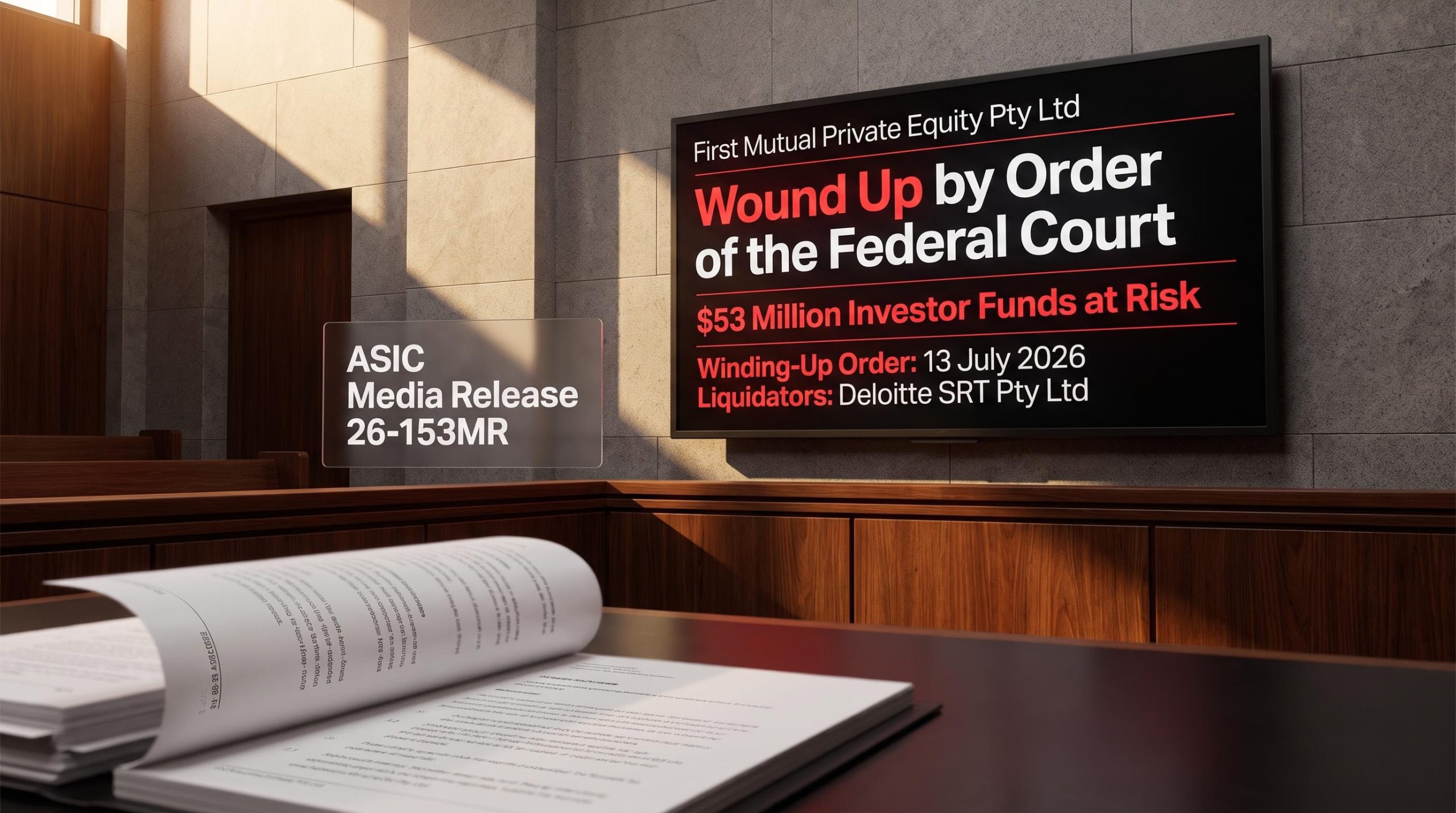

Following a court application by ASIC, First Mutual Private Equity Pty Ltd and its unregistered managed investment scheme have been wound up by the Federal Court of Australia, with liquidators from Deloitte now overseeing a structure that held approximately $53 million in investor funds. The winding-up order was issued on 13 July 2026 and represents the final step in an enforcement sequence stretching back nearly a year.

For anyone who invested with First Mutual or through the scheme operated by Gregory Raymond Cotton, the court order converts an ongoing investigation into an active insolvency process with named contacts, formal claim deadlines, and a statutory priority queue that will determine who gets paid and in what order.

Here is what the court order means for your money, who is now in charge of the process, and what you need to do before the liquidation advances.

A $53 million scheme reaches its legal endpoint

The Federal Court’s winding-up order on 13 July 2026 shut down First Mutual Private Equity Pty Ltd and the unregistered managed investment scheme operated by the company and Gregory Raymond Cotton. The regulator brought its application to the Federal Court with the aim of safeguarding both existing and prospective investors and ensuring that any remaining assets would be administered in an orderly, supervised manner.

ASIC media release 26-153MR confirms the Federal Court’s 13 July 2026 order and names Robert Woods and Salvatore Algeri of Deloitte SRT Pty Ltd as the appointed liquidators, providing the official regulatory record of the winding-up.

Funds at risk: ASIC identified approximately $53 million in investor funds as potentially misused or at risk during the freezing order proceedings in August 2025. That figure represents funds ASIC suspected were not used for their intended investment purpose, not a confirmed total loss.

The distinction matters. The $53 million is an early regulatory estimate of exposure, not a final accounting of what has been lost or what may be recovered.

- First Mutual Private Equity Pty Ltd: the corporate entity wound up by court order

- Gregory Raymond Cotton: the individual who operated the scheme alongside the company, both subject to the winding-up order

- ASIC: the regulator that brought the application to the Federal Court (media release 26-153MR)

When big ASX news breaks, our subscribers know first

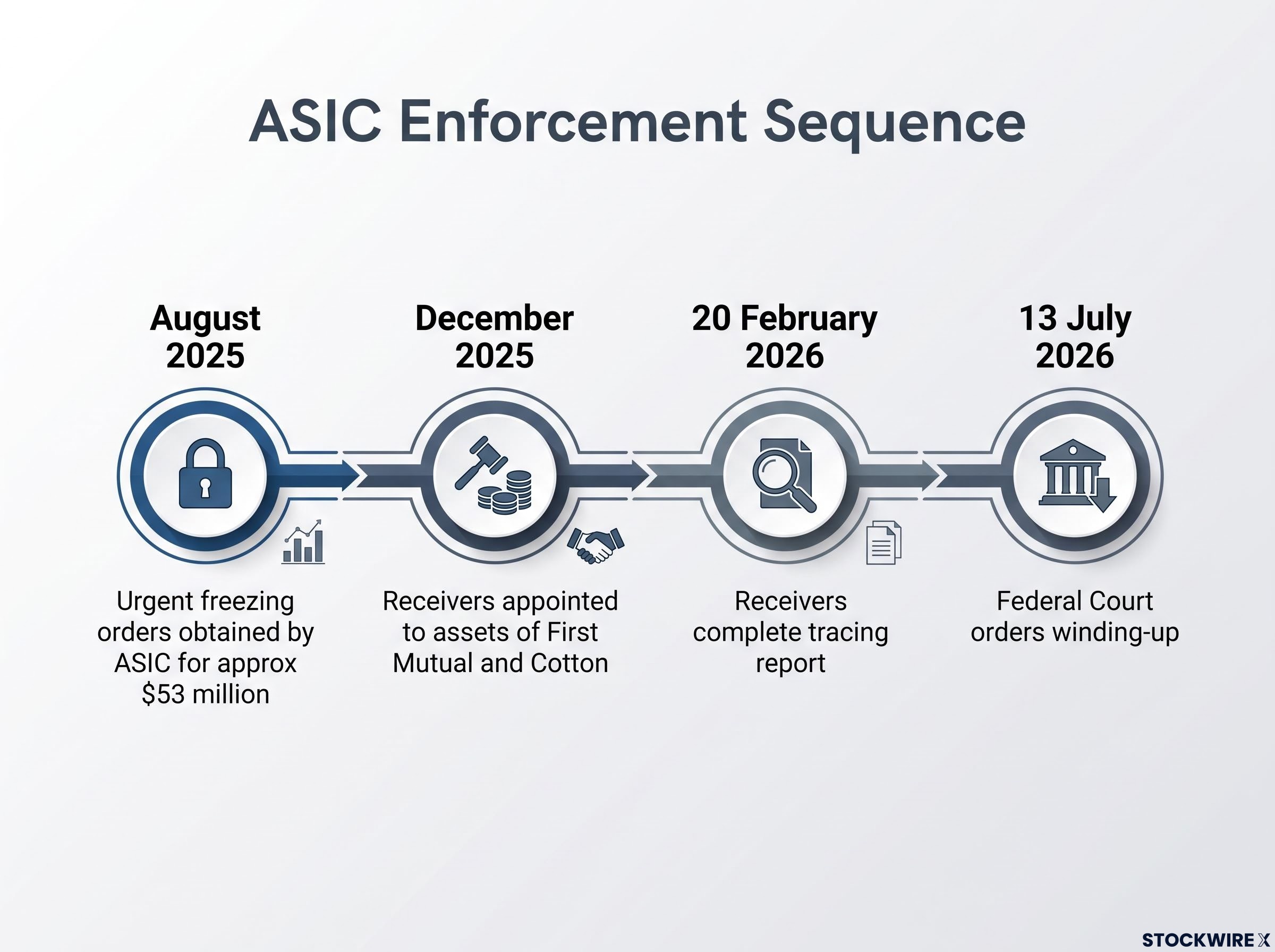

How ASIC built its case: from freezing orders to full dissolution

Each stage of ASIC’s intervention made the next one harder to avoid. The 13 July 2026 winding-up order was not a sudden move; it was the final step in a sequence where each phase produced findings that justified escalation.

- August 2025: ASIC obtained urgent freezing orders from the Federal Court, locking bank accounts, barring new liabilities, and blocking fund transfers while the regulator investigated the suspected misuse of approximately $53 million in investor funds.

- December 2025: Receivers were appointed to the assets of both Cotton and First Mutual, with a specific mandate to determine how much money was received from investors and trace where those funds went.

- 20 February 2026: The receivers completed their report, documenting the outcomes of the tracing exercise. The report is accessible to investors via Federal Court processes.

- 13 July 2026: The Federal Court ordered the company and scheme wound up and appointed liquidators to manage formal dissolution.

What the receivers found

The Receivers’ Report dated 20 February 2026 provides the most detailed available account of how investor funds moved through the scheme. Investors can access it through Federal Court processes, subject to any applicable conditions. Its findings formed part of the evidentiary basis on which the court ultimately ordered the winding-up.

The four-stage escalation tells you that ASIC’s concerns deepened at each phase. The regulator moved from freezing assets to appointing investigators to seeking full dissolution, a progression that reflects a considered assessment that the scheme could not be permitted to continue operating in any form.

What Deloitte’s liquidators are now responsible for

With effect from 13 July 2026, Robert Woods and Salvatore Algeri of Deloitte SRT Pty Ltd were installed as liquidators by the court, bringing the previous receiver arrangement to a close. The transition marks a shift from investigation into formal dissolution and asset administration.

| Liquidator | Firm | Contact |

|---|---|---|

| Robert Woods | Deloitte SRT Pty Ltd | fmpe@deloitte.com.au |

| Salvatore Algeri | Deloitte SRT Pty Ltd | fmpe@deloitte.com.au |

Their mandate covers four core responsibilities:

- Assuming operational control of First Mutual and the scheme

- Identifying and recovering assets that can be realised for the benefit of the liquidation estate

- Assessing creditor and investor claims to establish what each claimant is entitled to receive

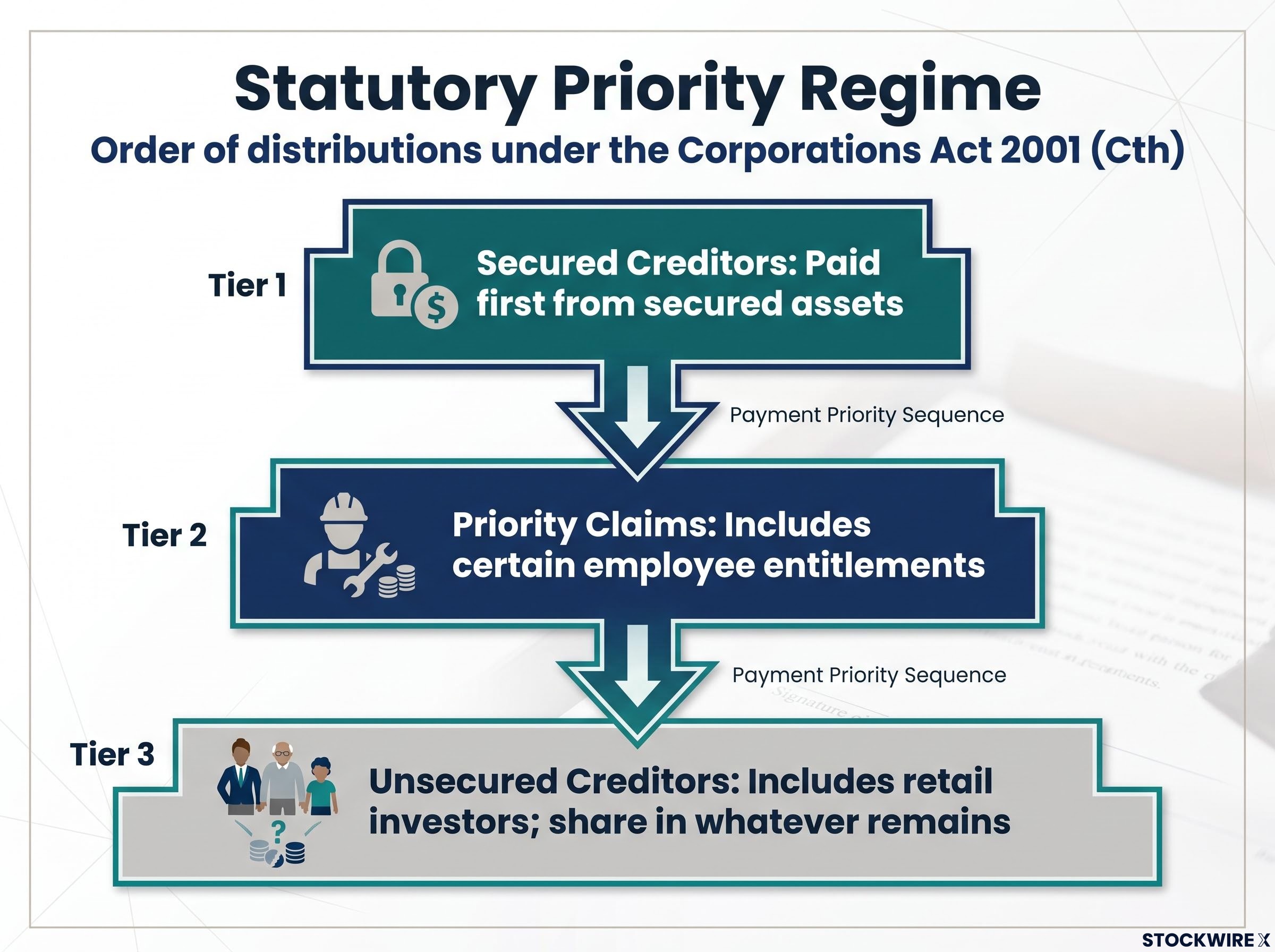

- Distributing available funds to creditors and investors in accordance with the statutory priority regime under the Corporations Act 2001 (Cth)

ASIC has stated clearly that recovery is not guaranteed. What investors ultimately receive depends on how much the liquidators can recover and how those funds must be shared among all claimants.

The appointment of Deloitte practitioners signals a structured, professional process. But the two things to take away from this section are the contact email (fmpe@deloitte.com.au) and the caveat: there is a process, and it may not result in full repayment.

Why unregistered schemes carry risks that registered ones do not

Under the Corporations Act 2001 (Cth), managed investment schemes must generally be registered with ASIC once they reach certain size thresholds or involve retail investors. Registration is the mechanism that brings a scheme under regulatory supervision.

When a scheme operates without registration, three protections that registered schemes provide are absent:

- Regulatory oversight: ASIC has routine supervisory powers over registered schemes, including the ability to intervene before investor harm escalates

- Transparency requirements: registered schemes must meet ongoing disclosure obligations, giving investors visibility into how their funds are being managed

- Formal investor protections: in the event of a scheme failure, registered structures provide clearer legal frameworks for investor claims and recovery

ASIC treats operating without registration as a serious compliance breach, not a technical oversight. In the case of First Mutual, the absence of registration is precisely why ASIC needed to seek court intervention rather than invoke routine supervisory powers.

How to check if a scheme is registered

ASIC’s Financial Services Register is the verification tool. Before committing funds to any managed investment scheme, you can search the register to confirm whether the scheme and its operator hold the required registration and licensing. If a scheme offering above a de minimis threshold is not on the register, that should function as an immediate red flag that stops your due diligence, not a minor compliance question to resolve later.

Managed fund due diligence frameworks that include AFS licence verification on ASIC Connect and a review of the manager’s enforcement history would have flagged the absence of registration before any capital was committed, a step the First Guardian and Shield Master Fund collapses from 2024-2025 made equally concrete.

What affected investors should do before the liquidation process advances

If you invested with First Mutual or through its associated scheme, four steps are available to you now, listed in order of priority.

- Contact the liquidators and lodge a formal claim. Reach out to Robert Woods and Salvatore Algeri at Deloitte SRT Pty Ltd and submit a proof of debt or creditor claim. Without a formal claim lodged, your entitlement cannot be considered in any distribution of recovered funds.

Liquidator contact: fmpe@deloitte.com.au

- Understand the statutory priority regime. Under the Corporations Act 2001 (Cth), distributions in a winding-up follow a set order:

- Secured creditors are generally paid first from secured assets

- Priority claims (such as certain employee entitlements) follow

- Unsecured creditors, which is likely to include many retail investors, share in whatever remains

Many investors will sit behind other claimants in this queue. Lodging a formal claim promptly is the minimum step required to remain in it at all.

- Monitor ASIC’s enforcement page for First Mutual for regulatory updates, and review the Receivers’ Report (dated 20 February 2026) via Federal Court processes to understand how funds were traced.

- Seek independent legal or financial advice from a practitioner experienced in insolvency and financial services. They can clarify your legal status, help you lodge claims correctly, and assess whether further options such as private claims or group proceedings may be available.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The next major ASX story will hit our subscribers first

ASIC’s investigation is active and further enforcement remains possible

The winding-up order deals with the company’s existence and the administration of remaining assets. It does not conclude ASIC’s broader investigation.

As at 13 July 2026, ASIC’s investigation into the conduct and affairs of First Mutual and Gregory Cotton continues to be active. The investigative track is separate from the civil remedy already obtained, and it may lead to:

- Civil penalty actions against individuals or entities involved

- Bans from providing financial services or managing companies

- Referrals for criminal prosecution, depending on the evidence gathered

Any enforcement outcomes from this track are separate from the liquidation process and do not automatically result in investor compensation. However, they may support future recovery or compensation mechanisms, and findings from the investigation could inform potential legal claims by affected investors.

The Capital Guard enforcement action, resolved just two weeks before the First Mutual winding-up order, illustrates a parallel dynamic: a legitimately licensed entity used to direct retail investor funds into a product that never existed, with AFCA complaint rights expiring on a hard deadline.

ASIC’s dedicated enforcement activities page for First Mutual Private Equity Pty Ltd is the primary source for ongoing updates. The relevant media releases are 26-153MR (winding-up order) and 25-174MR (initial proceedings).

| Case Detail | Information |

|---|---|

| Entity | First Mutual Private Equity Pty Ltd |

| Key individual | Gregory Raymond Cotton |

| Winding-up date | 13 July 2026 |

| Liquidators | Robert Woods and Salvatore Algeri, Deloitte SRT Pty Ltd |

| Funds at risk (ASIC estimate) | Approximately $53 million |

| Investigation status | Ongoing as of 13 July 2026 |

The story is not over for affected investors. Further enforcement actions could produce findings that inform future compensation mechanisms or legal claims, even where they do not translate automatically into money returned.

What this case signals for private investment schemes in Australia

The First Mutual case gives ASIC a demonstrated template for how it will dismantle an unregistered scheme when serious concerns arise. The four-stage sequence now sits in the public record:

- Stage 1: Freezing orders to lock assets and prevent further harm

- Stage 2: Receiver appointments to trace investor funds

- Stage 3: Receivers’ report to document findings and inform court proceedings

- Stage 4: Winding-up orders and liquidator appointments to formally dissolve the scheme

The $53 million in funds identified as at risk and the involvement of a named individual alongside a corporate entity are features ASIC treated as justifying the full sequence of court remedies. Affected investors now face an uncertain recovery outcome, and the liquidation process may take considerable time to resolve.

Investment scam losses in Australia reached $837.7 million in 2025 even as ASIC removed nearly 12,000 scam websites, a figure that contextualises the $53 million at risk in the First Mutual matter within a broader pattern of investor harm that regulatory intervention consistently struggles to outpace.

For any investor assessing private scheme opportunities, the practical takeaway is specific: verify registration status via ASIC’s Financial Services Register before committing funds. It is the clearest risk-reduction step available, and it is the step that would have flagged First Mutual before the regulatory intervention became necessary.

For readers wanting to understand how the First Mutual intervention fits within ASIC’s wider regulatory program, our dedicated guide to ASIC’s broader enforcement agenda covers the capital markets reform cycle, infrastructure accountability measures, and the enforcement priorities ASIC has formally embedded for 2025-2029.

Past performance does not guarantee future results. These statements are subject to change based on market developments and ongoing regulatory proceedings.