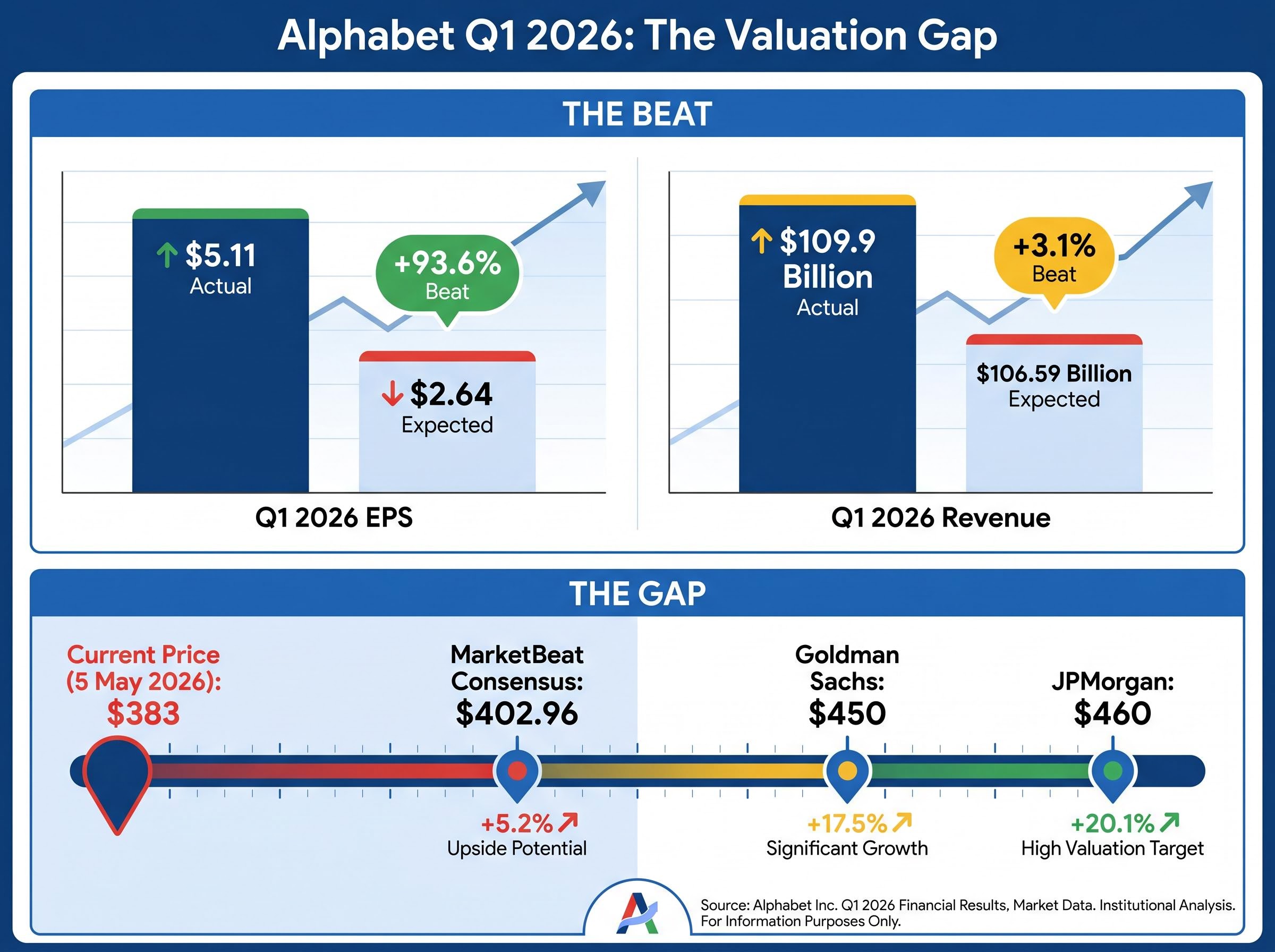

Alphabet just reported Q1 2026 earnings of $5.11 per share against a consensus estimate of $2.64. That is not a modest beat. It is a recalibration of what Wall Street thought the company could earn in a single quarter. While Nvidia and Broadcom trade at premium multiples on pure semiconductor AI exposure, Alphabet’s post-earnings picture raises a different kind of question: where does AI value actually accrue once the chips are built and the models are running? Revenue came in at $109.9 billion, above the $106.59 billion the Street expected, yet the stock trades near $383 as of 5 May 2026, below the average analyst target. This analysis examines why Alphabet’s AI investment case differs structurally from chip-focused plays, unpacking its cloud acceleration, autonomous vehicle lead, and quantum computing optionality as three compounding forces operating across distinct time horizons.

The earnings beat that reframes how investors should think about Alphabet

The scale of the miss in Street expectations is worth sitting with. Analysts expected $2.64 in earnings per share. Alphabet delivered $5.11.

Q1 2026 EPS: $5.11 actual versus $2.64 expected, a beat of approximately 94%.

Revenue of $109.9 billion cleared the $106.59 billion consensus by more than $3 billion. The stock has gained roughly 35% year-to-date, yet at approximately $383.25, it remains below every major post-earnings price target. Goldman Sachs raised its target to $450. JPMorgan went to $460. The MarketBeat consensus across 53 analysts sits at $402.96.

| Source | Price Target | Rating |

|---|---|---|

| Goldman Sachs | $450 | Buy |

| JPMorgan | $460 | Overweight |

| MarketBeat Consensus | $402.96 | Moderate Buy (53 analysts) |

| StockAnalysis Consensus | $390.49 | Strong Buy (45 analysts) |

Of 66 analysts surveyed by S&P Global, 59 rate the stock Buy or Strong Buy, an 89% bullish consensus. The question that frames everything that follows is straightforward: why does a company that just nearly doubled the consensus EPS estimate still trade below what most analysts believe it is worth?

The Magnificent 7 earnings divergence in late April 2026 illustrated precisely this dynamic: Alphabet surged to an all-time high on the same reporting cycle that sent Meta down more than 9%, as the market began pricing each hyperscaler’s capex-to-revenue conversion speed individually rather than treating AI spending as a unified trade.

When big ASX news breaks, our subscribers know first

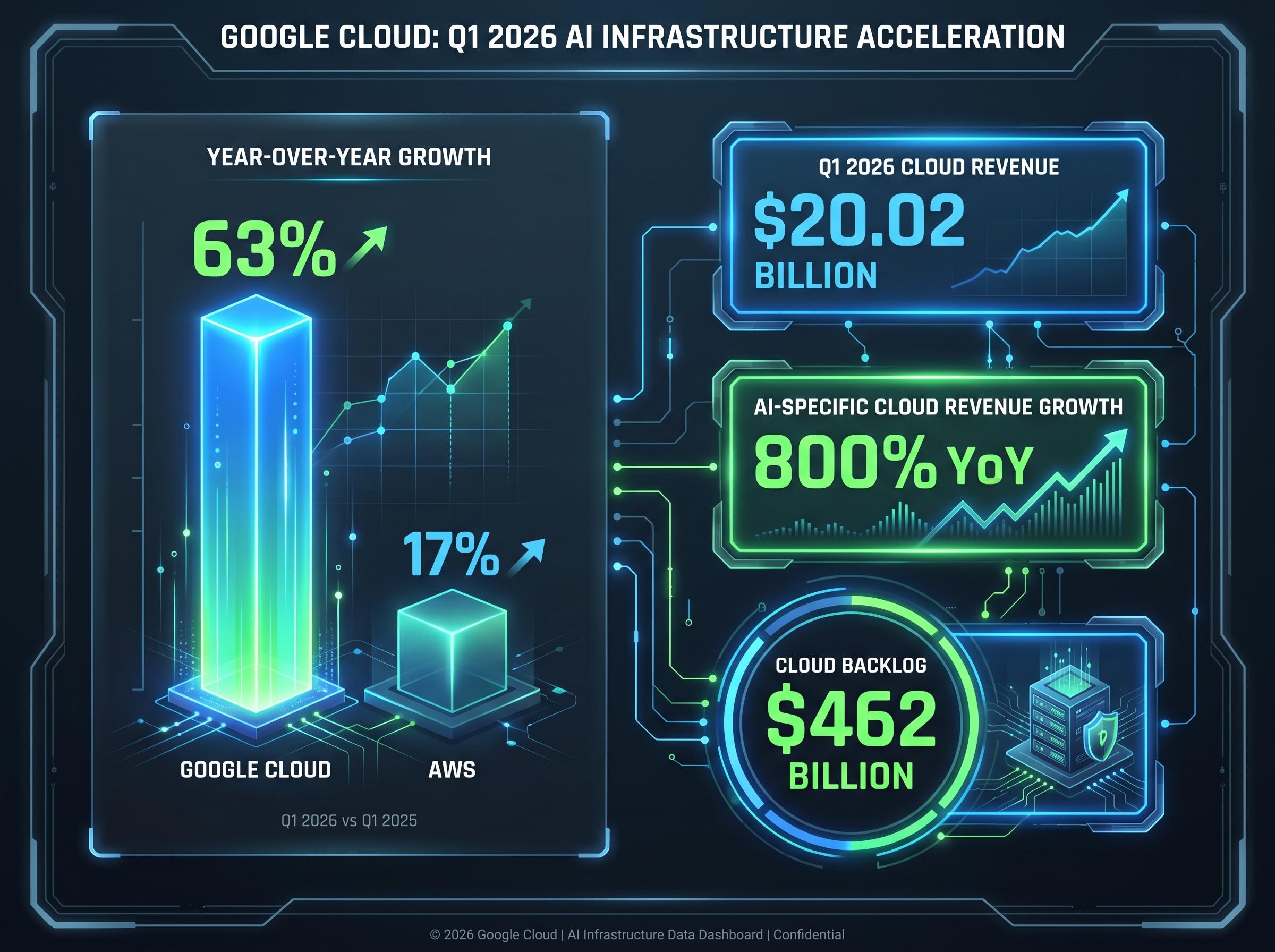

Google Cloud’s 63% growth tells the story of AI infrastructure monetisation

Google Cloud generated $20.02 billion in Q1 2026 revenue, a 63% increase year-over-year. That single segment now represents roughly 18% of Alphabet’s total quarterly revenue and runs at an annualised rate of approximately $80 billion.

The internal metrics are striking on their own:

- Q1 2026 Cloud revenue: $20.02 billion

- Year-over-year growth: 63%

- Annualised run rate: approximately $80 billion

- Cloud backlog: $462 billion in committed contracts

- AI-specific Cloud revenue growth: approximately 800% year-over-year

The $462 billion backlog figure is the data point that separates a strong quarter from a structural shift. That level of contracted demand suggests enterprise customers are not experimenting with Google Cloud for AI workloads; they are committing to it at multi-year scale.

The hyperscaler capex trajectory heading into 2027 provides the demand-side foundation for Google Cloud’s contracted backlog: with combined annual AI infrastructure spending across the four largest cloud operators projected to reach $725 billion in 2026 and potentially $1 trillion by 2027, the $462 billion committed contracts figure reflects enterprise customers locking in capacity before pricing and availability tighten further.

How Google Cloud’s growth rate compares to its hyperscaler peers

AWS reported approximately 17% growth in the same period. Exact market share figures between the hyperscalers remain unavailable, and growth rate comparisons are an imperfect proxy for competitive positioning. Still, the gap between 63% and 17% is wide enough to signal that Google Cloud is capturing enterprise AI workloads at a pace the largest incumbent is not matching.

Microsoft Azure benefits from its OpenAI partnership, which creates a comparable competitive dynamic on the AI infrastructure side. The three-way race between Google Cloud, AWS, and Azure will define cloud economics for the rest of the decade, and Google’s 800% AI revenue growth rate within Cloud positions it as the fastest-moving of the three on AI-specific demand.

What Waymo’s expansion into 12 cities actually means for long-term investors

Quarterly earnings cadence does not capture what Waymo represents. This is a decade-scale position on autonomous transportation, and the operational evidence of scaling is now concrete rather than speculative.

- Late 2025: Waymo announced expansion into five new cities: Miami, Dallas, Houston, San Antonio, and Orlando

- 2026 target: Operations across 12 cities

- End of 2026 goal: Surpassing 1 million weekly paid trips

- End of decade projection: Waymo could become a meaningful revenue contributor, according to Motley Fool analyst Keith Speights

These are not pipeline announcements. Waymo is deploying autonomous vehicles in cities with different traffic patterns, weather conditions, and regulatory frameworks, each expansion adding operational complexity that validates the technology at scale.

Why autonomous ride-hailing leadership is difficult to replicate

Waymo’s competitive position rests on a data flywheel that compounds with every mile driven. Each trip generates training data that improves the autonomous driving model, and that model improvement enables expansion into new geographies, which generates more data.

Competitors face the same physics problem, not just the same software challenge. Sensors must handle rain, construction zones, pedestrian behaviour, and edge cases that appear only at massive scale. Waymo’s lead in real-world miles creates a time-based barrier to entry. A rival with equivalent engineering talent would still need years of accumulated driving data to match the model’s situational awareness.

For investors evaluating Alphabet purely on search and cloud revenue, Waymo represents optionality that does not appear in a trailing price-to-earnings ratio but could materially re-rate the stock if autonomous ride-hailing reaches commercial scale.

Understanding Alphabet’s AI architecture: why this is a platform business, not a chip business

Most retail investors frame the AI trade through semiconductor companies. Nvidia sells the GPUs that train and run AI models. Broadcom provides the networking infrastructure that connects them. These are hardware businesses that monetise AI by selling picks and shovels to whoever builds.

Alphabet monetises differently. It owns the infrastructure layer (Google Cloud), the application layer (Search, Gemini, YouTube), and the research layer (Google DeepMind) simultaneously. The Transformer architecture, the foundational model structure underlying large language models including those powering ChatGPT, was developed at Google Brain (now merged into Google DeepMind).

The original Transformer architecture paper, published at NeurIPS 2017 by researchers at Google Brain, introduced the attention mechanism that became the structural foundation for every major large language model built since, including GPT-4 and Gemini.

The Transformer architecture that underpins modern AI, from ChatGPT to Google’s own Gemini, was invented at Google. Alphabet’s AI research is foundational, not derivative.

Google Gemini is positioned as one of the most capable AI models currently available, and it feeds directly into Cloud, Search, and advertising products. This creates a compounding loop that semiconductor companies do not replicate: research improves products, products generate revenue, revenue funds more research.

| Metric | Alphabet | Nvidia | Broadcom |

|---|---|---|---|

| Market Cap (approx.) | $4.66 trillion | Varies | Varies |

| Analyst Buy Rating % | 89% | High | High |

| Gross Margin | 60.43% | 71.07% | 64.96% |

| AI Revenue Signal | Cloud AI up ~800% YoY | GPU sales | Networking sales |

Alphabet’s 60.43% gross margin sits below Nvidia’s 71.07% and Broadcom’s 64.96%, reflecting a revenue mix that includes lower-margin hardware and data centre costs rather than an inferior competitive position. The three-horizon framework clarifies the structural difference: Cloud is monetising now, Waymo is monetising mid-decade, and Quantum AI could become relevant in the 2030s and beyond. No semiconductor stock offers that layered exposure.

The DOJ antitrust ruling and what it actually means for the investment thesis

Any honest assessment of Alphabet’s investment case must confront the regulatory risk directly.

In 2025, the Department of Justice ruled that Google holds a search monopoly. The ruling carried consequences, but not the ones many investors feared:

- What the DOJ found: Google maintains a monopoly in search

- What the remedy requires: Google must share some search data with competitors

- What was not ordered: No divestiture of any business unit, no structural breakup

- Current status: Appeals are ongoing as of early 2026

The distinction between what was feared and what was ordered matters for valuation. A forced breakup of search from cloud or YouTube would have represented a structural threat to the investment thesis. A data-sharing requirement, while a competitive headwind, does not alter Alphabet’s ability to monetise AI across its platform.

Why the analyst community remains bullish despite the ruling

Post-ruling, no material analyst downgrades were recorded. After Q1 2026 earnings, Goldman Sachs raised its target to $450 and JPMorgan went to $460, both well above the pre-ruling trajectory.

The MarketBeat breakdown as of early May 2026 shows 29 Buy ratings, 7 Strong Buy, and just 3 Hold. That is the market’s revealed preference: the search monopoly finding is a headwind worth monitoring, not a thesis-breaking development at the current remedy scope. Appeals could alter this calculus, and investors should track developments through 2026 and into 2027.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Quantum computing optionality: too early to value, too significant to ignore

In October 2025, Google Quantum AI demonstrated a benchmark that resists easy dismissal.

Google Quantum AI achieved a 13,000x speedup over the world’s fastest supercomputer in a physics simulation, a result that represents continued leadership in quantum computing research.

There is no near-term revenue impact. Quantum computing does not belong in a discounted cash flow model for 2026 or 2027. Google Quantum AI has published roadmap milestones toward meaningful real-world applications, but those milestones sit years away from commercial relevance.

What quantum computing does provide is the third layer of Alphabet’s AI time-horizon stack:

- Cloud: Monetising now (63% growth, $462 billion backlog)

- Waymo: Scaling toward monetisation (1 million weekly trips target by end of 2026)

- Quantum AI: Long-duration optionality (2030s and beyond)

Investors holding Alphabet are effectively holding a free option on quantum computing breakthroughs, embedded within a stock priced primarily on search, cloud, and advertising. That optionality has no direct comparator among semiconductor AI stocks, where the investment thesis begins and ends with the current hardware cycle.

Alphabet in 2026 rewards investors willing to look further than the chip cycle

Three investment time horizons are compounding simultaneously. Google Cloud is delivering now, with 63% growth and a $462 billion backlog of contracted demand. Waymo is scaling toward monetisation, targeting 1 million weekly paid trips by the end of 2026 across 12 cities. Quantum AI provides long-dated optionality that could become material in the 2030s.

The valuation gap persists. At approximately $383, GOOGL trades below the MarketBeat consensus of $402.96 and well below Goldman Sachs’ $450 and JPMorgan’s $460 targets. An 89% Buy or Strong Buy consensus among surveyed analysts suggests the earnings strength from Q1 2026 has not been fully absorbed into the stock price.

Investors assessing the Alphabet discount against analyst targets should also weigh the broader US equity valuation context, where the Buffett Indicator has reached 223.6% as of May 2026, approximately 2.4 standard deviations above its long-run trend; in an environment where macro valuation signals are elevated, individual stocks trading at apparent discounts to intrinsic value attract additional scrutiny around whether consensus targets embed sufficiently conservative assumptions.

Alphabet is not a chip trade. It is a position on which infrastructure layer captures the durable economics of the AI era. Investors looking to build a view should read the Q1 2026 earnings transcript and Waymo’s latest operational update alongside the post-29 April 2026 analyst reports from Goldman Sachs and JPMorgan for the most current data before making allocation decisions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.