The instrument most investors think of as passive, the one marketed as a neutral, low-cost way to own the market, is one of the most active forces shaping the prices they pay. Every dollar flowing into an exchange-traded fund triggers a mechanical chain of trades in the underlying stocks. At sufficient scale, that chain is not a footnote. It is a price-setting force.

That scale has arrived. Global ETF assets have grown to a point where flow mechanics are a meaningful input into how individual stocks are priced, not a theoretical concern confined to academic papers. The investor who understands this sees a fundamentally different market from the one who does not.

After reading this, you will be able to look at any ETF holding in your portfolio and ask the right question: how much of this price reflects what the company is actually worth, and how much reflects the mechanical demand created by fund flows? That distinction is not abstract theory. It is a practical lens that changes how you evaluate concentration, timing, and risk.

The engine underneath every ETF trade

Most investors buy an ETF the way they buy a single stock: click, confirm, done. What happens next, though, is mechanically different from anything a single stock purchase triggers. Your order sets off a sequence of trades in every stock the fund holds, executed in precise index weights, without anyone asking whether those stocks are cheap, expensive, or fairly valued.

The key actors in this process are authorised participants (APs), large financial institutions that sit between you and the underlying stocks. They are the ones assembling and disassembling the baskets. Understanding their role is the foundation for everything that follows, because every time you buy an ETF, you are participating in this mechanical chain whether you intend to or not.

The creation and redemption mechanism sits at the heart of ETF structure and costs, and how that wrapper is legally constructed determines both what you actually own and how the tax treatment of your returns is calculated across different account types.

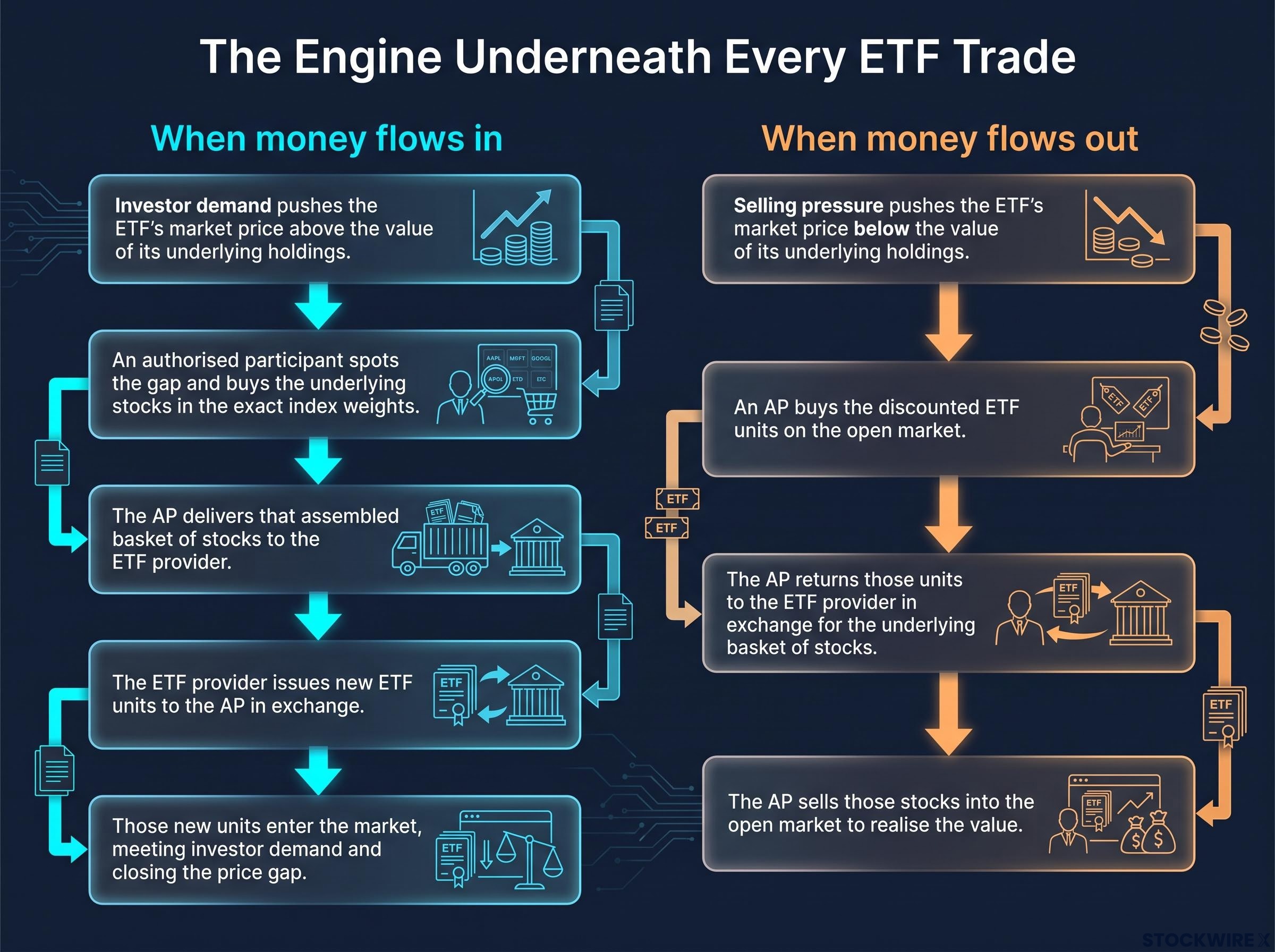

When money flows in

- Investor demand pushes the ETF’s market price above the value of its underlying holdings.

- An authorised participant spots the gap and buys the underlying stocks in the exact index weights on the open market.

- The AP delivers that assembled basket of stocks to the ETF provider.

- The ETF provider issues new ETF units to the AP in exchange.

- Those new units enter the market, meeting investor demand and closing the price gap.

When money flows out

- Selling pressure pushes the ETF’s market price below the value of its underlying holdings.

- An AP buys the discounted ETF units on the open market.

- The AP returns those units to the ETF provider in exchange for the underlying basket of stocks.

- The AP sells those stocks into the open market to realise the value.

The distinction from a traditional managed fund matters here. A fund manager can hold cash, stagger purchases, or simply choose not to buy a stock they consider overvalued. An ETF cannot. When money flows in, the underlying stocks must be bought. When money flows out, they must be sold. Research including the study “ETF Flows and Underlying Stock Returns: The True Cost of NAV-Based Trading” confirms that these flow-related transactions significantly affect stock prices, and the effects have been documented at daily frequency. The mechanism is fast, mechanical, and indifferent to valuation.

When big ASX news breaks, our subscribers know first

How market-cap weighting channels capital toward recent winners

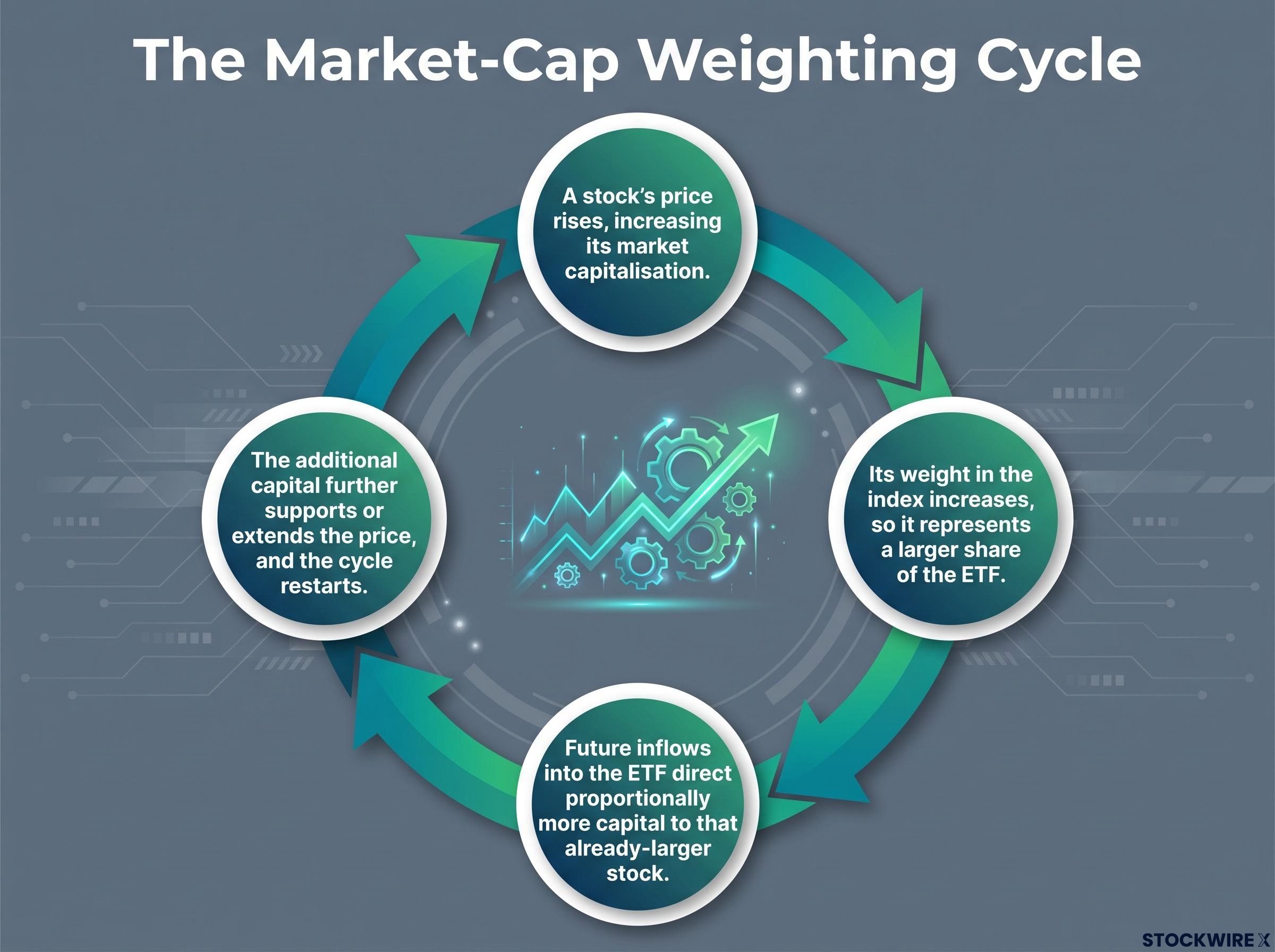

Once you understand the creation/redemption engine, the next question is: where does the money go? In most major index ETFs, the answer is determined by market-capitalisation weighting, meaning the largest companies by market value receive the largest share of every dollar invested. That sounds neutral. It is not.

The weighting creates a self-reinforcing cycle that operates in four steps:

- A stock’s price rises, increasing its market capitalisation.

- Its weight in the index increases, so it represents a larger share of the ETF.

- Future inflows into the ETF direct proportionally more capital to that already-larger stock.

- The additional capital further supports or extends the price, and the cycle restarts.

This is the mechanism behind concentration patterns you can see in real time. US-listed ETFs tracking major indices have channelled disproportionate capital into a narrow group of technology stocks, including the so-called Magnificent Seven, not because index funds made an active decision to overweight them, but because market-cap weighting mechanically routes more money toward whatever has already gone up.

Index fund concentration in US markets reached historically extreme levels by mid-2026, with five mega-cap stocks controlling roughly 23% of the broad market, a direct product of the cap-weighting feedback loop that channels every new dollar of passive inflow toward whatever has already appreciated the most.

Research under the label “Lost in the Rising Tide” argues that non-fundamental ETF demand can push prices away from fundamental values, particularly for stocks with high ETF ownership.

Academic work, including findings from Ben-David et al., documents the relationship between ETF ownership concentration and price deviation from fundamental value. For you, this means that buying a broad index ETF is not a neutral act. It is an implicit decision to keep adding capital to whatever has already become the most expensive, not the most fundamentally attractive. Your “passive” allocation carries a structural tilt toward recent winners that compounds with every inflow cycle.

What indiscriminate buying actually means for stock prices

The self-reinforcing cycle described above operates at the index level. But within each basket, something equally important happens at the stock level: every constituent gets bought or sold in proportion, regardless of individual quality.

When you purchase a thematic or index ETF, the fund buys every holding proportionally. Because the basket is purchased as a whole, a company with deteriorating fundamentals attracts the same proportional capital as one delivering record earnings. Quality is irrelevant to the flow; what matters is index membership. This indiscriminate demand causes holdings to move in tandem driven not by any shared business characteristics, but purely by their common presence in the same fund.

The documented effects on markets include:

- Increased comovement: stocks within the same index move together because ETF flows create simultaneous trades across all constituents.

- Non-fundamental price pressure: flow-driven ETF trades cause price movements in underlying stocks that are not tied to firm-specific news.

- Volatility amplification: ETFs increase the volatility of underlying stocks through arbitrage and flow-driven trading activity.

- Heightened sensitivity to global shocks: markets with substantial ETF presence show amplified price reactions to shifts in global risk appetite.

This creates a direct challenge to a foundational concept in investing. The efficient market hypothesis (EMH) holds that prices continuously incorporate all relevant information because market participants analyse and trade on fundamentals. That framework assumes demand is generated by reasoned judgement about company value. ETF flows operate on a different basis entirely: capital is deployed mechanically across every constituent, irrespective of what any individual business is doing, which injects a non-informational demand signal into prices that has nothing to do with underlying quality.

| What the EMH assumes | What ETF flows introduce |

|---|---|

| Prices are driven by informed analysis of fundamentals | Prices also reflect mechanical, non-informational basket demand |

| Demand is discretionary and stock-specific | Demand is indiscriminate and applied uniformly across every constituent |

| New information is the primary catalyst for price changes | Fund flows create price changes independent of any new information |

| Volatility reflects uncertainty about fundamental value | Volatility is amplified by arbitrage activity and flow-driven rebalancing |

For you, the practical implication is that the price of any stock you own through a popular ETF reflects two things at once: what the market thinks the company is worth, and how much non-fundamental flow demand that stock is currently receiving. Those two components are not always pointing in the same direction. Research shows that stocks with heavy ETF representation can be bid above their intrinsic value by sustained mechanical buying, while companies with little or no index presence may remain underpriced precisely because that same buying pressure bypasses them.

Where distortions are largest: thematic ETFs and small caps

The mechanisms described so far operate across all ETFs. But their severity is not uniform. In broad, highly liquid indices, the price impact of any single inflow is diluted across hundreds of large, actively traded stocks. In thematic and small-cap ETFs, the same mechanics hit a far more fragile surface.

Three conditions amplify the distortion, and you can use them as a checklist when evaluating any thematic ETF:

- Low liquidity in underlying holdings: when the stocks in the basket are thinly traded, even modest inflows move prices sharply because order size is large relative to normal volume.

- Narrow theme definition: the fund must buy every stock in the defined basket, regardless of how central each holding is to the theme or how stretched its valuation already is.

- Small free float: in small-cap names, limited shares available for trading mean that combined retail and institutional inflows can overwhelm normal supply.

Academic research confirms that ETF flow-induced trades have greater price impact when underlying securities are illiquid. Similar amplifying effects have been documented in emerging markets, volatility futures, and commodities, where ETFs amplify the global financial cycle and price swings.

The most dangerous feature is the asymmetry on the way out. Large institutional investors may direct substantial capital into small companies associated with a popular theme, and retail investors purchasing the ETF are buying broad category exposure rather than conducting analysis of individual holdings. When sentiment turns and flows reverse, those same illiquid stocks face outsized downside as ETFs and other holders sell into shallow markets.

Entering at peak inflow and media enthusiasm embeds substantial flow momentum risk, not just fundamental risk. The reversal, when it comes, does not mirror the ascent.

The thematic ETF behaviour gap quantifies exactly this risk: ARK Innovation reported a time-weighted return of roughly 233% while the typical investor experienced approximately negative 35%, because peak inflows arrived at peak valuations, precisely the entry-timing trap that flow-cycle awareness is designed to avoid.

This means thematic ETFs should not be evaluated as diversified exposure to a sector. They should be treated as high-beta, sentiment-driven instruments where the price of every holding is partly a function of how fashionable the theme currently is among ETF buyers.

Price cycles in ETF-driven markets: understanding the feedback dynamic

The flow mechanics described in previous sections do not operate as isolated events. They generate momentum cycles with their own internal logic, which is why strong performance in ETF-driven segments can feel so persistent on the way up and so violent on the way down.

The cycle follows a three-stage loop:

- Inflow-driven price support: ETF inflows push underlying stock prices higher through the creation mechanism.

- Performance signal amplification: higher prices improve the ETF’s recent performance metrics, attracting further investor attention and generating additional inflows.

- Rebalancing reinforcement: ETFs trade frequently to rebalance exposure after price moves and flows, creating additional demand in the same direction the price has already moved.

Research characterises this momentum dynamic as a feature of market behaviour generally, amplified rather than created by ETF mechanics. The critical finding is that ETF-induced demand can generate temporary, non-fundamental price levels that are vulnerable when flows slow or reverse. ETFs also increase sensitivity to global financial shocks, meaning a momentum cycle built on inflows can reverse sharply when global risk appetite shifts.

Leveraged ETFs and the extreme end of the feedback effect

Leveraged ETFs take the same feedback loop and operate it at higher intensity. These products must buy after price increases and sell after price decreases to maintain their constant leverage target, an effect that research compares to gamma hedging in options markets.

This rebalancing creates a feedback channel where ETF demand amplifies price changes, increasing volatility and introducing risks even for professional arbitrageurs. The mechanism is not categorically different from the standard ETF momentum loop. It is the same engine running at higher revolutions.

For you, this means any strong recent performance track record for a thematic or concentrated ETF should be interrogated. Some portion of that return may reflect where the fund sits in its flow cycle, not what the underlying companies have actually earned. A product showing 30% returns over six months could be partly riding flow momentum that reverses when the next inflow cycle ends.

The next major ASX story will hit our subscribers first

What this means for how you invest, not just how markets work

None of this is an argument against ETFs. Broad, low-cost index ETFs remain a sensible core holding for long-term investors. The research does not argue for avoidance. It argues for understanding.

The core reframe is this: a broad index ETF is not neutral exposure. It systematically overweights recent winners by market cap, which means your allocation is structurally tilted toward what has already appreciated, not toward what is most attractively valued. Index membership and weight are themselves risk factors, because they determine how much non-fundamental flow pressure each holding will experience.

Two adjustments follow directly from this understanding:

- Apply greater entry discipline to thematic and concentrated ETFs. Evaluate where the product sits in its flow cycle before buying. If recent performance has been strong, inflows are high, and media coverage is enthusiastic, a meaningful portion of the current price may reflect flow momentum rather than fundamental value. Valuation scrutiny matters more for these products than for broad indices.

- Recognise the potential value of selective active or factor strategies as a complement. If ETF flows systematically push some stocks away from fundamental values, fundamental analysis becomes more valuable in identifying mispriced names. Combining passive core exposure with selective active positioning can help exploit or hedge against the anomalies that non-fundamental demand creates.

| ETF type | Distortion risk | Investor consideration |

|---|---|---|

| Broad market index ETFs | Moderate: market-cap weighting creates structural tilt toward recent winners | Understand the concentration bias; consider equal-weight or factor alternatives as a complement |

| Sector and factor ETFs | Medium: narrower baskets increase per-stock flow impact | Monitor flow cycles and sector sentiment before adding exposure |

| Thematic and small-cap ETFs | High: illiquidity, narrow themes, and small free floats amplify all flow effects | Treat as high-beta, sentiment-driven instruments; apply strict valuation and timing discipline |

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Passive label, active consequences: investing with the full picture

You now hold three connected insights. The creation/redemption mechanism makes ETF flows a direct, mechanical force on individual stock prices. Market-cap weighting builds a structural tilt toward recent winners that compounds with every inflow cycle. And thematic and leveraged products amplify these effects in direct proportion to their illiquidity and concentration.

ETFs remain efficient, low-cost tools for most long-term investors. The argument is not to avoid them. It is to replace one assumption with a more precise understanding.

The question to carry into your next investment decision is not “is this ETF cheap?” It is: “Where is this ETF in its flow cycle, and what does that mean for the price of what I am actually buying?”

The word “passive” describes your role. It does not describe the market consequences of millions of investors taking that same action simultaneously.

For readers wanting to audit their own holdings, our dedicated guide to ETF portfolio concentration walks through a practical overlap-checking method that typically reveals a unique stock count 30-40% lower than investors initially estimate across a multi-fund portfolio.