A 5-Step Framework for Valuing Slowing Growth Stocks

11 hrs ago

The sign-up process takes five minutes. The platform looks familiar, the branding matches what you have seen on comparison sites, and the spreads seem competitive. You deposit, place your first trade, and assume the same protections apply as they would with any UK-regulated broker.

That assumption is almost universally wrong when the account sits under an offshore entity rather than the broker’s FCA-authorised one. This is not primarily a story about fraudulent platforms. It is about a structural regulatory difference that strips away legal rights you may not realise you had, while the interface stays identical.

After reading this, you will know exactly which protections the FCA framework gives you as a retail trader, what disappears when your account falls under an offshore entity, and the specific steps to confirm which framework governs your money before you deposit a single pound.

FCA authorisation creates legally enforceable obligations on brokers. It is not a badge of reputation or a marketing credential. For you as a retail trader, it means a specific set of rights that you can invoke, escalate, and, if necessary, enforce through independent bodies.

Those rights were not designed in the abstract. The protections were formalised through product-intervention rules from 2018-2019, following specific market events that demonstrated what happens without them. The Swiss National Bank’s January 2015 EUR/CHF shock, which removed the currency floor without warning, drove retail traders across Europe into catastrophic negative balances overnight. That single event accelerated regulators, including the FCA, toward the mandatory protections now in place.

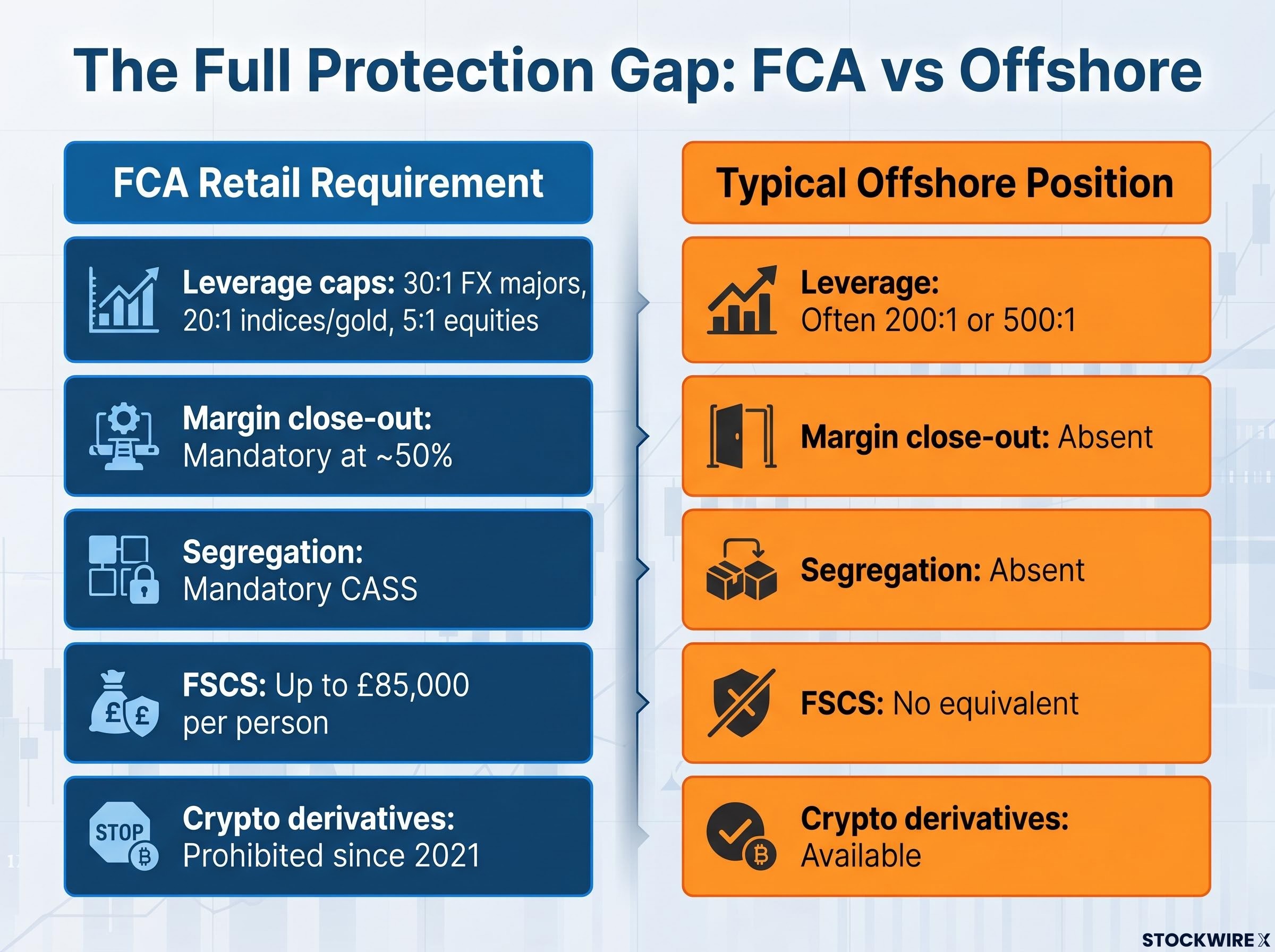

The FCA policy statement PS19/18 formalised these protections for retail CFD clients, establishing the 30:1 leverage cap on FX majors, the 50% margin close-out rule, and the mandatory negative balance protection requirement that together form the baseline framework governing FCA-authorised CFD brokers today.

Here is what those protections look like in practice:

These protections work as an interconnected system. Leverage caps limit the speed of loss. Margin close-out rules prevent that loss from compounding. Negative balance protection provides a hard floor. CASS segregation ensures the broker cannot use your capital for its own purposes. Understanding this architecture is what allows you to recognise exactly what you are giving up when you step outside it.

The scale of CFD trading losses across regulated retail populations gives that architecture concrete weight: ESMA data from Q1 2026 places the proportion of retail accounts losing money at between 74% and 89%, with average losses reaching up to 29,000 euros per client across the jurisdictions where leverage caps and negative balance protection are already mandatory.

The difference between FCA regulation and a typical offshore framework is not a single missing feature. It is the removal of an entire layered system, where each component was built to address a distinct category of harm.

| Protection | FCA Retail Requirement | Typical Offshore Position |

|---|---|---|

| Negative balance protection | Mandatory | Absent or discretionary |

| Leverage caps | 30:1 FX majors; 20:1 indices/gold; 5:1 equities | Often 200:1, 500:1 or higher |

| Margin close-out rule | Mandatory at ~50% of required margin | Absent or not standardised |

| Client money segregation (CASS) | Mandatory | Absent or unenforceable |

| FSCS compensation | Up to £85,000 per person per firm (firm failure) | No equivalent |

| FOS dispute resolution | Mandatory; decisions binding on firm | No equivalent |

| Risk warnings (audited % losing money) | Mandatory and standardised | Generic disclaimers only |

| Bonus/incentive restrictions | Prohibited | Frequently used |

| Crypto-asset derivative access | Prohibited for retail clients (since 2021) | Available |

Two elements in the table deserve particular attention. The Financial Services Compensation Scheme (FSCS), the UK’s statutory compensation scheme, covers up to £85,000 per eligible claimant per firm. The Financial Ombudsman Service (FOS) provides a dispute resolution route whose decisions are binding on the firm. Neither has any equivalent under most offshore frameworks.

FSCS scope clarification: FSCS compensation applies when an FCA-authorised firm becomes insolvent and cannot return your money. It does not cover trading losses. CASS segregation greatly improves, but does not absolutely guarantee, full and immediate recovery in insolvency. The FSCS operates as the additional backstop in those scenarios.

The crypto-asset derivatives ban for UK retail clients, in place since 2021, remains in force as of June 2026. This is distinct from the lifting of the ban on crypto exchange-traded notes (ETNs) for retail clients in October 2025, which covers a separate instrument category.

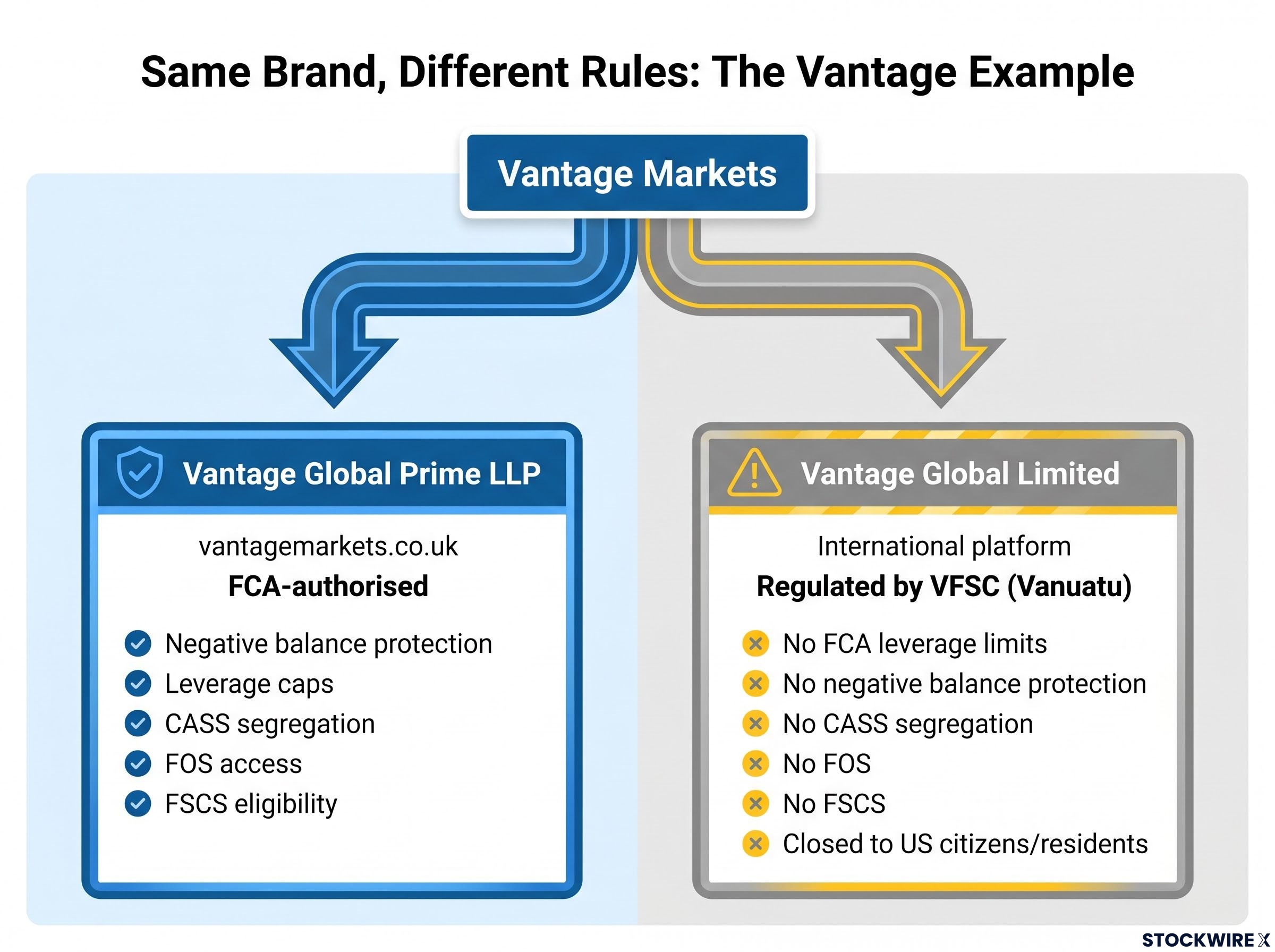

The abstract comparison becomes immediately concrete when you look at how a single broker group can operate under two entirely different regulatory frameworks, with the same branding on both.

Vantage Markets is a clear illustration. The group operates two entities:

The company’s own documentation makes clear that traders who sign up via the international platform do so without any solicitation from Vantage, with the firm characterising access as self-directed. The international platform is closed to individuals who hold US citizenship or residency. But for a UK-based trader who finds the international site through an ad or a search result, the distinction may not be obvious until after money has been deposited.

The principle to carry with you: Group-level FCA authorisation does not extend to accounts opened under the offshore entity. The question is never “does this broker have an FCA licence?” It is “under which entity is my account being opened?”

This pattern is not unique to Vantage. Many broker groups maintain both an FCA-authorised entity and a separate international entity under a less stringent regulator. The Vantage structure simply illustrates the mechanics in a way that makes the risk recognisable the next time you encounter it with any broker.

The appeal of offshore CFD brokers is real, and treating it as irrational does not help you make a better decision. Here are the four primary pull factors, and the regulatory reason each one is absent from FCA platforms:

The leverage and margin mechanics behind that acceleration are worth examining precisely, because the multiplicative relationship between leverage ratio and loss percentage is not intuitive: a 5% adverse price move on a 20:1 leveraged position produces a 100% loss on the margin deposit, not a 5% loss.

Each pull factor has a structural counterpart. Higher leverage means faster potential losses without the margin close-out backstop. Bonus structures create incentives to overtrade without the regulatory framework that limits those incentives because they are harmful.

There is also a fifth factor that is less about attraction and more about information: many traders simply do not realise they have moved outside FCA protection, particularly when the branding and interface are identical across a broker group’s FCA and offshore entities.

These checks take less than ten minutes and determine whether the legal safety net the UK has built for retail traders actually applies to your money.

Group-level FCA authorisation does not extend to accounts opened under a separate offshore entity within the same corporate structure. Verify the specific entity, not the brand.

This verification process works for any CFD broker you encounter, not just the examples discussed in this article.

The surface similarity between FCA-regulated and offshore CFD platforms obscures a difference that is not cosmetic but legal. The risk is structural, not necessarily a matter of broker intent. A well-intentioned offshore broker still cannot offer protections that do not exist under its regulatory framework.

For context, the FCA framework itself allows voluntary departures from certain retail protections. Traders who pursue elective professional client status with an FCA-authorised broker voluntarily reduce specific safeguards, including leverage caps and some disclosure requirements. This is a different mechanism from the offshore issue, but it illustrates the same principle: the FCA retail framework is the baseline, and any departure from it, whether through professional reclassification or through an offshore entity, reduces your protection.

The choice to trade with an offshore CFD broker is yours to make. The purpose of this article is to ensure that choice is made knowingly, with the trade-offs clearly understood. The five verification steps above are the foundation of any informed depositing decision; they cost you nothing but a few minutes, and they tell you everything about which legal framework stands behind your money.

For readers wanting to see how a comparable regulatory system handles the same structural risks, our full explainer on ASIC’s CFD framework examines the leverage caps, margin close-out rules, and negative balance protections that Australia introduced alongside the UK, including the compliance review that returned $40 million to more than 38,000 retail investors.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

FCA-authorised CFD brokers must provide negative balance protection, leverage caps of 30:1 on FX majors, mandatory client money segregation under CASS rules, and a margin close-out rule triggered at approximately 50% of required margin. Retail clients also gain access to FSCS compensation up to £85,000 and binding FOS dispute resolution.

An FCA-regulated broker is legally bound to protect retail clients through negative balance protection, leverage caps, client fund segregation, and access to statutory compensation and dispute resolution schemes; an offshore CFD broker operates under a separate, typically far weaker regulatory framework and provides none of those protections, even if it shares a brand name with an FCA-authorised entity.

Search for the specific legal entity (not just the brand name) on the FCA Register at register.fca.org.uk, confirm the counterparty entity named in your client agreement, check that the governing law is UK law, and verify that FSCS eligibility information is provided during onboarding. If the broker is offering leverage above 30:1 on FX majors, the account is almost certainly not under FCA retail protection.

No. Group-level FCA authorisation does not extend to accounts opened under a separate offshore entity within the same corporate structure. The question is which specific legal entity holds your account, not whether the broader group holds an FCA licence.

FCA retail leverage caps of 30:1 on FX majors were introduced specifically because higher leverage accelerates losses; the January 2015 EUR/CHF shock pushed retail traders across Europe into catastrophic negative balances overnight, demonstrating exactly what uncapped leverage can do. Offshore brokers operating outside the FCA's jurisdiction face no equivalent mandatory cap, so many offer 200:1 or 500:1 leverage without the negative balance protection backstop that would otherwise limit the damage.