One soft inflation print does not end a hiking cycle. Markets appear to believe it might. Bank of America does not.

June 2026 headline CPI came in at -0.4% month-over-month, while core CPI notched a monthly fall that has occurred on fewer than ten occasions in over four decades. Markets responded by pricing roughly 40-42 basis points of cumulative Fed tightening for the rest of the year. BofA economist Aditya Bhave, writing in a client note published 17 July 2026, argues that reading is too dovish by nearly half.

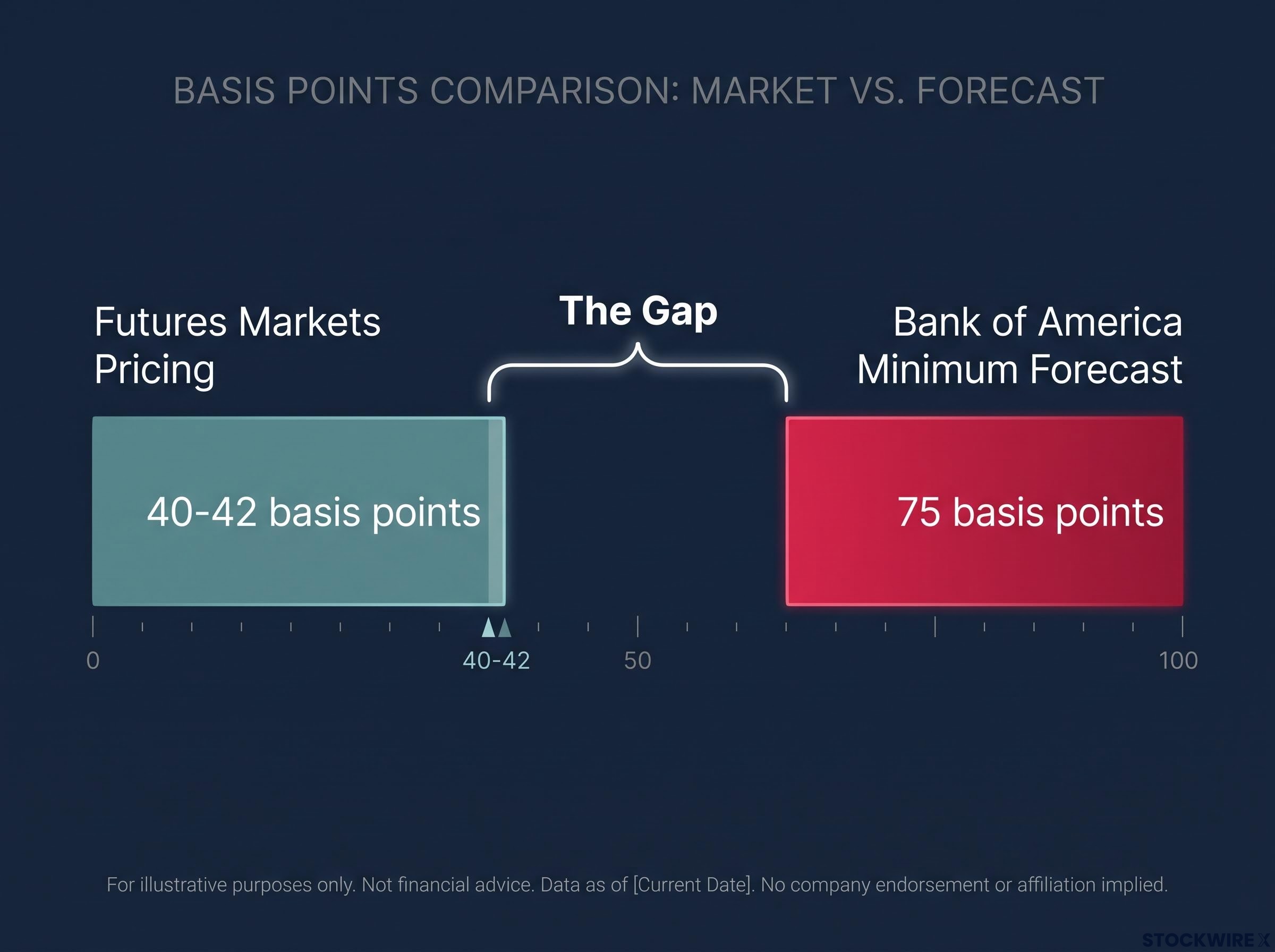

This piece works through BofA’s argument from the data layer to the institutional logic to the asset implications, so you can decide whether the gap between 40 basis points priced and 75 basis points forecast represents a market error worth positioning around.

What the June inflation data actually shows, and what it does not

The numbers looked encouraging at first glance. June 2026 headline CPI registered a 0.4% monthly drop, undershooting what analysts had anticipated. Core CPI also fell on a monthly basis, a result that has been recorded just seven times across the past four decades. On the back of those prints, BofA revised its core Personal Consumption Expenditures (PCE) tracking estimate for June down to 0.15% month-over-month, the measure the Federal Reserve actually uses to gauge underlying inflation pressure.

That revision is why BofA sees less urgency for a July move specifically. It is not why they see less tightening overall.

The distinction matters. A single soft monthly reading tells you where inflation went in one period. The year-over-year core PCE reading tells you where inflation sits relative to the Fed’s 2% target. That annual figure stood at 3.4% in May 2026 (the latest available data) and BofA projects it at approximately 3.3% going forward.

May 2026 core PCE held at 3.4% year-over-year, precisely matching consensus and sitting 140 basis points above the Fed’s 2% target, a reading that confirmed the central bank had no justification to shift away from its restrictive stance even before the June data complicated the picture.

- June headline CPI: -0.4% month-over-month

- Core CPI monthly decline: seventh occurrence since 1985

- Core PCE year-over-year: 3.4% actual (May 2026), approximately 3.3% projected

The Fed’s own July 2026 Monetary Policy Report characterises inflation as “elevated” relative to the 2% objective, citing ongoing supply shocks and sector-specific pressures.

The 130-140 basis point gap between current core PCE and the Fed’s target is the number that should anchor your assessment, not the monthly direction of a single component.

The Fed’s 2026 Monetary Policy Report confirms that core price inflation ran at 3.4% over the 12 months ending in May, providing the official data foundation beneath BofA’s argument that a single soft monthly print cannot close a 130-140 basis point gap to target.

When big ASX news breaks, our subscribers know first

Why BofA reversed course on rate hikes, and what the new forecast says

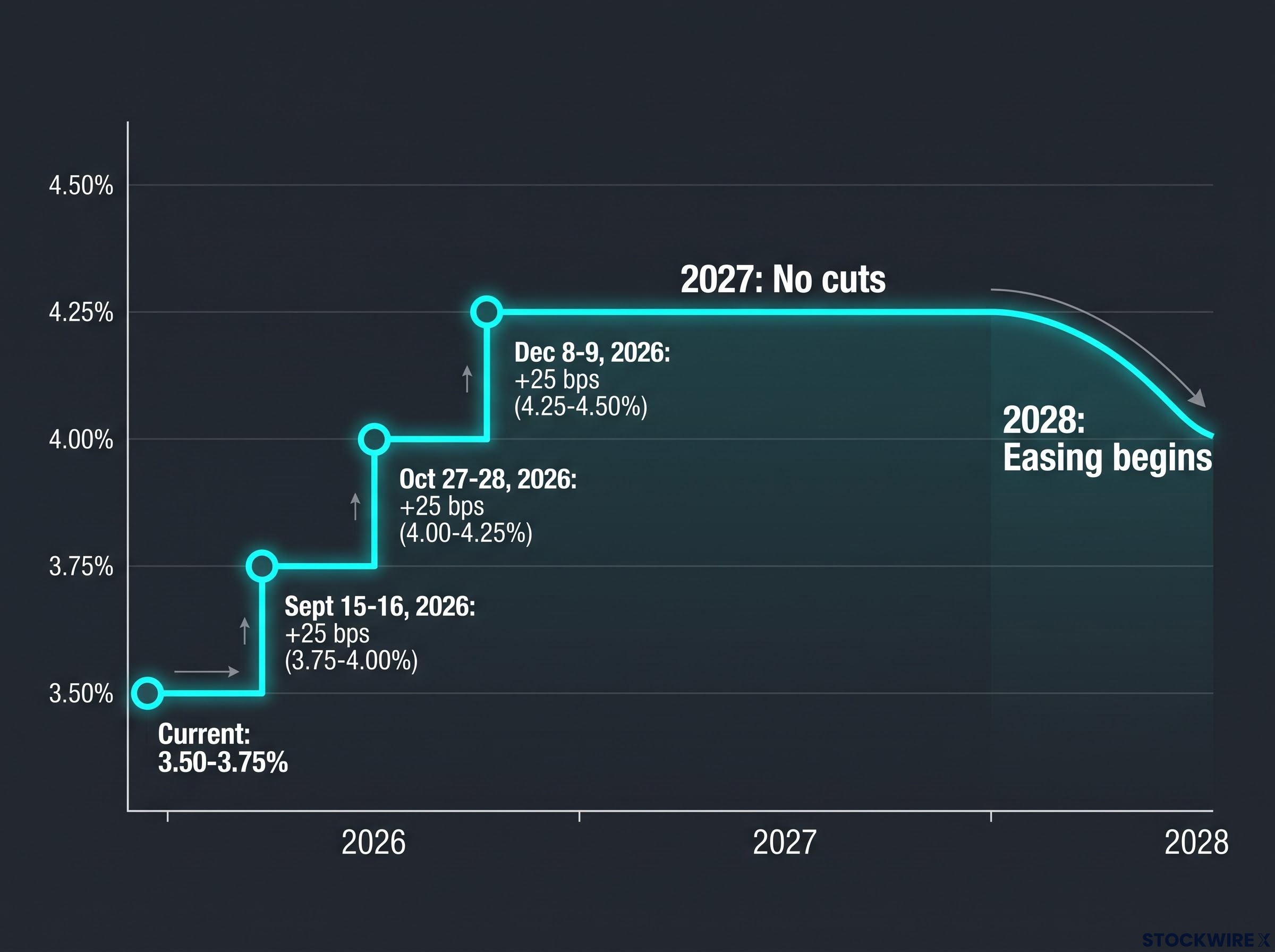

BofA spent the first half of 2026 with a baseline of no hikes. That changed in late June 2026, when the bank formally reversed its call, with the note published around 22 June 2026. Bhave’s 17 July follow-up lays out the logic and the meeting-by-meeting path.

The forecast is specific: three 25-basis-point hikes in September, October, and December 2026, bringing the fed funds target range from its current 3.50-3.75% to 4.25-4.50% by year-end. After that, BofA sees no cuts in 2027, with easing beginning only from 2028 onward.

| Meeting | Action | Post-Meeting Target Range |

|---|---|---|

| Current (as of July 2026) | Baseline | 3.50-3.75% |

| September 15-16, 2026 | +25 bps | 3.75-4.00% |

| October 27-28, 2026 | +25 bps | 4.00-4.25% |

| December 8-9, 2026 | +25 bps | 4.25-4.50% |

A no-cuts-until-2028 path means you should be thinking about a “higher for longer” environment lasting not months but years. That changes the calculus for any rate-sensitive exposure held today. BofA’s own forward PCE projection of approximately 3.3% year-over-year, with 2% not reached before 2028, is the data anchor beneath the timeline.

The gap between what markets are pricing and what BofA is forecasting

Two numbers frame the tension at the centre of this call:

- Futures markets are pricing approximately 40-42 basis points of cumulative tightening in 2026

- BofA’s minimum forecast calls for 75 basis points

If BofA is correct, the front end of the rate curve must reprice significantly higher. That creates a bear-flattening bias across the yield curve, where short-term yields rise faster than long-term ones, compressing the spread and pressuring anyone positioned for a dovish second half.

Bear-flattening dynamics were already visible in May 2026 as 30-year Treasury yields briefly exceeded 5.19%, a level not seen since 2007, with sector rotation accelerating and institutional allocators beginning to stress-test equity risk premia against a structurally higher rate environment.

For investors holding long-duration positions or rate-sensitive equity exposures, the implication is direct: repricing risk that is not yet reflected in current valuations.

Reading the July pause correctly

The July 28-29 FOMC meeting is the first test. BofA sees a July hike as possible but not the base case. The soft June data gives the Fed cover to skip without appearing to capitulate on inflation.

The distinction BofA draws is between a tactical skip and a dovish pivot. A pause in July does not change BofA’s total tightening forecast. It changes only the timing. The same 75 basis points would be delivered across the remaining meetings: September 15-16, October 27-28, and December 8-9.

Markets that interpret a July hold as “the hiking cycle is over” are, in BofA’s framing, misreading a scheduling choice as a policy signal. If that misread persists, it could produce a short-term relief rally followed by a sharper correction when the cycle resumes in September.

Understanding why core PCE is the number that drives Fed policy

When BofA argues the Fed should keep hiking despite a soft monthly print, the argument rests on a specific measure. Understanding which measure, and why, allows you to filter noise from signal in every future inflation release.

The Fed’s statutory inflation target is expressed in terms of core PCE, not headline CPI. Core PCE strips out volatile food and energy prices and captures a broader basket of consumer spending than CPI does, making it a more durable gauge of underlying price pressure.

The logic runs in three steps:

- The Fed targets core PCE year-over-year at 2%

- That reading currently sits at 3.3-3.4%, roughly 130-140 basis points above target

- One soft monthly print does not change the annual trend

BofA frames the June monthly CPI decline as “noise, not signal,” because the year-over-year core PCE reading, the measure the Fed actually targets, has not materially shifted.

This is not selective framing. It reflects how the Fed itself thinks about the data. The Fed’s own 2026 core PCE projection sits at approximately 3.3%, with 2% not reached before 2028. When you see a monthly CPI figure generate headlines, check where core PCE year-over-year sits before drawing conclusions about policy direction. That single habit gives you a more accurate read on the rate path than any headline number will.

The Warsh factor, and why BofA sees institutional reasons to move

BofA’s hawkish call is not purely data-driven. It also reflects a specific reading of the new Fed chair’s incentives.

Kevin Warsh was sworn in on 22 May 2026. His first FOMC decision came on 17 June 2026, where rates were held at 3.50-3.75%. BofA’s reading of that hold, and of Warsh’s subsequent congressional testimony, is that the new chair has reinforced a hawkish reaction function without providing any procedural off-ramps for delay.

BofA’s credibility thesis runs as follows: moving relatively early in his tenure allows Warsh to establish himself as a determined inflation fighter, while attributing the underlying problem to the policy choices of his predecessor. Hiking sooner locks in that advantage. A prolonged delay, by contrast, risks making the inflation problem his own to answer for.

Bhave’s assessment of Warsh’s recent congressional testimony draws out four key takeaways from the session: a reaffirmed intention to bring inflation back to target; an upbeat assessment of the productivity outlook; an absence of any fresh policy direction; and no suggestion that newly formed task forces or ongoing policy reviews would justify pushing tightening further down the calendar.

Warsh’s congressional testimony on 14 July 2026 confirmed the Fed’s commitment to price stability was unanimous, closing the interpretive gap that had allowed markets to treat the June hold as a soft pivot and reinforcing the hawkish reaction function BofA had already priced into its three-hike forecast.

A Fed chair with strong institutional incentives to demonstrate inflation-fighting credibility is less likely to interpret a single soft data print as permission to pause indefinitely. That is precisely why BofA sees Warsh as unlikely to shift the hiking path on the basis of June’s CPI alone. Fed policy is not purely a mechanical response to data; understanding the new chair’s credibility calculus helps you anticipate moves that the numbers on their own would not predict.

The next major ASX story will hit our subscribers first

What to watch before the September decision arrives

BofA has been specific about what would change its call. Three conditions would derail the planned hikes:

- A significant slowdown in payroll growth

- Persistently weak core PCE readings

- A substantial drop in equity markets

Short of those, the base case holds. The question for investors is whether the data between now and September confirms BofA’s view or undercuts it.

| Meeting Date | BofA Expected Action | Key Data to Watch Before Meeting |

|---|---|---|

| July 28-29, 2026 | Possible pause (skip, not pivot) | Fed communication, Warsh tone at press conference |

| September 15-16, 2026 | +25 bps (first projected hike) | July and August core PCE, payroll reports, equity market stability |

| October 27-28, 2026 | +25 bps | September core PCE, labour market trajectory |

| December 8-9, 2026 | +25 bps | Q3 GDP revision, cumulative PCE trend |

The September 15-16 meeting is the first real test of whether the market’s 40-basis-point view or BofA’s 75-basis-point view is correct. Watch the futures-implied cumulative tightening number between now and then. If it drifts toward 75, BofA’s view is being adopted. If it stays near 40, the gap persists and positioning risk builds for one side or the other.

Investors who positioned based on the June CPI print face the sharpest repricing risk if BofA proves right. Knowing what data BofA itself says would change its call gives you a concrete checklist rather than a fixed directional bet.

One soft print does not reprice a cycle

BofA’s core argument compresses to a single point: the June CPI miss was meaningful enough to reduce July urgency but not large enough to change the total tightening required. The year-over-year core PCE reading, not the monthly headline, is the policy signal, and that signal still points to 75 basis points of hikes.

The central tension you should carry forward is live, not settled. Futures pricing approximately 40 basis points versus BofA’s minimum 75 basis points represents a market dislocation that will resolve in one direction or the other before year-end.

Treat the current pause window as an opportunity to assess your rate-sensitive exposure, not as confirmation that the hiking cycle has ended.

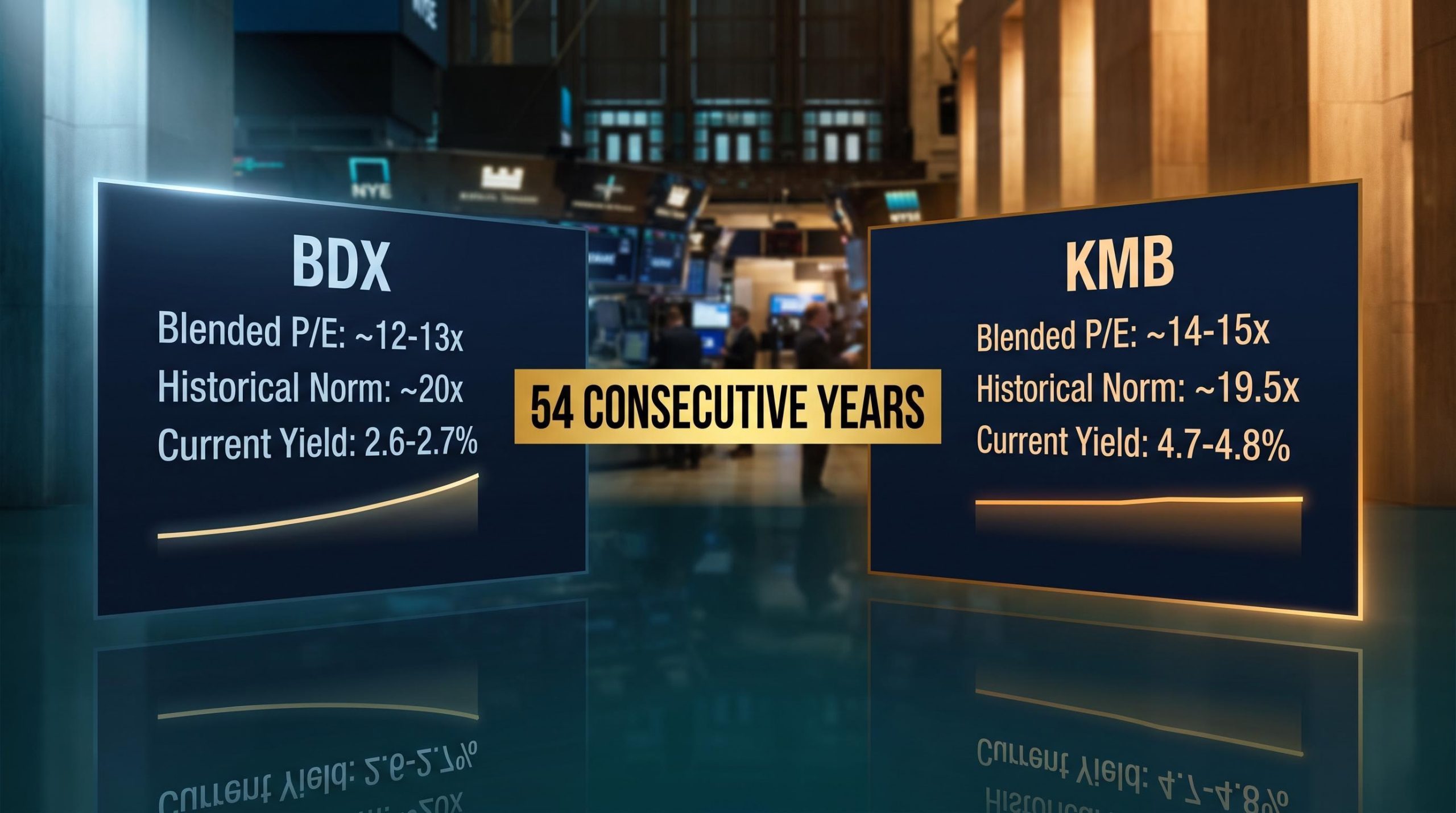

Rate-sensitive equity exposure absorbs prolonged tightening very differently depending on balance-sheet quality, dividend coverage, and duration characteristics, with historically costly errors clustering around concentrated bets on a rapid pivot that central bank communications are explicitly ruling out.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.

—