Why Barclays Sees 56% Upside in a Beaten-Down Automation Stock

1 hr ago

Bank of America published a single research note on 2 May 2026 that converted a diffuse anxiety into a precise figure: 838 million jobs worldwide, roughly one in every four positions, carry meaningful exposure to generative AI. The finding, produced by a team of economists led by Benson Wu, lands at a moment when AI capital expenditure is already contributing measurably to GDP growth and financial sector layoffs are accelerating by the thousands. What follows unpacks who faces the sharpest risk, which economies sit on both sides of the exposure line, what wages and earnings data reveal about workers already affected, and what the research signals for equity valuations and consumer spending trends.

The headline number demands context before it becomes useful. Bank of America’s 838 million estimate refers to jobs with meaningful generative AI exposure, a measure of which tasks within a role can be addressed by current or near-term AI systems. Exposure is not displacement. A role classified as exposed may see 30-50% of its task bundle automated while the position itself persists in a restructured form.

Autonomous AI agents replacing human-driven tasks represent the mechanism through which generative AI moves from abstract exposure risk to concrete headcount decisions; the dismantling of per-seat SaaS models has already produced over $1 trillion in market capitalisation losses in the enterprise software sector as investors reprice the assumption that human operators are irreplaceable in workflow execution.

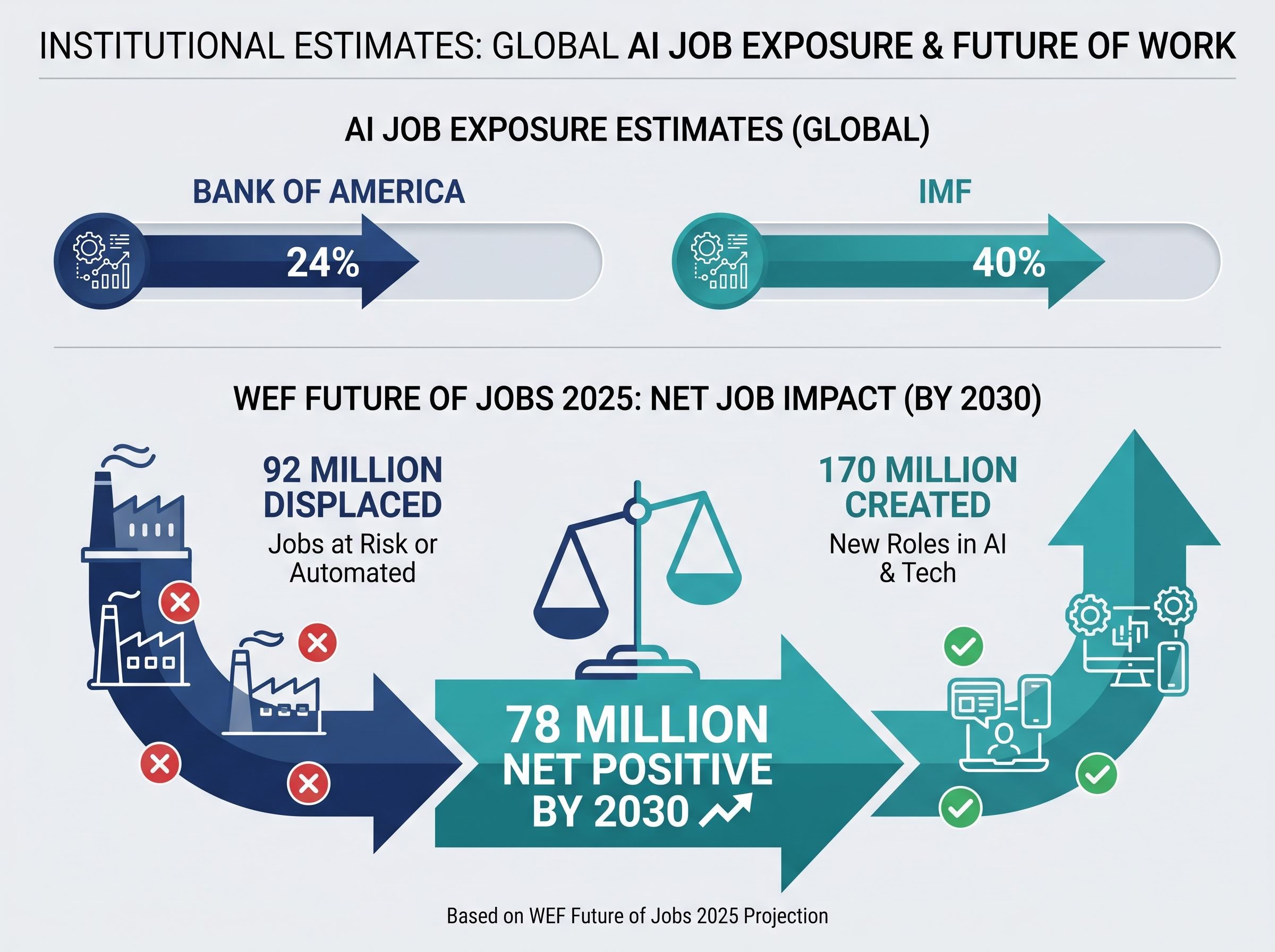

838 million jobs globally, approximately 24% of total employment, face meaningful generative AI exposure. Bank of America, 2 May 2026, citing International Labour Organization data.

The figure also sits within a wide range of institutional estimates:

The spread between Bank of America’s 24% and the IMF’s 40% is not a rounding difference. It reflects fundamentally different assumptions about what constitutes substitutable work, and readers tracking AI-related equity themes need to understand which estimate underpins which market narrative.

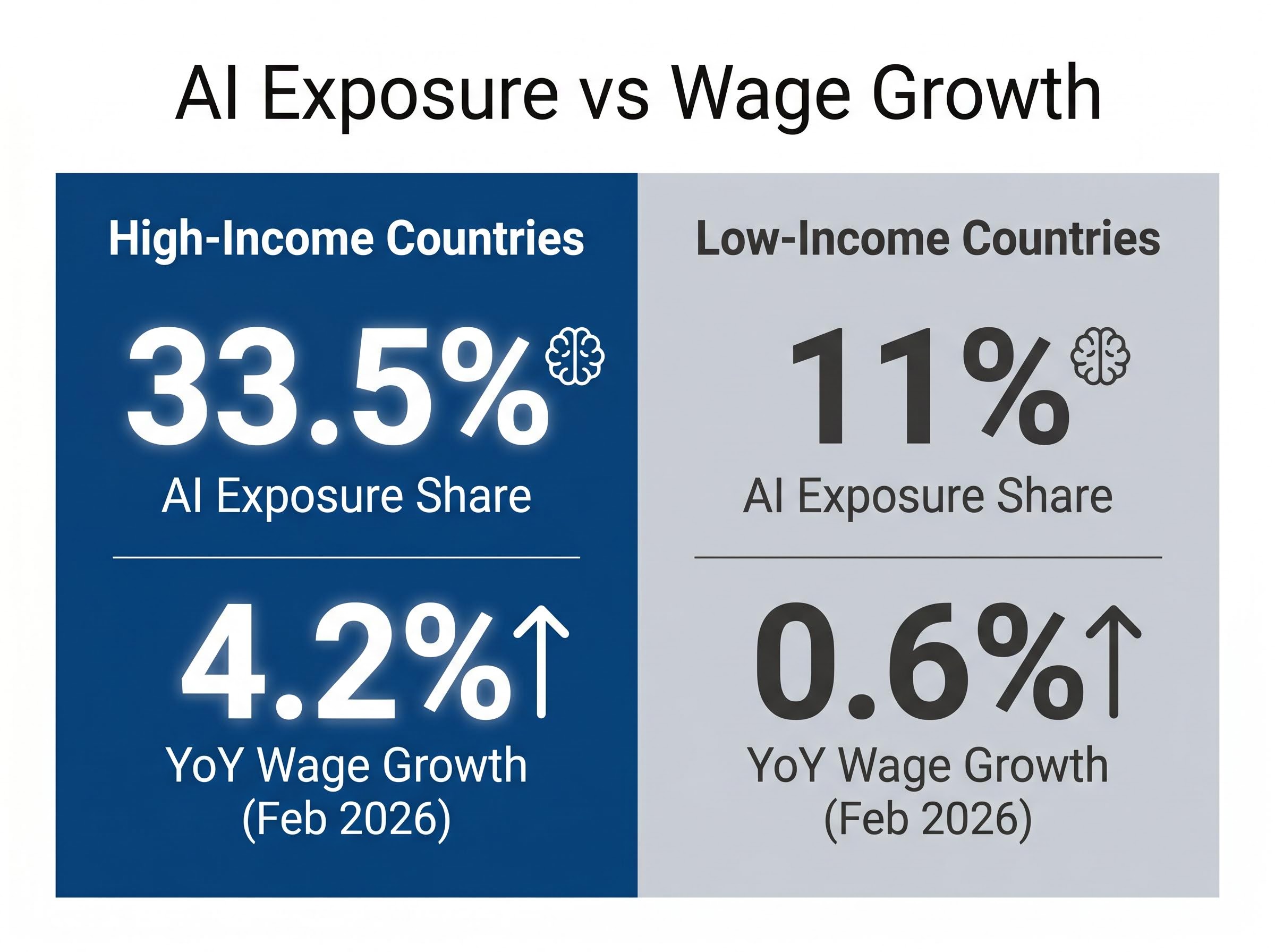

High-income countries show 33.5% job exposure versus 11% in low-income countries, according to Bank of America’s research. The gap traces directly to the prevalence of non-routine cognitive work in wealthier economies: the accounting, legal analysis, software development, and financial modelling tasks that generative AI addresses most effectively are concentrated in nations where service-sector employment dominates.

The IMF Staff Discussion Note on AI and the future of work places advanced economy exposure at approximately 60 percent, roughly double the global average, precisely because high-income labour markets are weighted toward the non-routine cognitive tasks that generative AI addresses most directly.

That concentration creates a paradox. The same structural features that make wealthy economies more exposed also give them greater absorptive capacity: deeper capital markets, stronger retraining infrastructure, and the technology firms that capture AI productivity gains.

| Country Income Group | AI Exposure Share | GDP Capex Contribution | Wage Growth Context |

|---|---|---|---|

| High-income | 33.5% | Up to 1.3 percentage points (U.S., Q2 2025) | 4.2% YoY (Feb 2026) |

| Middle-income | Between high and low estimates | Technology payments rising 6.9% YoY | 1.2% YoY (Feb 2026) |

| Low-income | 11% | Limited documented contribution | 0.6% YoY (Feb 2026) |

Bank of America specifically flagged frontier AI firms as the primary beneficiaries of efficiency gains. In white-collar sectors including finance and professional services, AI adoption is lifting output per worker without translating into hiring. The correlation between adoption and job growth in these sectors remains weak, meaning the productivity dividend is accruing to firms rather than distributing through employment growth.

The national percentages dissolve into individual stories when the demographic data arrives. Bank of America identified three groups carrying disproportionate exposure:

Workers under 25 are experiencing disproportionate employment declines in AI-exposed fields, driven primarily by falling job-finding rates rather than direct layoffs. Felten-Raj-Seamans index data, cited in Bank of America research.

The education finding is counterintuitive and consequential. Computer systems design and related services employment has declined approximately 5% since late 2022, with a broader 1% employment drop across the top 10% of AI-exposed sectors. These are graduate-level fields. The roles that require degrees are precisely the roles generative AI can partially perform.

For consumer spending models, the concentration of risk among educated young workers carries a long-run implication: if graduate-level entry wages compress or hiring timelines lengthen, the spending cohort that drives household formation and discretionary consumption faces structural headwinds.

Aggregate payroll data tells one story. Bank of America’s consumer data for February 2026 shows overall payroll growth remains positive at 1.3% year-over-year. Broad employment has not collapsed.

The differentiated picture beneath that aggregate is considerably less reassuring. Wage growth by income tier has diverged sharply: 4.2% for high-income workers, 1.2% for middle-income workers, and just 0.6% for low-income workers. Job-change pay raises have fallen to 6.7%, down from an 8.6% average in 2025. McKinsey analysis documents software testing roles shifting toward oversight functions with 5-10% pay reductions in 2025-2026.

Dallas Fed research from February 2026 adds a structural dimension: returns on experience are rising in AI-exposed occupations, meaning entry-level workers face worsening conditions while experienced workers capture relative gains.

| Worker Category | YoY Wage Growth | Key Source |

|---|---|---|

| High-income | 4.2% | BofA consumer data, Feb 2026 |

| Middle-income | 1.2% | BofA consumer data, Feb 2026 |

| Low-income | 0.6% | BofA consumer data, Feb 2026 |

| Job-changers | 6.7% (down from 8.6%) | BofA consumer data, Feb 2026 |

| Technologically displaced | ~3% real earnings loss on re-employment | Goldman Sachs |

Goldman Sachs’ longitudinal tracking data extends the picture over a decade. Workers displaced from technology-affected fields trail continuously employed peers by nearly 10 percentage points in cumulative earnings growth over ten years. They also trail workers displaced from other industries by approximately 5 percentage points over the same period.

The research cited telephone operators and typists as historical analogues, occupations where automation created permanent earnings scarring for displaced workers even as the broader economy generated new roles.

Bank of America economists argued that fears of mass unemployment conflict with established economic theory, citing three prior transitions:

The World Economic Forum projects a net creation of approximately 78 million jobs by 2030: 170 million created against 92 million displaced.

The U.S. Bureau of Labor Statistics projects software developer employment to grow 15% from 2024 to 2034, even though software development is itself among the most AI-exposed fields. Bank of America, with an AI adoption score of 76 out of 100, shed approximately 1,000 jobs through AI-enabled attrition in early 2026 while simultaneously reporting productivity gains.

The BLS occupational outlook for software developers projects 15 percent employment growth from 2024 to 2034, a rate described as much faster than the average across all occupations, which illustrates the tension at the core of AI labour analysis: the field most capable of building AI systems is also among those most structurally exposed to its outputs.

The specific feature that complicates these historical comparisons is generative AI’s application to non-routine cognitive work. Prior automation waves addressed routine manual and routine cognitive tasks. This wave targets the analytical, creative, and communicative tasks that previous technologies left largely untouched, making the transition pathway less predictable than historical analogies suggest.

The labour market data carries direct portfolio implications. Three signals stand out for sector allocators:

AI capital expenditure contributed up to 1.3 percentage points to U.S. GDP growth in Q2 2025, according to the BofA Institute. Broader Wall Street AI-related layoffs now number in the thousands across major financial firms.

AI capex and GDP contribution have become a primary lens through which analysts are assessing the macroeconomic footprint of the current cycle, with hyperscaler commitments reaching an estimated 2% of US GDP in 2026 and the semiconductor supply chain capturing the majority of that capital before it reaches labour markets.

The structural dynamic is becoming visible in financial models. Productivity gains from AI adoption are accruing to capital in the form of higher margins and lower wage-cost ratios rather than distributing through higher wages. For analysts forecasting operating leverage in AI-adopting firms, the implication is that margin expansion may prove more durable than historical patterns suggest, provided adoption continues to substitute for labour rather than complement it.

No specific firms have been publicly flagged for elevated valuation risk from AI-related labour disruption as of early May 2026. The financial sector’s pace of attrition warrants continued monitoring.

The 838 million figure is a starting point, not a conclusion. Read without distributional context, it obscures more than it reveals. Aggregate employment and payroll data remain positive. Beneath them, entry-level wages, job-finding rates for young workers, and re-employment earnings for displaced workers are all under pressure.

Four variables determine whether AI exposure translates into opportunity or hardship for a given worker or economy: income tier, age cohort, country development level, and sector. The gap between 33.5% exposure in high-income countries and 11% in low-income countries is the clearest single-number summary. The divergence between 4.2% high-income wage growth and 0.6% low-income wage growth is the current real-world signal that distributional pressure is already visible in consumer data.

Three indicators warrant monitoring in the months ahead:

Semiconductor market concentration has reached levels that exceed dot-com era peaks, with the sector now representing approximately 13% of US equity market capitalisation, a structural feature that amplifies the portfolio risk for investors overweight AI infrastructure at precisely the moment when the labour market disruptions documented by Bank of America are feeding through into consumer spending headwinds.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AI job exposure refers to the share of tasks within a role that current or near-term generative AI systems can address. Bank of America measured it by assessing which task bundles within occupations are substitutable by AI, finding that exposure does not necessarily mean displacement, as a role may see 30-50% of its tasks automated while the position itself continues in a restructured form.

Bank of America's research note published on 2 May 2026 estimates that approximately 838 million jobs globally, roughly 24% of total employment, face meaningful generative AI exposure, though this figure differs from IMF estimates of 40% globally due to differing assumptions about what constitutes substitutable work.

Bank of America identified younger workers under 25, women concentrated in administrative and professional service roles, and workers with higher levels of education as the groups carrying disproportionate AI exposure risk, with the education finding being particularly counterintuitive as graduate-level cognitive roles are precisely those generative AI can partially perform.

Bank of America's February 2026 consumer data shows a stark divergence in wage growth by income tier: high-income workers saw 4.2% year-over-year gains, while middle-income workers saw just 1.2% and low-income workers only 0.6%, suggesting AI productivity gains are accruing to capital and higher earners rather than distributing broadly across the workforce.

The research signals potential operating margin expansion for AI-adopting firms in finance and professional services as productivity rises without corresponding hiring, while weak wage growth for lower-income workers (0.6% year-over-year) points to headwinds for consumer-facing equities dependent on discretionary spending from that cohort.