremental stress even as their reported margins looked healthy.

It was not. The problem is what the hold confirmed rather than what it prevented. Three consecutive hikes had already pushed net interest margins higher, and that benefit was largely priced into bank valuations before June began. The hold did not unlock a new tailwind; it signalled that the margin expansion chapter was closing.

What replaced it is a less comfortable story. Two consequences are now front of mind for the sector:

For investors still holding bank shares on the thesis of margin expansion, the June hold is the clearest signal yet that this chapter is done. The next one, centred on credit quality and loan volume trajectory, has already begun. Recalibrating expectations now, rather than waiting for August reporting season to force the adjustment, is the practical read here.

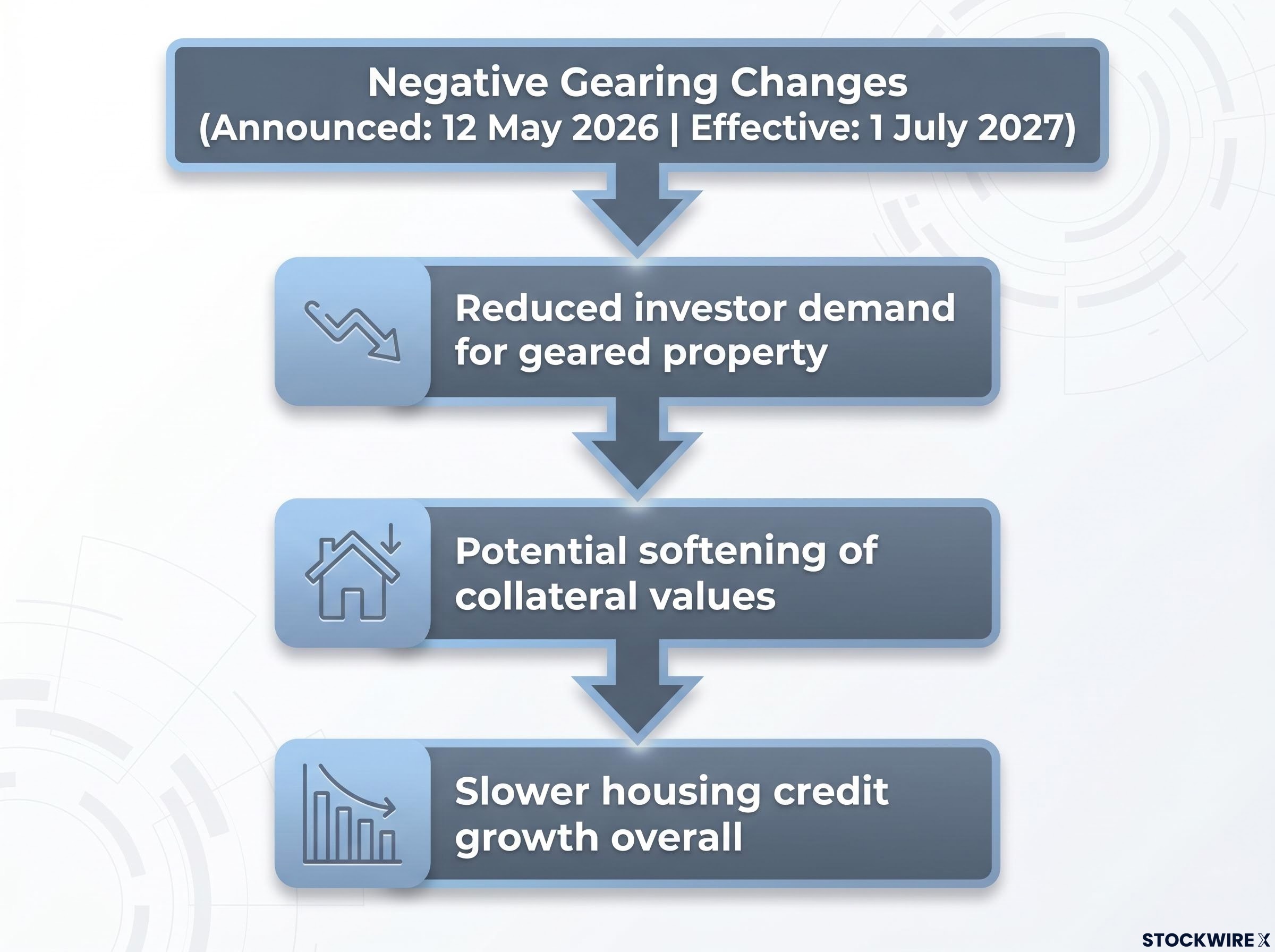

The Federal Budget announced on 12 May 2026 introduced changes to negative gearing for residential property. Negative gearing is the practice of borrowing to invest in property where the rental income is less than the costs (including interest), and then claiming the loss against other income to reduce tax. The changes, effective 1 July 2027 with grandfathering provisions for existing arrangements, reduce the tax incentive that has historically fuelled investor demand in Australia’s housing market.

For the big four banks, the connection between a tax policy change and their share prices runs through a specific three-stage mechanism:

Morgan Stanley’s June 2026 analysis quantified housing collateral risk across the Big Four by projecting a potential 10% residential price fall by end-2027, producing a 4% earnings downgrade and repositioning ANZ above CBA in its preference order specifically because of CBA’s dominant mortgage market share and the differential exposure that creates in a housing cycle downturn.

Regal Funds Management’s Mark Nathan commented that the Federal Budget represented a meaningful shift in the sector’s outlook, with the market moving away from what had previously been a workable growth assumption toward a more cautious position, as confidence in housing-linked earnings was revised downward.

Multiple analysts cited by Motley Fool Australia reporting flagged softening mortgage demand and a rising risk of bad debt accumulation as key concerns for the big four. The negative gearing change does not threaten the solvency of any major bank. But it does signal that the residential mortgage book, the core growth engine for all four, is entering a period of structurally slower expansion and heightened collateral risk. That is the angle most housing market commentary misses: this is not just a property story. It is a bank earnings story.

The structural strengths of Australia’s big four have not changed. These are well-capitalised, systemically important institutions with dominant market shares. Their capital positions are not under question. This is not a distress scenario.

What has changed is the environment in which those strengths operate. The margin tailwind from rate hikes has largely played out. The negative gearing changes have introduced a policy headwind to housing credit growth that was not in anyone’s models 12 months ago. Both forces are now locked in, and the question for the second half is how well each bank manages through them.

August reporting season is the sector’s first credible test under these conditions. Three metrics will tell you more than the share price alone:

CBA arrears data from Q3 2026 already showed personal loan arrears spiking 30 basis points in a single quarter, a forward-looking signal that arrived before the June hold and reinforces why the sector’s credit quality trajectory, not its margin level, is now the primary earnings variable heading into August reporting.

NAB’s June outperformance is worth noting but insufficient on its own to conclude it is better positioned than peers. One month of relative strength does not answer whether its credit quality and volume growth will hold up under the same pressures facing the entire sector. The investment thesis for bank shares in H2 2026 is less about chasing growth and more about assessing balance-sheet resilience and dividend durability.

Payout ratios above 75-80% warrant closer scrutiny when credit charges are rising, and the balance sheet metrics that matter most for that assessment, including NPL ratios, CET1 buffers, and deposit funding composition, vary enough across CBA, ANZ, NAB, and Westpac to produce materially different dividend durability conclusions even when reported earnings look similar.

June confirmed what the rate cycle had already been signalling: the margin expansion story is largely exhausted. The sector is now in a phase defined by credit quality management and volume defence, not pricing power. That was the direction of travel before June; the month’s performance simply removed any remaining ambiguity.

What has changed is the addition of a structural policy headwind. Before the Federal Budget, the outlook for bank earnings was primarily a rate-cycle question: when would hikes stop, and would margins hold? The negative gearing announcement layered in a separate constraint on housing credit growth, one that operates on a different timeline and cannot be resolved by RBA decisions alone. The investment case is now more complex than a simple call on rates.

The practical takeaway for anyone assessing bank share exposure is that this is no longer a sector-level decision. Investing in ASX bank shares in the second half of 2026 requires an opinion on individual bank credit quality, provisioning discipline, and the sustainability of dividends under tighter conditions. Dividends and capital management remain the pull factors for income-oriented investors, but the margin of safety in those dividends now depends on metrics that were secondary concerns a year ago.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

Negative gearing is the practice of borrowing to invest in property where rental income falls short of costs, with losses claimed against other income to reduce tax. The Federal Budget changes announced on 12 May 2026 reduce this tax incentive from 1 July 2027, directly shrinking the pool of investor mortgage applications and slowing housing credit growth, the core earnings engine for all four major banks.

The RBA's hold at 4.35% on 16 June 2026 confirmed the end of margin expansion rather than opening a new tailwind, because three prior hikes had already been priced into bank valuations. What investors refocused on instead were the two emerging headwinds: dampened loan volume growth and rising credit quality risk from households absorbing multiple repayment increases.

NAB was the only major bank to beat the ASX 200's 0.5% return in June 2026, rising 1.4% from $37.33 to $37.86. ANZ gained 0.4% but fell short of the benchmark, while CBA slipped 0.2% and Westpac was the clear underperformer, falling 2.2%.

Three metrics will matter most: mortgage arrears trajectory (CBA data already showed personal loan arrears spiking 30 basis points in a single quarter), loan book growth direction, and how aggressively management teams are building impairment provisions. Rising provisions signal that banks themselves see deteriorating credit conditions ahead.

Payout ratios above 75-80% warrant closer scrutiny when credit charges are rising. Dividend durability now depends on NPL ratios, CET1 buffers, and deposit funding composition, metrics that vary enough across CBA, ANZ, NAB, and Westpac to produce materially different conclusions even when reported earnings look similar.