SpaceX’s $800 Price Target: Right Direction, Wrong Timeline?

1 hr ago

Artificial intelligence is making markets more efficient on ordinary days. Spreads are tighter, information moves faster, and routine pricing errors get corrected before most investors notice them. That same efficiency, though, is quietly building a structural problem: the smarter markets become, the more precisely they can all be wrong in the same direction at the same time.

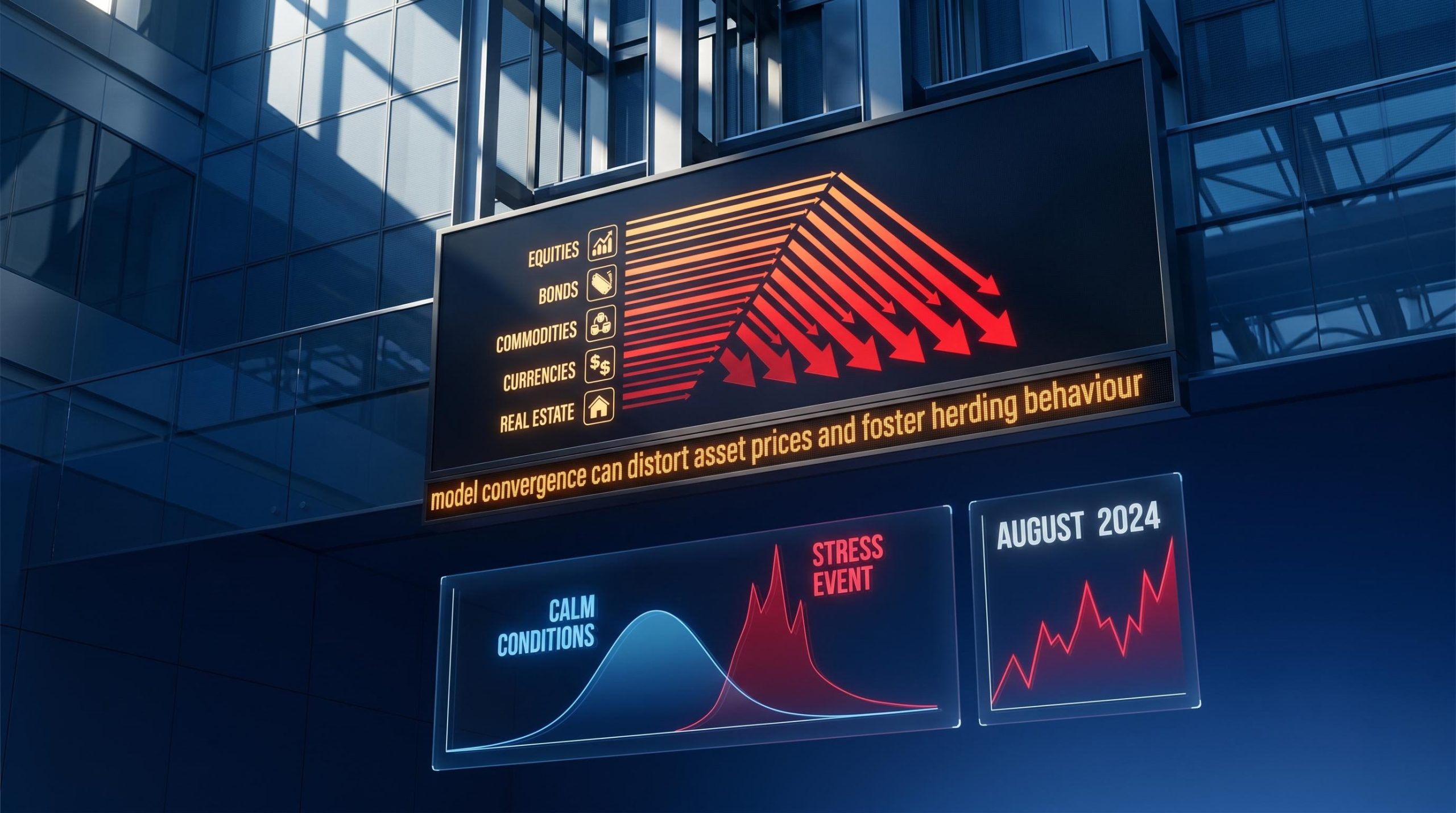

The tension sits at the centre of a growing body of institutional warnings. Bernstein researchers have flagged synchronised trading signals and correlated AI-driven strategies as a systemic concern. The European Central Bank has warned that model convergence can distort asset prices and foster herding behaviour. None of this means a crash is imminent. It means the architecture of tail risk is changing in ways that historical models were not designed to capture.

Here is the framework for separating AI’s demonstrated daily benefits from its structurally plausible but underappreciated tail-risk profile, grounded in real events and credible institutional warnings.

The crowding pathway starts well before any crisis. It starts in the training data.

When AI systems across many institutions draw on similar datasets, those models tend to surface the same patterns and push toward the same trade ideas at the same time. Converging signals produce converging positions. What looks like independent analysis from dozens of different funds turns out to be the same edge, arrived at by the same means.

Unlike traditional algorithmic programs that follow fixed decision rules, AI trading systems adapt their own behaviour from incoming data, which means their failure modes are structurally less transparent and harder to anticipate than those of the rule-based predecessors they are replacing.

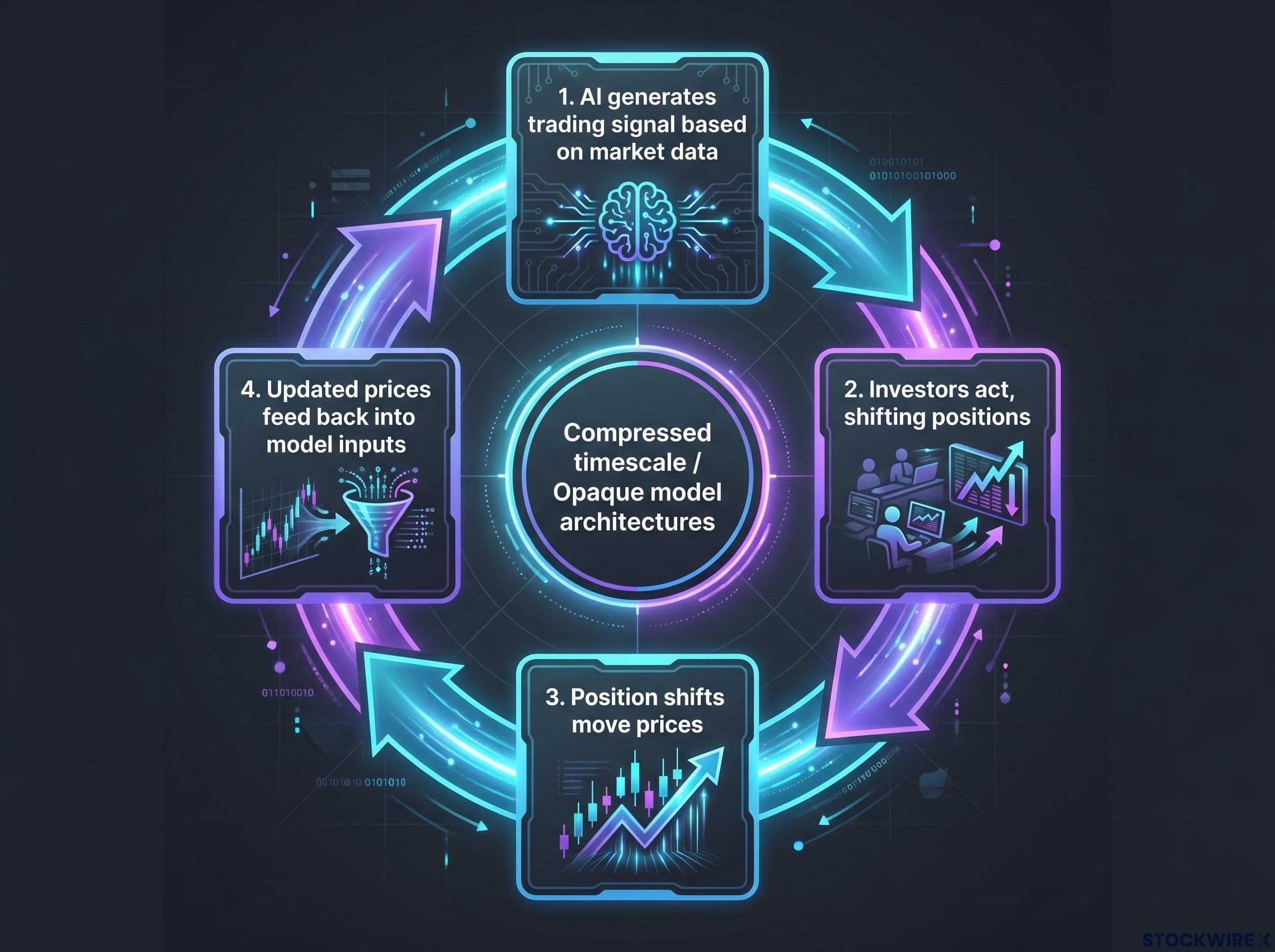

The three-stage pathway is straightforward:

Legal and policy commentary characterises advanced AI trading as capable of creating a “monoculture” where participants draw from the same data and employ similar models. The ECB’s warning connects this directly to instability:

The European Central Bank has warned that model convergence can distort asset prices, increase correlations, foster herding behaviour, and contribute to bubble formation.

The ECB research bulletin on AI model convergence details how shared architectures and overlapping training data push institutions toward correlated positioning, with the bank identifying herding behaviour and asset price distortion as the primary transmission channels from model similarity to market instability.

The risk is not about any individual AI strategy failing. It is about the market’s collective loss of the diverse opinions that ordinarily provide counterparties during a shock. On calm days, the monoculture is invisible. Under stress, when all those correlated positions must unwind simultaneously, it becomes the defining feature of the sell-off.

Crowded institutional positioning in AI-linked equities has moved beyond a theoretical concern: the BofA June 2026 fund manager survey recorded 80% of respondents naming long global semiconductors as the most crowded trade in the survey’s 12-year history, a concentration pace with no historical precedent that sits directly on top of the monoculture dynamic described here.

Crowding explains why positions cluster. The reflexivity problem explains why they can reinforce themselves until the market’s price signal no longer reflects independent information.

A reflexivity feedback loop (a self-reinforcing cycle where model outputs and market prices amplify each other) operates in four steps:

Bernstein researchers characterised this as a distinct systemic risk category from crowding. The loop is structurally similar to the reflexivity framework developed by George Soros, but with two differences that matter. First, the timescale is compressed: AI systems can complete the cycle across many institutions faster than human-mediated reflexivity ever could. Second, the feedback mechanism is embedded inside opaque model architectures, making it harder for risk managers or regulators to identify the pattern while it is running.

The Kogod School of Business has stressed that AI’s speed, overreliance, and monitoring challenges make these feedback loops harder to detect and dampen. Deep-learning architectures make it structurally difficult to trace which price movements originated in model outputs versus independent market information.

Regulatory frameworks designed for human-mediated strategies were not calibrated for feedback cycles operating at millisecond timescales. Fabricated AI-generated content has shown a capacity to shift U.S. equity prices in the short term, with corrections only arriving once verification caught up, adding a further reflexivity-adjacent tail-risk channel.

The speed dimension means the loop can complete multiple cycles before any human decision-maker has the information to intervene. That is what separates AI-era reflexivity from historical precedents you may already understand.

The evidence does not point to AI being simply good or simply dangerous for markets. It points to a structural asymmetry: AI smooths the distribution of ordinary returns while fattening the left tail.

| AI benefits (calm conditions) | AI risk amplifiers (stress conditions) |

|---|---|

| Faster information processing | Collective simultaneous reaction to shocks |

| Tighter bid-ask spreads | Synchronised de-risking protocols firing across firms |

| Improved risk measurement | Higher correlation across portfolios during stress |

| Compression of routine informational inefficiencies | Liquidity evaporation as algorithms step back together |

| Reduced average market inefficiency | Sharper, faster tail moves with less warning |

Bernstein research characterises the net picture as better routine functioning paired with a heightened probability of severe dislocations when conditions deteriorate. Academic work on AI and financial fragility reaches the same conclusion from a different direction: AI can improve price prediction while simultaneously making markets more fragile, volatile, and prone to crisis.

The BIS bulletin on AI fragility in financial markets provides cross-institutional evidence that machine learning strategies can improve price prediction while simultaneously increasing systemic vulnerability, a finding that sits directly behind the dual efficiency and fragility framing this analysis applies.

The benefits and risks are not in tension with each other. They are structurally linked. The same convergence that produces daily efficiency gains is what makes the stress-period outcome worse. For your own investment process, the implication is that AI may make day-to-day portfolio management genuinely better while also meaning that when the tail event arrives, it arrives faster and with less warning than historical patterns would suggest.

In August 2024, the yen carry trade unwound rapidly. Automated strategies and risk controls compressed and amplified stress in ways consistent with the crowding and feedback mechanisms described above. Bernstein research pointed to this episode to show how correlated automated systems can pile pressure onto already-stressed conditions and sharpen the pace of volatility.

Three structural features of the episode mirror the crowding-and-reflexivity framework:

An important evidentiary caveat: Direct public evidence that advanced AI-specific models, as opposed to more traditional algorithmic and quantitative systems, were the primary driver of this episode is limited. The event is a structural illustration, not a confirmed AI-driven crash. This is a distinction worth maintaining, because analytical honesty about the evidence strengthens rather than weakens the broader argument.

The August 2024 episode functions as a preview rather than a proof. It shows you what the stress dynamic looks like at scale, even before AI becomes the dominant force in execution. The mechanisms at work (simultaneous automated de-risking, correlated exits, liquidity evaporation) are precisely what the crowding and reflexivity frameworks predict would occur if AI adoption deepens.

Sentiment-driven valuations in AI equities proved particularly fragile when three shocks arrived in a single session on 26 June 2026, including a Fed hawkish pivot and an OpenAI IPO delay, illustrating how narrative-dependent positions unravel faster than fundamental repricing once cheap capital and a landmark catalyst recede simultaneously.

The current evidentiary state is clear: plausible risk with credible institutional warnings, not imminent catastrophe. No fully documented AI-driven crash exists yet. But vulnerability is measurable and growing, and the mechanisms are well-understood enough to act on.

Academic research presented to European regulators has found that large language models can function as effective trading agents, and explicitly warns that widespread use of similar LLM-based strategies could introduce new systemic risks. Cross-country empirical research links increased AI investment to higher financial systemic risk, particularly in more developed markets. Bernstein identifies common exposures, leverage, and liquidity mismatches as the primary amplification channels.

Stress-testing is the primary practical response. What AI-era scenarios should add to your existing frameworks:

Standard historical volatility-based risk models may be structurally inadequate for tail events produced by synchronised AI behaviour. The honest investor takeaway is not to abandon AI tools, but to stress-test portfolios against scenarios that existing models were not designed to capture.

Tail risk hedging through structures such as collars and long-dated puts addresses precisely the scenario the AI fragility framework predicts: AI forecasting tools are structurally biased toward median outcomes and compress away the probability mass in the tails where synchronised de-risking events actually live.

On the regulatory side, proposed responses in the literature include:

Whether these measures materialise before the next significant stress event is one of the two variables that will determine how this risk unfolds.

The evidence aligns clearly on some claims and not at all on others. Knowing the difference is the most useful thing you can take from this analysis.

| Claim | Evidence status | Source basis |

|---|---|---|

| Synchronised algorithms and crowding amplify stress | Supported | ECB warnings, academic literature, Bernstein research, policy analysis |

| Reflexive feedback loops create self-reinforcing price distortions | Supported, consistent with AI fragility frameworks | Bernstein research, Kogod School analysis, systemic risk literature |

| AI lowers routine inefficiency while worsening the severity of stress-period dislocations | Supported | Dual efficiency/fragility frameworks, Bernstein research |

| An AI-driven crash has already occurred | Not supported | No fully documented case exists; August 2024 is illustrative, not conclusive |

| LLMs as trading agents introduce new systemic risks | Supported by academic work | Research presented to European regulators |

Advanced deep-learning AI is not yet dominant in live trading systems, but integration is deepening. Two conditions would move this from plausible risk to acute threat: deeper penetration of advanced AI (particularly LLM-based systems) into live execution, and a stress episode severe enough to trigger simultaneous de-risking at scale.

What you should watch: the pace of AI adoption in asset management, the degree to which model architectures are converging across institutions, and whether regulatory diversity requirements materialise before the next significant stress event. The risk is not a warning to exit markets. It is a structural shift in tail-risk dynamics that warrants updating the mental models and stress scenarios you already use.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and evolving AI adoption patterns.

The primary risks are model convergence (where AI systems trained on similar data produce correlated positions), reflexivity feedback loops (where model outputs move prices that then feed back into the same models), and synchronised automated de-risking (where multiple AI-driven strategies exit positions simultaneously during stress events, draining liquidity faster than historical norms).

A reflexivity feedback loop occurs when an AI system generates a trading signal, investors act on it and move prices, and those updated prices feed back into the model as apparent confirmation of the original signal, creating a self-reinforcing cycle. AI compresses this cycle to millisecond timescales across multiple institutions simultaneously, making it harder to detect and dampen than human-mediated reflexivity.

Direct public evidence that advanced AI models were the primary driver is limited; the episode is better characterised as involving traditional algorithmic and quantitative systems rather than confirmed AI-specific architectures. It functions as a structural illustration of what synchronised automated de-risking looks like at scale, not as a confirmed AI-driven crash.

When multiple institutions train AI systems on similar datasets, those models identify the same signals and build correlated positions, creating a market monoculture where aggregate positioning is far less diverse than it appears. The ECB has specifically warned that this dynamic distorts asset prices, increases correlations, and fosters herding behaviour that can contribute to bubble formation.

Investors should stress-test portfolios against scenarios that standard historical volatility models were not designed to capture, including simultaneous multi-firm de-risking, correlation spikes beyond historical training data, and liquidity withdrawal speeds far exceeding past norms. Tail risk hedging structures such as collars and long-dated puts are specifically suited to the scenario AI fragility frameworks predict, since AI forecasting tools are structurally biased toward median outcomes and underweight the probability mass in the tails.