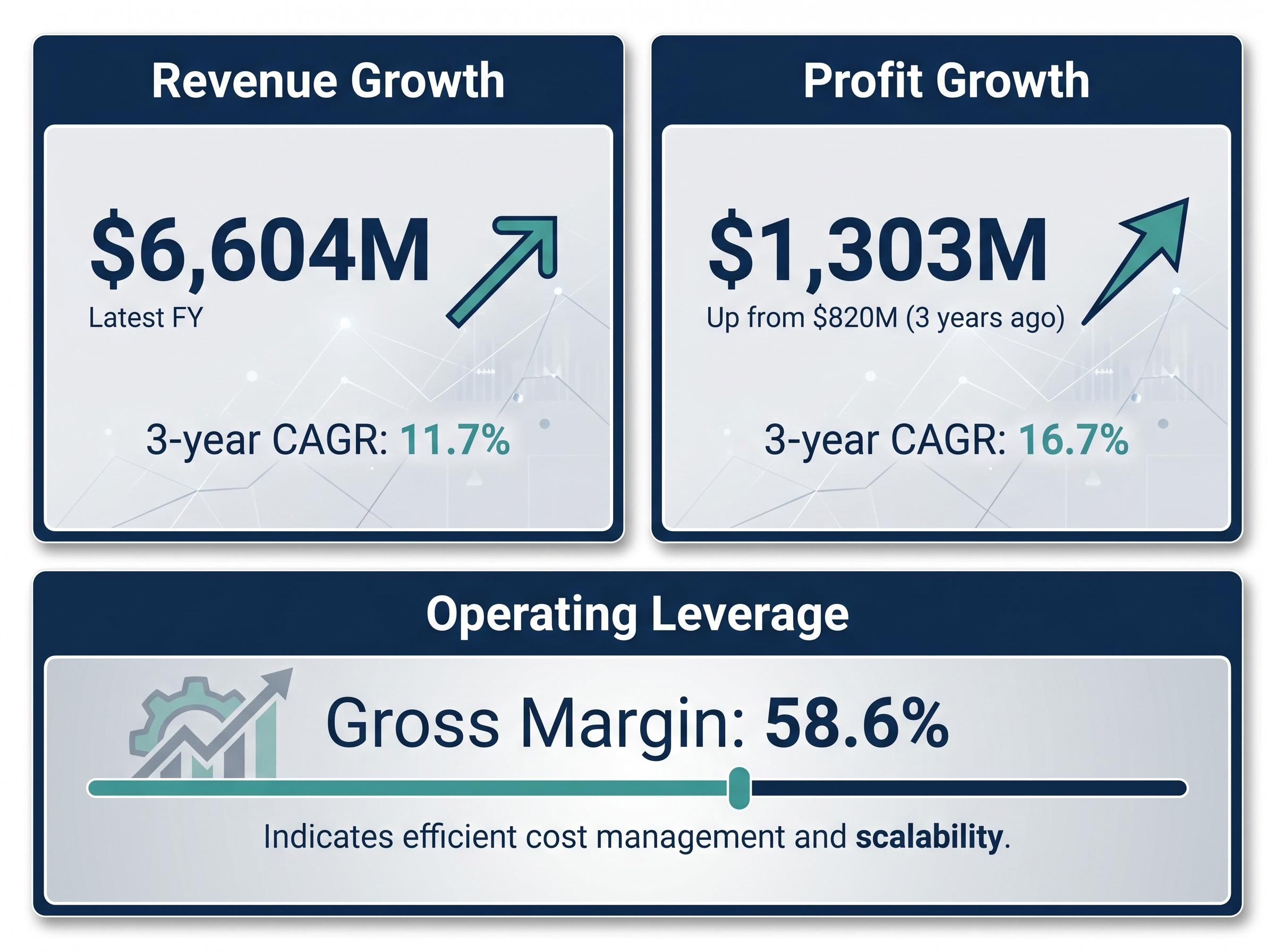

Aristocrat Leisure has grown revenue at 11.7% per year for three consecutive years and delivered profit of $1,303 million in its most recently reported financial year. Yet the Aristocrat Leisure share price has fallen 13% since the start of 2026. That kind of separation between business performance and market pricing is precisely what fundamental analysts look for.

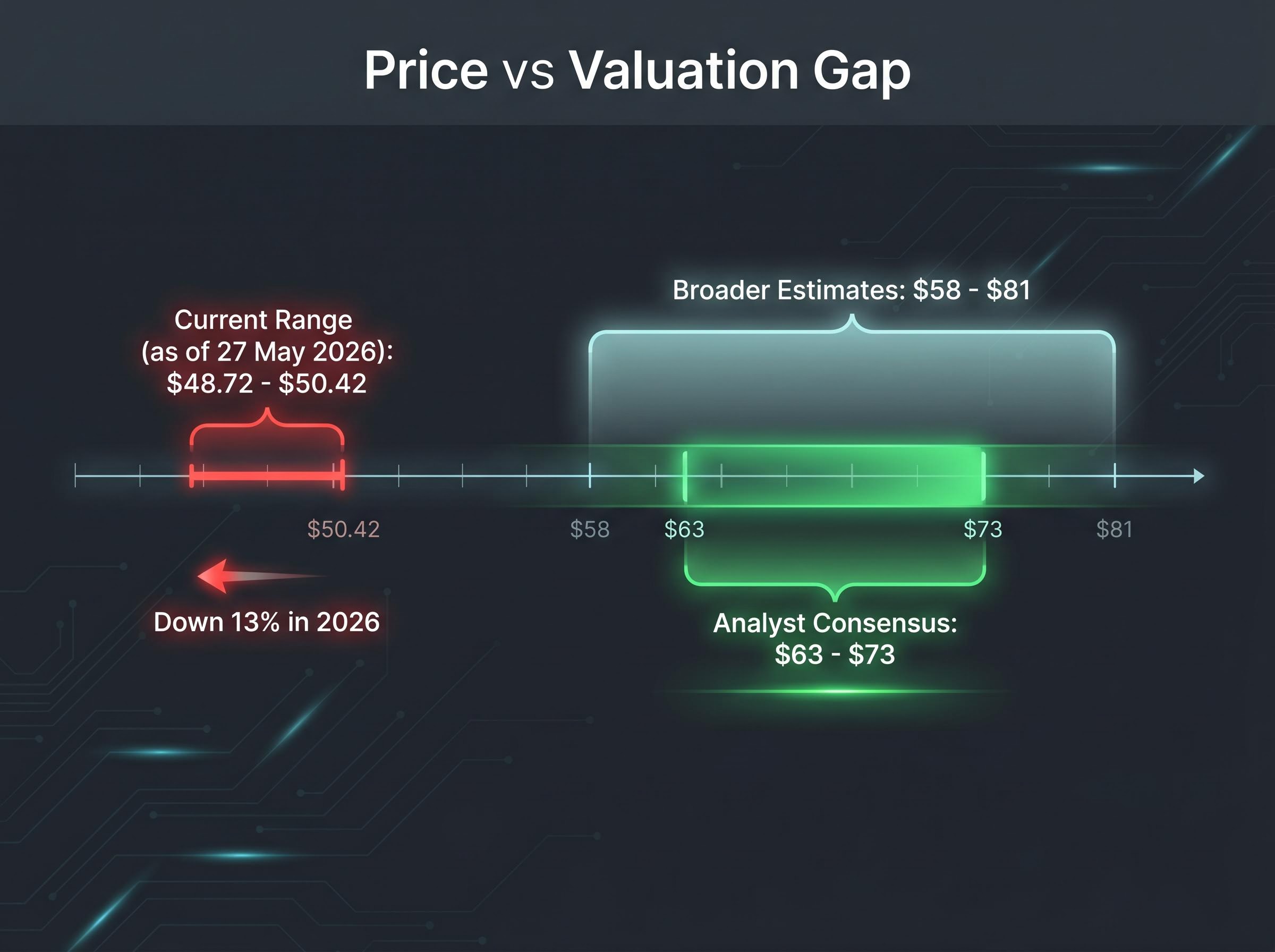

As of 27 May 2026, ALL trades around $48.72-$50.42 on the ASX, well below analyst consensus price targets that cluster in the $63-$73 range, according to broker estimates. A half-year result released just weeks ago (on 13 May 2026) showed a 16% surge in normalised net profit after tax and amortisation (NPATA), the company’s preferred profit measure. The gap between reported performance and market pricing is worth interrogating.

What follows uses Aristocrat as a live case study to walk through the core disciplines of fundamental analysis: understanding the business model, reading financial metrics, assessing balance sheet health, and separating business quality from valuation as two distinct questions. Readers will finish with a framework applicable to any ASX blue-chip and a grounded view of where Aristocrat sits right now.

What Aristocrat actually does, and why the model matters

Founded in 1953 by Len Ainsworth and headquartered in Sydney, Aristocrat Leisure is Australia’s largest gaming machine manufacturer and one of the top-tier global slot manufacturers. The company operates across two broad segments, and the mix between them shapes earnings quality in ways that matter for any investor assessment.

Land-based gaming

Aristocrat designs, manufactures, and distributes physical gaming machines to casino operators and venues worldwide. Two commercial arrangements define how revenue flows from this segment:

- Outright sale: The operator purchases the machine and Aristocrat books the revenue at the point of sale, a one-off transaction.

- Revenue-sharing (participation): Aristocrat retains ownership of the machine, places it on the operator’s floor, and takes an ongoing share of the machine’s earnings, generating recurring income over the machine’s useful life.

The revenue-sharing model is the more analytically significant of the two. It creates a predictable, recurring income stream tied to machine performance rather than to the timing of a single transaction.

Digital gaming

Aristocrat’s online and mobile gaming operations have grown to represent close to half of total company revenue. This is a structural shift in the business, not simply a product extension. A company that earns nearly half its revenue from digital operations carries a different risk and growth profile than a pure hardware manufacturer: digital scales differently, carries different margin characteristics, and opens addressable markets that physical distribution cannot reach.

When big ASX news breaks, our subscribers know first

Three years of financial results that are hard to ignore

The trajectory tells its own story. Aristocrat reported revenue of $6,604 million in its most recent financial year, the result of a 11.7% compound annual growth rate (CAGR) over three years. CAGR measures the smoothed annual growth rate over a multi-year period, stripping out the noise of any single year’s result and revealing the underlying trend.

Profit tells a sharper story. From $820 million three years ago to $1,303 million in the most recently reported year, profit has compounded at 16.7% annually. That profit is growing faster than revenue signals margin expansion: the company is extracting more profit from each dollar of revenue as it scales. Gross margin, the percentage of revenue retained after direct costs, sits at 58.6%, a level that reflects strong pricing power and cost discipline at the core business level before overheads are considered.

Profit CAGR: 16.7% over three years. When profit compounds faster than revenue, it signals that operating leverage is working in the company’s favour, a hallmark of a business that scales efficiently.

The most recent half-year result reinforced the trend. HY2026 NPATA grew 16%, announced on 13 May 2026, indicating the trajectory has not stalled.

Aristocrat’s HY26 results showed normalised NPATA of $794 million (up 16.3% in constant currency), a 13.6% dividend increase, and an expanded EBITA margin of 36.9%, with management reaffirming full-year NPATA growth guidance and setting a US$1 billion Interactive Revenue Target for FY29.

| Metric | Value | What it signals |

|---|---|---|

| Revenue (latest FY) | $6,604M | Scale of the business at current run-rate |

| Revenue CAGR (3-year) | 11.7% | Consistent double-digit top-line growth |

| Gross margin | 58.6% | Strong pricing power and cost discipline |

| Profit (latest FY) | $1,303M | Absolute profit generation capacity |

| Profit CAGR (3-year) | 16.7% | Margin expansion; profit growing faster than revenue |

Consistent double-digit revenue growth combined with profit accelerating ahead of it is the signature of a compounding business. Readers who learn to read a CAGR trajectory, rather than fixating on a single year’s result, are better equipped to distinguish cyclical noise from structural quality.

Reading the balance sheet, debt, and return on equity

Strong revenue and profit figures paint an encouraging picture from the income statement. The balance sheet asks a different question: can the financial structure sustain and amplify that profitability?

Three metrics frame the answer for Aristocrat:

- Net debt: $1,449 million. Net debt measures total borrowings minus cash on hand. For a company generating over $1.3 billion in annual profit, this level represents a manageable obligation rather than a structural burden.

- Debt-to-equity ratio: 38.3%. This means shareholder equity exceeds total debt, a position generally considered more comfortable than the reverse. A ratio below 100% indicates the business is not over-leveraged relative to the capital its shareholders have invested.

- Return on equity (ROE): 20.0% (FY2024). ROE measures how efficiently a company converts shareholder capital into profit. A figure above 15% is typically considered strong for an ASX-listed industrial or technology business.

ROE of 20.0%. A return on equity at this level signals that management is deploying shareholder capital efficiently, generating $0.20 of profit for every $1.00 of equity in the business.

Aristocrat also maintains an active on-market share buy-back programme. Reports indicate a new programme of up to $750 million was announced, though the specific details of this programme have not been independently verified. Buy-backs reduce outstanding shares and can signal management confidence in the company’s intrinsic value.

A company can look impressive on revenue and profit metrics while carrying debt levels that create fragility. Checking the balance sheet alongside the income statement is a discipline that separates thorough analysis from surface-level assessment.

For investors wanting to move beyond ratios into the full mechanics of reading a financial statement, our dedicated guide to ASX balance sheet analysis walks through working capital, debt-to-equity calculation, and book value per share with sector-specific benchmarks and the five most common mistakes Australian retail investors make.

What the share price decline actually tells us (and what it does not)

Aristocrat’s share price has fallen approximately 13% year-to-date as of 27 May 2026, trading in the $48.72-$50.42 range. Analyst consensus price targets, based on broker estimates that have not been independently verified, cluster between $63 and $73, with the broader range spanning approximately $58 to $81.

That gap is significant. It is also not, on its own, a buy signal.

A 13% decline in a fundamentally strong business is a reason to look more closely at valuation. It is not a reason to assume the market is wrong. Markets can reprice a quality business for reasons that do not appear in the income statement: sector rotation, macroeconomic sentiment, liquidity shifts, or changes in the discount rate investors apply to future earnings.

The risks driving the current discount include Australian electronic gaming machine regulatory reform, post-pandemic digital engagement normalisation, unproven iGaming scale at meaningful revenue, and foreign exchange exposure across Aristocrat’s predominantly USD-earning operations, factors that sector-rotation selling alone does not fully explain.

The core principle: Business quality and share price performance are two separate questions. Conflating them is one of the most common errors retail investors make.

A fundamental analyst asks two distinct questions:

- Quality assessment: Is this a well-run business with sustainable competitive advantages and a strong financial profile?

- Valuation assessment: Is the current market price attractive relative to what the business is worth?

Answering “yes” to the first question does not automatically answer the second. The share price decline makes the valuation question more interesting, but the quality assessment must be completed before the valuation question can be meaningfully addressed.

The fundamentals of fundamental analysis, explained through Aristocrat’s case

Fundamental analysis is the practice of assessing a company’s intrinsic value by examining its financial health, business model, competitive position, and growth trajectory, rather than focusing on share price movements alone. Aristocrat’s current situation provides a useful framework for applying this discipline.

The process follows a logical sequence:

- Understand the business model. What does the company do, and how does it generate revenue? Aristocrat’s mix of one-off sales, recurring revenue-sharing, and digital operations tells an investor about earnings predictability and growth levers.

- Assess financial performance. Revenue growth, profit growth, and gross margin together indicate whether a business is scaling efficiently. Aristocrat’s 11.7% revenue CAGR, 16.7% profit CAGR, and 58.6% gross margin collectively signal a business that is growing and expanding margins simultaneously.

- Check balance sheet health. ROE and net debt function as a paired check on whether growth is being funded sustainably. A 20.0% ROE alongside net debt of $1,449 million (in a business generating $1,303 million in annual profit) suggests the growth is not being purchased through excessive leverage.

- Evaluate valuation separately. This is the final step, not the first.

Reading the metrics as a connected picture

No single metric tells the full story. Revenue growth without profit growth may indicate a company spending to buy market share. Profit growth with deteriorating margins may reflect cost-cutting rather than genuine demand. The metrics gain meaning when read together as a system.

Why valuation is the final question, not the first

Even a high-quality business can be a poor investment if acquired at an excessive price. The reverse is equally true: a short-term share price decline does not invalidate a business’s fundamentals. Aristocrat’s 13% year-to-date decline sits alongside the strongest half-year profit growth the company has reported in recent periods. The quality question and the price question require separate answers.

Aristocrat’s trajectory points in one direction, but further research is required

The evidence assessed in this analysis points in a consistent direction. The positive signals identified include:

- Revenue compounding at 11.7% annually over three years

- Profit growing faster than revenue, with a 16.7% CAGR

- Gross margin of 58.6%, indicating strong core business economics

- Manageable net debt relative to profit generation

- ROE of 20.0%, signalling efficient capital deployment

- An active buy-back programme suggesting management confidence in the company’s value

What this analysis has not assessed:

- A full discounted cash flow or comparable company valuation

- Whether the current share price represents fair value, a discount, or a premium

- The specific drivers behind the 13% year-to-date share price decline

- Competitive dynamics or regulatory risks that could alter the growth trajectory

Further research is required before forming an investment view. Identifying a quality business is only half the analytical process; determining whether the current price offers value requires a separate, rigorous valuation assessment.

Two upcoming dates could materially inform the picture: the 2026 Investor Briefing on 1 July 2026 and the FY2026 Full-Year Results on 12 November 2026. Both represent opportunities for the company to confirm whether the current growth trajectory is sustained.

Investors wanting to build out the valuation assessment that this analysis deliberately leaves open will find our full explainer on multi-method ASX valuation, which walks through a structured five-step sequence combining P/S screening, EV/EBITDA benchmarking, DCF, and DDM with a worked example that shows how each method cross-checks the others.

The fundamentals are strong, but the investment case is still being written

This analysis has moved through the analytical sequence: business model understood, financial metrics assessed, balance sheet evaluated, and the distinction between price and value established. Aristocrat’s three-year financial trajectory demonstrates the characteristics of a compounding business, with profit growth outpacing revenue growth, strong margins, manageable debt, and efficient capital deployment.

No investment decision should rest on fundamentals alone without a parallel valuation assessment. The 13% share price decline makes that valuation question more pressing, not less. Investors considering Aristocrat would benefit from tracking the 1 July 2026 Investor Briefing and the 12 November 2026 full-year results as the next natural tests of whether the trajectory holds.

The framework applied here, moving from business model to financial performance to balance sheet to valuation, is not specific to Aristocrat. It is the discipline of fundamental analysis itself, applicable to any ASX-listed company where the numbers invite closer examination.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.