ASX 200 Enters June 2026 With Stretched Valuations and Upside Risk

9 hrs ago

Meta Platforms has told investors it will spend between $125 billion and $145 billion on capital expenditure in 2026, a figure that dwarfs every rival in the technology sector and forces a question that no earnings call soundbite can settle: is this AI infrastructure buildout a competitive moat being constructed, or a financial liability being accumulated? In late May 2026, Meta formalised its Enterprise Solutions initiative, embedding engineers and product managers with corporate clients to accelerate AI adoption. CEO Mark Zuckerberg has signalled the company could monetise surplus AI computing infrastructure by offering third-party access, a move that would position Meta against AWS, Azure, and Google Cloud in a market Bank of America projects could surpass $1 trillion by 2028. What follows is an examination of what is confirmed, what remains speculative, and what the strategic shift from advertising platform to AI infrastructure company means for the long-term META investment case.

Meta’s Enterprise Solutions initiative was formally announced in late May 2026. It is an organisational and go-to-market effort, not a separately reported financial segment. No revenue line items tied to Enterprise Solutions appear in Meta’s formal filings as of 31 May 2026, and no client adoption metrics have been disclosed.

That distinction matters more than the headline suggests. The market has moved quickly to price in enterprise AI momentum, but the financial reporting has not moved with it.

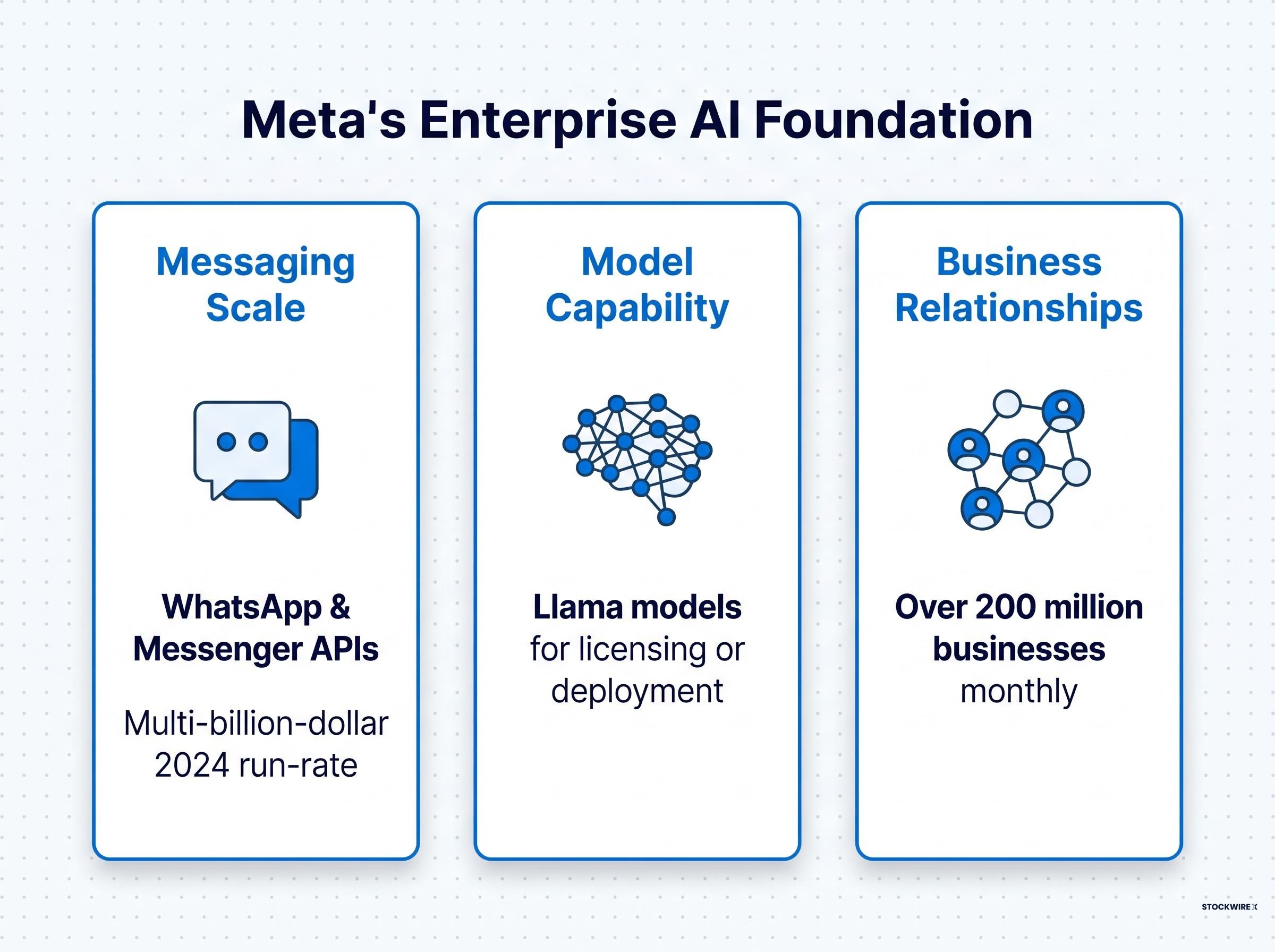

Meta’s enterprise-facing activities currently sit across three areas, each at a different stage of commercial maturity:

More than 200 million businesses use Meta’s apps monthly for business purposes including advertising and messaging, according to the company’s 2024 Form 10-K.

That figure represents the scale of existing business relationships, not adoption metrics for the newly branded Enterprise Solutions initiative. Investors evaluating META on enterprise AI momentum need to understand which parts of the story are reported financial reality, and which remain strategic intention. As of today, the gap between the two is wide.

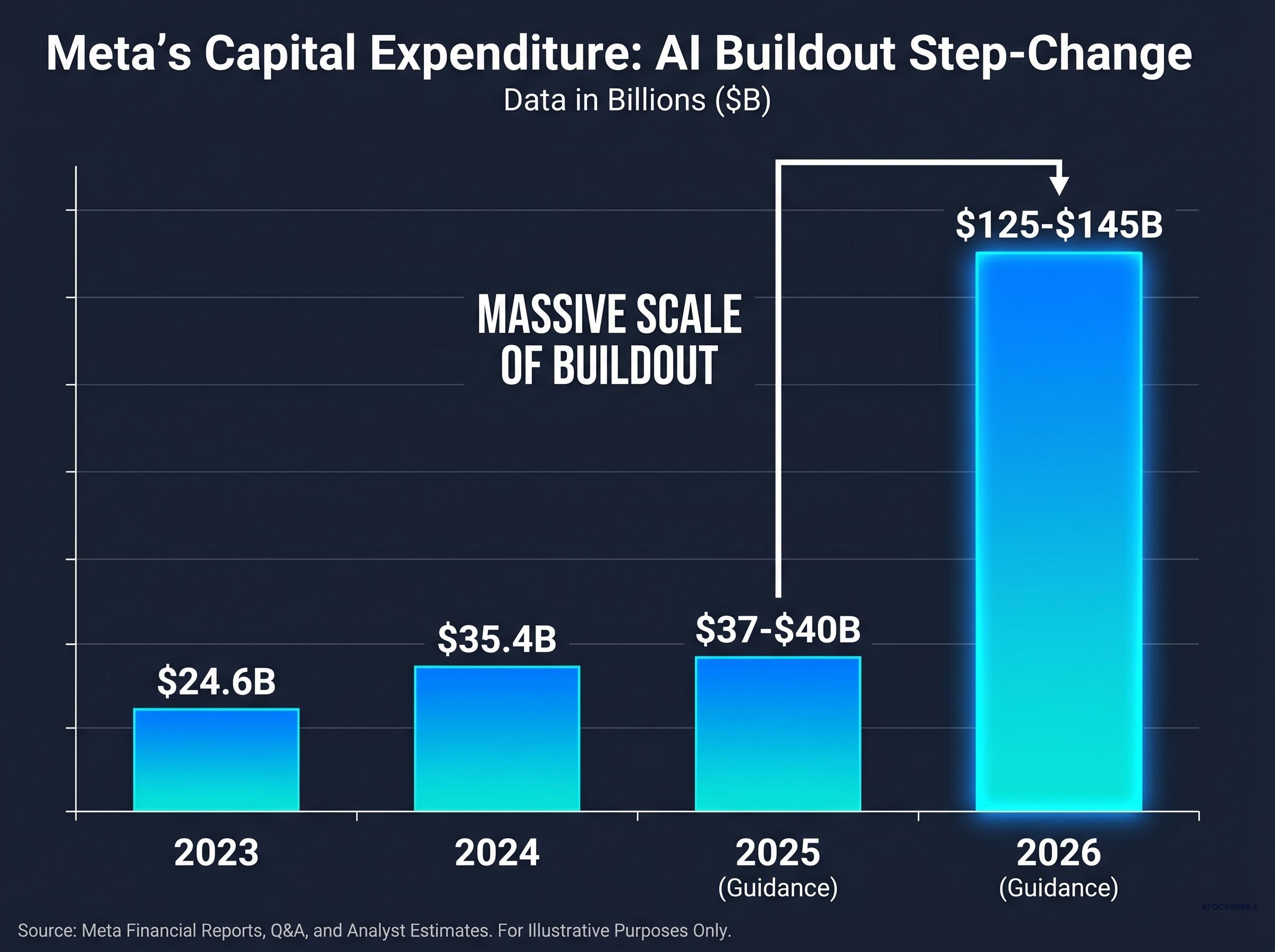

The numbers tell the story of acceleration more clearly than any management commentary.

| Year | Capex Figure | Status | Primary Justification (per filing) |

|---|---|---|---|

| 2023 | $24.6 billion | Actual | Servers including AI infrastructure and data centres |

| 2024 | $35.4 billion | Actual | Servers including AI and non-AI hardware and data centres |

| 2025 | $37-$40 billion | Guidance | Continued AI and data centre investment |

| 2026 | $125-$145 billion | Guidance | Higher component pricing and additional data centre costs for future capacity |

The step-change between 2025 and 2026 is not a gradual ramp. Capex guidance more than tripled in a single year. That is a structural recalibration of Meta’s capital allocation, and it creates a depreciation obligation that investors need to model explicitly against returns through 2027 and 2028.

The free cash flow implications of the capex raise are substantial: revised analyst estimates cut Meta’s 2026 free cash flow from approximately $35 billion to $25 billion, and the company carries around $50 billion in debt alongside $107 billion in locked-in near-term infrastructure obligations that limit financial flexibility regardless of how advertising revenues perform.

Meta’s filings describe this investment as directed at first-party product improvements: advertising systems, content recommendations, AI assistants, and generative AI features. The official justification is not a cloud business.

“Investing aggressively in AI, which we expect will drive long-term value across our apps and devices.” — Meta Q1 2026 management commentary, 29 April 2026

The statement frames the spend as internally directed. Whether the infrastructure eventually serves external customers is a separate, unanswered question.

Enterprise AI adoption, in practical terms, refers to companies deploying artificial intelligence tools to automate workflows, manage customer interactions, and analyse data at scale. These tools are typically accessed through APIs (application programming interfaces, which allow software systems to communicate with each other), embedded models, or managed infrastructure provided by a technology vendor.

The reason Meta’s position in this market is structurally plausible, rather than purely aspirational, comes down to three existing assets:

Bank of America projects the combined enterprise AI and cloud services market could surpass $1 trillion by 2028. That is a broad third-party market estimate, not a Meta-specific revenue forecast, but it frames the size of the opportunity that the company’s infrastructure is being positioned to address.

Three categories of service are plausible based on Meta’s current infrastructure and public commentary:

API access to Llama-based models would allow enterprise customers to integrate Meta’s AI capabilities into their own products and workflows. Managed AI deployment for business messaging would extend the existing WhatsApp and Messenger business tools with AI-powered automation. Potential third-party access to surplus compute infrastructure would move Meta into direct competition with cloud hyperscalers.

The third category, surplus compute commercialisation, is a possibility Zuckerberg has signalled. It is not a formal announced product with timelines, pricing, or capacity commitments.

The more useful question for investors is not whether Meta can win the cloud wars. It is whether Meta needs to win them at all.

AWS, Azure, and Google Cloud hold deep enterprise relationships, established pricing models, compliance certifications, and developer ecosystems that took years to build. Meta’s filings and Q1 2026 commentary acknowledge competition from “other large technology companies” for AI talent, infrastructure, and products, but do not directly compare Meta to hyperscalers on cloud market share. No public source provides specific market share projections for a Meta cloud offering against these incumbents.

Custom silicon economics are shaping the infrastructure layer that Meta is building into: as inference workloads are projected to represent approximately 80% of the AI accelerator market by 2030, purpose-built chips from Alphabet, Amazon, and Microsoft are becoming most competitive precisely in the segment where Meta’s $125-$145 billion build is being deployed, creating a cost-per-token competitive dynamic that affects both what Meta pays to build and what enterprise customers will eventually compare it against.

The structural advantages and disadvantages are distinct:

FedRAMP authorization requirements represent one of the most significant structural barriers for any technology vendor seeking to serve U.S. federal government customers, requiring independent third-party assessment, continuous monitoring, and agency sponsorship before a cloud product can be approved for use across federal systems.

Bank of America’s investment thesis reframes the competitive question. Rather than positioning Meta as a cloud market share challenger, the thesis identifies enterprise customer revenues as a mitigant to the financial risks tied to overbuilding AI capacity.

Elevated depreciation costs are anticipated by investors for 2027 and 2028, tied directly to the infrastructure buildout now under way. If recurring enterprise revenues are established before that depreciation cycle peaks, even a fraction of the broader market opportunity could offset the margin pressure. The question is not whether Meta captures 10% of the cloud market; it is whether surplus compute monetisation at any meaningful scale changes the risk profile of a $125 billion capex commitment.

Bank of America maintains a Buy rating on Meta Platforms with an $835 price target, as of 31 May 2026, as reported in coverage authored by Jaiveer Shekhawat and published on Investing.com.

Bank of America: Buy rating, $835 price target on META as of 31 May 2026.

The bull case rests on three components, ordered by proximity to confirmation:

The investor concern context is real. Meta’s stock underperformed the broader market following October earnings, when the company disclosed substantial increases in operating and capital expenditure tied to AI development. The market’s scepticism centres on whether $125-$145 billion in 2026 capex generates adequate returns before depreciation peaks in 2027-2028.

Bank of America acknowledges this concern within its thesis. The bull case is not a dismissal of depreciation risk; it is an argument that enterprise monetisation catalysts could arrive in time to change the calculus.

The gap between the current thesis and a conviction position can be measured in four specific data points that Meta has not yet disclosed:

Meta’s management has characterised AI investment as a long-term value driver. The stock’s trajectory through 2026 and 2027 will likely be determined by whether enterprise monetisation signals emerge before the depreciation cycle peaks.

Meaningful disclosure would include a revenue or annual recurring revenue figure attributed to enterprise AI or compute services, client count or contract metrics for the Enterprise Solutions initiative, and explicit guidance on capex-to-enterprise-revenue conversion. Absent this level of disclosure, the enterprise AI opportunity remains a strategic thesis rather than a reported financial reality.

Investors who understand what specific disclosures are missing can monitor Meta’s quarterly communications for the signals that would either confirm or challenge the enterprise AI thesis, rather than reacting to headline sentiment. The investment case is not settled. It is waiting for the data.

For investors trying to benchmark when the missing disclosures described above might actually arrive, our full explainer on Goldman’s 2027 AI revenue timeline examines why Goldman Sachs analyst Gabriela Borges has dated meaningful AI software revenue outperformance to 2027, the specific monetisation test she applies to separate real AI fundamental stories from narrative-driven momentum, and why only two companies in Goldman’s coverage universe currently meet that standard.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Meta's Enterprise Solutions initiative, formalised in late May 2026, is an organisational and go-to-market effort that embeds engineers and product managers with corporate clients to accelerate AI adoption. It is not a separately reported financial segment, and no revenue line items tied to it appear in Meta's formal filings as of 31 May 2026.

Meta has guided for $125-$145 billion in capital expenditure in 2026, more than tripling its 2025 guidance of $37-$40 billion. The company attributes this to higher component pricing and additional data centre costs for future capacity.

Bank of America maintains a Buy rating on Meta Platforms with an $835 price target as of 31 May 2026, citing AI-related product introductions, emerging enterprise adoption trends, and the potential for enterprise revenues to offset depreciation risks tied to the infrastructure buildout.

Meta has signalled the possibility of offering third-party access to surplus AI computing infrastructure, which would put it in competition with cloud hyperscalers. However, Meta currently lacks an established cloud product, enterprise compliance certifications, and the developer ecosystems that incumbents have built over many years.

Investors should watch for enterprise AI revenue reported as a separate line item, client adoption metrics tied to the Enterprise Solutions initiative, a formal announcement of surplus compute commercialisation with pricing and capacity details, and a capex moderation signal in future guidance. None of these disclosures have been made as of 31 May 2026.