What a Random ASX Backtest Reveals About Managing Market Risk

3 hrs ago

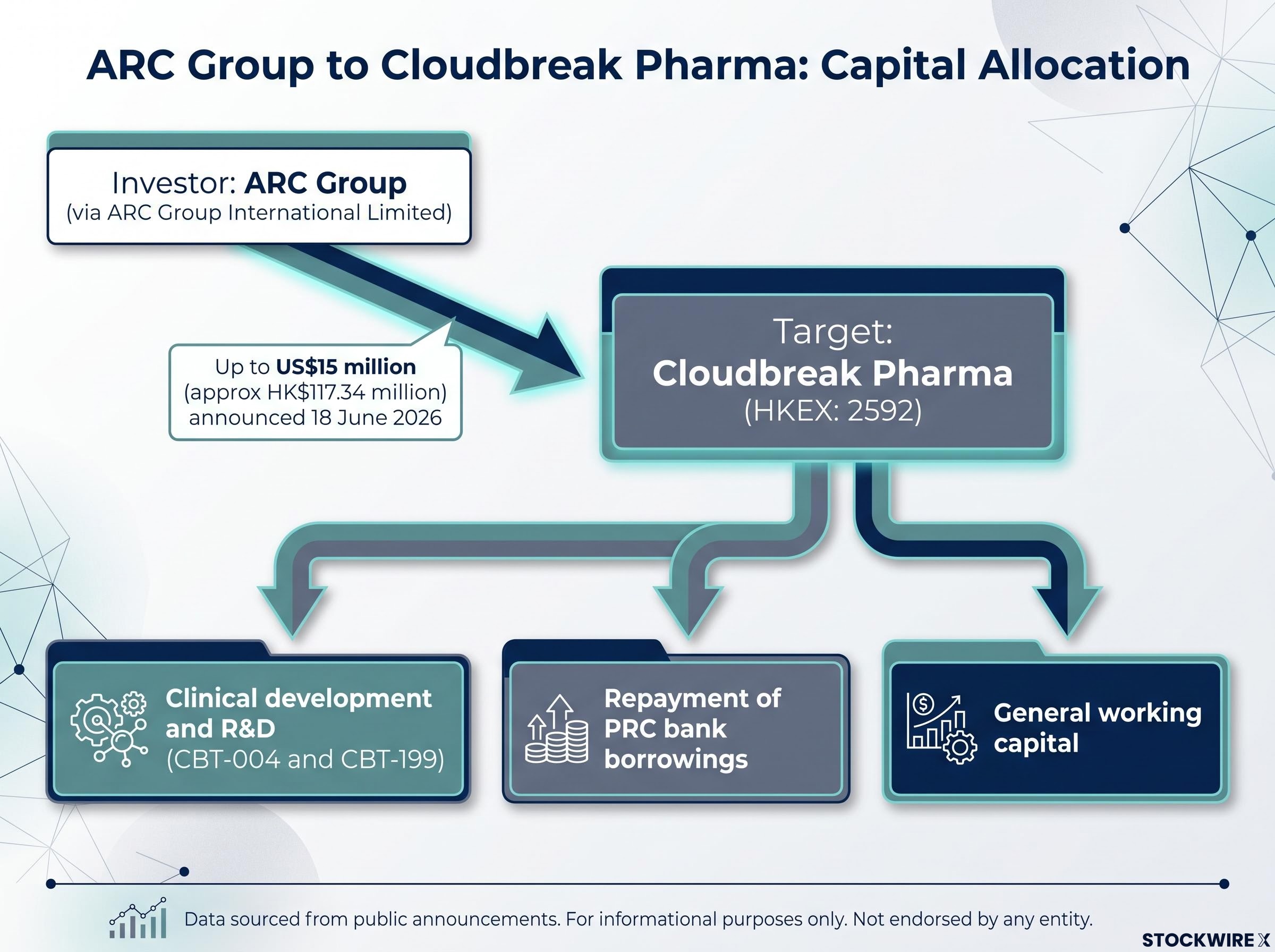

ARC Group has committed up to US$15 million in a negotiated equity subscription to Hong Kong-listed ophthalmology biotech Cloudbreak Pharma (HKEX: 2592), bypassing the open market entirely to place primary capital directly onto the company’s balance sheet. The deal was announced on 18 June 2026 and, if completed, will fund late-stage clinical programmes targeting eye diseases in ageing populations.

The transaction sits at the intersection of two trends worth tracking: the broadening of Asia-based asset managers into clinical-stage biotech, and the continued maturation of the Hong Kong Stock Exchange (HKEX) as a credible venue for institutional cross-border life sciences capital. This is a deal that rewards a close read, because the structure, the pipeline, and the caveats reveal more than the headline number.

Here is what the deal mechanics, the clinical thesis, and the risk profile actually tell you about how Asian capital is moving into biotech right now.

The core detail: this is not a stock purchase. ARC Group International Limited, a wholly owned subsidiary of ARC Group, is subscribing for newly issued shares in Cloudbreak Pharma. The proceeds flow directly to Cloudbreak’s balance sheet as primary capital, not to a selling shareholder.

The total subscription commitment reaches as high as US$15 million (roughly HK$117.34 million at the exchange rate prevailing at announcement). The transaction remains subject to the terms of the share subscription agreement being fulfilled and all necessary approvals obtained, meaning completion is not yet assured.

That conditionality is the first thing any reader treating this as a market signal should internalise. The negotiated structure signals bilateral alignment and strategic conviction, not a passive portfolio allocation, but the capital has not definitively changed hands.

Cloudbreak has disclosed a three-part allocation of the subscription proceeds, and the sequencing tells you as much as the amounts.

The clinical logic deserves the most attention. CBT-004 completed its Phase 2 clinical trial in the United States in April 2025, meeting its primary endpoint: statistically significant improvement in conjunctival hyperemia (redness of the eye’s surface) versus vehicle (the inactive control formulation used in the trial).

CBT-004 Phase 2 result: The trial met its primary endpoint, demonstrating statistically significant improvements in conjunctival hyperemia versus vehicle, establishing clinical proof of concept for the drug’s mechanism.

An end-of-Phase-2 meeting with the Food and Drug Administration (FDA) was completed in January 2026, confirming alignment on the Phase 3 path forward. Phase 3 initiation is targeted for Q1 2027, with trials designed to evaluate efficacy at three months and safety at twelve months.

Securing FDA registrational trial design agreement before committing Phase 3 capital is a material risk-reduction step that clinical-stage eye disease programmes have increasingly pursued, with PYC Therapeutics completing an equivalent alignment process for its VP-001 programme targeting RP11, a blinding retinal disease with no approved treatment.

The combination of pipeline investment and balance sheet deleveraging tells you Cloudbreak is positioning for the cost structure of Phase 3 rather than simply burning through funds. That financial discipline is the kind of signal institutional investors like ARC Group will have scrutinised before committing.

The investment thesis reveals itself through three specific choices: sector, company profile, and listing venue.

Nigel Wong, Head of Asset and Wealth Management at ARC Group, framed the rationale in structural terms.

“Healthcare is one of the most resilient long-term value drivers in Asian markets.”

ARC Group’s stated preference is for businesses that combine strong research and development with executable commercial strategy. Cloudbreak’s footprint spanning both the United States and China was characterised as a competitive strength, offering simultaneous access to two of the world’s biggest healthcare markets rather than introducing an additional layer of jurisdictional complexity.

The cross-border listing complexity that ARC Group characterised as a strength in Cloudbreak’s case sits within a broader regulatory architecture that has evolved significantly since 2023, with the CSRC overseas listing regime now running parallel to exchange and SEC processes and giving Beijing real rejection authority over China-connected issuers.

The listing venue rationale is where the signal extends beyond Cloudbreak. ARC Group explicitly cited HKEX’s disclosure standards as a transparency positive, reinforcing the exchange’s biotech regime (established through 2018 reforms enabling pre-revenue biotech listings) as an institutional-grade cross-border investment platform. That endorsement tells you something about how global institutional capital is now assessing Hong Kong’s biotech exchange, not just one company’s pipeline.

ARC Group noted that its pipeline of comparable assessments across healthcare and life sciences in Asia remains active, with a sustained focus on scalable platforms and capital-efficient growth opportunities across the region.

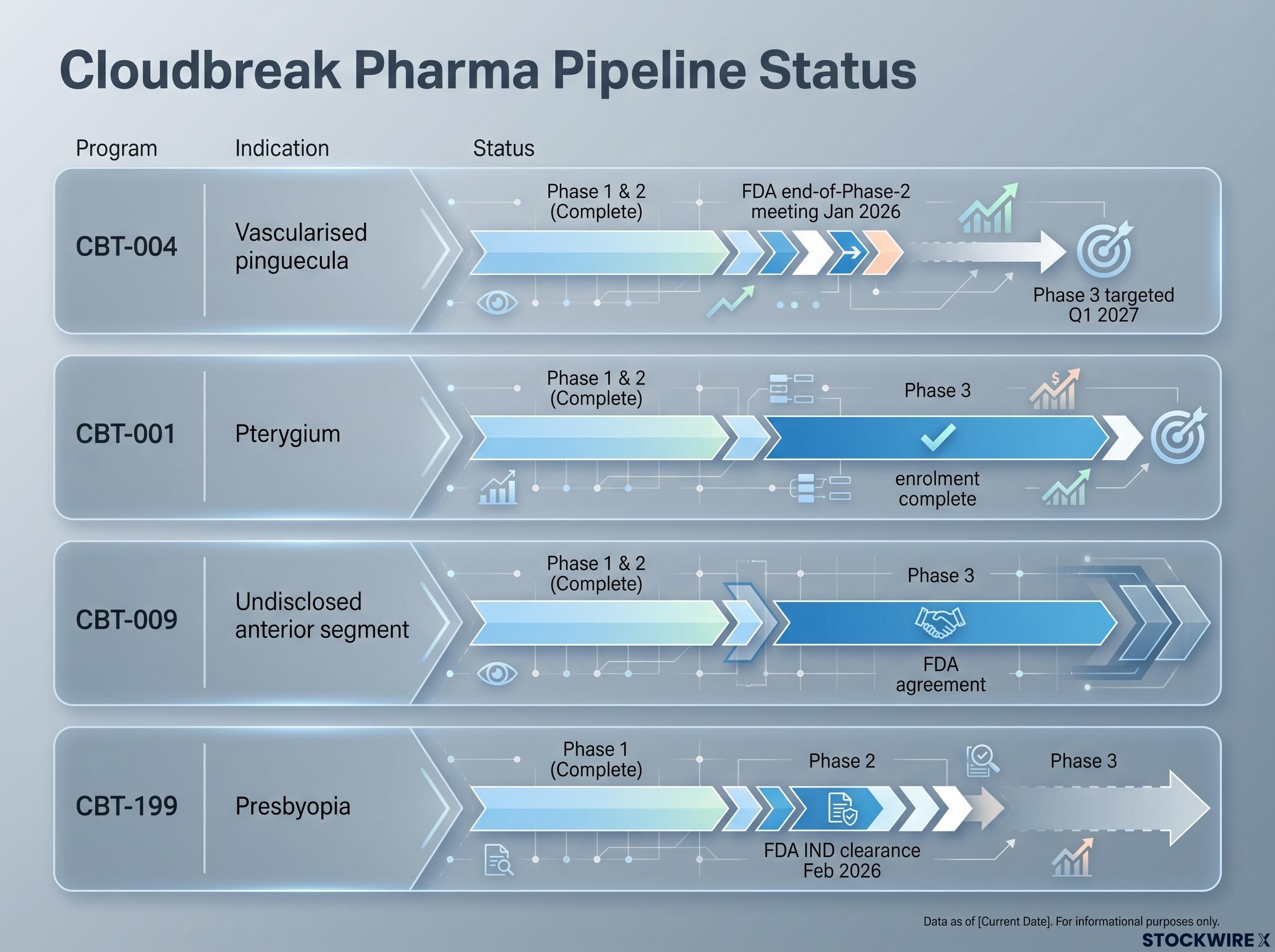

Cloudbreak is a platform company, not a single-asset bet. Its pipeline targets anterior segment eye diseases, conditions affecting the front of the eye, across four named programmes.

| Asset | Indication | Stage | Latest milestone |

|---|---|---|---|

| CBT-004 | Vascularised pinguecula | Phase 3 targeted Q1 2027 | FDA end-of-Phase-2 meeting completed January 2026 |

| CBT-001 | Pterygium | Phase 3 (enrolment complete) | International multi-centre trial fully enrolled |

| CBT-009 | Undisclosed anterior segment | Phase 3 (FDA agreement) | FDA agreement to enter Phase 3 |

| CBT-199 | Presbyopia | Phase 2 | FDA IND clearance for Phase 2, February 2026 |

CBT-004, the lead asset, is a topical multi-kinase inhibitor. It targets VEGFR and PDGFR, two receptor families involved in abnormal blood vessel growth and inflammation, to treat vascularised pinguecula, a non-cancerous growth on the eye’s surface that becomes increasingly common with age. The target patient population is predominantly elderly, reflecting ageing demographics as a structural market driver.

The commercial logic of targeting anterior segment eye disease programmes in ageing populations extends beyond Cloudbreak’s pipeline, with other clinical-stage ophthalmology biotechs presenting first-in-indication data at ARVO 2026 for conditions including RP11 and ADOA, both of which carry zero approved treatment options and address structural demographic demand.

The breadth across related indications reduces single-asset concentration risk. But each programme carries its own regulatory timeline and execution risk.

Positive Phase 2 data does not guarantee Phase 3 success or eventual regulatory approval. Phase 3 for CBT-004 is targeted but not yet initiated, and the distance between a successful Phase 2 readout and a marketed product remains substantial. Three categories of risk are material here:

Capital at this stage of drug development is placed long before the outcomes are known. That is the risk ARC Group is absorbing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and these forward-looking statements are subject to change based on market developments and company performance.

Zoom out from the deal mechanics and three capital markets signals come into focus.

ARC Group’s stated forward pipeline of similar assessments across healthcare and life sciences in Asia suggests this is a repeatable strategy, not an isolated transaction. For readers tracking where institutional capital is moving in Asia, this combination of deal structure, sector choice, and venue rationale points toward a maturation of the HKEX biotech ecosystem with implications beyond one deal.

This transaction carries two distinct theses. The first is clinical: that anterior segment eye diseases in ageing populations represent a large, underserved market addressable through topical therapeutics. The second is structural: that HKEX has matured into an institutional-grade venue for cross-border biotech capital deployment, and that mid-market Asian managers are prepared to underwrite clinical risk through negotiated, PE-style structures in a public-market setting.

The deal fits a pattern that Bridgewater Co-CIO Bob Prince identified at the HSBC Global Investment Summit in May 2026: institutional Asia allocation increasingly requires country-level precision and regime-aware portfolio construction rather than broad regional exposure, as modern mercantilism and AI reshape which Asian markets and sectors attract durable capital.

The transaction remains conditional. Readers tracking this deal should monitor for completion confirmation before treating it as a closed market signal. The next milestone that tests the clinical thesis is Phase 3 initiation for CBT-004, targeted for Q1 2027.

ARC Group, via its wholly owned subsidiary ARC Group International Limited, has agreed to subscribe for newly issued shares in Cloudbreak Pharma (HKEX: 2592) for up to US$15 million (approximately HK$117.34 million). The deal was announced on 18 June 2026 and remains conditional on share subscription agreement terms and necessary approvals.

Cloudbreak has allocated the proceeds across three uses: advancing lead clinical assets CBT-004 and CBT-199 through their next development stages, repaying PRC bank borrowings to clean up the balance sheet, and funding general working capital ahead of Phase 3 trials.

CBT-004 completed a Phase 2 trial in the United States in April 2025, meeting its primary endpoint with statistically significant improvement in conjunctival hyperemia versus vehicle. An end-of-Phase-2 meeting with the FDA was completed in January 2026, and Phase 3 initiation is targeted for Q1 2027.

ARC Group cited healthcare as a resilient long-term value driver in Asian markets, Cloudbreak's dual US-China commercial footprint as a competitive strength, and HKEX's disclosure standards as an institutional-grade transparency positive following the exchange's 2018 biotech reforms.

Three material risk categories apply: pipeline and regulatory risk (Phase 3 has not yet initiated for CBT-004 and positive Phase 2 data does not guarantee approval), cross-border operational risk across the US, Hong Kong, and mainland China, and deal completion risk as the subscription remains conditional and capital has not definitively changed hands.