Nvidia’s Biggest Customers Are Building Its Biggest Rivals

34 mins ago

The Philadelphia Semiconductor Index (SOX) just completed something that has never happened before in its recorded history: 18 consecutive winning sessions, stretching from late March through late April 2026. It did so while Treasury yields climbed, oil-driven inflation accelerated on the back of U.S.-Iran tensions, and the global bond market sold off. The AI stock market has behaved as if the traditional relationship between rising rates and growth equity valuations has been suspended. This analysis examines the structural forces behind that divergence, explains why hyperscaler capital expenditure is creating a demand profile that differs from prior growth cycles, and delivers a forward-looking framework for assessing whether the conditions sustaining the rally are durable or approaching a fracture point.

Eighteen consecutive sessions. From late March to late April 2026, the SOX index rose every single day, the longest winning streak in its history. The index closed at 11,305.50 on 19 May 2026 and traded in an intraday range of approximately 11,528-11,662 on 20 May, holding near record territory even after the streak formally ended. Through mid-May, the post-streak trading range remained 11,300-12,100.

What makes the streak analytically significant is not the number itself; it is the environment in which it occurred. The streak unfolded against:

SOX anchor data: The index closed at 11,305.50 on 19 May 2026, with a post-streak trading range of 11,300-12,100 through mid-May.

Prior periods of AI enthusiasm produced sharp rallies followed by equally sharp reversals when macro conditions tightened. This time, the streak held and the subsequent pullback was measured, not violent. The question that demands an answer is structural, not anecdotal: what made the demand regime beneath this rally different?

Nvidia’s $5 trillion market capitalisation milestone was documented by Forbes as the first time any company had reached that threshold, a data point that contextualises the scale of capital appreciation the AI hardware cycle has generated from its late-2022 baseline.

The streak was not built on narrative momentum alone. It was built on a capex cycle with identifiable buyers, contracted delivery timelines, and near-term revenue visibility that distinguishes AI hardware demand from the growth stock categories that typically suffer most in rising-rate environments.

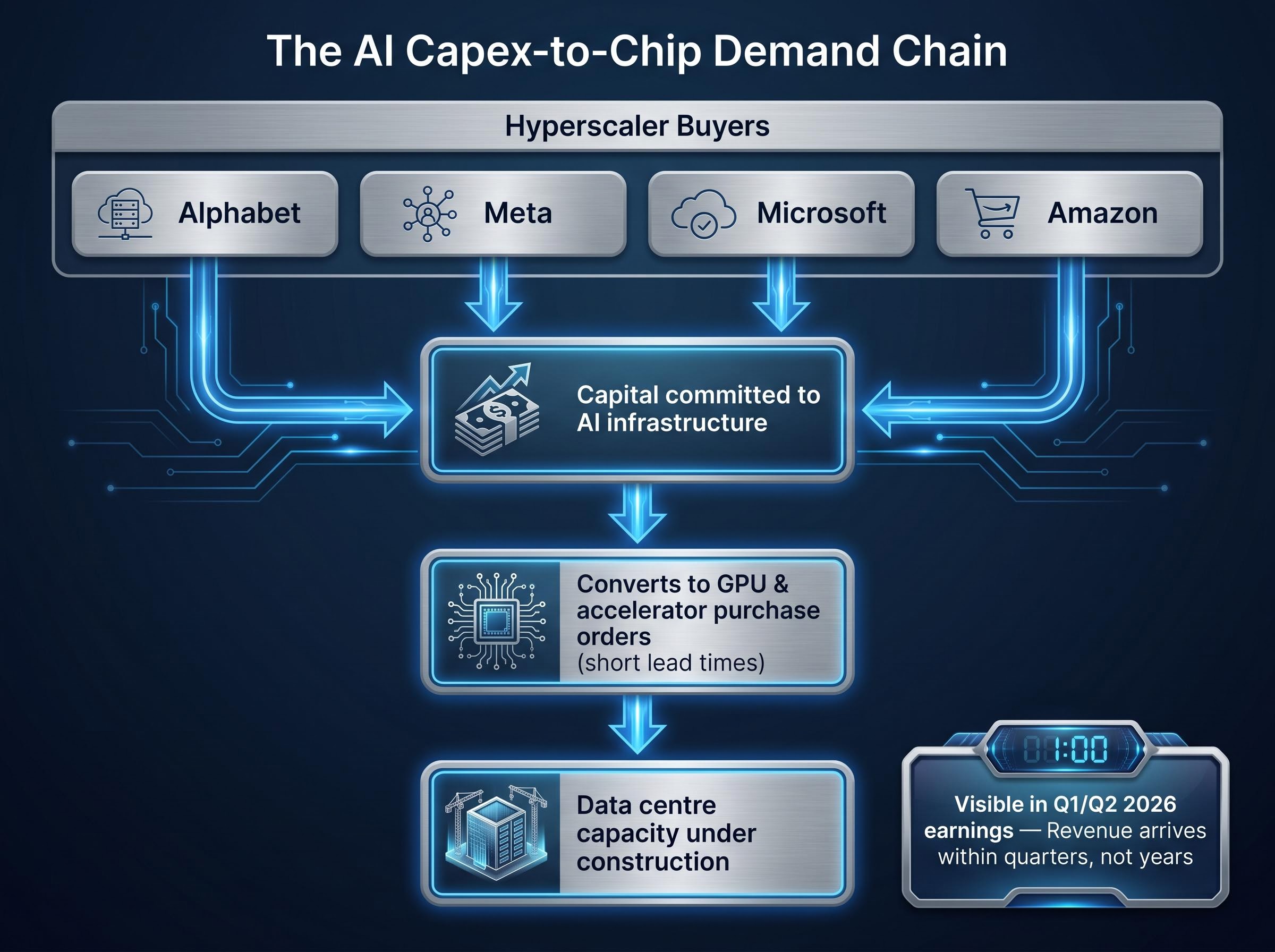

When Alphabet, Meta, Microsoft, and Amazon commit capital to AI infrastructure buildout, that capital converts into GPU and accelerator purchase orders with short lead times. These are not speculative bets on future consumer adoption. They are capital goods orders from four of the largest balance sheets in the world, directed at data centre capacity that is already under construction. The demand pipeline is visible in quarterly capex disclosures (available through SEC EDGAR filings and Q1/Q2 2026 earnings releases), and the revenue it generates arrives within quarters, not years.

The scale of the commitment underpinning this demand chain has grown beyond anything the semiconductor industry has previously absorbed: hyperscaler capex commitments for 2026 reached approximately $725 billion in combined guidance from Amazon, Microsoft, Alphabet, and Meta, with Q1 2026 spend alone hitting $130 billion, and the trajectory points toward a $1 trillion annual run rate by 2027.

This creates an earnings visibility profile that is qualitatively different from traditional software-as-a-service growth. The key distinguishing characteristics:

Growth stocks are theoretically more sensitive to rising rates because a larger share of their value is tied to distant future cash flows. As discount rates rise, those distant cash flows shrink in present-value terms. AI hardware leaders in 2026 are generating large, near-term cash flows from the capex cycle described above, which compresses their effective duration.

The analytical framework applied by strategists including Keith Lerner at Truist Advisory Services, Dan Ives at Wedbush Securities, Ross Mayfield at Baird, and Brian Belski at Humilis Investments treats these companies as earnings-compounding infrastructure beneficiaries rather than duration-sensitive growth stocks. The higher-yield environment becomes valuation-damaging only when yields rise faster than AI earnings expectations can keep pace. Through mid-2026, earnings revisions have outrun yield movement.

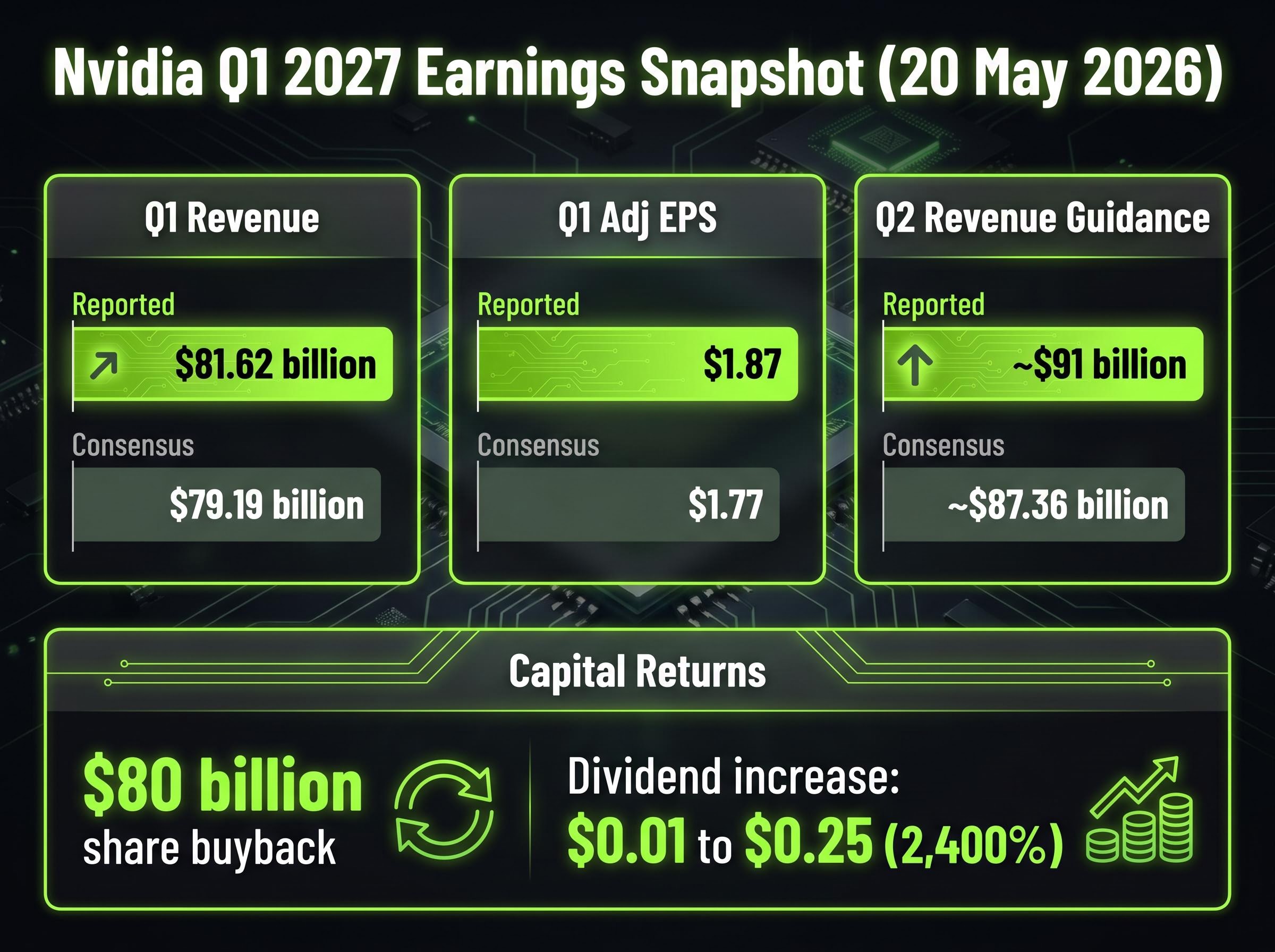

Nvidia’s fiscal Q1 2027 results, released on 20 May 2026, provided the most granular data point available for testing whether the AI demand thesis is holding or fraying.

| Metric | Reported | Consensus estimate | Result |

|---|---|---|---|

| Q1 revenue | $81.62 billion | $79.19 billion | Beat |

| Q1 adjusted EPS | $1.87 | $1.77 | Beat |

| Q1 GAAP EPS | $2.39 | N/A | Reported |

| Q2 revenue guidance | ~$91 billion (±2%) | ~$87.36 billion | Above consensus |

The earnings beat is the confirmed past. The more analytically significant number is the Q2 2027 guidance of approximately $91 billion, which exceeded expectations by roughly $3.6 billion. Guidance signals the demand pipeline, not just confirmed activity. It tells the market that hyperscaler purchase orders for the coming quarter are running ahead of what the analytical community had modelled.

Nvidia’s fiscal Q1 2027 earnings confirmed revenue of $81.62 billion against a consensus estimate of $79.19 billion, with adjusted EPS of $1.87 beating the $1.77 consensus, figures that Kiplinger’s live coverage tracked in real time as the results were released on 20 May 2026.

Capital return decisions reinforced the signal. Nvidia authorised an $80 billion share buyback and raised its quarterly dividend from $0.01 to $0.25 per share, a 2,400% increase. Management teams do not commit to permanent capital return programmes of this magnitude unless their internal demand visibility supports sustained earnings durability.

Jensen Huang, Nvidia’s Chief Executive Officer, characterised the current AI infrastructure cycle as the “largest buildout in human history,” noting that agentic AI is already generating measurable economic value.

Shares dipped approximately 0.3% in after-hours trading following the release. That modest reaction, against a backdrop of beats on every major metric and above-consensus guidance, reveals the expectations regime at work: the market had already priced a strong quarter. The question is no longer whether Nvidia can beat; it is whether the beat can keep accelerating. The company’s market capitalisation has exceeded $5 trillion, having grown from its late-2022 baseline in approximately three years.

The AI hardware complex did not shrug off macro headwinds because those headwinds were trivial. Each one carried a transmission mechanism that would ordinarily affect semiconductor and growth stock valuations. The relevant question is where, specifically, those transmission mechanisms were interrupted.

Rising yields compress the present value of future earnings, a straightforward relationship that has historically punished growth equities in tightening cycles. For AI hardware leaders, the transmission has been partially interrupted because near-term earnings compounding is outpacing the discount rate expansion. The earnings revision momentum for the AI semiconductor cohort has exceeded the pace of yield increases through mid-2026.

This is a dynamic condition, not a permanent structural break. The threshold logic is specific: the yield-valuation damage mechanism activates when yield rises outpace earnings expectation revisions. Should AI earnings revision momentum stall while yields continue climbing, the traditional transmission reasserts itself.

U.S.-Iran tensions lifted crude oil prices on Gulf supply disruption fears, adding to inflation expectations and briefly pressuring equity sentiment. Defence and energy shares outperformed on tension spikes, while broader indices saw modest pullbacks. AI and megacap strength absorbed the geopolitical risk premium at the headline index level, preventing the kind of broad market repricing that would typically accompany this degree of regional tension.

| Macro headwind | Traditional transmission to growth stocks | Why the transmission is partially interrupted in 2026 |

|---|---|---|

| Rising yields | Higher discount rates compress present value of future earnings | AI earnings revision momentum exceeds yield movement pace |

| Oil-driven inflation | Erodes consumer spending power; forces tighter monetary policy | AI hardware demand is institutional capex, not consumer-facing |

| Iran geopolitical risk | Elevates risk premiums broadly; triggers risk-off positioning | Megacap AI strength offsets risk premium in headline indices |

| Bond market selloff | Competes for capital allocation away from equities | AI capex visibility provides earnings certainty that bonds cannot match |

The SOX remained in the 11,300-12,100 range through mid-May despite all four headwinds operating simultaneously. The override is real, but it depends on the continued strength of the AI earnings cycle. A direct military escalation or shipping lane disruption would represent a qualitative escalation that the current framework may not fully absorb.

A structural market regime shift differs from a cyclical momentum trade in three ways: the earnings power driving it is durable rather than sentiment-dependent, the customer concentration is identifiable rather than diffuse, and the demand visibility extends across multiple quarters rather than collapsing when narratives shift.

The $3.8 trillion added to semiconductor market valuations over six weeks through May 2026 has renewed debate about whether the industry is experiencing a genuine semiconductor supercycle driven by structurally permanent agentic AI workloads, or a speculative episode that will compress once hyperscaler return-on-investment scrutiny intensifies.

The AI hardware rally qualifies on the structural criteria. Hyperscaler capex commitments are multi-year in nature. Nvidia’s guidance trajectory implies accelerating demand, not plateauing demand. Jensen Huang’s characterisation of Nvidia as the “sole platform across all major cloud environments” reflects competitive positioning that resembles a structural moat rather than cyclical leadership.

Nvidia has been described as operating as the “sole platform across all major cloud environments,” a positioning that, if sustained, suggests structural competitive advantage rather than temporary market share.

The cyclical component has not disappeared, however. The earnings multiple expansion embedded in the run from sub-$1 trillion to above $5 trillion in market capitalisation contains sentiment-driven premium that is sensitive to AI project return-on-investment scrutiny. If the structural foundation holds but the sentiment layer compresses, the result is a valuation correction within an intact regime, not a regime fracture.

The specific conditions that could fracture the regime:

The capex-to-revenue lag sits at the centre of the monetisation scrutiny risk: Morningstar analyst Dennis Li has identified an 18-24 month gap between infrastructure commitment and revenue generation, and Gartner estimates only 20% of current AI agent pilots are scalable to production by 2027, meaning the current earnings revision cycle could stall before the buildout generates the enterprise returns that justify it.

The 2024-2026 market experience has produced an analytical framework that can be distilled into four monitoring variables. These are the inputs that matter most for assessing whether the current AI equity regime remains intact at the individual position level.

At $5 trillion in market capitalisation with Q2 guidance implying continued revenue acceleration toward $91 billion, Nvidia’s valuation multiple requires ongoing earnings expansion to justify. A stall in guidance growth, even without a miss, could compress the multiple significantly.

The dividend increase from $0.01 to $0.25 per share per quarter (a 2,400% increase) and the $80 billion buyback authorisation carry analytical weight beyond their direct shareholder return. Management teams commit to permanent capital return programmes of this scale only when their internal demand visibility supports high confidence in earnings sustainability. Any future reduction in the buyback pace or a dividend freeze would function as a leading indicator that management’s own assessment of demand durability has shifted.

Monitoring changes to this capital return posture in future quarters provides a signal that precedes revenue data by at least one reporting cycle.

The evidence is clear on one side of the equation: AI hardware demand has demonstrably overridden traditional macro headwinds through mid-2026. The SOX’s 18-session winning streak, its post-streak resilience in the 11,300-12,100 range, and Nvidia’s earnings trajectory all point to a demand regime with structural foundations rather than purely narrative ones. The override, however, is conditional. It depends on the continued acceleration of hyperscaler capex, the maintenance of earnings revision momentum above yield movement, and the absence of supply chain disruptions or monetisation evidence that undermines the buildout thesis.

The forward monitoring priorities:

These are specific, testable conditions. The AI equity regime has earned the benefit of evidence, not the benefit of the doubt.

For investors wanting to stress-test the structural case against the most prominent institutional bearish counterargument, our deep-dive into Michael Burry’s SOXX put position examines Scion Asset Management’s January 2027 puts at a $330 strike, the specific dot-com era comparisons Burry cited publicly on 8 May 2026, and why Goldman Sachs’ earnings floor analysis reaches the opposite conclusion from the same data.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Philadelphia Semiconductor Index (SOX) tracks the performance of major semiconductor companies listed in the United States and is widely used by investors as a benchmark for the health of the chip sector and broader technology hardware cycles. It is particularly relevant during periods of AI infrastructure buildout because semiconductor firms are the primary suppliers of the GPUs and accelerators that hyperscalers purchase.

AI hardware companies in 2026 generate large near-term cash flows from contracted hyperscaler purchase orders, which compresses their effective duration and reduces their sensitivity to rising discount rates. The key dynamic is that earnings revision momentum for the AI semiconductor cohort outpaced the pace of yield increases through mid-2026, interrupting the traditional transmission mechanism that punishes growth stocks when rates rise.

Nvidia reported Q1 revenue of $81.62 billion against a consensus estimate of $79.19 billion, with adjusted EPS of $1.87 beating the $1.77 consensus, and issued Q2 guidance of approximately $91 billion, roughly $3.6 billion above analyst expectations. The above-consensus guidance is particularly significant because it signals that hyperscaler purchase orders for the coming quarter are running ahead of what the market had modelled.

Combined AI infrastructure capex guidance from Amazon, Microsoft, Alphabet, and Meta reached approximately $725 billion for 2026, with Q1 2026 spend alone hitting $130 billion and the trajectory pointing toward a $1 trillion annual run rate by 2027. This level of committed institutional spending creates earnings visibility that analysts describe as qualitatively different from traditional software or consumer-facing growth businesses.

The four primary fracture conditions identified are: a meaningful downward revision in hyperscaler capex guidance, evidence that AI infrastructure buildout is outpacing enterprise monetisation, a yield spike that exceeds AI earnings revision momentum, and a supply chain disruption that constrains semiconductor production capacity. Morningstar analyst Dennis Li has also flagged an 18-24 month lag between infrastructure commitment and revenue generation as a potential stall risk for the current earnings revision cycle.