How Hormuz Closure at $104 Oil Is Reshaping Every Asset Class

5 hrs ago

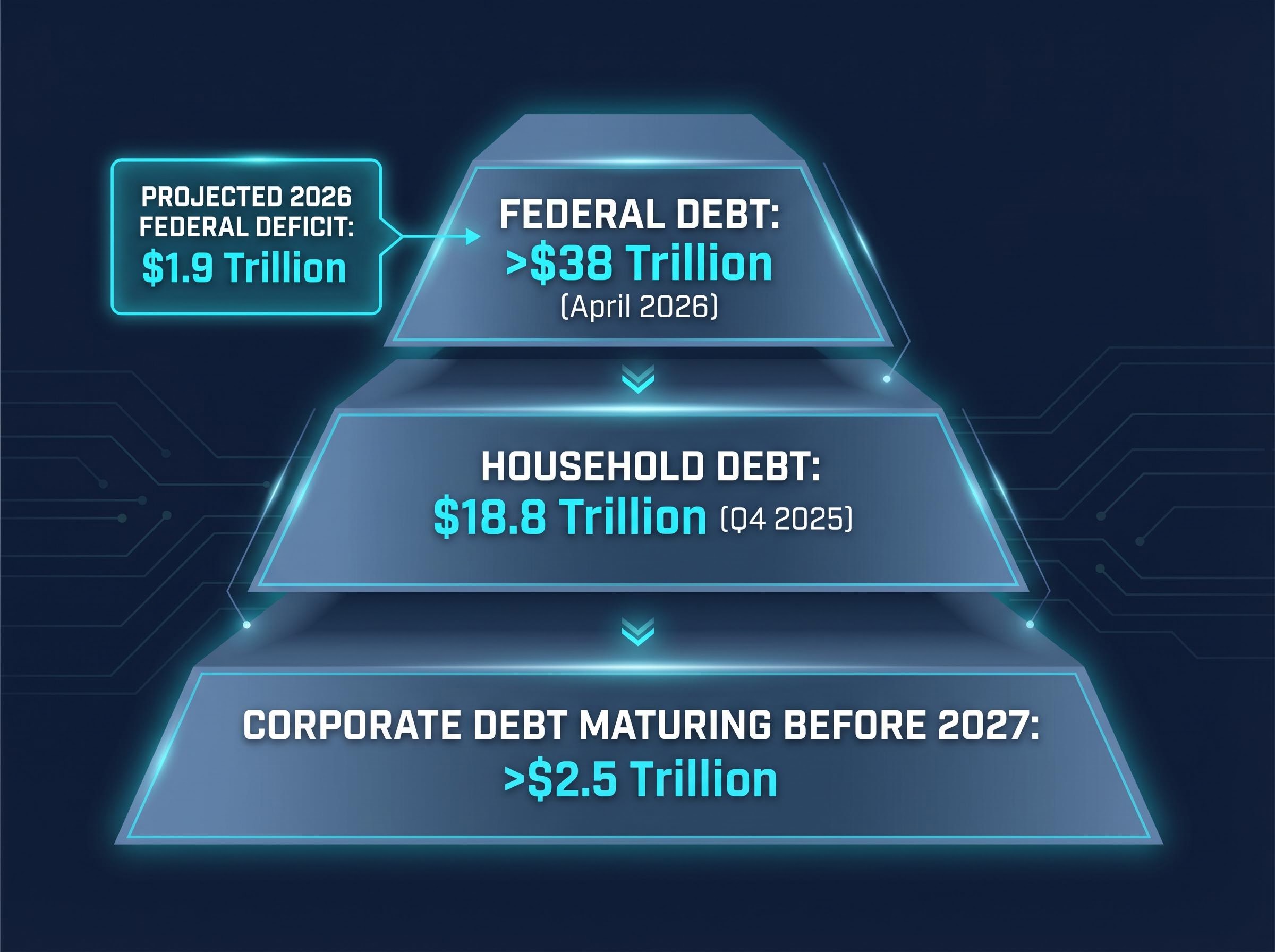

The U.S. federal government is on track for a projected $1.9 trillion deficit in 2026. American corporations are posting some of the strongest profit margins on record. According to economist John Hussman, those two facts are not a coincidence but a dependency, one that carries direct implications for the AI-driven equity rally that has defined markets over the past two years.

Hussman published a note on 27 April 2026 arguing that the AI market rally is not self-sustaining. His structural claim: corporate profits at current levels are quietly subsidised by debt accumulation across government, households, and corporations. As that borrowing picture grows more precarious, the earnings foundation beneath elevated AI stock valuations may be shakier than markets are pricing in.

This analysis unpacks the debt-to-profit linkage Hussman identifies, examines what the hard numbers say about fiscal trajectories and AI sector performance in 2026, and assesses what a shift in borrowing conditions could mean for investors holding AI-exposed equities.

Corporate profits are not just high. They are, in Hussman’s framing, structurally impossible without the borrowing that supports them.

That is the counterintuitive claim at the centre of his 27 April 2026 note. Post-tax corporate profits, adjusted for inventory valuation and capital consumption, increased more than 10% year-over-year through the end of 2025, according to U.S. Commerce Department data via FRED. The headline reading is strength. Hussman’s reading is fragility: those profits are downstream of a federal government running $1.78 trillion deficits in FY 2025, a household sector carrying $18.8 trillion in debt, and a corporate sector layering on leverage to fund AI infrastructure at historic scale.

Hussman has characterised current AI profit expectations as resembling the structure of a Ponzi scheme, where returns to early participants depend on continued inflows rather than organic value creation.

The comparison is deliberately provocative, but it rests on a documented accounting relationship rather than rhetoric alone. Total U.S. federal debt now exceeds $38 trillion as of April 2026, per the U.S. Treasury Department. If Hussman’s structural argument holds, AI stock valuations are not just expensive relative to current earnings; they are expensive relative to earnings that may themselves be artificially elevated. That reframing changes the risk calculus materially.

Hussman is not a fringe voice. He anticipated the dot-com collapse with a similar structural analysis in the late 1990s. Whether his current warning proves similarly prescient remains an open question, but the mechanics of his argument deserve examination on their own terms.

Hussman’s MarketCap/GVA ratio is registering at historically unprecedented levels as of April 2026, a valuation metric that places the current AI-driven rally in direct structural comparison to the 1929 crash and the 2000 dot-com peak, when concentration in a small number of high-growth names similarly masked the fragility of the broader earnings base.

The logic is simpler than it appears, and it is not a political argument. It is an accounting identity.

In the sectoral balances framework, one sector’s deficit is, by definition, another sector’s surplus. When the federal government spends $1.9 trillion more than it collects in revenue (the projected FY 2026 deficit), that money flows into the private sector. Some of it becomes household income. Some of it becomes corporate revenue. The Bureau of Economic Analysis (BEA) documents these flows; they are not theoretical.

The three layers of the current debt structure illustrate the scale:

Economists broadly project persistent deficits exceeding 6% of GDP through 2030, surpassing Congressional Budget Office (CBO) baseline projections. That trajectory means the subsidy dynamic is likely to continue in the near term. The question is what happens at the margin.

The CBO Budget and Economic Outlook projections for 2026 to 2036 establish the official nonpartisan baseline for federal deficit and debt trajectories, projecting federal debt rising to approximately 120% of GDP by 2036 and confirming the structural persistence of deficits that underpin the sectoral balances dynamic Hussman identifies.

The $18.8 trillion in household debt is not idle on balance sheets. It translates directly into consumer spending, which in turn sustains corporate revenue lines. When households borrow to spend, companies book revenue that would not exist without that leverage. For AI-exposed technology companies, whose products and services ultimately depend on enterprise and consumer demand, this linkage matters.

Corporate debt adds a distinct pressure. Over $2.5 trillion in U.S. corporate debt matures before 2027, and refinancing at elevated interest rates could compress margins independently of any fiscal policy change. For capital-intensive AI infrastructure companies carrying significant debt loads, the refinancing environment represents a near-term headwind that earnings projections may not fully reflect.

A speculative asset bubble forms when prices embed future earnings growth that is uncertain, creating asymmetric downside risk if those expectations are revised. The label is not about whether the underlying technology has value. It is about whether current stock prices have priced in more value than the near-term evidence supports.

The numbers visible on any investor’s screen make the case for applying that scrutiny to AI equities in 2026.

| Company | P/E Ratio (Approx.) | 2026 CapEx Commitment |

|---|---|---|

| Nvidia (NVDA) | ~40-50x | Part of $500B+ hyperscaler buildout |

| Microsoft (MSFT) | ~35x | Leading hyperscaler investor |

| Alphabet (GOOGL) | ~25x | Major AI infrastructure expansion |

| Meta (META) | ~30x | Significant AI compute investment |

Note: P/E ratios are medium-confidence estimates as of April 2026, inferred from available price and earnings data.

AI-related capital expenditure is projected at $650 billion in 2026, up approximately 70% from 2025 levels. Hyperscalers alone are expected to invest over $500 billion. The gap between that investment and the revenue it has generated so far is precisely what has drawn institutional scrutiny. BlackRock‘s Investment Institute has raised concerns over whether AI revenue is adequately matching the scale of investment, while Vanguard has offered a sharper formulation of the risk.

Vanguard has noted that AI exuberance may produce stock downside even if the broader economic impact of AI is positive, a decoupling of technology’s real-world value from its equity market pricing.

AI capital expenditure ROI sustainability has become the central institutional concern of 2026, with a KPMG survey finding that 75% of large-company CEOs believe generative AI has been overhyped even as nearly 80% continue allocating capital to it, a paradox that mirrors the gap between Hussman’s structural fragility argument and the earnings momentum that consensus forecasters are still projecting.

That distinction matters. The question for investors is not whether AI will be economically significant. It is whether today’s share prices have already absorbed that significance, and then some.

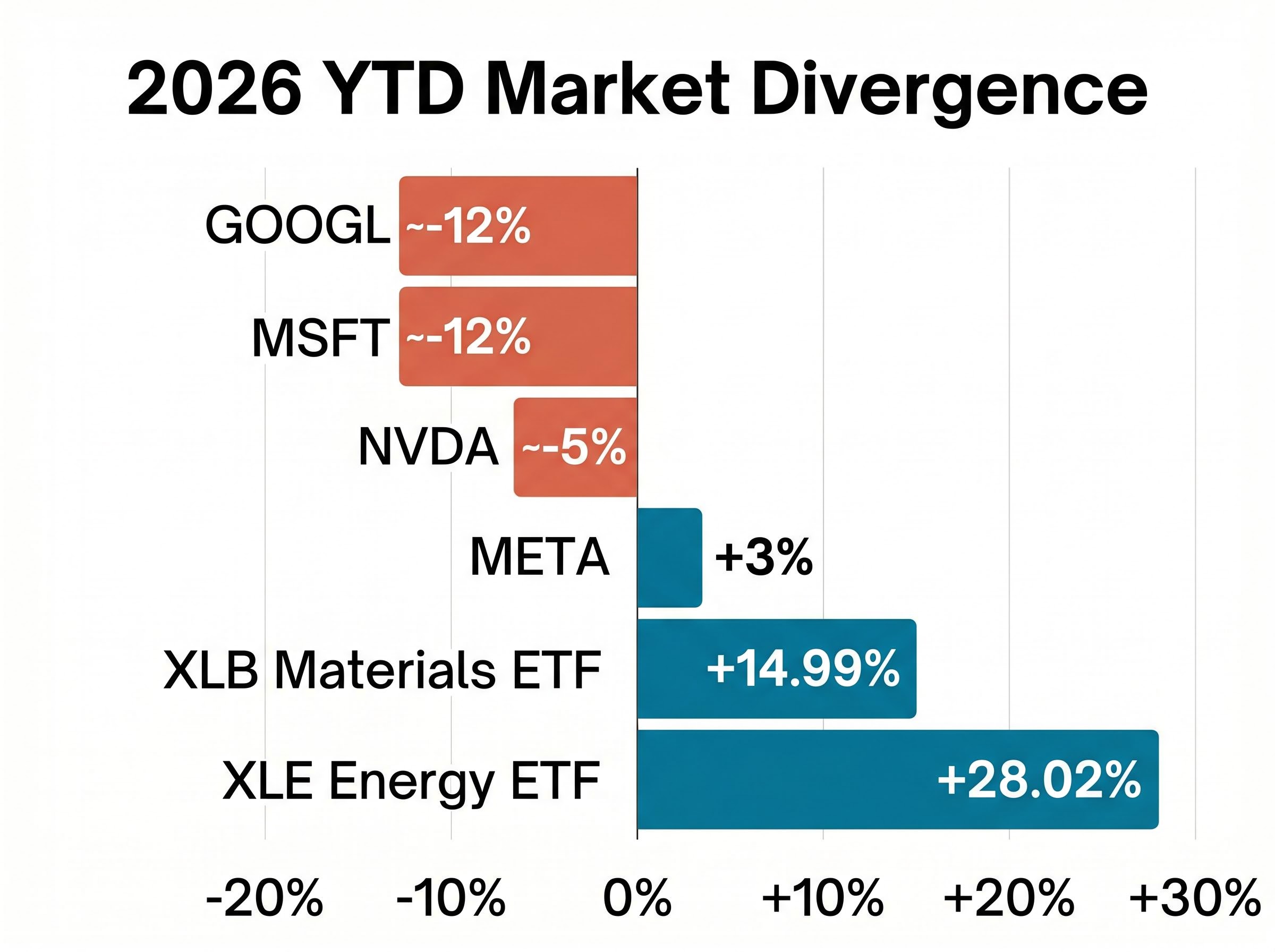

The year-to-date performance data does not confirm a bubble. It does, however, document a divergence worth examining.

| Ticker / Asset | Type | YTD Return (2026) |

|---|---|---|

| NVDA | AI / Semiconductor | ~-5% |

| MSFT | AI / Cloud | ~-12% |

| GOOGL | AI / Cloud | ~-12% |

| META | AI / Social | ~+3% |

| XLE | Energy ETF | +28.02% |

| XLB | Materials ETF | +14.99% |

Three of the four major AI-exposed stocks are in negative territory for 2026. Energy has surged over 28%. Materials have gained nearly 15%. The rotation pattern is visible.

The software sector’s 16.5% year-to-date decline through mid-April 2026 illustrates how valuation fragility operates in practice: a sector where Microsoft beat Q1 earnings expectations by 12.5% still fell sharply, suggesting that multiple compression at elevated P/E ratios can produce severe price declines even when the underlying earnings are delivering, precisely the asymmetric downside risk that elevated valuations create.

The logic behind such a rotation follows a recognisable sequence:

S&P 500 earnings are still projected to rise 15% in 2026, driven substantially by AI spending, according to Reuters. That optimistic counterpoint is real and should not be dismissed. Deloitte, however, has projected that overdone AI investment is likely to produce a market pullback around 2027, suggesting the current spending pace may be running ahead of near-term returns.

The divergence is not a verdict. It is a question the market is beginning to ask.

The transmission mechanism is straightforward to describe, even if its timing is impossible to predict.

If fiscal tightening reduces deficit spending, the corporate cash flows that depend on that spending compress. If corporate cash flows compress, the earnings growth assumptions embedded in AI stock valuations come under pressure. If those assumptions are revised downward, stocks trading at 35-50x earnings face repricing risk that is proportional to the multiple.

The counterargument is equally clear. Consensus forecasts project persistent deficits exceeding 6% of GDP through 2030, per Deloitte and CBO analysis. Near-term fiscal tightening appears unlikely given the current policy trajectory. The subsidy dynamic, in other words, may continue for years.

Federal Reserve policy paralysis adds a further dimension to the earnings fragility argument: with core PCE sitting at 2.97% and growth already slowing, the Fed cannot deliver the rate cuts that would ease corporate refinancing costs, meaning the debt maturity pressure arriving before 2027 hits balance sheets in a higher-for-longer rate environment rather than a loosening one.

Three distinct risk triggers merit monitoring, even if their timing remains uncertain:

Hussman has specifically argued that any return toward fiscal discipline would compress corporate profit margins from current elevated levels. Goldman Sachs has separately flagged the structural concern that investing more than $500 billion in AI with uncertain near-term returns creates capital allocation risk.

The fiscal scenario is long-dated and politically contingent. The corporate debt maturity wall is neither.

Over $2.5 trillion in U.S. corporate debt matures before 2027, per the OECD Global Debt Report 2026. Companies that borrowed at lower rates will face refinancing at today’s elevated levels. For capital-intensive AI infrastructure plays, whose CapEx commitments are already stretching balance sheets, the additional margin pressure could be material.

Goldman Sachs and Seeking Alpha analysis have both flagged this maturity schedule as a potential equity market catalyst, particularly for companies whose debt service costs may rise faster than their AI investments generate returns. This risk does not require a policy change to activate. It arrives on a schedule.

Hussman’s debt-to-profit thesis offers a structurally coherent framework for understanding why AI stock valuations may be more fragile than headline earnings figures suggest. The accounting relationships he identifies are documented, and the scale of the numbers involved, $38 trillion in federal debt, $18.8 trillion in household debt, $2.5 trillion in corporate debt maturing before 2027, is difficult to dismiss.

The honest uncertainty remains. Consensus forecasts do not anticipate rapid fiscal tightening, and AI earnings momentum is real for now, with S&P 500 earnings projected up 15% in 2026.

The question for investors is not whether AI will eventually prove economically significant. Most evidence suggests it will. The question is whether current stock prices are justified given the debt dependencies and CapEx uncertainties that underpin today’s profit levels. That question does not require a prediction. It requires ongoing scrutiny of the numbers behind the numbers.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

An AI stock bubble forms when share prices embed future earnings growth that is uncertain, creating asymmetric downside risk if those expectations are revised downward. It is not about whether AI technology has value, but whether current prices have already priced in more value than near-term evidence supports.

In the sectoral balances framework, when the federal government spends more than it collects, that money flows into the private sector as household income and corporate revenue. This means the projected 1.9 trillion dollar federal deficit in 2026 is, by accounting identity, partially subsidising the corporate profit margins that underpin AI stock valuations.

In a note published on 27 April 2026, Hussman argued that the AI market rally is not self-sustaining, characterising current AI profit expectations as resembling a Ponzi scheme structure where returns depend on continued debt inflows rather than organic value creation.

Over 2.5 trillion dollars in U.S. corporate debt matures before 2027, meaning companies must refinance at today's elevated interest rates. For capital-intensive AI infrastructure companies already stretching their balance sheets, rising debt service costs could compress margins before their AI investments generate proportional returns.

Investors should monitor three key risk triggers: any movement toward fiscal tightening that could compress corporate revenue, the 2027 corporate debt refinancing wall arriving in a higher-for-longer rate environment, and whether 650 billion dollars in projected 2026 AI capital expenditure generates adequate near-term returns to justify current valuations.