How to Know Whether to Hold Cash or Stay Invested

1 min ago

Jensen Huang said $100 billion of compute can be delivered per gigawatt of power. That number has been quoted, misquoted, and conflated with at least two other “$100 billion” figures circulating around Nvidia’s AI infrastructure story in 2026. Before you can evaluate what it means for data centre economics or Nvidia’s competitive position, the first step is understanding what the number actually refers to, and what it does not.

The $100 billion per gigawatt figure is a forward-looking efficiency target. It is not a description of what one gigawatt of AI compute costs or generates today. Getting that distinction wrong leads to materially inflated expectations, and it is easy to see why it happens: multiple “$100B” figures exist simultaneously in Nvidia’s public narrative, each referring to something different.

Here is how to separate the three claims, understand why power efficiency has become a financial metric rather than a technical specification, and know which numbers to track as the GPU upgrade cycle accelerates through the second half of 2026 and beyond.

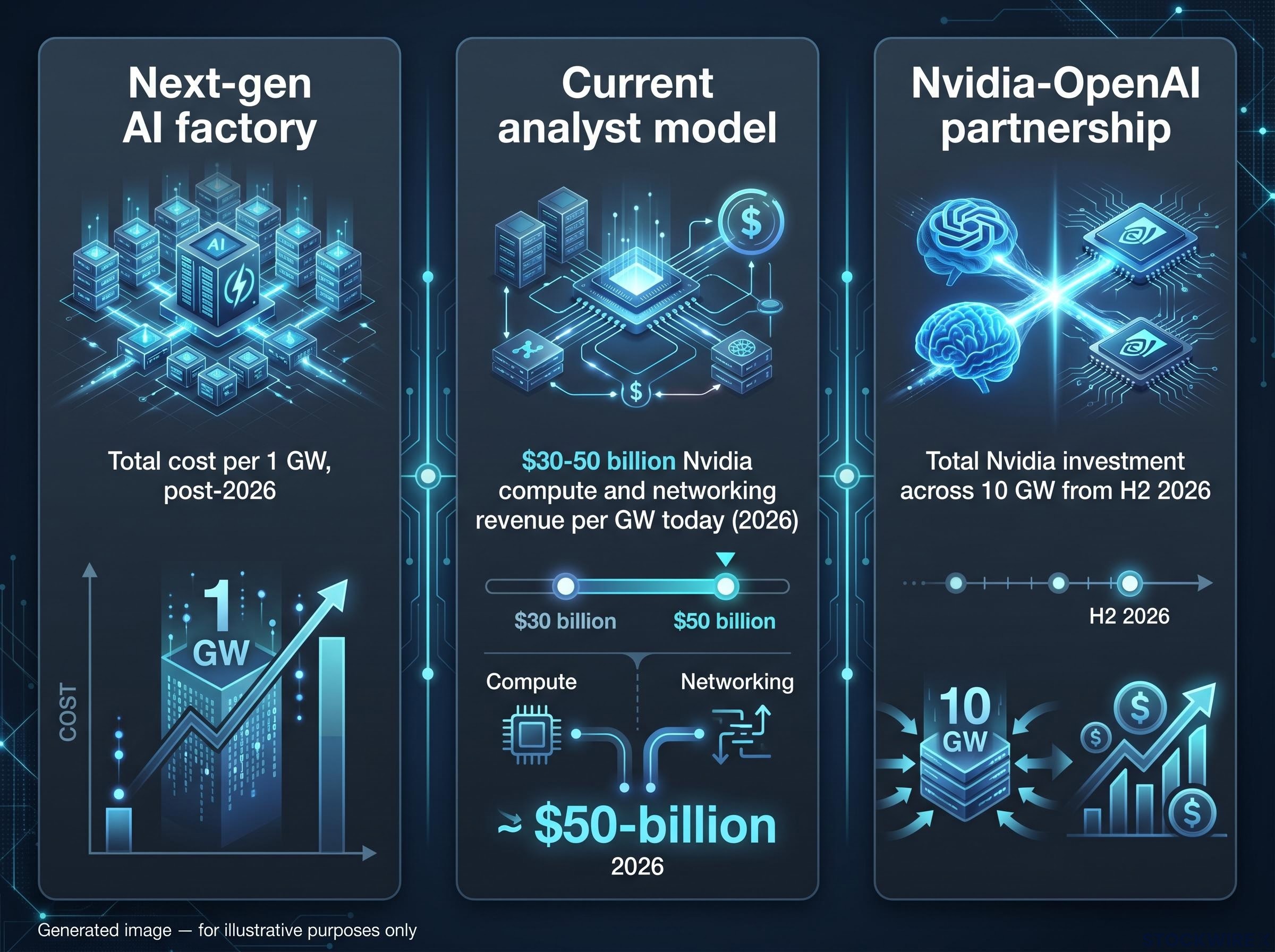

At least three separate “$100 billion” narratives exist in Nvidia’s public communications and analyst coverage right now. They sound similar. They are not. Conflating them produces meaningfully different conclusions about what Nvidia’s AI infrastructure business is actually worth per unit of power.

The first strand is the forward-looking cost of a next-generation 1-GW AI factory. Huang has projected that a future facility at that scale could cost on the order of $100 billion in total, with Nvidia capturing roughly half through its compute and networking stack. Nvidia management has explicitly confirmed this is a forward-looking projection, not a description of current economics.

The second strand is what analysts model today. According to Nvidia management, current deployments produce approximately $30-40 billion in compute revenue for each gigawatt of power, with analyst models that capture broader networking revenue placing the figure closer to $40-50 billion. The precise figure depends on what you include, but the range is consistent: tens of billions, not a hundred.

The third strand is the Nvidia-OpenAI partnership. Nvidia committed up to $100 billion progressively as OpenAI deploys at least 10 GW of Nvidia-based AI data centres, beginning with the Vera Rubin platform in H2 2026. That $100 billion is spread across 10 GW, not per GW.

The Nvidia-OpenAI partnership press release confirms that Nvidia’s $100 billion commitment is structured progressively across at least 10 GW of deployments, with the first gigawatt on the Vera Rubin platform targeted for H2 2026, making the per-GW math in any single-facility comparison materially different from the total figure.

Nvidia management has confirmed that the $100B/GW figure is a forward-looking estimate, tied to expected gains in energy efficiency as new architectures roll out. It does not describe what current infrastructure costs or generates today.

| Narrative | What $100B refers to | GW scale | Timeframe |

|---|---|---|---|

| Next-gen AI factory projection | Total cost per 1 GW, future-state | 1 GW | Forward-looking, post-2026 |

| Current analyst model | Nvidia compute and networking revenue per GW today | 1 GW | Current, 2026 |

| Nvidia-OpenAI partnership | Total Nvidia investment across 10 GW | 10 GW | Deployments from H2 2026 |

Treating the forward projection as today’s benchmark overstates current economics by roughly two to three times. For any valuation or capital expenditure analysis built on that assumption, the distinction is material.

Power, not floor space or headcount, is now the binding constraint in large-scale AI data centres. Huang and the major hyperscalers increasingly describe their AI infrastructure in megawatts and gigawatts because available electricity and cooling capacity have become the rate-limiter for expanding AI compute. When you cannot get more power, the question shifts from “how big is your data centre” to “how much useful work can you extract from each watt.”

AI electricity demand at the grid level explains why power has become the binding constraint in the first place: the IEA projects combined data centre and AI consumption will exceed 1,000 TWh in 2026, more than double 2022 levels, which is why every discussion of AI infrastructure has shifted from floor space to gigawatts.

That is what the compute-revenue-per-GW ratio captures. It measures how much AI workload, and how much monetisable service, can be run on a fixed power envelope. If you are already familiar with capital efficiency ratios in other sectors, this framing is immediately legible:

In AI infrastructure, the scarcest input is power. When a new GPU architecture improves how much useful compute can be extracted from each watt, it directly lifts margins and capital efficiency without requiring more land, more power contracts, or more cooling infrastructure. The same gigawatt simply earns more. That is why this ratio has migrated from engineering documentation into earnings calls and analyst models.

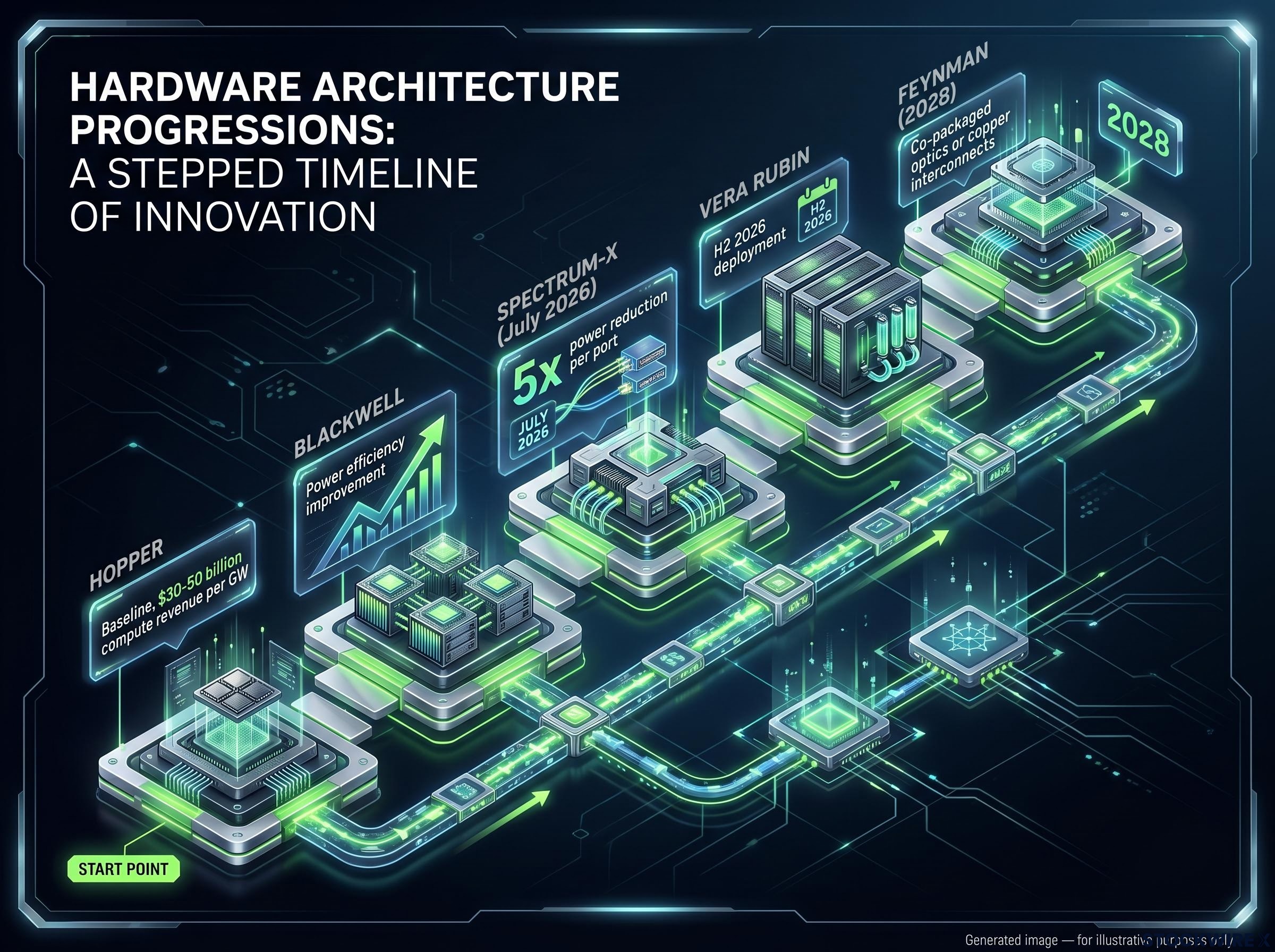

Each successive GPU platform improves the compute-revenue-per-GW ratio, and the progression from Hopper to Blackwell to Vera Rubin illustrates the pattern concretely:

The economic logic connecting these steps is straightforward. If a new platform delivers more training and inference per watt, then a fixed gigawatt of power supports more paying workloads. That lifts revenue per GW even if the physical footprint and power contract stay constant.

The same gigawatt of power, occupied by a newer GPU generation, generates more monetisable compute. That is the financial core of Nvidia’s upgrade cycle argument.

This changes how hyperscaler customers think about hardware refreshes. The financial payoff of upgrading is now expressed in better GW monetisation, not just faster processing speeds. Nvidia’s pricing power is supported because customers pay not only for speed but for better monetisation of their most constrained resource: power. When you read Nvidia’s next GPU platform announcement, the most financially significant claim is not the performance headline but what the new architecture does to the revenue-per-GW ratio at customer facilities.

Chip-level efficiency gains alone are not sufficient to reach the $100 billion per GW forward projection. The rest of the gains come from interconnects, networking, and system architecture, each contributing meaningfully to the ratio. Nvidia has structured its roadmap to optimise across the full stack, not just the GPU itself.

Three layers matter:

Nvidia’s co-packaged optics technical documentation details how integrating optical engines directly onto the switch ASIC reduces power consumption by up to 3.5x per port, the underlying mechanism that supports the efficiency improvements cited in Nvidia’s architecture roadmap and referenced in earnings-call discussions of the revenue-per-GW ratio.

The underlying principle is consistent across all three layers. Every watt that can be shifted from moving bits to doing useful compute improves total economic output per gigawatt. Nvidia’s confirmed product roadmap, fully on schedule as of 12 July 2026, including the Rubin Ultra timeline and NVLink domain architecture disclosed at Computex, reflects this full-stack approach.

From the Feynman platform onwards, due in calendar year 2028, hyperscaler customers will have the option to select between NVLink implementations built on co-packaged optics or copper interconnects. That optionality gives hyperscalers flexibility in how they balance power reduction against cost at very large cluster scales.

Feynman is the furthest confirmed point on Nvidia’s roadmap and serves as evidence that system-level efficiency planning is already embedded in hardware decisions at least two generations forward. If you are assessing how durable Nvidia’s efficiency trajectory is, the fact that 2028 platform decisions are already designed around power optimisation tells you this is a structural priority, not a single-generation improvement.

The conceptual framework is useful only if you can apply it to real-world signals. Here are four specific metrics that operationalise the power-efficiency thesis, each framed as an observable signal with a clear interpretation:

Custom silicon competition from Alphabet, Amazon, and Microsoft is most acute in inference workloads, which are projected to represent approximately 80% of the AI accelerator market by 2030, meaning the competitive compute-per-watt benchmark you track matters most in the segment where hyperscaler in-house chips are already purpose-built to compete.

Watching these four metrics together is more revealing than any single GW announcement or quarterly revenue figure in isolation. When they move in the same direction, rising compute revenue per GW, next-generation architectures named in new power deals, faster refresh cycles, and a widening efficiency lead, that would constitute strong evidence that the $100B/GW projection is tracking as a realistic medium-term outcome rather than a marketing aspiration.

The $100 billion per gigawatt figure is most useful not as a present-day benchmark but as a directional signal. It tells you where Nvidia believes AI data centre economics are heading, and it tells you that the company is making a strategic bet that power efficiency will be the axis on which competition is fought.

The current gap is clear. Today’s dense AI deployments support approximately $30-50 billion of Nvidia compute revenue per GW. The $100 billion target represents roughly a doubling to tripling of economic output from the same power footprint. That gap is where the architectural roadmap does its work: Blackwell, Vera Rubin, and Feynman each move the ratio upward, with Vera Rubin’s initial deployment in H2 2026 serving as the first major step under the current roadmap.

The question to carry forward is not whether Nvidia will hit $100 billion per GW in a specific year. It is whether the compute-revenue-per-GW ratio continues to improve at the pace the architectural roadmap implies. Every future Nvidia announcement related to power, efficiency, or AI factory economics can be read through that single lens: is the ratio moving in the direction the roadmap promises, and at the speed it needs to?

For investors wanting to understand how export control dynamics affect Nvidia’s addressable compute revenue globally, our dedicated guide to Nvidia’s China gray-market pricing covers the mechanics of locked-out demand, why the 2x DGX B300 premium represents upside Nvidia cannot capture, and how policy changes could reprice the China segment faster than any product cycle.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking projections, including Nvidia’s $100B/GW target, are subject to market conditions, technological progress, and competitive dynamics.

It is a forward-looking efficiency target describing how much compute revenue a next-generation 1 GW AI factory could generate, not a measure of what current infrastructure costs or produces today. Current deployments support approximately $30-50 billion in Nvidia compute revenue per gigawatt.

There are three distinct $100B figures: the forward-looking cost projection for a 1 GW next-generation AI factory, the current analyst revenue estimate of $30-50 billion per GW, and the Nvidia-OpenAI partnership commitment of $100 billion spread across at least 10 GW of deployments beginning in H2 2026.

Power has replaced floor space as the binding constraint in large-scale AI infrastructure because available electricity and cooling capacity now limit how fast AI compute can be expanded. The compute-revenue-per-GW ratio measures how much monetisable AI workload can be run on a fixed power envelope, making it a direct indicator of capital efficiency.

Each successive platform delivers better compute per watt, meaning the same fixed power envelope supports more paying AI workloads. Vera Rubin, targeted for initial deployment in H2 2026, is the first major step in Nvidia's roadmap toward the $100B per GW projection.

The four metrics are: compute revenue per GW (currently $30-50 billion, forward target $100 billion), which GPU architecture fills announced GW-scale power deals, the cadence of hardware refresh cycles, and competitive compute-per-watt benchmarks versus AMD, Intel, and custom hyperscaler silicon.