The most obvious way to invest in AI, buying the companies building it, may be the riskiest approach of all. That sounds counterintuitive when the technology is clearly reshaping every industry it touches. But the paradox is worth sitting with, because it shapes how you should think about where your capital actually belongs.

Frontier AI competition is intensifying, yet identifying which lab, chip designer, or cloud provider will dominate a decade from now requires a level of technical foresight that even domain experts cannot reliably provide. Add to that a structural margin problem: competitive pressure is already forcing prices downward across AI services, while large enterprise buyers are deliberately spreading workloads across multiple vendors to prevent any single provider from gaining pricing leverage. That creates a double layer of uncertainty that makes high-multiple frontier AI names a structurally fragile base for long-term compounding.

Here is a framework for building AI exposure around businesses whose moats get stronger as AI spreads, rather than businesses that need to win the AI race to justify their valuations. It covers the specific risks of frontier AI bets, the structural logic of network effects, two concrete case studies, and a five-question checklist you can apply to any company in your portfolio.

Why betting on frontier AI winners is harder than it looks

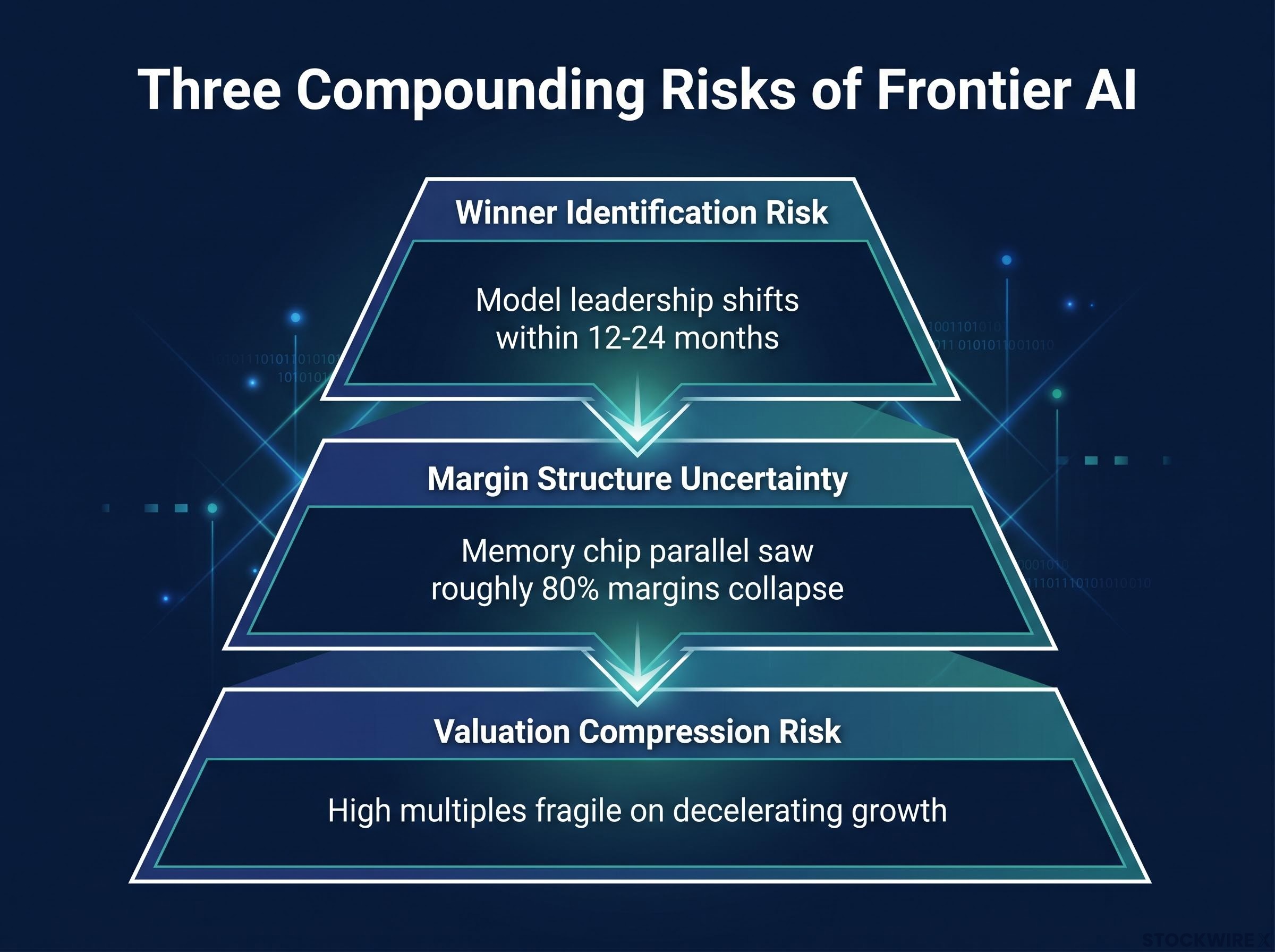

The difficulty here is not whether AI is transformative. It clearly is. The difficulty is whether the businesses that look like leaders today can be reliably identified and held with conviction across a 5-10 year timeframe. Three layers of risk compound on top of each other, and each one is worth understanding on its own terms.

- Winner identification risk. Model leadership can shift within 12-24 months due to architectural innovations, compression techniques, or on-device inference advances. Picking the lab or cloud provider that will dominate a decade from now requires precision about future technical leadership that even specialists cannot reliably deliver.

- Margin structure uncertainty. Current profit pools may not be structurally durable. Enterprise customers are explicitly designing multi-vendor stacks to limit lock-in, which constrains long-term pricing power for any single provider.

- Valuation compression risk. Paying high multiples for businesses with uncertain long-term economics is a double bet: the business must succeed operationally, and the market must continue to award it a premium multiple. History shows that even successful growth companies often experience multiple compression once growth decelerates or competition normalises.

The memory chip parallel is instructive. When memory supply tightened historically, gross margins surged toward roughly 80%, attracting fresh capital until new capacity arrived and margins collapsed back toward commodity levels. The margin structures emerging across AI-adjacent hardware and infrastructure today follow a recognisably similar pattern.

These three risks do not exist in isolation. They compound. Winner uncertainty makes it harder to justify paying a high multiple. Margin cyclicality makes it harder to trust the earnings that multiple is applied to. And valuation compression risk means that even if the business executes, your returns can still disappoint over a long horizon. That compounding fragility is the structural problem with frontier AI as a portfolio foundation, and it is the reason an alternative framework matters.

AI stock valuation risk is compounded by an index-level illusion: large opposing moves by individual winners and losers cancel each other out, leaving investors exposed to single-stock concentration they believe they have diversified away through passive allocations.

When big ASX news breaks, our subscribers know first

What makes a business genuinely resistant to AI disruption

Genuine resilience to AI disruption does not come from owning superior technology. It comes from occupying a structural position inside a network that a new AI-powered entrant cannot simply rebuild from scratch.

The alternative framework targets two overlapping categories. First, AI-resistant businesses with structural moats, especially network effects, that are hard for any new AI product to displace. Second, AI-leveraged businesses with large existing audiences or cost bases where AI functions primarily as a cost-reduction and efficiency tool, not a competitive battlefield. The strongest investments sit at the intersection of both.

Economic moat investing formalises this intuition into five distinct sources of competitive advantage: intangible assets, switching costs, network effects, cost advantage, and efficient scale, with multiple reinforcing sources considered far more durable than any single structural driver.

A dual-sided network effect, in plain terms, works like this: buyers join a marketplace because sellers and inventory are already there. Sellers join because buyers and demand are already there. As the network grows, its value becomes self-reinforcing. Each new participant makes the platform more useful for everyone else.

Contrast that with a single-user tool. A better AI-powered note-taking app can win users one by one, because each person makes a standalone decision. Displacing a marketplace, on the other hand, requires simultaneous migration of entire communities of buyers and sellers. That is a fundamentally different and far harder problem.

Why AI mostly strengthens marketplace moats rather than eroding them

An AI-superior entrant still faces what is known as the cold-start problem: it cannot offer its tools to buyers and sellers who are not yet on its platform. The incumbent’s advantage is not software quality. It is network density plus trust plus transaction data plus logistics integration, and an entrant needs all of those simultaneously to compete.

For network-effect businesses, AI improves operations on top of an already-dense network, widening the moat rather than eroding it. Specific applications include:

- Auto-generated listings, categorisation, and pricing guidance for merchant onboarding

- Fraud detection and risk scoring powered by years of proprietary transaction data

- Logistics routing, demand forecasting, and inventory optimisation

- Recommendation quality and ad targeting that improve with scale

The incumbent’s data advantage feeds the AI improvement loop. An entrant cannot replicate that loop without first having the network, and building the network is precisely the part AI cannot shortcut. Understanding this tells you which types of businesses are worth targeting when building an AI-aware portfolio: those where the moat is structural density, not software superiority.

MercadoLibre as a case study in AI-resilient compounding

MercadoLibre is the largest e-commerce and fintech ecosystem in Latin America, operating across approximately 18 countries and serving a region of roughly 670 million people. That ecosystem, built over more than two decades, is the practical illustration of everything the framework describes in theory.

The business runs six interlocking pillars, each reinforcing the others:

| Pillar | Function | AI Application |

|---|---|---|

| Marketplace (Mercado Libre) | Core e-commerce platform connecting buyers and sellers | Search relevance, recommendation quality |

| Logistics (Mercado Envíos) | Proprietary delivery and fulfilment network | Routing optimisation, demand forecasting |

| Payments (Mercado Pago) | On-platform and off-platform transactions and wallets | Fraud detection, transaction risk scoring |

| Credit (Mercado Crédito) | Lending to merchants and consumers | Credit underwriting using proprietary data |

| Merchant tools (Mercado Shops) | Storefront and selling infrastructure | Automated listing creation, onboarding acceleration |

| Advertising (Mercado Ads) | Promoted listings and targeted marketing | Ad targeting precision, conversion optimisation |

Each pillar reinforces the others: logistics quality keeps buyers on the platform, payments enable frictionless checkout, credit gives merchants working capital to grow inventory, and advertising lets them reach intent-rich buyers. Disrupting one pillar is hard. Disrupting all six simultaneously is a problem no AI startup can shortcut.

The platform’s strength means MercadoLibre is not competing in any AI race. Instead, it can draw on whichever AI tools are best at any given moment to sharpen recommendation quality, tighten fraud detection, refine credit underwriting, accelerate merchant onboarding, and optimise logistics, all running on top of proprietary transaction data that no outside entrant can replicate. In this context, AI serves as fuel for an engine that already exists, rather than a threat to its foundations.

The margin expansion story is the investment punchline. Current margins are below what comparable mature marketplace businesses achieve, because the company has been investing heavily in logistics infrastructure, geographic expansion, and fintech capabilities. As fintech and advertising, both higher-margin segments, scale relative to the core marketplace, operating leverage should drive earnings to compound faster than sales. Many mature marketplace and platform businesses ultimately reach 30-40% operating margins or higher. MercadoLibre is below that range today, with a visible path to converge.

When a business is expanding at roughly 20% annually, trades at around 16 times earnings, and has management that believes that pace is sustainable across multiple years, it presents the kind of risk-reward profile this framework is designed to surface. Even in a scenario where growth slows to approximately 10% per year, an entry at 16 times earnings still offers an attractive return proposition.

That combination of moat quality, multiple growth levers, margin expansion potential, and reasonable valuation entry is precisely what the structural framework prioritises over high-multiple frontier AI bets.

Netflix and the scale advantage in AI-driven content economics

Netflix is not a technology company in the way frontier AI labs are. Its most valuable asset is a direct billing and distribution relationship with hundreds of millions of paying subscribers across the globe. That subscriber relationship provides global distribution at scale, a data-rich recommendation engine, and a pricing and billing platform operating across many countries. If AI makes content cheaper to produce, Netflix is positioned to monetise those cheaper inputs through an already-installed global distribution base.

AI tools are already lowering costs and enabling formats that were previously uneconomical. Specific applications include:

- Scriptwriting assistance and story development acceleration

- Localisation across dozens of languages at lower per-title cost

- Visual effects and post-production workflow compression

- New format experimentation, including interactive shows, game-like experiences, and personalised content variants

These tools are broadly available. Any studio or streaming platform can access them. Which is exactly why the question is not who has the best AI tools, but who benefits most from using them.

Why scale asymmetry matters more than AI access

Access to AI tools is not the differentiator, because most of these tools are available to everyone. The differentiator is the base over which cost savings are applied.

A given percentage cost reduction on a multi-billion dollar content budget yields far more absolute dollars than the same reduction on a smaller competitor’s budget. A 10% cost saving means dramatically more to a platform spending several billion dollars per year on content than to one spending hundreds of millions. That absolute dollar advantage can be reinvested in flagship content that reinforces the distribution moat, improving subscriber retention and acquisition while maintaining or improving margins.

This is the opposite of the naive reading that cheaper content production helps challengers more than incumbents. Scale asymmetry means AI is likely to entrench the advantages of already-large content platforms rather than democratise the field. Netflix does not need to be a frontier AI lab. It needs to remain an efficient, scaled distribution platform that plugs in best-available AI tools wherever they improve content economics, and the subscriber relationship ensures those improvements compound at a scale competitors cannot match.

The next major ASX story will hit our subscribers first

Five questions for evaluating any company’s AI exposure

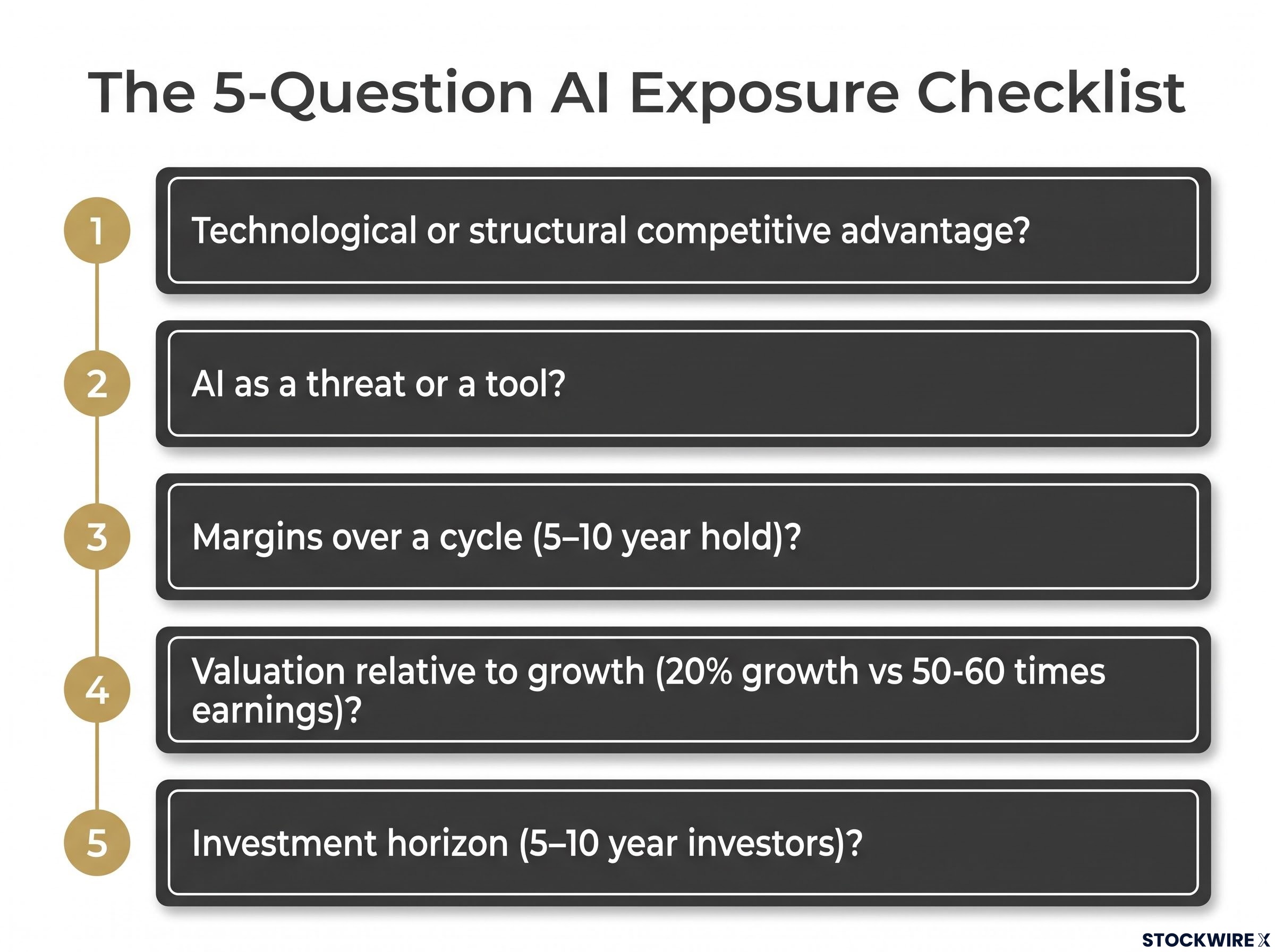

The framework so far gives you the logic. These five questions give you the tool. You can apply them to any business you already hold or are considering, and the sequence moves from moat quality through to your own investment horizon.

- Is the competitive advantage technological or structural? If a company’s moat is “we have the best model,” that advantage is vulnerable every time a new architecture or compression technique arrives. If the moat is network effects, switching costs, regulatory positioning, or distribution scale, it is more resistant to technological shifts. A good answer here is one where the moat exists independently of any specific technology generation.

- Is AI a threat or a tool for this business? A threat means the company competes directly in AI models, infrastructure, or tooling, and its position depends on staying ahead technically. A tool means the company uses AI to reduce costs, improve user experience, or enhance risk management, regardless of which lab wins the underlying technology race. You want the businesses where AI is a tool, not the arena.

- What do margins look like over a cycle? Are current margins cyclically elevated, for example due to supply shortages or hype-driven demand, or structurally improving through operating leverage and mix shift into higher-margin segments? Cyclically elevated margins mean-revert. Structurally improving margins compound. The distinction matters enormously over a 5-10 year hold.

Enterprise AI adoption data reinforces the framework’s margin argument: only an estimated 12-20% of enterprises achieve meaningful operational AI embedding, meaning most of the cost savings and productivity gains used to justify elevated AI valuations have not yet materialised in aggregate corporate earnings.

- What is the valuation entry point relative to growth? A business growing at approximately 20% at a moderate earnings multiple offers a far better margin of safety than a similar grower at 50-60 times earnings. Entry price is not an afterthought. In a high-uncertainty technological regime, it is active risk management.

- What is your investment horizon, and does the thesis require short-term outperformance to work? This is often the most underestimated question. More speculative AI names may outperform this approach in any given quarter or even year. If that will cause you to abandon the framework, the framework is not for you.

The horizon question is the foundation. This entire framework is built for 5-10 year investors comfortable with periods where speculative AI names outperform temporarily. The thesis is about durable compounding, not quarterly performance. If your timeframe is shorter, the risk-reward calculus changes fundamentally.

Having these five questions stops you from making a binary AI/not-AI portfolio decision. Instead, you have a repeatable analytical process for sizing any position in any company with meaningful AI exposure.

Where AI disruption actually takes you as a long-term investor

The framework translates into four specific portfolio construction principles you can apply now:

- Prefer businesses with multiple independent growth levers over single-driver AI bets. MercadoLibre’s combination of marketplace, logistics, payments, credit, and advertising, each reinforcing the others, is the structural template. A business with one growth driver needs that driver to keep working. A business with six can absorb setbacks in any one.

- Favour structural margin expansion over cyclically elevated margins. Margins driven by ecosystem scale and higher-margin segment mix are durable. Margins driven by temporary supply constraints and hype-fuelled demand are not. The memory chip analogy applies broadly across AI-adjacent sectors.

- Use valuation as active risk management, not an afterthought. Entry price matters more, not less, in a period of elevated technological uncertainty. A business with strong structural characteristics trading at a moderate multiple gives you room for error. The same business at 50-60 times earnings requires near-perfect execution and sustained multiple expansion, the double bet that history shows is fragile.

- Maintain a genuinely long-term horizon to allow compounding in resilient, AI-leveraged businesses that may be less exciting in the short run. The framework’s value does not appear in any single quarter. It appears over 5-10 years as structurally advantaged businesses compound while cyclically elevated competitors mean-revert.

Speculative AI names may well outpace this approach over any given stretch of time, and that possibility is worth acknowledging plainly. The goal here is not to claim an edge in the next quarter. It is to identify where the conditions for durable, long-run compounding are most reliably present.

As AI becomes more pervasive and more businesses use it as a commodity tool, the structural moat question, network effects, switching costs, subscriber relationships, distribution scale, becomes more important as a differentiator, not less. You are not avoiding AI exposure by applying this framework. You are choosing where in the AI value chain your capital is positioned, and that positioning decision matters more than whether your portfolio holds stocks labelled “AI” or not.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—