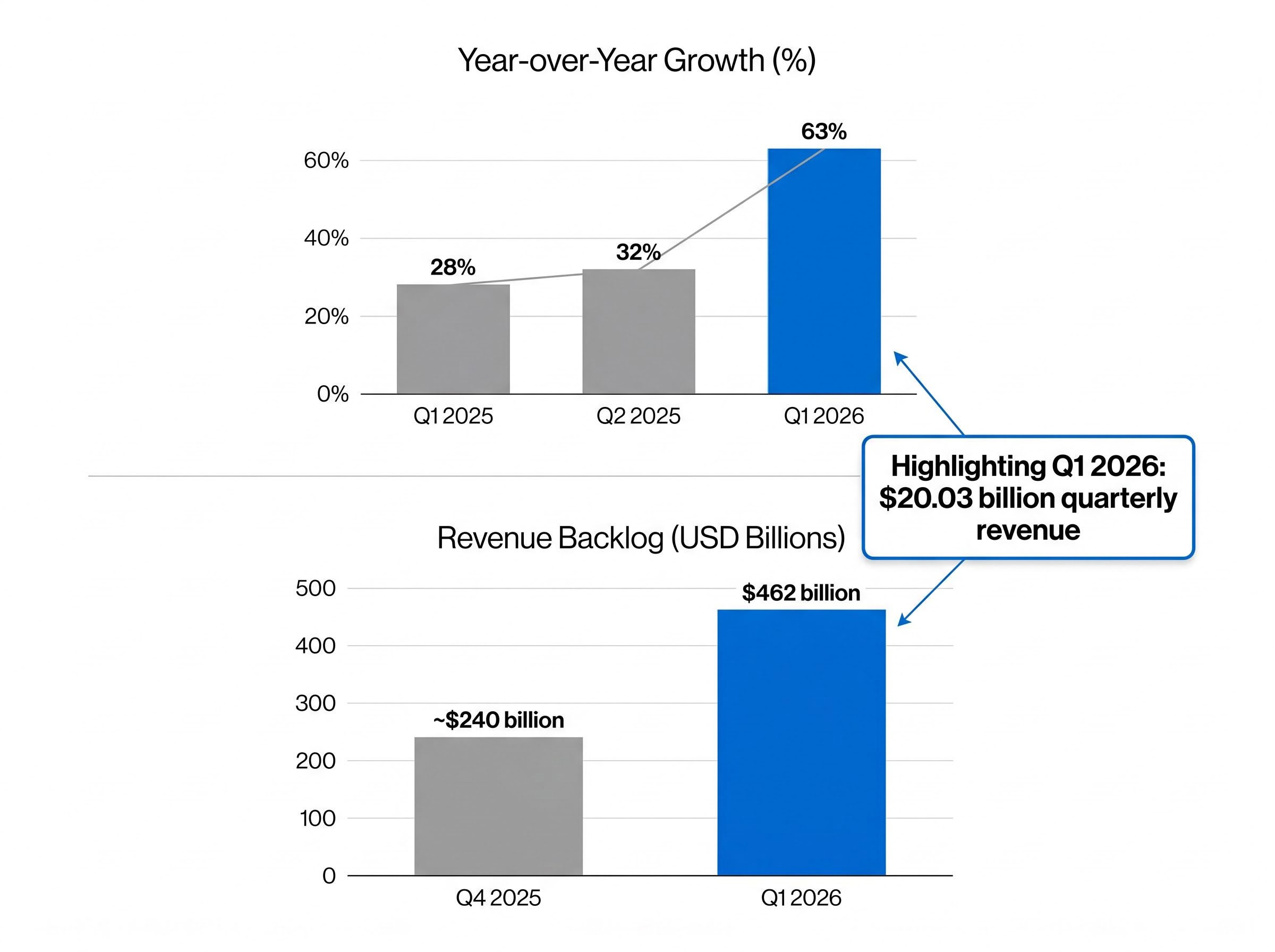

Google Cloud’s revenue backlog doubled sequentially to $462 billion in a single quarter, with management confirming that more than $230 billion converts to recognised revenue within 24 months. That is not a pipeline number. It is a structural reorientation of Alphabet’s revenue mix.

Alphabet reported Q1 2026 total revenue of $109.9 billion, up 22% year-over-year, with earnings per share of $5.11, an 82% increase. But the headline results are almost beside the point. The story investors are now pricing is whether Google Cloud Platform’s (GCP) 63% growth rate and near-800% generative AI revenue expansion represent a durable inflection or a demand pull-forward that flatters the near-term numbers. With GOOGL trading at $400.27 as of 13 May 2026, up approximately 35% year-to-date, the market has already moved. The question is whether the fundamentals justify holding or adding at current levels.

This analysis unpacks the five variables that determine whether the cloud inflection is sufficient to reframe Alphabet as an AI infrastructure company: the backlog mechanics, the margin story, the competitive spread versus AWS and Azure, the capex trade-off, and the investment case implied by current valuation.

From 28% to 63%: what the cloud acceleration actually means

GCP’s growth rate has not simply risen. It has compressed into a trajectory that looks less like incremental improvement and more like a demand curve bending upward under enterprise AI adoption pressure.

The sequence matters:

- Q1 2025: approximately 28% year-over-year growth

- Q2 2025: approximately 32% year-over-year growth

- Q1 2026: 63% year-over-year growth, with quarterly revenue reaching $20.03 billion

That $20.03 billion quarterly figure implies a cloud business running at roughly $80 billion annualised, before any backlog conversion effect is applied. A year ago, GCP was growing at the pace of a maturing cloud platform. Today, it is accelerating at a rate that exceeds its own prior peak.

Generative AI product revenue within GCP grew approximately 800% year-over-year in Q1 2026, according to Alphabet’s earnings disclosure.

That 800% figure is striking, but its significance lies in what it signals about enterprise behaviour rather than its headline scale. Enterprises are not experimenting with AI workloads on GCP; they are making multi-year infrastructure commitments, the kind that lock in revenue well beyond the current reporting period and distinguish between momentum and structural re-rating.

Alphabet’s AI repricing thesis rests on a distinction that most search-era valuation frameworks miss: the company is not layering AI onto a search business but deploying a vertically integrated stack across chip design, cloud infrastructure, and consumer AI products that each compound the others.

The backlog confirms it. Contracted but unrecognised revenue doubled from approximately $240 billion in Q4 2025 to $462 billion in Q1 2026. Understanding what that number actually means, and what it does not, is where the analysis sharpens.

When big ASX news breaks, our subscribers know first

The $462 billion backlog decoded: conversion mechanics, timeline, and revenue implications

A cloud backlog figure represents contracted revenue that has not yet been recognised on the income statement. It is not a pipeline, not a letter of intent, and not a forecast. It is money under contract, awaiting delivery and recognition.

That distinction matters because backlog figures across the industry vary enormously in quality. Some reflect short-term consumption commitments; others reflect multi-year infrastructure deals with built-in escalation clauses. What makes GCP’s $462 billion figure unusual is not the absolute number alone but the rate at which it accumulated.

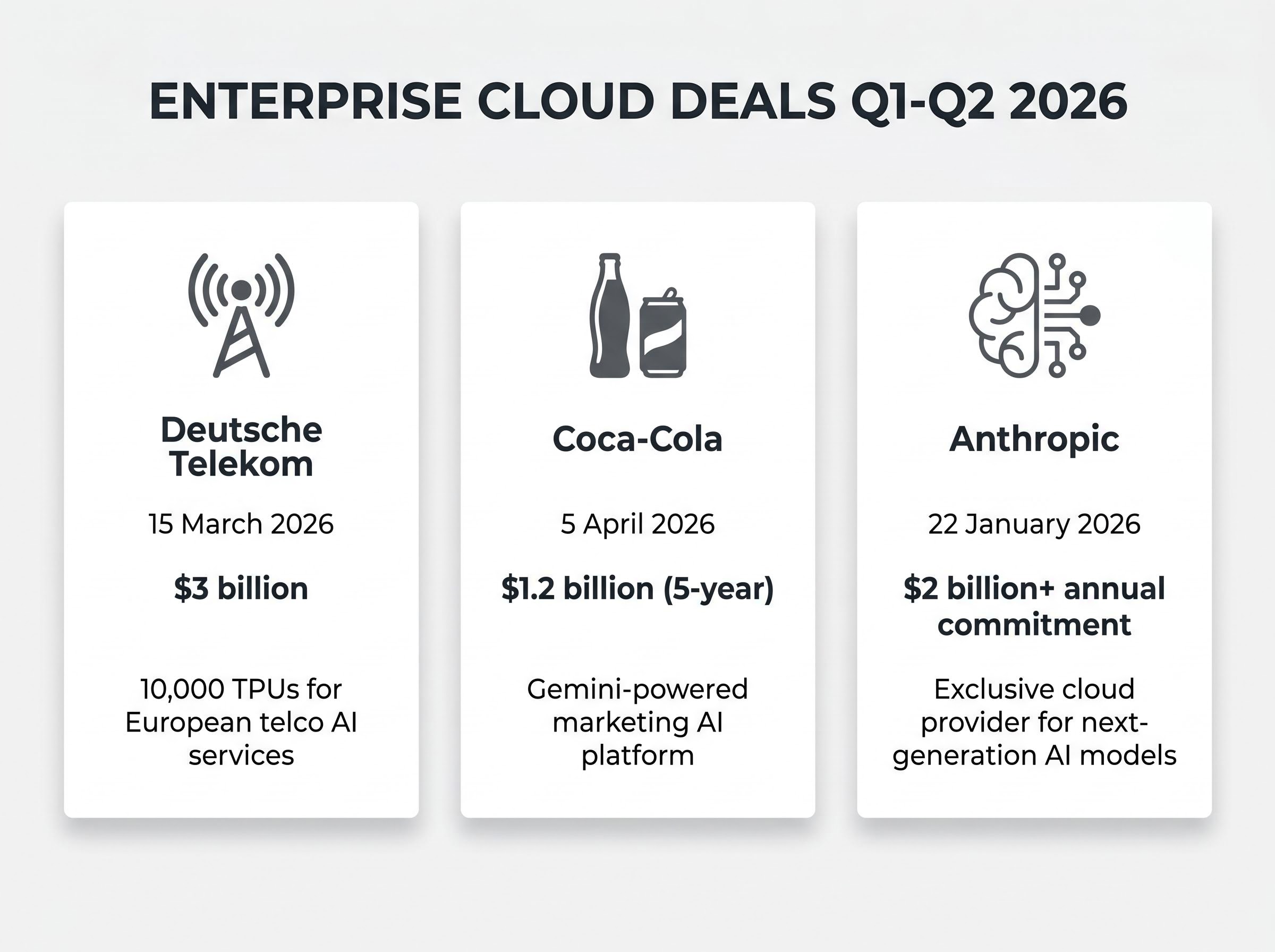

The backlog approximately doubled in a single quarter, from roughly $240 billion at the end of Q4 2025. Several named enterprise contracts contributed to that acceleration:

| Contract Party | Announcement Date | Deal Value | Deal Focus |

|---|---|---|---|

| Deutsche Telekom | 15 March 2026 | $3 billion | AI infrastructure, including 10,000 TPUs for European telco AI services |

| Coca-Cola | 5 April 2026 | $1.2 billion (5-year) | Gemini-powered marketing AI platform |

| Anthropic | 22 January 2026 | $2 billion+ annual commitment (projected) | Exclusive cloud provider for next-generation AI models |

Note: Deal values reflect publicly disclosed figures where available, as reported in Alphabet’s Q1 2026 10-Q filing and associated earnings materials.

What $230 billion in 24-month conversion implies for Alphabet’s revenue mix

CEO Sundar Pichai confirmed during the Q1 2026 earnings call on 29 April 2026 that more than 50% of the backlog is expected to convert to recognised revenue within 24 months. That implies approximately $230 billion or more in near-term conversion, translating to roughly $115 billion per year in recognised cloud revenue from backlog alone.

The market responded accordingly. FY2026 consensus cloud revenue estimates were revised upward approximately 22% to $105.2 billion, from a pre-earnings consensus of $86.3 billion, according to FactSet data. That revision signals institutional confidence that conversion execution is achievable, though the question of whether the conversion rate holds under delivery pressure remains an open one.

The margin transformation that changes Alphabet’s financial identity

GCP’s operating margin in Q1 2026 reached 32.9%, generating $6.6 billion in operating income. For a cloud segment that was running at low-to-mid single-digit margins in prior years and approximately 18% in the year-ago period, the expansion is not incremental.

Three factors are driving the shift:

- AI compute supply-demand tightness: Demand for AI training and inference capacity currently exceeds available supply, supporting pricing power across hyperscaler platforms.

- Enterprise contract mix: Longer, higher-value deals (such as the Deutsche Telekom and Coca-Cola commitments) carry more favourable unit economics than consumption-based workloads.

- Proprietary TPU deployment: Alphabet’s tensor processing units reduce reliance on third-party GPU procurement, improving infrastructure cost efficiency.

Goldman Sachs (30 April 2026) characterised cloud operating income tripling as “a game-changer for Alphabet’s multiple expansion.”

The comparison within Alphabet’s own segment hierarchy adds context. Google Services operates at approximately 45% margins, reflecting the high-margin economics of search and advertising. Cloud’s 32.9% is meaningfully below that, but the gap has compressed from more than 40 percentage points to roughly 12 in under two years.

There is a nuance worth noting. The supply-demand tightness in AI compute that currently supports cloud pricing could ease as hyperscaler capacity expands through 2026 and 2027. If it does, the margin tailwind becomes a potential margin headwind. Investors modelling sustained 30%+ cloud margins may be assuming a supply constraint that is, by design, temporary.

How GCP’s 63% growth compares with AWS and Azure, and what the gap signals

All three major hyperscalers grew cloud revenue in Q1 2026. The question is not whether the category is expanding but who is gaining disproportionately, and what that tells investors about where enterprise AI infrastructure spend is flowing.

| Provider | Q1 2026 Revenue | YoY Growth | Operating Income / Margin | Backlog / RPO |

|---|---|---|---|---|

| GCP | $20.03B | 63% | $6.6B / 32.9% | $462B (doubled QoQ) |

| Azure | ~$42B (est.) | ~40% | Not disclosed | AI revenue +60% YoY |

| AWS | ~$37.6B (implied) | 28% | $14.2B | RPO $140B (+20% YoY) |

AWS retains the highest absolute operating income at $14.2 billion, reflecting its more mature, larger-scale business. Azure has held steady at approximately 40% growth for three consecutive quarters. GCP’s 63% represents the sharpest acceleration among the three, and the sequential backlog doubling has no direct parallel in AWS or Azure disclosures.

Three structural explanations underpin GCP’s relative outperformance:

- Proprietary TPU infrastructure reduces cost per AI training run, attracting workloads from GPU-constrained competitors

- Anthropic exclusive cloud designation channels one of the largest independent AI model developers onto GCP infrastructure

- Gemini Enterprise integration across the Google Workspace install base creates a distribution channel for AI services that neither AWS nor Azure replicates directly

JPMorgan raised its price target to $460 in May 2026, citing GCP’s outpacing of both peers as validation of the backlog. Morgan Stanley characterised cloud acceleration as structural rather than cyclical. The market share shift story, for a business that was the third-place hyperscaler as recently as 2023, is becoming harder to dismiss.

The capex trade-off: what $180-190 billion in annual spending means for free cash flow and returns

The cloud inflection has a cost, and it is not a small one.

Q1 2026 capital expenditure reached $35.7 billion, approximately 2x year-over-year. Full-year 2026 guidance stands at $180-190 billion, with approximately 70% earmarked for cloud AI infrastructure. That is the largest capital commitment in Alphabet’s history.

The hyperscaler capex trajectory extends well beyond Alphabet’s own commitment: combined 2026 spending across Amazon, Microsoft, Alphabet, and Meta is projected at approximately $725 billion, with analysts estimating a $1 trillion annual run rate by 2027, a scale that raises structural questions about debt-funded infrastructure sustainability across the entire sector rather than at any single company.

The capex falls into three primary categories:

- AI data centre buildout: approximately 70% of total, including 12 new AI data centres brought online since Q1 2025

- TPU and GPU procurement: securing compute capacity for enterprise AI demand

- Network and connectivity infrastructure: supporting data transfer and latency requirements across global regions

The free cash flow impact is direct. Free cash flow declined approximately 50% year-over-year in Q1 2026. For a company whose buyback programme has been a meaningful contributor to EPS growth in prior years, that compression constrains near-term shareholder returns.

An Oracle OCI integration announced on 12 December 2025, targeting a $10 billion joint backlog opportunity, provides a partial offset to capex concentration risk by distributing some infrastructure demand across a multi-cloud arrangement. But the core tension remains.

What suppressed free cash flow means for shareholder returns in 2026

Reduced free cash flow compresses near-term buyback capacity. Management has indicated that elevated capex is expected to continue, meaning the free cash flow headwind is not a one-quarter event but a multi-year investment cycle condition.

The backlog provides revenue visibility, but converting $462 billion in contracts into margin-accretive recognised revenue depends on infrastructure scaling on time and on budget. That is a multi-year execution risk, and it is the most concrete near-term pressure point in the cloud investment thesis.

At $400 and 29x forward earnings, does the cloud inflection justify the valuation?

GOOGL trades at approximately 29.4x forward earnings as of 12 May 2026, with a market capitalisation of roughly $5 trillion. Analyst price targets from Goldman Sachs ($450) and JPMorgan ($460) imply 12-15% upside from current levels, requiring either continued P/E expansion or meaningful forward earnings upgrades.

Alphabet’s EPS mechanics in Q1 2026 were substantially inflated by a one-time equity gain of approximately $36.9 billion, meaning the headline $5.11 per share figure overstates core operational performance; on an adjusted basis, EPS came in closer to $2.62, just below the $2.63 consensus estimate, a distinction that changes the valuation entry point calculation for investors modelling normalised earnings power.

The investment case at current levels is not binary. It depends on which conditions materialise:

- Base case: Cloud revenue converts at the consensus rate (approximately $105 billion FY2026), Google Services remains stable at 16%+ growth, and capex peaks within 12-18 months. GOOGL trades in line with analyst targets.

- Bull case: Cloud outperforms consensus, search antitrust remedies are behavioural rather than structural, and AI infrastructure demand sustains 30%+ cloud margins. Bullish five-year scenarios suggest a path toward approximately 100% upside.

- Bear case: Department of Justice antitrust remedies in the search monopoly case (ruled August 2024 by Judge Amit Mehta) or the ad tech monopoly case (ruled April 2025) result in structural remedies that reduce Google Services revenue. AI-native competitors erode search query volume before cloud revenue scales sufficiently to offset. Bearish five-year scenarios imply approximately 50% potential downside.

Morgan Stanley characterised “cloud acceleration as structural rather than cyclical, with the $462B backlog implying multi-year AI revenue visibility exceeding AWS.”

The antitrust variable deserves explicit framing. Remedies proceedings in both cases remain ongoing as of May 2026; no asset divestiture has been ordered to date. Sell-side analysts at Goldman Sachs have broadly characterised the proceedings as “headline risk, not fundamental,” though structural remedies, if imposed, could alter the calculation materially.

The DOJ remedies proceedings against Google, addressed by Assistant Attorney General Gail Slater in remarks that explicitly cited both the search monopoly ruling and the April 2025 ad tech decision, underscore that structural intervention remains an active government priority rather than a resolved backstory.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Reframing Alphabet: advertising giant with a cloud option, or AI infrastructure company with an advertising legacy?

The data is now on the table. The question is what it adds up to.

Google Services, encompassing search, YouTube (which generated $9.9 billion in advertising revenue in Q1 2026, up 10.7%), and subscriptions (350 million total paid subscribers, up from 325 million at the end of the prior year), still accounts for roughly 80%+ of total quarterly revenue. Cloud at $20.03 billion represents approximately 18% of the $109.9 billion quarterly total.

Those proportions ground the reframing question in reality. Alphabet is not yet an AI infrastructure company by revenue composition. However, the trajectory is moving faster than the current mix suggests.

If the 24-month backlog conversion executes at the implied rate, cloud could approach 35-40% of total revenue within two years. FY2026 cloud consensus of $105.2 billion against total Alphabet revenue already implies cloud approaching 25% for the full year. JPMorgan’s top pick designation explicitly frames the investment thesis around GCP validating Alphabet’s identity as an AI infrastructure platform.

Three threshold conditions would confirm identity reframing rather than diversification:

- Cloud exceeds 30% of total revenue on a sustained basis

- Cloud operating income exceeds Google Services operating income within five years

- A post-antitrust environment where search distribution costs are structurally lower

The antitrust uncertainty makes the reframing question time-sensitive. If search distribution remedies reduce Google Services revenue, cloud’s relative contribution rises not just through growth but through base shrinkage, a structurally different dynamic.

The variables that determine which narrative wins

Cloud’s projected share of total revenue in FY2026 at approximately $105 billion against estimated total Alphabet revenue represents a meaningful step toward the infrastructure narrative. Yet Google Services margins of approximately 45% still exceed cloud’s 32.9%, so the overall margin impact of cloud share gains depends on how quickly cloud margins converge upward. The speed of that convergence, not the backlog number alone, determines whether the identity shift becomes self-evident in Alphabet’s financial profile.

The Magnificent Seven valuation spread places Alphabet at approximately 29x earnings, the lowest multiple in the group, despite its cloud growth rate exceeding every peer; that discount reflects the market still partially pricing Alphabet as a search and advertising business rather than as an AI infrastructure platform where the backlog provides multi-year revenue visibility that chip-cycle-dependent peers cannot match.

The inflection is real. Whether the price reflects it is the harder question.

Google Cloud’s $462 billion backlog, 63% growth rate, and 32.9% operating margin represent a genuine inflection in Alphabet’s business mix. The sell-side consensus revisions, 22% upward on FY2026 cloud estimates, reflect institutional recognition that this is not a cyclical quarterly beat.

At 29.4x forward earnings with analyst targets of $450-$460 and GOOGL already up 35% year-to-date, the cloud story is partially priced. The remaining upside depends on whether the backlog conversion rate holds and capex peaks within the expected 12-18 month window.

The framing question investors can use to make their own assessment: is the cloud inflection large enough, fast enough, and margin-accretive enough to offset a scenario where antitrust remedies and AI-native search competition pressure the Google Services base? The backlog says the opportunity is real. The $180-190 billion capex commitment says it is expensive. The answer sits somewhere between the two.

—