Aristocrat Leisure’s share price sits roughly 31% below its 52-week high of A$73.29, yet the analyst consensus 12-month price target of approximately A$63.04 implies around 25% upside from late May 2026 levels. For a company that has nearly doubled its net profit over three years and maintains a return on equity of approximately 20%, the gap between where the stock trades and where the Street thinks it belongs is not easily explained by earnings deterioration alone. This article unpacks the financial record behind the pullback, explains how Aristocrat’s shift toward digital revenue changes its earnings quality profile, and provides a framework for investors weighing whether the discount reflects structural risk or a repricing opportunity in a fundamentally sound business.

A 31% gap from peak to present: what the share price chart is actually telling us

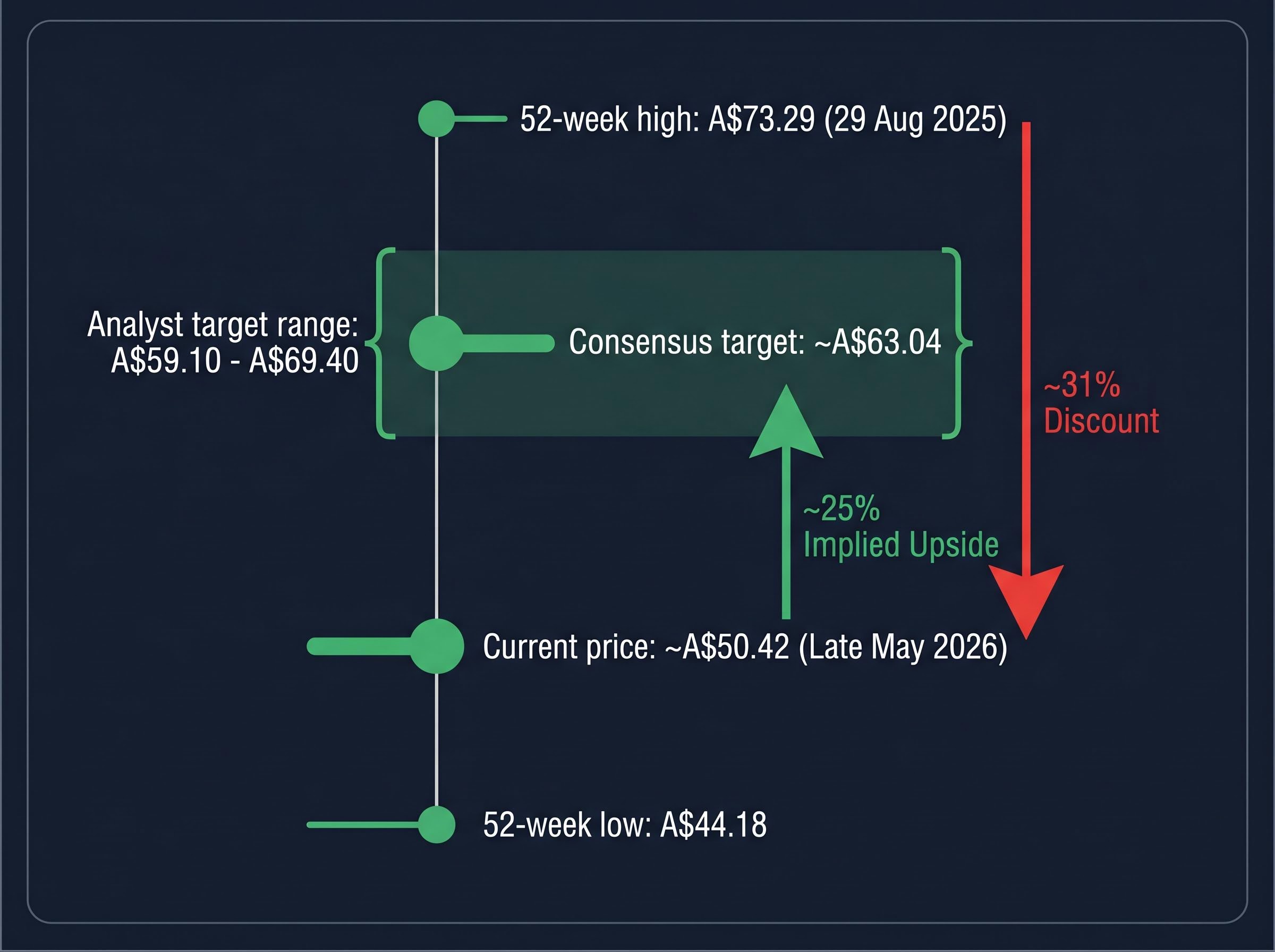

Aristocrat Leisure (ASX: ALL) closed near A$50.42 in late May 2026, a figure that carries more weight when measured against three reference points:

- Current share price: approximately A$50.42 (late May 2026)

- 52-week high: A$73.29 (reached 29 August 2025)

- 52-week low: A$44.18

The distance from peak to present is significant. A 31% drawdown from the August high places the stock closer to its 52-week floor than its ceiling. Yet the analyst community has not followed the share price down.

The analyst consensus 12-month price target sits at approximately A$63.04, with a range of A$59.10 to A$69.40, implying roughly 25% upside from current levels. Multiple brokers maintain Overweight or Outperform ratings.

That divergence is the analytical puzzle. If the fundamentals had deteriorated in lockstep with the share price, the broker consensus would reflect it. The fact that price targets remain materially above the current level suggests the pullback is driven by something other than an earnings collapse.

| Metric | Value |

|---|---|

| Share price (late May 2026) | ~A$50.42 |

| 52-week high | A$73.29 (29 August 2025) |

| 52-week low | A$44.18 |

| Discount to 52-week high | ~31% |

| Analyst consensus 12-month target | ~A$63.04 (range A$59.10–A$69.40) |

| Implied upside | ~25% |

When big ASX news breaks, our subscribers know first

Three years of compounding: how Aristocrat’s financials earned its premium status

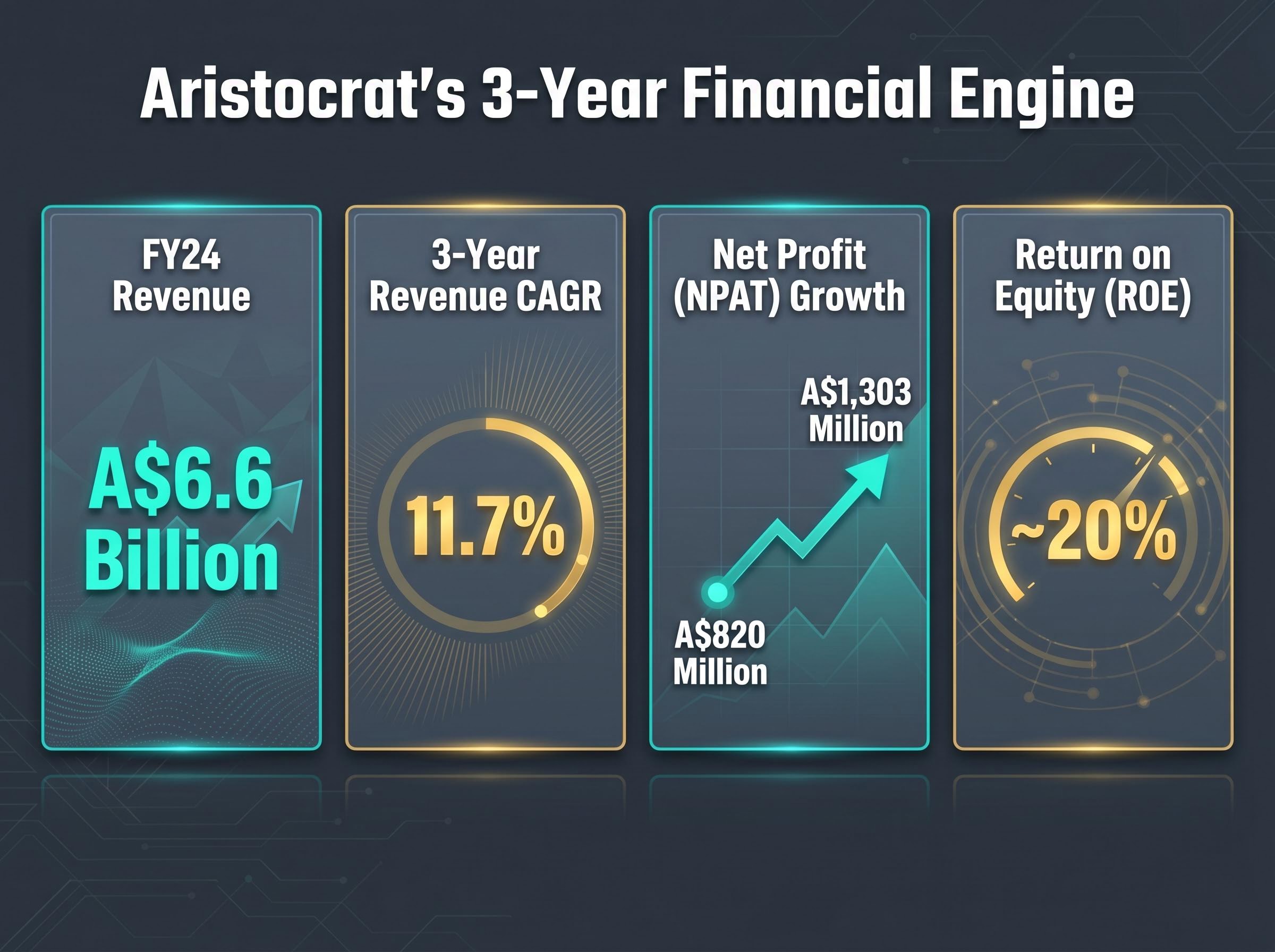

The financial record over three fiscal years tells a story of consistent acceleration rather than a single strong quarter. FY24 group revenue reached A$6,604 million (A$6.6 billion), underpinned by a three-year annualised revenue growth rate of 11.7%. For a company operating in a mature industry, double-digit compounding at this scale is uncommon.

Net profit after tax (NPAT) moved from A$820 million to A$1,303 million over the same three-year period, a near-doubling that demonstrates operating leverage, not just top-line expansion. Cash generation remained strong enough to fund both dividends and buybacks without straining the balance sheet.

Four data points capture the pattern:

- Revenue: A$6.6 billion in FY24, growing at 11.7% annualised over three years

- NPAT: from A$820 million to A$1,303 million across the same period

- ROE: approximately 20%

- Capital management: consistent cash generation supporting dividends and share buybacks

This is the trajectory that earned Aristocrat its premium market status. It is also the trajectory that makes the current 31% discount difficult to reconcile with fundamental performance alone.

The HY26 results confirmed that the financial trajectory visible in the FY24 annual record has continued into the current period, with normalised NPATA up 16.3% in constant currency and recurring revenue exceeding 70% of group revenue, making the share price weakness difficult to attribute to any deterioration in reported earnings.

Why ROE of 20% matters for a gaming company of this size

Return on equity (ROE) measures how effectively a company converts the capital shareholders have invested into profit. An ROE of approximately 20% means that for every dollar of equity on the balance sheet, Aristocrat generated roughly 20 cents in annual profit.

For a large-cap business, 20% ROE sits meaningfully above the cost of capital. It signals that reinvested earnings are generating real incremental returns rather than simply maintaining scale. In a capital-intensive segment like land-based gaming manufacturing, where hardware development and distribution consume significant resources, sustaining 20% ROE across a growth cycle points to disciplined capital allocation, not just revenue expansion.

From slot machines to smartphones: understanding Aristocrat’s transformed business model

Aristocrat built its reputation on physical gaming machines, but the company that exists today earns its revenue through two distinct models operating across physical and digital channels.

The first model is outright machine sales: a casino operator purchases a gaming cabinet, and Aristocrat recognises revenue at the point of sale. This produces lump-sum, front-loaded income that is inherently tied to hardware replacement cycles and casino capital expenditure budgets. When operators pull back on capex, this revenue line contracts.

The second model is participation arrangements: Aristocrat retains ownership of the machine, places it on a casino floor, and earns a share of the gaming revenue it generates. This produces recurring, smoother income that is less sensitive to capex cycles and more predictable over time.

| Model Type | Revenue Recognition | Earnings Predictability | Example Context |

|---|---|---|---|

| Outright machine sale | Lump-sum at point of sale | Lower; tied to operator capex cycles | Casino purchases 200 new cabinets |

| Participation arrangement | Ongoing revenue-sharing | Higher; recurring income stream | Casino shares gaming revenue with Aristocrat per machine |

The shift that many investors underestimate is how far the digital transformation has already progressed. Mobile and online gaming now accounts for close to half of total group revenue in FY24. Aristocrat describes itself as a “global gaming content and technology company and mobile games publisher,” a self-characterisation that reflects reality rather than aspiration. The company’s fiscal year ends 30 September.

Land-based gaming peers such as Ainsworth Game Technology illustrate the contrast clearly: Ainsworth generated CY25 revenue of $290.8 million growing at 10%, but its underlying profit before tax fell 9% and recurring revenue represented only 34% of group revenue, compared to Aristocrat’s recurring revenue base exceeding 70% of group revenue in the most recent half.

Pixel United and the digital revenue engine

Aristocrat’s digital division, Pixel United, historically encompassed Product Madness, Big Fish, and Plarium. Following the divestiture of Plarium in November 2024, the remaining portfolio focuses on social casino, role-playing, and strategy games.

FY24 Pixel United bookings reached US$1.745 billion, broadly flat year-on-year. Within that figure, social casino bookings exceeded US$1 billion for the first time, a milestone that demonstrates the durability of the core franchise even as post-pandemic engagement has normalised.

The margin story is where the real signal sits. Pixel United’s Adjusted EBITDA margin reached 36% in FY24, up 410 basis points year-on-year. That improvement came through optimised user acquisition spend and lower overhead costs, meaning profitability expanded even without bookings growth. Flat revenue with rising margins is a sign of a maturing digital business improving unit economics.

What the market is pricing in: risks behind the discount

A 31% pullback on a high-ROE, double-digit-growth business does not happen without identifiable concerns. Four risk categories, ranked by approximate near-term earnings relevance, offer the most plausible explanation:

- Domestic regulatory tightening: Australian states, particularly New South Wales, are advancing electronic gaming machine (EGM) reforms including cashless gaming mandates, pre-commitment cards, reduced maximum bets, and stricter anti-money-laundering obligations. Any tightening directly affects Aristocrat’s domestic machine sales volumes and participation revenue.

- Digital competition and normalisation: Pixel United operates alongside global publishers including Playtika, Zynga, and major Chinese studios. Post-COVID normalisation of mobile engagement has moderated bookings growth, with FY24 bookings at US$1.745 billion broadly flat year-on-year.

- Execution on online real-money gaming: Aristocrat’s expansion into iGaming and iLottery platforms remains a forward-looking bet. Markets typically price such initiatives with caution until proof of scale emerges.

- FX and macro exposure: With a material share of revenue denominated in US dollars, currency movements create volatility in reported AUD results. Broader discretionary sector caution adds a cyclical layer.

The NSW Gaming Reform Roadmap, delivered by the Independent Panel on Gaming Reform in November 2024, established the trajectory for cashless gaming implementation and harm-reduction mandates across the state, providing the clearest legislative signal yet of the compliance costs and revenue constraints facing EGM operators and suppliers like Aristocrat.

Aristocrat’s own risk disclosures consistently flag Australian EGM reform as a material risk factor, particularly reforms around cashless gaming and pre-commitment mandates across multiple states.

These risks are not abstract. Each has a specific earnings transmission mechanism, and the market appears to be pricing some combination of all four into the current discount.

The U.S. opportunity and digital growth as the long-side of the ledger

The same regulatory environment creating domestic headwinds is opening a substantially larger addressable market offshore. In the United States, tribal and commercial casino expansion across Class II and Class III markets continues as a structural tailwind. At the 2026 Indian Gaming Tradeshow and Convention (NIGA) in March 2026, Aristocrat debuted new Class II games and system solutions, signalling ongoing investment in this growth corridor.

Five catalysts sit on the long side of the ledger:

- Digital monetisation growth through Pixel United margin expansion and online real-money gaming scaling

- U.S. regulatory liberalisation via state-by-state iGaming and online sports betting legalisation

- New game and cabinet cycles driving replacement demand in land-based markets

- Capital management activity (dividends and buybacks) supported by consistent cash generation

- U.S. tribal and commercial casino expansion broadening the installed base

The Pixel United margin trajectory reinforces this view. A 36% Adjusted EBITDA margin, up 410 basis points in FY24, demonstrates that digital earnings quality is improving even as bookings growth has plateaued. Higher margins on a stable revenue base translate directly to improved free cash flow conversion.

Why iGaming legalisation in the U.S. matters specifically for Aristocrat

State-by-state iGaming legalisation creates a direct revenue opportunity that goes beyond Aristocrat’s existing social and free-to-play digital income. The current Pixel United model generates bookings from in-app purchases in free-to-play games. Real-money online gaming, by contrast, earns regulated wager-based revenue, a fundamentally different and potentially higher-value income stream.

The distinction matters because it represents a shift in revenue type, not just revenue volume. If online real-money gaming scales successfully, Aristocrat adds a third earnings pillar alongside land-based hardware and digital free-to-play, one that operates within regulated frameworks and carries its own margin and growth profile.

Discount or value gap: what the numbers suggest for investors weighing entry now

The quantitative signals, taken together, present a coherent picture. A 31% discount to the 52-week high. Approximately 25% implied upside to the analyst consensus target of A$63.04. A 20% ROE. An 11.7% three-year revenue CAGR. Net profit nearly doubled from A$820 million to A$1,303 million. Multiple brokers maintaining Overweight or Outperform ratings with price targets above spot.

The price-to-sales discount of approximately 16% below Aristocrat’s five-year historical average captures a dimension of the valuation gap that P/E comparisons alone can miss; when a company’s revenue growth rate remains at 11.7% annualised while its revenue multiple compresses, the implied earnings yield on future sales improves materially for investors buying at current levels.

The investor question is not whether Aristocrat is a strong business. The financial record suggests it is. The question is whether the unresolved risks are adequately compensated by the current discount.

| Dimension | Bull Case | Bear Case |

|---|---|---|

| Financial record | Near-doubled NPAT, 20% ROE, 11.7% revenue CAGR | Growth rate may decelerate from elevated base |

| Growth optionality | U.S. iGaming, digital margin expansion, new game cycles | iGaming execution unproven at scale |

| Key risk | Australian regulation priced in; U.S. tailwinds offset | Regulatory tightening could structurally impair domestic revenue |

| Market signal | Broker consensus implies ~25% upside; Overweight ratings | Market discount may reflect information not yet in consensus |

Some risks are cyclical and likely to normalise: broad macro sentiment and post-COVID digital engagement moderation fall into this category. Others are structural and harder to price: Australian regulatory reform and execution on real-money online gaming carry genuine uncertainty about long-term earnings impact.

The discount is real, but so is the fundamental record. For investors conducting their own analysis, the central question is whether the market has over-corrected relative to identifiable fundamentals, or whether it is pricing in structural risks that consensus has not yet fully absorbed.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

31% below its peak, but not below its fundamentals

Aristocrat Leisure’s financial record, double-digit revenue growth, near-doubled net profit, 20% ROE, and improving digital margins, describes a structurally sound business. Nothing in the FY24 data or the company’s forward-looking disclosures suggests a deterioration that would justify a permanent re-rating of the share price.

Regulatory and competitive risks are real and should not be dismissed. Australian EGM reform carries genuine uncertainty for domestic revenue, and the iGaming expansion remains a forward-looking bet without proof of scale. These are legitimate reasons for the market to demand a discount.

Analyst consensus and broker ratings, however, suggest the correction has overshot relative to fundamental value. The frameworks outlined in this article, the dual revenue model, the risk taxonomy, and the growth catalyst inventory, provide a structured basis for investors to form their own view on whether the current discount represents a window or a warning.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.