Why AI Makes Markets Safer Daily but Riskier in a Crisis

4 hrs ago

For roughly two years, Nvidia’s revenue story was inseparable from the spending decisions of a handful of cloud giants. Meta, Microsoft, Google, Amazon: their quarterly capex guidance moved Nvidia’s stock price more reliably than almost any other variable. That concentration was a strength when hyperscaler budgets were accelerating. It was also a single point of vulnerability.

That dynamic just changed in a measurable way. Nvidia confirmed, via a Citi analyst note reported by Investing.com on 12 July 2026, that non-hyperscaler business led the most recent quarter’s growth. Not supplemented it. Led it.

Here is what the demand shift actually means beneath the headline: which customer segments are now driving growth, why their spending patterns differ from hyperscalers, and what that tells you about the durability of Nvidia’s revenue base heading into the next earnings cycle.

This was not a sudden event. Nvidia indicated that demand from AI laboratories, sovereign customers, and enterprise on-premise deployments had been gathering momentum across roughly the past two years, reaching the point in the most recent quarter where non-hyperscaler buyers became the primary engine of growth. Bain’s analysis of GTC 2026 reinforced the timeline, noting that AI has moved from pilots to “real enterprise deployment” across organisations that are rebuilding operating models around AI rather than treating it as a bolt-on tool.

The contrast between phases is worth making explicit:

When asked about Meta’s cloud expansion plans, Nvidia chose not to offer any comment, a notable omission. That kind of selective silence signals the company is actively managing the narrative around individual hyperscaler exposure, reinforcing the diversification framing rather than letting a single customer relationship define the story.

For the reader, this timeline matters. A two-year structural build is not a one-quarter anomaly driven by a single large deal. It is a trend with enough duration to evaluate as durable.

The assumption that large enterprises would simply rent AI capacity from cloud providers is reasonable on the surface. The hyperscalers built the infrastructure first, they offer it as a service, and the economics of shared capacity should favour the cloud buyer. That assumption is breaking down for a meaningful cohort of enterprises, and the reasons are specific.

The Bain framing of AI moving from pilots to real deployment sits against a harder statistical backdrop: enterprise AI adoption rates remain low, with an estimated 70-80% of AI pilots failing or stalling before reaching operational scale, meaning the cohort of enterprises genuinely committing to infrastructure-level deployment is still a fraction of the total addressable market.

For data-sensitive, regulated industries such as healthcare, financial services, and industrials, keeping AI workloads on-premises or in hybrid configurations is driven by data sovereignty requirements, compliance obligations, and latency needs. A hospital system running real-time diagnostic inference cannot tolerate the round-trip delay of a cloud API call. A bank subject to data residency regulation cannot send customer data to a third-party data centre in another jurisdiction.

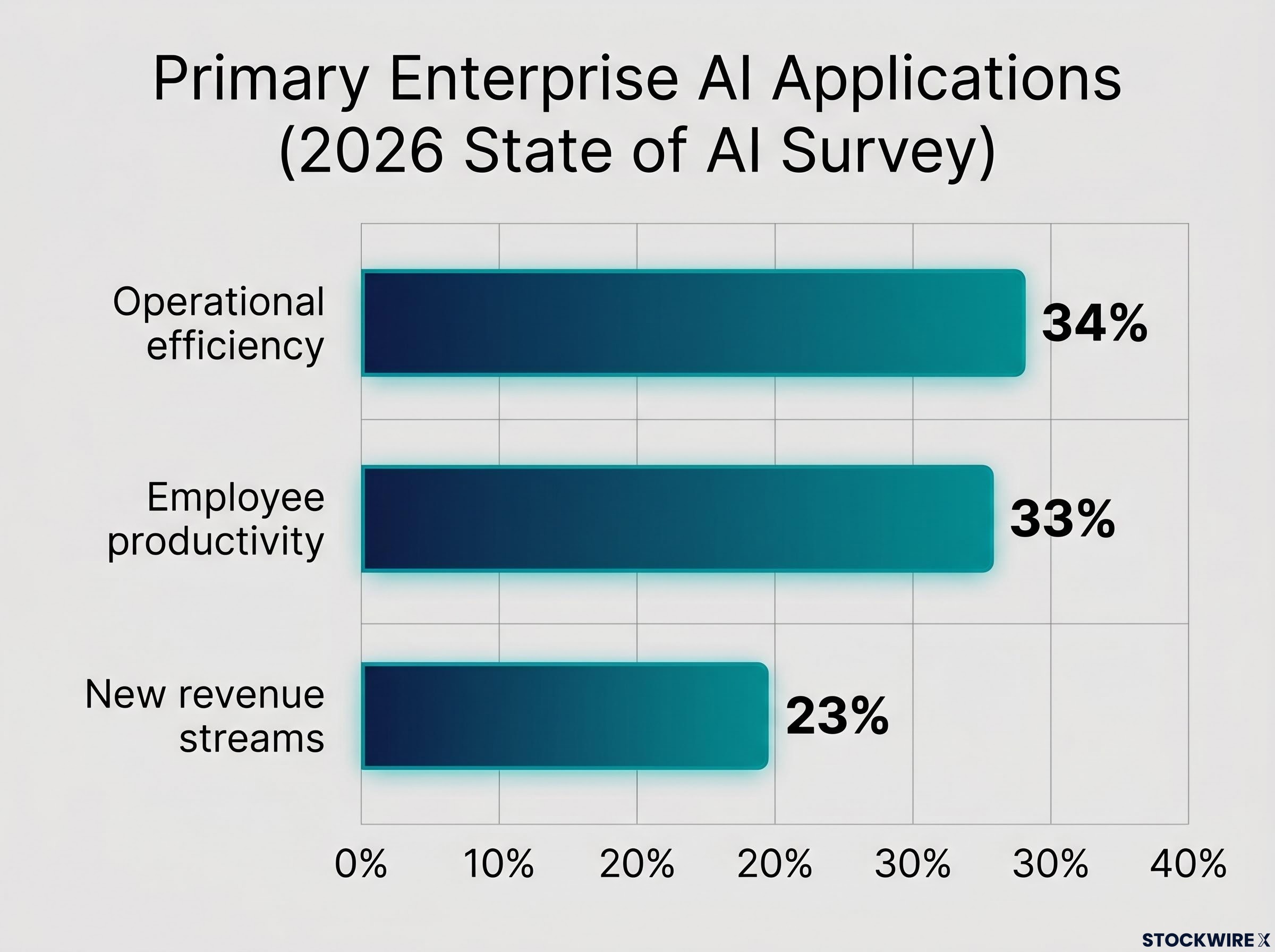

Nvidia’s own survey data points to the use cases that justify infrastructure ownership. According to the 2026 “State of AI” survey, the primary enterprise applications are operational efficiency (34%), employee productivity (33%), and new revenue streams (23%). These are ongoing operational workloads, not one-off experiments, which makes the economics of owning infrastructure rational for organisations running them at scale.

Bain’s GTC 2026 assessment framed this directly: enterprises are rebuilding operating models around AI, not treating it as a bolt-on tool.

Nvidia’s in-house models, Nemotron and Cosmos, are built to support enterprise and sovereign deployment rather than to challenge leading frontier model developers, carving out a distinct role as tools for the deployment layer across these customer segments. The model-agnostic approach (supporting both open-source and proprietary models) maximises infrastructure utilisation across diverse customer segments. And once enterprises commit to a specific AI infrastructure stack, the switching costs in skills, integrations, and embedded workflows make those deployments structurally sticky. The revenue relationship looks less like a commodity hardware sale and more like a long-duration services contract.

Government AI spending operates on a fundamentally different logic from corporate capex. Sovereign AI programmes are national or government-led initiatives to build domestic AI infrastructure with local data residency, local language support, and strategic independence from foreign cloud providers. The spending decisions are driven by policy and national competitiveness, not quarterly earnings cycles.

That distinction matters analytically. When a hyperscaler cuts capex in response to a soft quarter, it flows directly into Nvidia’s revenue. Sovereign programmes are budget-driven by multi-year policy commitments and are relatively insulated from that kind of reallocation. According to the Citi analyst note of 12 July 2026, Nvidia communicated that sovereign and enterprise on-premise deployments are expected to account for a rising share of overall market demand as physical AI adoption broadens.

Sovereign AI infrastructure commitments are becoming more concrete: Nvidia’s June 2026 partnership package in South Korea, covering memory supply with SK Hynix, cloud infrastructure with SK Telecom, AI data centres with Naver, and energy systems with Doosan, illustrates how multi-party government-adjacent ecosystems are being assembled around a single national AI buildout agenda.

The scope of government use cases makes the demand concrete:

Open-source model availability, including Nvidia-supported open models, specifically facilitates government adoption. Public-sector deployments often require transparency, auditability, and customisation that proprietary cloud APIs cannot provide. Nvidia’s full-stack positioning (chips, networking, software platforms) gives it a clear supplier role across these programmes.

For investors and analysts, sovereign AI demand functions more like government procurement than technology capex. It adds a counter-cyclical buffer to Nvidia’s revenue that hyperscaler spending cannot provide.

The question shifts here from who is buying Nvidia’s hardware to where the hardware ends up physically. Physical AI refers to AI systems that operate in the physical world: autonomous vehicles, industrial robots, warehouse automation systems, and smart infrastructure that require real-time local inference. These systems cannot depend on high-latency cloud connections. A robotic arm on a factory floor needs to make decisions in milliseconds, not wait for a response from a data centre hundreds of kilometres away.

The infrastructure implication is structural. Edge inference and embedded compute must be deployed at the point of operation, pushing spending into enterprise and sector-specific budgets rather than cloud provider capex lines. This is demand that is, by its physical nature, non-hyperscaler.

Nvidia raised its AI chip demand outlook to $1 trillion through 2027, framed specifically as inference-driven, reflecting AI doing productive work rather than experimentation. Bain’s assessment is that physical AI is crossing into real deployment timelines in automotive, robotics, and healthcare. The adoption follows industrial capex cycles and regulatory approval timelines, producing a multi-year, multi-sector demand tail that extends well beyond the initial generative AI training boom.

| Physical AI Sector | Deployment Type | Infrastructure Requirement | Approximate Adoption Timeline |

|---|---|---|---|

| Automotive | Autonomous driving, ADAS | In-vehicle edge inference | 2025-2030+ |

| Industrial Robotics | Factory automation, quality control | On-premises local compute | 2025-2028 |

| Warehouse/Logistics | Autonomous picking, routing | Facility-level edge compute | 2025-2027 |

| Healthcare | Real-time diagnostics, surgical AI | Hospital-embedded inference | 2026-2030+ |

A reader evaluating Nvidia’s revenue longevity should understand that physical AI is not an incremental upside scenario. It is a structural demand floor that grows independently of whether any hyperscaler increases or cuts its training capex.

Nvidia’s competitive position is often discussed in terms of chip performance. That framing misses where the real lock-in sits. The company operates a three-layer stack: accelerators, high-performance networking (InfiniBand and Ethernet), and a software platform built around CUDA, SDKs, microservices, and proprietary models. Each layer adds a different type of switching friction.

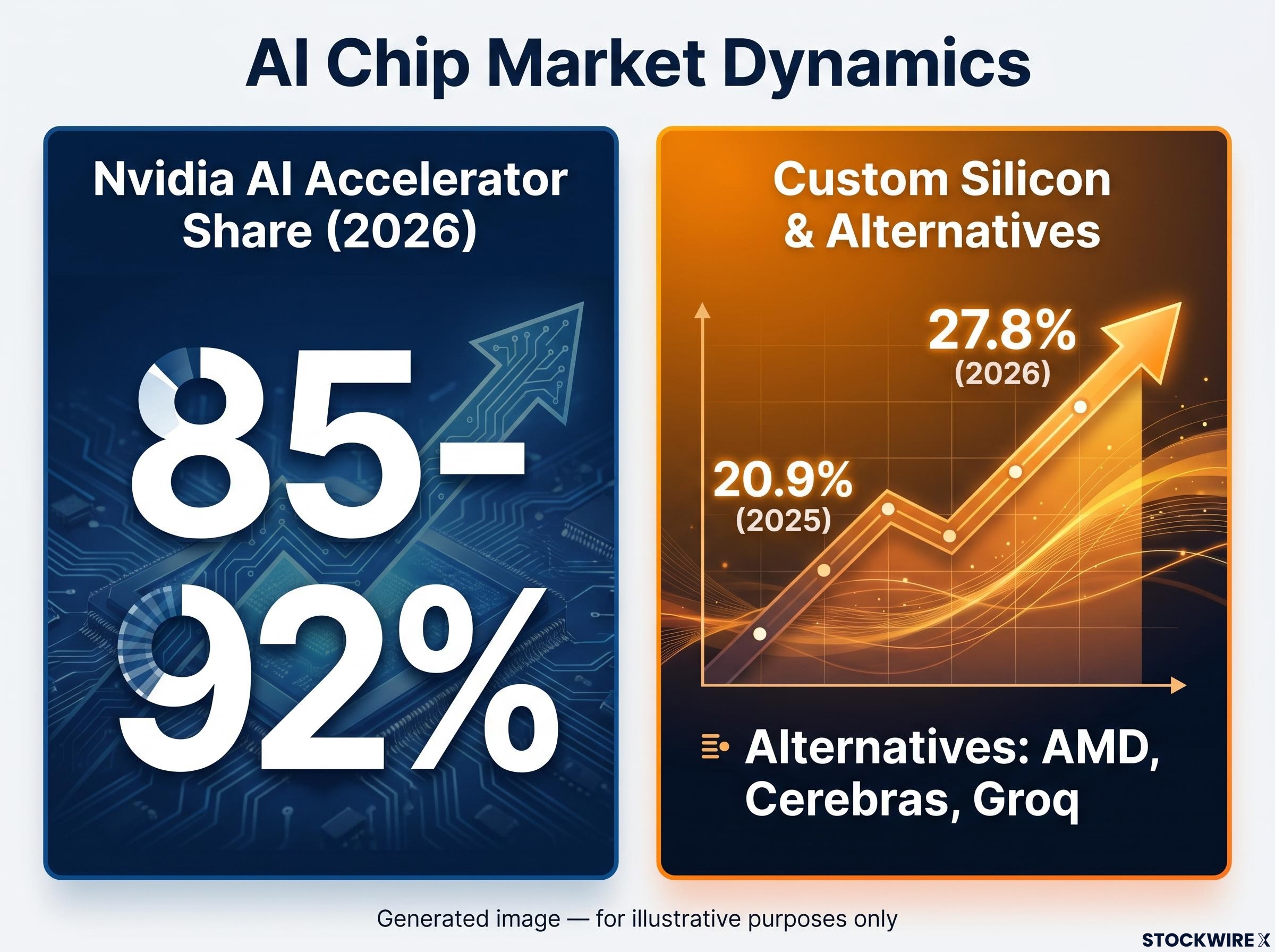

Nvidia holds an estimated 85-92% AI accelerator market share as of 2026, according to analyst estimates.

That figure is commanding, but the stack strategy is designed to make share loss structurally harder than raw chip-to-chip performance comparisons suggest.

| Stack Layer | What It Includes | Switching Friction It Creates |

|---|---|---|

| AI Accelerators | GPUs, specialised AI chips | Hardware replacement cost, performance gap risk |

| Networking | InfiniBand, Ethernet for AI clusters | Cluster re-architecture, interconnect redesign |

| Software and Models | CUDA, SDKs, Nemotron, Cosmos, microservices | Retraining staff, re-engineering workflows, rebuilding integrations |

The competitive context is real. Custom silicon and alternatives are projected to lift their share of the AI chip market from roughly 20.9% in 2025 to around 27.8% by 2026. AMD’s Instinct GPUs, Cerebras, and Groq are the most relevant alternatives for enterprise and government segments specifically. The market share erosion figure tells you that Nvidia’s position is being tested at the margins. But the stack strategy means share loss requires a customer to abandon not just a chip but an entire integrated workflow, and that is a substantially higher bar.

Software platforms and services also generate revenue between hardware refresh cycles, smoothing Nvidia’s revenue profile and reducing dependence on episodic capex decisions.

The demand profile is genuinely different from two years ago. That deserves specific articulation before the risks do.

What has structurally improved:

The risks that diversification does not neutralise, however, are real and worth monitoring with equal specificity.

Custom silicon competition from within Nvidia’s own customer base introduces a structural paradox: the same $700 billion AI capex wave funding Nvidia’s order book is simultaneously bankrolling the ASIC programmes at Alphabet, Amazon, and Microsoft that are most competitive precisely in the inference segment projected to represent 80% of the accelerator market by 2030.

What remains to watch:

The honest framing is that the demand base is more durable than two years ago, but the competitive and regulatory environment is also more complex. Customer diversification is genuinely positive for revenue durability. It does not remove the obligation to monitor competitive share trends and export policy developments as the enterprise and government segments mature.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding demand projections and market share are subject to change based on market developments and competitive dynamics.

Nvidia’s customer base transformation is not a single quarter’s event. It is a two-year structural shift now visible in revenue leadership by non-hyperscaler segments. Evaluating the company’s outlook requires tracking enterprise deployment momentum, sovereign programme announcements, and physical AI adoption timelines alongside hyperscaler capex guidance.

Three variables are worth watching ahead of future earnings and industry events: the scale and pace of sovereign AI programme commitments globally, physical AI deployment timelines in automotive and industrials where regulatory approvals are the gating factor, and competitive alternative silicon uptake in enterprise deals where buyers have the sophistication to evaluate beyond the Nvidia ecosystem.

The demand story has genuinely diversified, which reduces some risks and introduces others. Anyone still reading Nvidia primarily through the hyperscaler capex lens is working from an incomplete map.

Investors evaluating where durable value sits across the broader AI buildout will find our deep-dive into AI infrastructure binding constraints examines how power availability, cooling density, and grid interconnection timelines are concentrating investable value at layers of the stack that sit below the chip and software debate this article covers.

—

Beyond Meta, Microsoft, Google, and Amazon, Nvidia's growing customer base includes AI laboratories, sovereign government programmes, and enterprises deploying on-premise AI infrastructure in sectors like healthcare, financial services, and industrials.

Data sovereignty requirements, compliance obligations, and latency constraints drive regulated industries toward on-premise deployments; a hospital running real-time diagnostic inference or a bank subject to data residency rules cannot rely on third-party cloud infrastructure.

Sovereign AI refers to national government programmes that build domestic AI infrastructure with local data residency and strategic independence from foreign cloud providers; because these commitments are driven by multi-year policy budgets rather than quarterly earnings cycles, they add a counter-cyclical buffer to Nvidia's revenue that hyperscaler spending cannot provide.

Analyst estimates put Nvidia's AI accelerator market share at approximately 85-92% as of 2026, though custom silicon alternatives are projected to grow from roughly 20.9% of the market in 2025 to around 27.8% by 2026.

Physical AI refers to systems that operate in the real world, including autonomous vehicles, industrial robots, and warehouse automation, where real-time local inference makes cloud connectivity impractical; Nvidia raised its AI chip demand outlook to $1 trillion through 2027, framed specifically around this inference-driven deployment wave.