Samsung Q2 2026 Profit Forecast to Hit 86 Trillion Won, Up 18x

30 mins ago

Australia’s most important piece of capital markets infrastructure failed publicly. The CHESS replacement programme collapsed, the governance culture that allowed it was exposed in a formal inquiry, and the operator responsible, ASX, was found to lack “the aspiration to be a steward of critical market infrastructure.”

At the same time, the regulator overseeing that operator has published a roadmap arguing Australia’s markets need to be more globally competitive. ASIC’s 2025-2026 reform agenda is not a single policy document. It is a coordinated sequence of actions spanning regulatory relief for digital-money experiments, a corporate planning overhaul, a public inquiry into ASX’s governance failures, commissioned research on FinTech and RegTech, and a new roundtable series designed to bring public and private sector leaders into the same room.

Those two facts sit in tension. Here is the sequencing logic behind the reform programme, what each pillar commits to, and what it means for firms and investors trying to operate in or into Australian markets right now.

ASIC’s 2025-2026 activity is not a set of parallel announcements. It is a deliberately sequenced programme, and the order of moves carries its own message. The logic unfolds in four stages:

Each stage creates conditions for the next. The CFR Plus Better Regulation Roadmap, linking ASIC, APRA, the RBA, and Treasury, provides the whole-of-government frame that binds the stages together. Commissioner Simone Constant has framed competitive capital markets as central to ASIC’s institutional mandate, not a secondary ambition.

ASIC’s capital markets roundtable identified three priority opportunity areas: – Modern market infrastructure supported by surveillance automation and ongoing collaboration between public and private sector participants – Regular cross-border regulator coordination to maintain pace with global developments – Well-defined, open channels through which firms can develop and bring new products to market, supported by engaged and constructive regulators

The sequencing tells firms and investors something specific: these reform commitments are structurally embedded in ASIC’s corporate plan and cross-regulator architecture, not a one-cycle priority that could be quietly shelved. That changes how you should weight the regulatory direction of travel in your own planning.

The most damaging finding in the April 2026 inquiry report was not a technology failure. It was a governance one. The panel found that ASX’s resilience had been “compromised in favour of shareholder returns” and that the exchange “lacks the aspiration to be a steward of critical market infrastructure.” Those are not observations about a delayed software project. They describe a strategic and cultural failure at the operator of Australia’s clearing and settlement system.

ASIC treated the findings as a competitiveness problem, not merely a compliance matter. The inquiry established that infrastructure quality is a variable in whether institutional and international capital wants to operate in Australian markets at all.

The CHESS settlement proceedings, resolved in June 2026 with ASX paying $20.5 million in penalties plus $3 million in ASIC legal costs, closed the civil litigation chapter while leaving the governance and technology reset obligations firmly open.

ASIC, in collaboration with the RBA, has required ASX to implement a comprehensive Commitments Plan with specific deadlines and accountability structures.

| Requirement | Responsible party | Deadline |

|---|---|---|

| Board independence for clearing and settlement facilities | ASX Board | Ongoing (mandated) |

| Strategic reset of Accelerate technology programme (including CHESS replacement), agreed with ASIC and RBA | ASX, ASIC, RBA | 30 June 2026 |

| Leadership capability and risk management uplift | ASX executive and board | Ongoing (mandated) |

| Additional $150 million capital charge in net tangible assets | ASX | 2027 |

The $150 million capital charge and the mandated governance reset are not remediation for past failures alone. They set a new baseline expectation for what systemically important market operators must demonstrate to retain their operating position. If you are a large intermediary or a listed entity, the standard ASIC now applies to ASX is the standard it will increasingly apply to you.

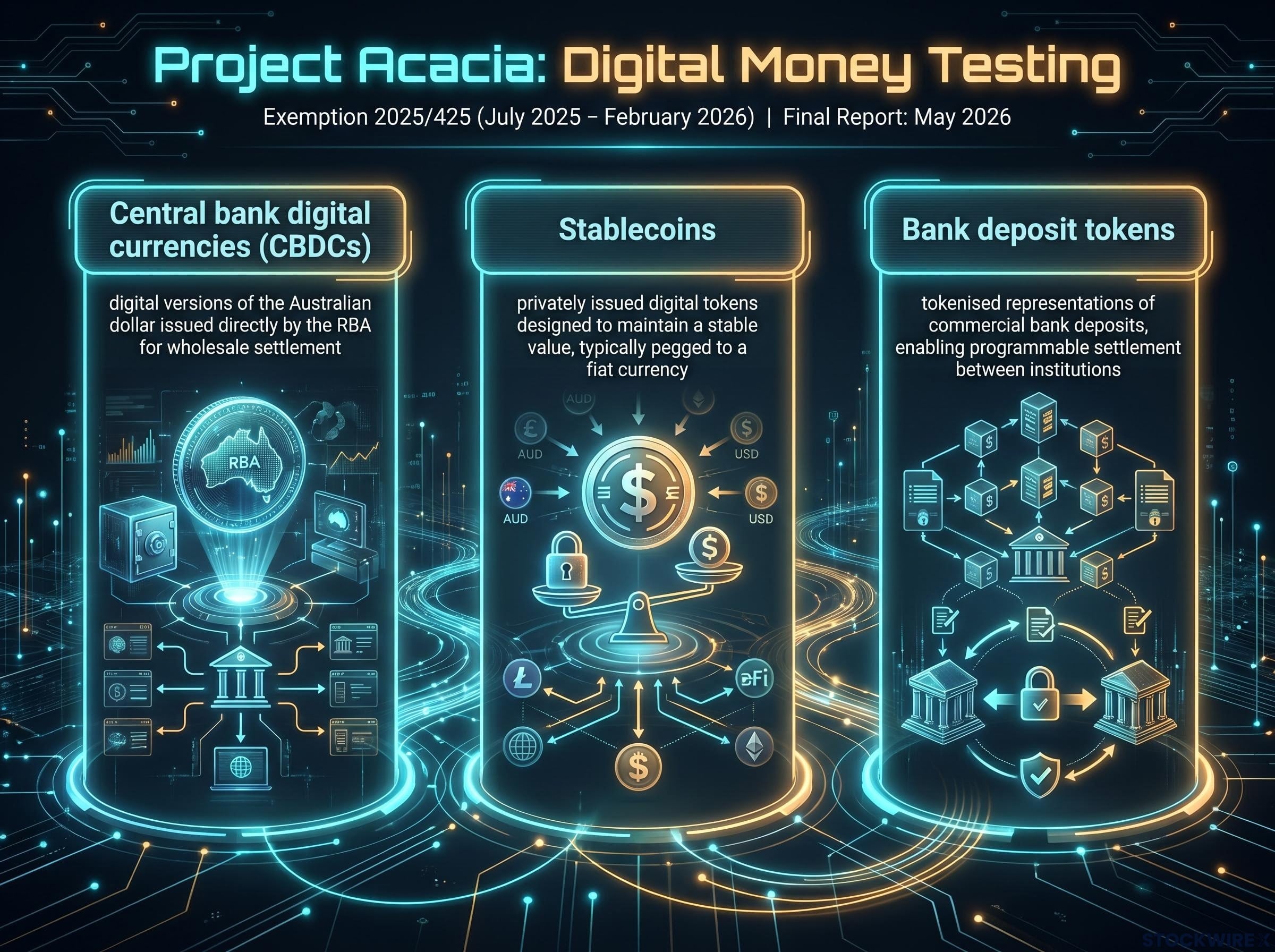

Australia is genuinely experimenting. Project Acacia, led by the RBA and the Digital Finance Cooperative Research Centre (DFCRC) with ASIC providing regulatory relief, is the country’s most substantive test of digital money in wholesale tokenised asset markets. The regulatory relief instrument (Project Acacia Participation Exemption 2025/425) allowed participants to test tokenised asset transactions under eased licensing conditions from July 2025 through February 2026.

Three forms of digital money were tested:

The RBA’s final report, published May 2026, delivered a constructive but conservative conclusion.

Tokenised private money (stablecoins and bank deposit tokens) can co-exist with tokenised forms of central bank money in wholesale markets, and existing access arrangements to central bank money remain broadly appropriate.

That finding tells you where Australia is choosing to position itself. Singapore, Switzerland, and the EU have been operating tokenised-asset sandboxes and pilot regimes that move faster. Australia’s approach is competitive for institutional and wholesale-focused participants who value well-governed experimentation. It is less attractive to market actors seeking rapid retail-facing digital-asset liberalisation.

This is a deliberate positioning choice, not a lag. If you are designing an Australian digital-finance strategy, plan for a well-governed, incrementalist regulatory trajectory.

Australia’s approach to financial market innovation, as mapped in ASIC REP 835, extends well beyond Project Acacia: atomic settlement eliminating the T+1 and T+2 settlement window entirely, AI-related concentration risks invisible to individual firm frameworks, and a co-evolution model that treats investor protection and innovation as complementary rather than competing objectives.

The phrase “simpler and better regulation” invites scepticism. It sounds like a commitment to reduce paperwork. The structural picture is more substantive than that.

The Better Regulation Roadmap is a whole-of-government architecture involving ASIC, APRA, the RBA, and Treasury under the Council of Financial Regulators Plus (CFR Plus). It commits regulators to three specific outcomes:

ASIC’s 2025-29 corporate plan formalises these commitments alongside traditional priorities around market disclosure and professional conduct. The plan treats simpler, more navigable regulation and stronger digital and data resilience as co-equal institutional priorities.

ASIC’s corporate plan formalises competitive capital markets as a co-equal institutional priority alongside traditional mandates covering market disclosure and professional conduct, embedding the simplification and digital capability commitments into the agency’s formal four-year operating framework.

The practical examples matter more than the strategic language. The federal government’s whole-of-government reform agenda includes streamlining superannuation-related ASIC instruments and simplifying reporting relief for group entities, both without reducing investor protections. Cross-regulator data sharing is the feature most likely to reduce compliance friction for large, complex firms, because fragmented reporting obligations across ASIC, APRA, and the RBA are a direct cost that competitors in better-coordinated jurisdictions do not bear.

For cross-border and complex firms, the combination of reduced duplicative reporting and improved regulator data-sharing translates into lower compliance overhead and more predictable supervision. Whether these commitments materialise as specific instrument changes or remain strategic intentions is the distinction that matters for your compliance budgeting and product structuring decisions.

For readers wanting to assess how much of the simplification agenda has already moved from strategy to measured delivery, our full explainer on ASIC’s simplification progress covers the REP 830 findings in detail, including the 380% expansion in electronic lodgement options and the cross-regulator insurance and superannuation data deduplication work targeting completion by November 2026.

ASIC’s 2026 enforcement priorities are part of the same competitiveness architecture, not a counterweight to it. The three focus areas are specific:

The logic is straightforward. Markets that are transparent, well-reported, and free of manipulative conduct are more attractive to institutional and international capital. Markets perceived as lax on misconduct repel it.

ASIC’s insider trading enforcement posture is built on a measurable foundation: ASIC Report 787 ranked Australian equity markets among the world’s cleanest across a six-year measurement period, and the regulator has since established a dedicated prosecution team and carried insider trading as a formal priority into both 2025 and 2026 to defend that standing.

Enforcement credibility is a competitive asset, not a drag on innovation. When ASIC targets reporting failures and governance lapses, it is building the market-quality conditions that institutional investors assess before allocating capital to Australian equities.

The dedicated surveillance programme on financial reporting non-lodgement is a direct signal to listed entities and their boards. ASIC is treating disclosure quality as a market structure issue, and the enforcement consequences for non-compliance are rising.

There is a risk on the other side. Enforcement that becomes unpredictable or disproportionate for good-faith innovators would undermine the facilitative positioning ASIC is building through Project Acacia and the roundtable series. That balance is a live tension worth monitoring.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Five concrete watch points will determine whether the reform agenda delivers structural change or cycles through another commitment that stalls on delivery.

| Watch point | Key milestone or indicator | Timing |

|---|---|---|

| ASX Commitments Plan delivery | Accelerate programme reset agreed with ASIC and RBA; $150 million capital charge met | 30 June 2026 (reset); 2027 (capital) |

| Digital-money and tokenisation developments | Post-Acacia initiatives; evolution of wholesale-focused approach | Ongoing from May 2026 final report |

| Better Regulation implementation | Legislative and regulatory changes delivering on simplification commitments | 2026-2027 |

| Cross-regulator data sharing | Reduced fragmented reporting obligations for multi-regulated firms | 2026-2027 |

| Roundtable outcomes | Publication of themes and actionable outcomes from ASIC capital markets roundtable series (REP 835 and ongoing) | 2026 |

The execution risks are real, and they should not be softened:

The honest assessment for firms making medium-term decisions about Australian market participation is this: the structural conditions are being built, but the execution is unproven. Track the ASX milestone deliveries and the roundtable output publications as leading indicators rather than waiting for a definitive competitiveness verdict.

ASIC has sequenced experimentation, planning, infrastructure accountability, and enforcement recalibration in a way that is structurally coherent and cross-regulator embedded. That distinguishes this cycle from previous modernisation attempts that relied on a single agency or a single initiative.

The outcome is bifurcated. If ASX delivers on its Commitments Plan and simplification materialises as specific instruments, Australia’s capital markets will be meaningfully more competitive for institutional investors and cross-border firms by 2027. If execution stalls, the competitiveness problem documented in ASIC’s own roadmap will persist.

The leading signal is not the next policy announcement. It is whether the milestones already committed to, the Accelerate reset, the capital charge, the instrument-level simplification, actually arrive on schedule. Track execution, not intention.

These statements are speculative and subject to change based on market developments and regulatory outcomes. Past performance does not guarantee future results.

ASIC's 2025-2026 capital markets reform agenda is a four-stage programme spanning regulatory relief for digital-money experiments under Project Acacia, a formal capital markets roadmap and corporate plan, an inquiry into ASX's governance failures, and updated enforcement priorities targeting reporting non-lodgement and market integrity.

The April 2026 inquiry panel found that ASX's resilience had been compromised in favour of shareholder returns and that the exchange lacks the aspiration to be a steward of critical market infrastructure, concluding that the failure was a strategic and cultural one, not merely a technology project delay.

Project Acacia is an RBA and DFCRC-led experiment, supported by ASIC regulatory relief, that tested three forms of digital money in wholesale tokenised asset markets: central bank digital currencies, stablecoins, and bank deposit tokens, running from July 2025 through February 2026 with a final report published in May 2026.

ASX paid $20.5 million in penalties plus $3 million in ASIC legal costs in June 2026, closing the civil litigation chapter, while remaining obligations under the Commitments Plan, including a $150 million additional capital charge by 2027 and a mandated governance reset, remain open.

The five concrete watch points are: the ASX Accelerate programme reset agreed with ASIC and the RBA by 30 June 2026; the $150 million ASX capital charge due by 2027; post-Acacia digital-money developments; legislative changes delivering on simplification commitments in 2026-2027; and publication of actionable outcomes from ASIC's capital markets roundtable series.