Most investors who say they are “investing in AI” are actually making a concentrated bet on one narrow slice of a much longer chain. If your AI exposure begins and ends with a GPU designer or a ChatGPT-adjacent application company, you are not investing in AI broadly. You are investing in a single layer of it, often without knowing what sits above or below.

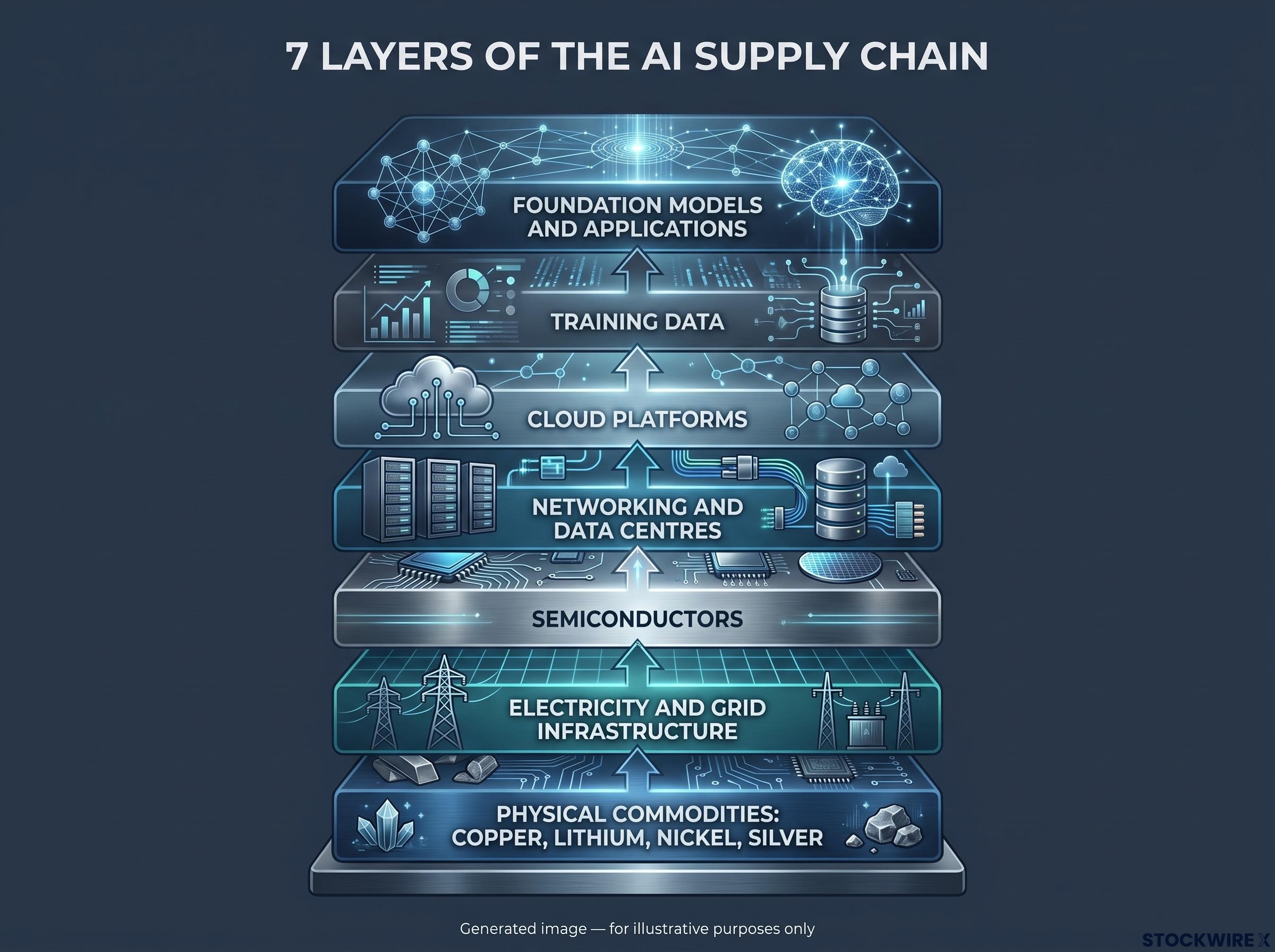

The AI ecosystem is not a single technology. It is a multi-layer supply chain with seven structurally distinct levels, running from physical commodities in the ground to the interface on your phone screen. Each layer has different economics, different competitive dynamics, and different risk characteristics. Value does not flow evenly across them, and neither does risk.

What follows here is a structured map of the entire AI supply chain, layer by layer. By the time you reach the end, you will know which layer any AI-related company operates in, what kind of moat that layer tends to generate, and where the current bottlenecks are concentrating returns.

The AI supply chain is not one investment, it is seven

When you hear “AI investing,” your mind probably goes straight to the companies building models or the chips powering them. That instinct is understandable, but it compresses seven structurally different businesses into a single mental category. The more useful frame is a stack of sequential dependencies, where each layer requires the one below it to function.

Here are the seven layers, from the base of the stack to the top:

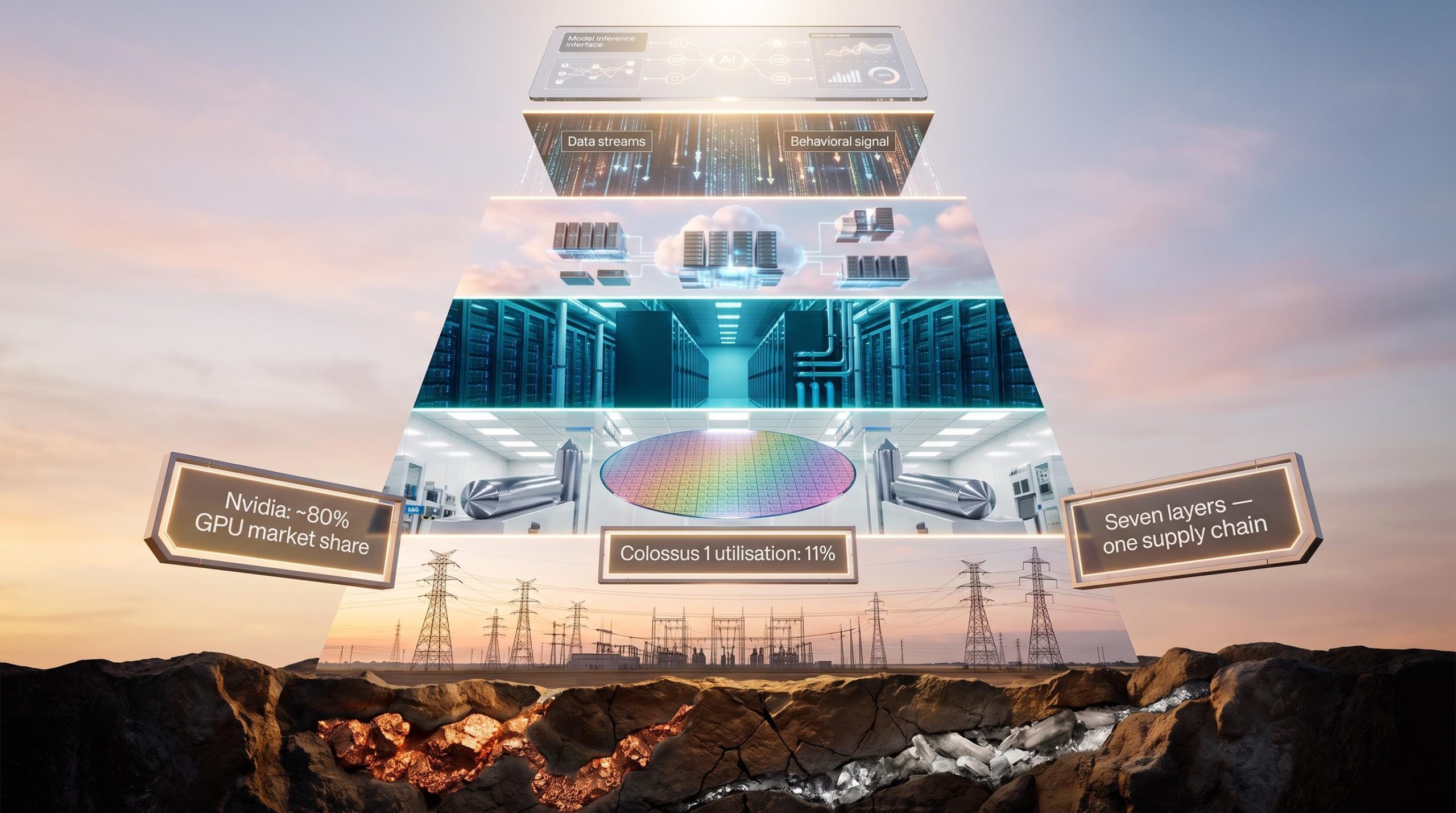

- Physical commodities: copper, lithium, nickel, silver, and specialty metals that physically build AI infrastructure

- Electricity and grid infrastructure: the power supply, grid connections, and energy generation that keep data centres running

- Semiconductors: GPUs, accelerators, foundries, lithography equipment, and high-bandwidth memory

- Networking and data centres: switches, optical interconnects, cooling systems, and specialised facilities

- Cloud platforms: hyperscalers that aggregate hardware into scalable AI-as-a-service offerings

- Training data: the proprietary datasets that feed model development

- Foundation models and applications: the models and products most people see when they think of AI

The layers are sequential, not parallel. A disruption at layer two (energy) cascades through every layer above it. A shortage at layer three (semiconductors) constrains what the cloud platforms can offer and what models can be trained. Which layer a company operates in determines its moat type, its exposure to different macro drivers, and how it performs as the binding constraint in the AI build-out shifts over time.

Frontier foundation model training already costs tens of millions of dollars and is heading toward hundreds of millions. The majority of that spend is concentrated in the hardware and cloud layers below. Buying a single AI application company is structurally different from buying a GPU maker or a copper miner, and understanding that difference is the first step toward deliberate rather than accidental AI exposure.

The scale of the AI investment boom gives the supply chain map its urgency: US IT spending hit 4.9% of GDP in Q1 2026, surpassing both the dot-com peak and the cloud buildout peak, with combined hyperscaler capital expenditure commitments for 2026 sitting in the $600-805 billion range before sovereign-scale programmes like the Stargate Project are included.

When big ASX news breaks, our subscribers know first

What the physical layers supply (and why they matter to investors)

The most glamorous part of the AI story gets the most attention. The most necessary part gets the least. At the base of the stack sit two layers that most investors overlook entirely: physical commodities and electricity.

- Commodities: Copper wires every power connection and networking cable in a data centre. Lithium and nickel supply the backup batteries and grid-scale storage that keep facilities operational. Silver and specialty metals go into circuit boards and high-end electronics. Companies in this space include diversified miners and specialty metal producers.

- Electricity and grid infrastructure: Every AI data centre is, at its core, a large industrial electricity load. It needs high-capacity grid connections, long-term power purchase agreements, and increasingly its own onsite generation. Your exposure options here include regulated utilities, grid operators, renewable power developers, and manufacturers of high-voltage equipment.

AI power infrastructure is attracting capital at a pace that is shifting technology sector valuations away from software multiples and toward physical asset economics, with Wall Street projecting $530-700 billion in global data centre IT spending through 2026 alone and alternative energy providers emerging as a primary beneficiary class.

Running a local AI model on a laptop for a single query caused the device to run at maximum fan speed for approximately 8 minutes. That is the thermal and energy intensity of AI compute at consumer scale. At data-centre scale, multiply by millions of simultaneous queries.

These companies benefit from AI infrastructure growth regardless of which models or platforms ultimately win. No model can be trained, and no inference can be run, without copper, power, and cooling. If you want AI exposure that is insulated from model competition and platform risk, the commodities and energy layers offer structurally indirect but durably necessary positions.

Semiconductors and the chokepoint economics of AI hardware

A handful of semiconductor companies capture an outsized share of AI-related value. The reason is not just market share but the physical and intellectual complexity that makes replication nearly impossible.

Nvidia holds approximately 80% of the discrete GPU and AI accelerator market. Its dominance originated from an unexpected overlap: the parallel processing architecture designed for gaming graphics turned out to be precisely what AI model training demands. AMD and a handful of smaller competitors contest specific workloads, but the gap remains wide.

The real-world consequences of hardware choices are measurable. SpaceX’s Colossus 1 cluster was assembled using three distinct GPU models from Nvidia, including H100s. Because each model completed tasks at different speeds, the processors fell out of sync during training runs, leaving the overall facility with a hardware utilisation rate of roughly 11%. Colossus 2 corrected this by standardising on a single GPU specification across the entire system, which made it viable for full model training rather than inference workloads alone. The choice between hardware uniformity and a mixed configuration determined whether a multi-billion dollar facility could actually develop new models.

For your portfolio, the Colossus case tells you that semiconductor exposure is not just a bet on chip demand. It is a bet on which architectural choices dominate the next build-out cycle.

Foundries, equipment, and memory: the rest of the hardware stack

TSMC fabricates the advanced chips designed by Nvidia, AMD, and others. Its geographic concentration in Taiwan represents a systemic geopolitical risk that runs through every layer above it. ASML supplies the extreme-ultraviolet lithography tools needed for the most advanced chip nodes and has no direct competitor at the leading edge. Memory suppliers including Micron and SK Hynix provide the high-bandwidth memory AI workloads demand, a distinct bottleneck from raw compute.

| Sub-layer | Key function | Representative companies | Primary moat type |

|---|---|---|---|

| GPU / accelerator designers | Design processors optimised for AI training and inference | Nvidia, AMD | IP, scale, software ecosystem |

| Foundries | Fabricate advanced chips at leading-edge nodes | TSMC | Manufacturing complexity, capex |

| Equipment makers | Supply lithography and fabrication tools | ASML | Sole-source technology monopoly |

| Memory suppliers | Provide high-bandwidth memory for AI workloads | Micron, SK Hynix | Scale, process technology |

Semiconductors offer the most direct and levered exposure to AI compute growth. But the concentration of value in a small number of firms with deep IP and manufacturing moats means the risk profile looks very different from owning an AI application company.

From raw hardware to cloud services: how hyperscalers aggregate the stack

Hardware and data centres only become economically powerful when aggregated at massive scale. That is what the hyperscalers do, and it is why they occupy such a structurally advantaged position in the AI supply chain.

The three dominant cloud platforms are:

- Amazon Web Services (AWS): The largest cloud platform by market share, now offering AI-specific training clusters and managed model APIs alongside its core infrastructure

- Microsoft Azure: Holds a direct stake in OpenAI, giving it a unique distribution channel for frontier model capabilities integrated into enterprise products

- Google Cloud Platform (GCP): Develops its own frontier models (Gemini) while also investing in Anthropic, positioning it on both sides of the model and infrastructure divide

Between the raw hardware and these platforms sits a physical intermediary layer: networking and data-centre infrastructure. Companies like Arista Networks, Cisco, and data-centre operators including Next DC and AirTrunk in Australia build the high-performance switches, optical interconnects, and liquid cooling systems that make large-scale AI compute physically possible.

Owning a hyperscaler is effectively owning a share of every AI workload that runs on its infrastructure, regardless of which application wins.

The structural characteristics that entrench hyperscaler advantage are well established: high fixed costs, strong network effects, high switching costs, and economies of scale. For you as an investor, this layer offers the closest equivalent to owning the infrastructure that every AI workload must pass through, without needing to pick the winning model or application.

Hyperscaler earnings divergence in Q1 2026 made the structural advantages described here visible in real-time: Google Cloud grew 63% year-over-year while Meta fell approximately 10% after earnings, with markets actively rewarding infrastructure commitment and punishing heavy AI spending without a visible near-term returns pathway.

Why training data is quietly becoming the binding constraint

Here is where the assumption flips. Most investors assume that compute power, specifically GPUs and cloud capacity, is the scarce resource in AI. That was true two years ago. It is becoming less true now.

People in very senior roles at major technology companies have reported that the real bottleneck on frontier model development is no longer processing capacity but access to sufficient high-quality data. Usable public web content has been substantially depleted, and the volume of material available from open internet sources has largely been absorbed by existing training runs.

The arXiv research on training data scarcity projects that human-generated public text cannot sustain frontier model scaling beyond this decade, providing a quantitative basis for why data access is displacing compute as the primary binding constraint on AI development.

The scramble for new data is producing some unusual strategies. Technology companies are reportedly approaching retailers to license camera footage of physical environments, illustrating just how scarce usable training data has become. Academic research now treats data acquisition as a first-class stage in the AI supply chain, with traditional supply-chain tools struggling on verifiability and traceability.

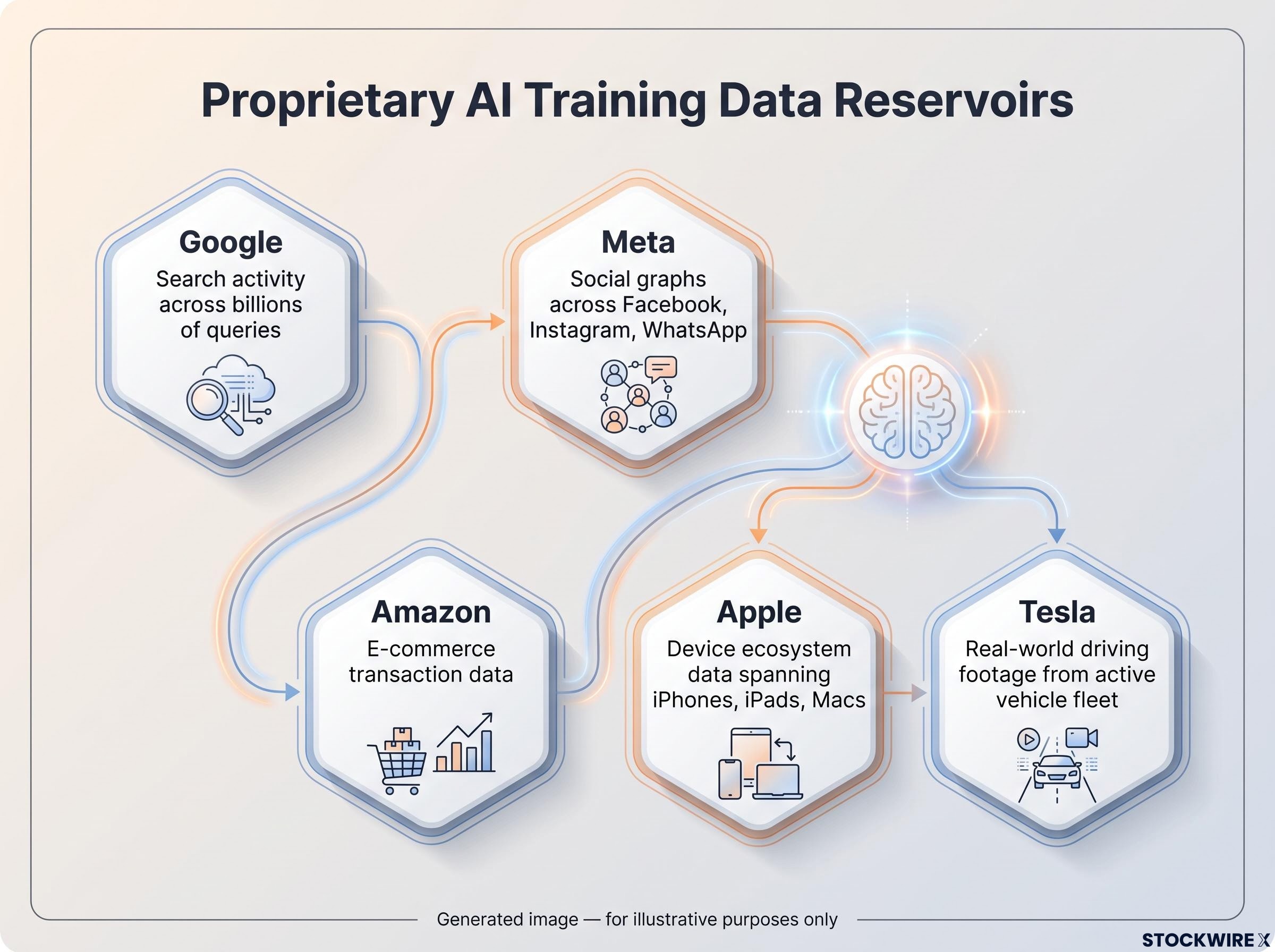

Which companies hold the data advantage

The companies best positioned are not AI startups. They are large incumbent platforms sitting on deep reservoirs of proprietary behavioural data:

- Google: Search activity across billions of queries generates continuous, high-signal data on human intent and knowledge-seeking behaviour

- Meta: Social graphs and interaction data across Facebook, Instagram, and WhatsApp capture patterns of human communication and preference

- Amazon: E-commerce transaction data provides detailed records of purchasing behaviour, product preferences, and commercial intent

- Apple: Device ecosystem data spanning iPhones, iPads, and Macs captures usage patterns across applications, health, and daily routines

- Tesla: An unmatched volume of recorded real-world driving footage from its active vehicle fleet gives it a domain-specific data moat in autonomous vehicles

For you, the data scarcity shift means that platforms previously valued primarily for advertising or e-commerce revenues may be underpriced for their AI training data assets. Pure-play AI companies without proprietary data pipelines face a structural disadvantage that compounds over time.

Foundation models and applications: the most visible but most contested layer

This is the layer you almost certainly think about first when you hear “AI investing.” It is also, structurally, the most competitive and the least capital-protected.

The foundation model landscape includes:

- OpenAI (GPT series, ChatGPT): first-mover in consumer AI, backed by Microsoft’s infrastructure and distribution

- Anthropic (Claude series): positioned on AI safety and enterprise reliability, backed by Google and Amazon

- Google Gemini: developed in-house with direct integration into Google’s search and cloud products

- Meta Llama: open-weights models that commoditise access to frontier capabilities

- xAI Grok: built on SpaceX’s Colossus infrastructure with access to X (formerly Twitter) data

The competitive dynamics here are structurally different from hardware or cloud. Capital barriers are lower relative to chips and fabs. Entry and exit happen rapidly. Most new products sit at the top of the stack and must compete primarily on distribution, domain expertise, and workflow integration rather than underlying model superiority, because generic AI capability is increasingly available to any company via API.

Generic AI capability is becoming a commodity. Durable value at the application layer depends on distribution, domain context, and workflow lock-in.

Where durable differentiation does exist, it comes from domain-specific context, proprietary workflows, integration into existing enterprise systems, and user relationship lock-in. Apple’s comparatively restrained AI positioning (Apple Intelligence has been considered underwhelming relative to competitors) illustrates that financial resources alone do not guarantee application-layer dominance; distribution and user experience matter more.

Understanding this dynamic prevents you from over-allocating to highly visible AI names whose competitive moats may be shallower than their market positioning suggests, particularly once underlying model capabilities commoditise further.

The next major ASX story will hit our subscribers first

Using the supply chain map to make deliberate investment decisions

You have now seen the full stack. The question is what to do with it. Here is a four-question framework you can apply to any AI-related investment you encounter:

- Which layer does this company operate in? Commodities, energy, semiconductors, networking, cloud, data, or applications? Each responds to different macro drivers and competitive dynamics.

- What kind of moat does that layer tend to generate? Scale and capex moats (chips, fabs, cloud) behave differently from data moats (platforms) or distribution moats (applications).

- Which current bottleneck does this company benefit from? Is the position leveraged to compute shortage, energy constraints, cooling capacity, or data scarcity?

- How does this position perform if the binding constraint shifts? A company that benefits from a GPU shortage may fare differently once data becomes the primary constraint.

Research from central banks and consultancies warns that highly visible AI names can trade at levels reflecting speculative enthusiasm more than current earnings power. Lower-profile infrastructure or data-rich incumbents may carry more durable leverage. The organising principle from industry analysis is direct: intelligence commoditises downward, and value accrues at bottlenecks.

The BIS Annual Economic Report on AI valuations flags that equity prices for firms at the core of AI development embed implied long-term earnings growth well above historical benchmarks, with hyperscaler capital expenditure frequently outpacing reported earnings and requiring debt issuance to sustain.

| Layer | Moat type | Current bottleneck exposure | Key valuation risk |

|---|---|---|---|

| Physical commodities | Resource access, scale | Infrastructure build-out demand | Cyclical commodity pricing |

| Electricity / grid | Regulatory, infrastructure | Grid capacity constraints | Regulatory and policy shifts |

| Semiconductors | IP, manufacturing complexity | GPU and memory shortage | Geopolitical concentration (Taiwan) |

| Networking / data centres | Operational, location | Cooling and power density | Construction cycle timing |

| Cloud platforms | Scale, switching costs | Overall compute demand | Capex commitments vs. returns |

| Training data | Proprietary data access | Data scarcity (emerging) | Privacy and copyright regulation |

| Models / applications | Distribution, workflow lock-in | User acquisition and retention | Commoditisation of model capability |

Concentrating entirely in GPU designers means your AI exposure rests on a single bottleneck. Spreading across a hyperscaler, a data-centre operator, a memory supplier, and a data-rich platform gives you structurally distinct positions at different points in the stack. A structured framework prevents both under-exposure (dismissing AI as a bubble) and over-concentration (buying only the most visible names).

Which layer you own determines which AI story you are in

The AI supply chain is not a single bet. It is seven structurally distinct investment decisions, each with different moats, different risk exposures, and different sensitivities to where the binding constraint sits at any given moment. Your copper miner responds to different forces than your hyperscaler, and both behave differently from your application-layer pure play.

The most important question you can ask about any AI-related position is not “is this company an AI winner?” but “which layer does it occupy, and is the moat at that layer durable as the bottleneck shifts?”

The binding constraint has already moved once, from raw compute availability to training data scarcity, and it will move again. The supply chain map is not a static reference. It is a dynamic framework worth revisiting as the technology matures, as new bottlenecks emerge, and as value migrates through the stack.

For investors wanting to apply the supply chain map to a concrete portfolio construction problem, our dedicated guide to AI exposure without frontier lab bets examines why network-effect businesses and structural moat companies offer more durable compounding than frontier model positions, with specific analysis of valuation compression risk at the application layer.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.