How the Hormuz Closure Drives Oil Prices and Inflation

2 mins ago

ANZ declared an 83-cent interim dividend on 1 May 2026, franked at 75%, payable 1 July. At a trailing yield of approximately 4.8%, the stock now sits above every other Big Four bank on raw income return. For income investors weighing whether that headline number translates into a genuine portfolio advantage, the answer depends on franking mechanics, capital support, analyst conviction, and the rising rate environment that has pushed six-month term deposits to 4.46%. This analysis breaks down each layer of ANZ’s dividend profile, from grossed-up yield calculations to the divided broker consensus, and builds a framework for deciding whether the income case justifies a position.

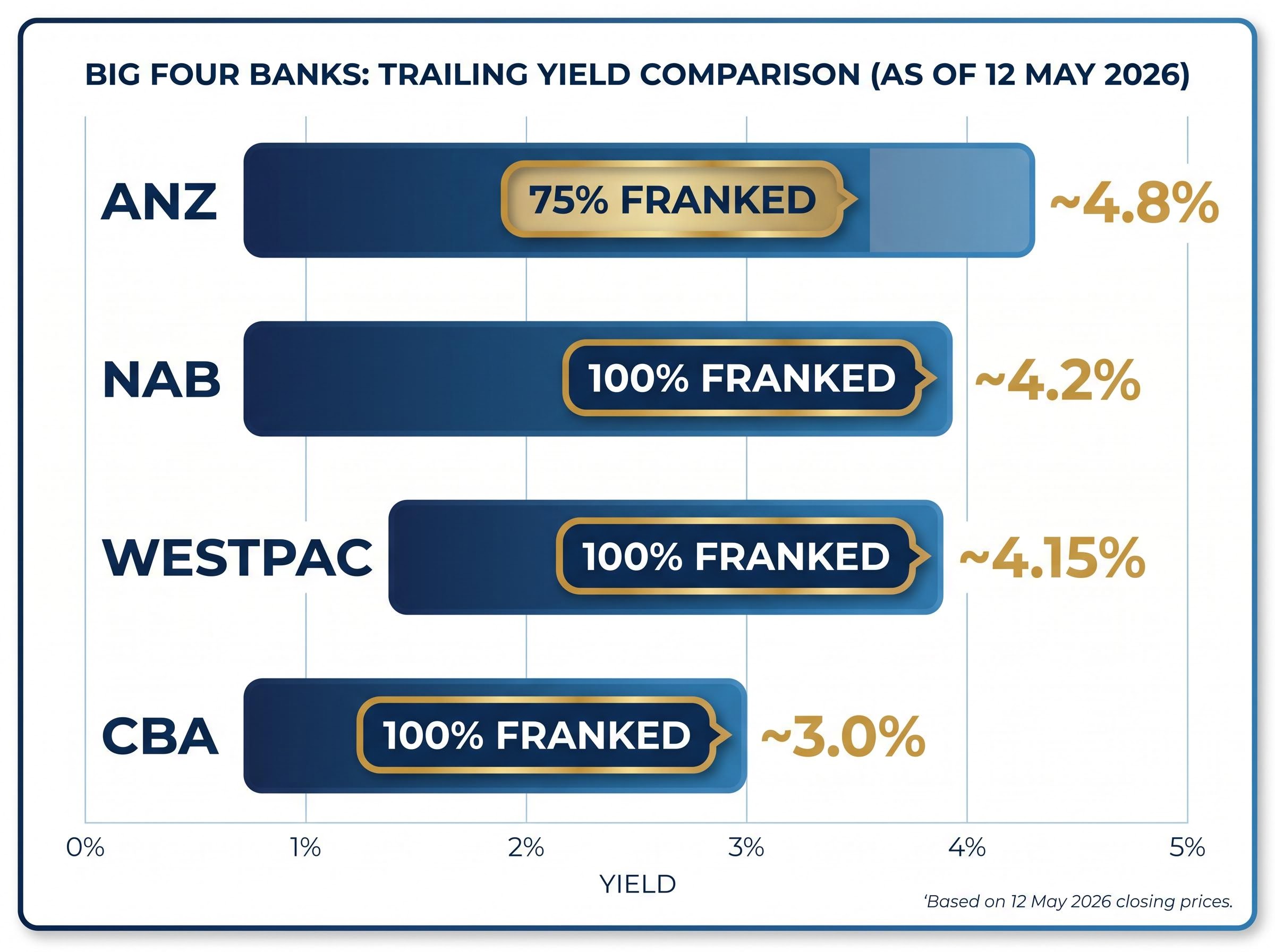

On a trailing basis, ANZ offers the highest yield among Australia’s major banks. The gap is not trivial: 4.8% versus 4.2% for NAB, 4.15% for Westpac, and 3.0% for CBA, based on 12 May 2026 closing prices.

The complication arrives one line down the table. CBA, NAB, and Westpac all pay 100% franked dividends. ANZ pays at 75%.

| Bank | Trailing Yield | FY2026 DPS Forecast | Franking Level |

|---|---|---|---|

| ANZ | ~4.8% | $1.66-$1.68 | 75% |

| CBA | ~3.0% | ~$4.95 | 100% |

| NAB | ~4.2% | ~$1.70 | 100% |

| Westpac | ~4.15% | ~$1.53 | 100% |

That franking difference changes the after-tax comparison materially, depending on who is receiving the dividend.

Franking credits represent tax already paid at the corporate level. A 100% franked dividend carries the full corporate tax offset; a 75% franked dividend carries three-quarters of it.

For an SMSF in pension phase (zero tax rate), franking credits are fully refundable. ANZ’s higher raw yield partially offsets the smaller credit, and the effective after-refund return narrows the gap with NAB and Westpac considerably. For an investor at the 32.5% marginal rate, the grossed-up yield on ANZ’s 4.8% at 75% franking sits below what a 100% franked 4.2% yield from NAB delivers after the full credit is applied. At the 47% top marginal rate, the shortfall widens further; the tax offset from full franking becomes increasingly valuable as the marginal rate rises.

The yield headline is real. The ranking, once adjusted for tax position, is not automatic.

For SMSF trustees and individual investors who want to work through the exact numbers, our dedicated guide to franking credit calculations covers the 30/70 formula in full, with worked examples showing how a $1,000 fully franked dividend becomes $1,428.57 of effective value for pension-phase members receiving the ATO cash refund.

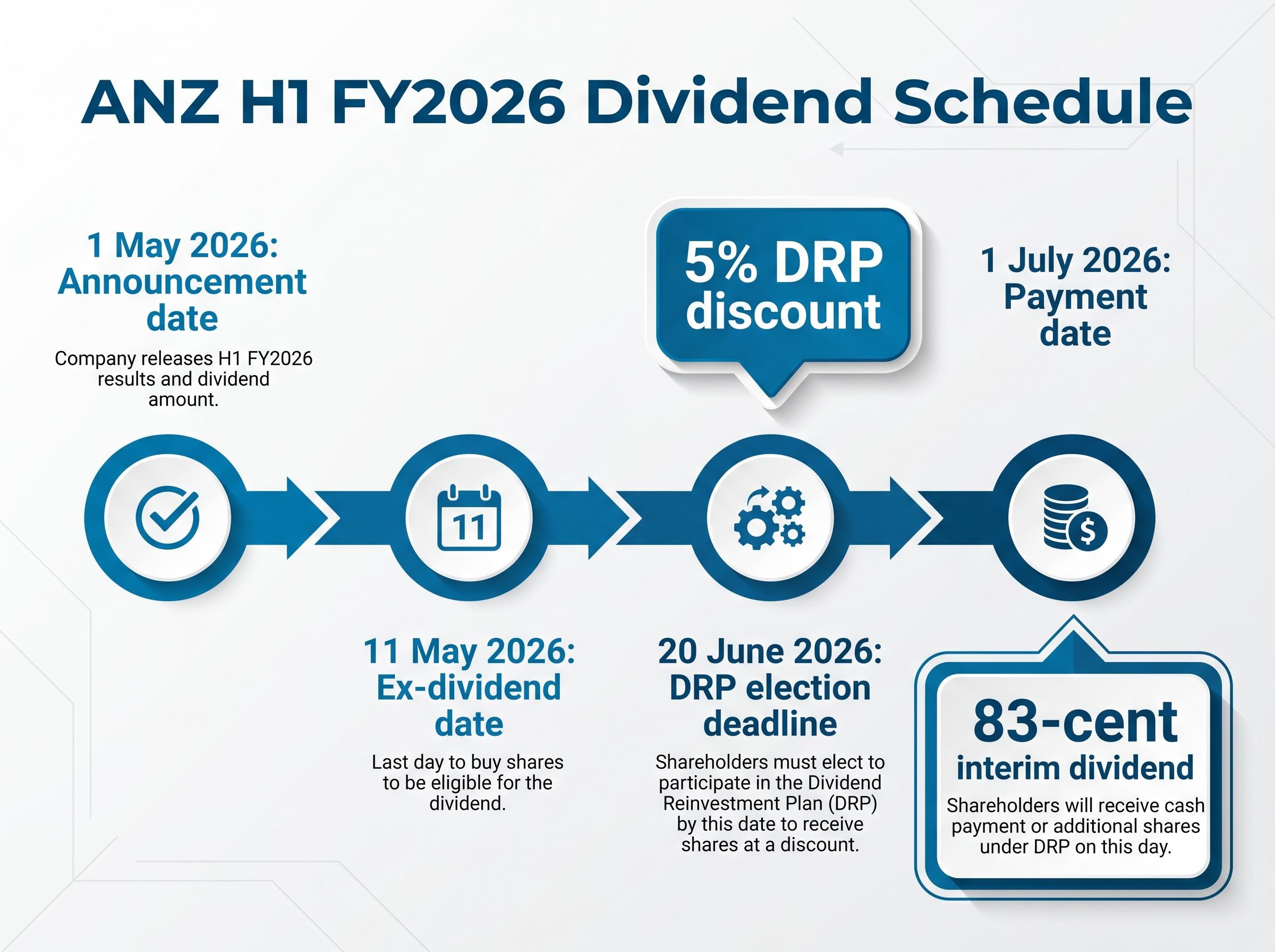

The 83-cent payout did not arrive from a stretched balance sheet. ANZ’s H1 FY2026 results, announced 1 May 2026, showed the bank operating with considerable headroom.

Key H1 FY2026 metrics:

The Suncorp acquisition, completed 31 July 2024, was the primary scale driver behind the profit surge. Integration costs of approximately $150 million were absorbed within the half, and $300 million in annual cost savings are targeted by mid-2026.

Capital Position ANZ’s CET1 ratio stood at 12.4% as of 31 March 2026, up 36 basis points from September 2025. A further 30-50 basis points of improvement is expected from Suncorp synergies by year-end.

That 12.4% CET1 ratio sits comfortably above regulatory minimums and supports the 75% payout ratio without requiring the bank to retain additional capital. Even if revenue growth moderates from here, the 22% reduction in operating expenses provides dividend headroom that did not exist twelve months ago.

APRA’s capital buffer requirements for Australian authorised deposit-taking institutions specify a Common Equity Tier 1 conservation buffer of 2.5–3.75%, plus an additional 1.0% loading for Domestic Systemically Important Banks, which means ANZ’s 12.4% CET1 ratio sits with meaningful headroom above the effective regulatory floor.

ANZ pays dividends semi-annually. The 83-cent interim has been maintained since July 2024, and the FY2026 consensus forecast of $1.66-$1.68 implies a matching final payment later this year.

The franking level itself has moved: the current 75% represents a 5 percentage point increase from the prior payment’s 70%, signalling improving franking credit capacity within the group.

Key dates for the H1 FY2026 interim dividend, in order:

Investors who did not hold shares before the 11 May ex-dividend date will not receive the July payment. The next actionable deadline is 20 June, the cut-off for electing into the dividend reinvestment plan.

ANZ’s DRP offers a 5% discount to the market price, with no brokerage or administration fees. For long-term holders, that discount compounds: each reinvested dividend acquires more shares than a market-price purchase would, and those additional shares generate their own dividends in subsequent periods.

Participation has been climbing. FY2025 saw approximately 22% of eligible shares enrolled, up from 18% in FY2024. The increase suggests a growing cohort of shareholders treating ANZ as a compounding income position rather than a trading one. A Bonus Option Plan also exists as an alternative reinvestment mechanism for eligible shareholders.

A six-month term deposit currently pays approximately 4.46%. ANZ yields approximately 4.8%. The gap looks narrow, but the two income sources operate on entirely different terms.

A term deposit offers a guaranteed, non-frankable return. The principal is protected, the rate is locked, and there is no capital upside or downside. When the term expires, the investor receives exactly what was promised.

A Big Four bank dividend offers semi-annual cash flow with franking credits attached, DRP optionality at a discount, and exposure to the underlying share price. That exposure cuts both ways: ANZ’s share price sits approximately 21% above its level twelve months ago, meaning total return has significantly exceeded the yield-only figure. If conditions reverse, the same exposure works against the income investor.

| Income Source | Gross Yield | Tax Treatment | Capital Upside | Liquidity |

|---|---|---|---|---|

| ANZ Dividend | ~4.8% | 75% franked | Yes (equity exposure) | Daily (ASX-traded) |

| 6-Month Term Deposit | ~4.46% | Fully taxable, no franking | None | Locked until maturity |

| NAB Dividend | ~4.2% | 100% franked | Yes (equity exposure) | Daily (ASX-traded) |

The RBA raised the cash rate to 4.35% on 5 May 2026, the third consecutive hike. In this environment, SMSF investors benefit most from the ANZ yield: franking credits are fully refundable for zero-tax entities, which enhances the effective return above the term deposit rate even at 75% franking. For investors in higher tax brackets, the term deposit’s guaranteed nature and simplicity may close the gap entirely once the franking discount is applied.

The RBA cash rate target of 4.35%, effective from the May 2026 decision, sets the benchmark against which term deposit rates are priced, and the narrowing gap between the 4.46% six-month deposit rate and ANZ’s 4.8% equity yield reflects how aggressively the rate cycle has compressed the traditional income premium of bank shares over deposit products.

The comparison requires a like-for-like, tax-adjusted framework. A raw rate comparison between 4.8% and 4.46% understates the structural differences between the two.

Sixteen analysts cover ANZ. The consensus price target sits at approximately ~$37.07–$37.50, implying roughly 8% upside from the $34.48 closing price as of mid-May 2026.

Analyst Consensus The consensus price target of ~$37.07–$37.50 across 16 analysts implies approximately 8% upside from current levels, a modest premium that reflects the market’s view that ANZ is close to fair value.

The distribution tells a more layered story. Eight analysts rate the stock as a hold. Six carry buy or strong buy ratings. Two rate it sell or strong sell. The spread between the lowest target ($24.96) and the highest ($41.50) is unusually wide for a Big Four bank.

Bank share valuation frameworks that combine the Dividend Discount Model with price-to-book and ROE analysis produce a wider range of fair value estimates than any single metric alone, which partly explains why the analyst target spread for ANZ extends from $24.96 to $41.50 depending on the assumptions applied to net interest margin trajectory.

The bear target implies a roughly 28% drawdown from current levels. A move of that magnitude would not just impair total return; it would likely signal fundamental deterioration severe enough to prompt a dividend review.

Individual broker positions as of May 2026:

Recent share price context: ANZ fell 1.88% to $34.48 on the day, down approximately 7% over the prior week and 5% year-to-date, while remaining up 21% year-on-year.

The disagreement is not primarily about near-term dividend sustainability. Buy-rated brokers including Macquarie, Morgan Stanley, and UBS all describe the dividend as secure, with the Suncorp integration viewed as non-dilutive to payout capacity.

The divergence centres on post-Suncorp integration execution risk and the net interest margin trajectory in a rising rate environment. Bears see margin compression as a structural risk that the current earnings surge has masked. Bulls see cost synergies and variable-rate loan repricing as tailwinds that extend the earnings runway. For income investors, the distinction matters: dividend sustainability has broad analyst agreement, but the capital risk profile does not.

The components of the income case are clear. A 4.8% trailing yield, the highest in the Big Four. A FY2026 DPS forecast of $1.66-$1.68, supported by a 75% payout ratio and a 12.4% CET1 ratio. A DRP offering compounding at a 5% discount. And a rising rate environment where term deposits at 4.46% are closer competitors than they were twelve months ago.

Three investor profiles fit ANZ’s income characteristics well:

Investors exploring how to construct a position around ANZ’s income characteristics alongside complementary holdings will find our full explainer on building an ASX dividend portfolio, which covers sector diversification across franking levels, DRP compounding mechanics, payout ratio sustainability screens, and ex-dividend date sequencing for consistent quarterly income flow.

Three conditions would weaken the income case:

Forward Income Marker The CommSec FY2027 DPS forecast of $1.72 implies continued, if modest, dividend growth beyond the current fiscal year, though forward estimates remain subject to earnings trajectory and payout policy decisions.

ANZ’s 4.8% yield is the highest among the Big Four, backed by a 12.4% CET1 ratio, 70% cash profit growth, and a credible Suncorp integration story. The income case is supported by substance, not just the headline number.

It is also incomplete without two adjustments. The 75% franking discount means the after-tax comparison with NAB and Westpac depends entirely on the investor’s tax position. The grossed-up yield calculation is the first step, not an optional one. The second is the 20 June 2026 DRP election deadline for those intending to reinvest the July payment at a 5% discount.

The analyst consensus is divided, and the $24.96 bear target cannot be ignored. Income investors who understand it as an outlier execution scenario, rather than a base case, have grounds for holding with conviction. Those who dismiss it entirely accept a capital risk they have not priced.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

ANZ's current interim dividend is franked at 75%, meaning it carries three-quarters of the corporate tax offset rather than the full amount paid by CBA, NAB, and Westpac at 100% franking. This matters because your effective after-tax return from ANZ's dividend depends on your marginal tax rate, and at higher tax brackets the full franking offered by peers can outweigh ANZ's higher raw yield.

ANZ's H1 FY2026 interim dividend of 83 cents per share is payable on 1 July 2026, with an ex-dividend date of 11 May 2026 and a dividend reinvestment plan election deadline of 20 June 2026.

ANZ offers a trailing yield of approximately 4.8% versus a six-month term deposit rate of around 4.46%, but the comparison is not straightforward because ANZ's dividend carries 75% franking credits and equity capital risk, while a term deposit provides a guaranteed, fully taxable return with no share price exposure.

ANZ's dividend reinvestment plan offers a 5% discount to the market price with no brokerage or administration fees, allowing long-term holders to acquire additional shares below market value and compound their income position over time.

Sixteen analysts cover ANZ, with a consensus price target of approximately $37.07 to $37.50, implying around 8% upside from the mid-May 2026 closing price of $34.48; however, individual targets range from a bear case of $24.96 to a bull case of $41.50, reflecting disagreement over post-Suncorp integration execution and net interest margin trajectory.