Salesforce vs Shopify: How to Tell Real AI Monetisation Apart

3 mins ago

Raymond James analyst Brian Gesuale initiated coverage of SpaceX this week with an $800 per share price target and a Strong Buy rating, the highest published target on Wall Street. The number is large. The logic behind it is larger, and considerably more specific than a round number suggests.

The target is not a prediction that SpaceX will be worth $800 a share. It is the output of a probability-weighted scenario architecture built on three interdependent pillars: Starship achieving near-total launch cost compression, Starlink and adjacent platforms scaling into high-margin recurring businesses, and entirely new orbital market categories reaching commercial scale by 2031. Each pillar carries its own assumptions, and each assumption sits at or near the optimistic edge of what independent technical and market analyses currently support.

Here is what the model actually requires, where the external evidence agrees with it, and where the gaps are wide enough that your own probability assessment matters more than the analyst’s.

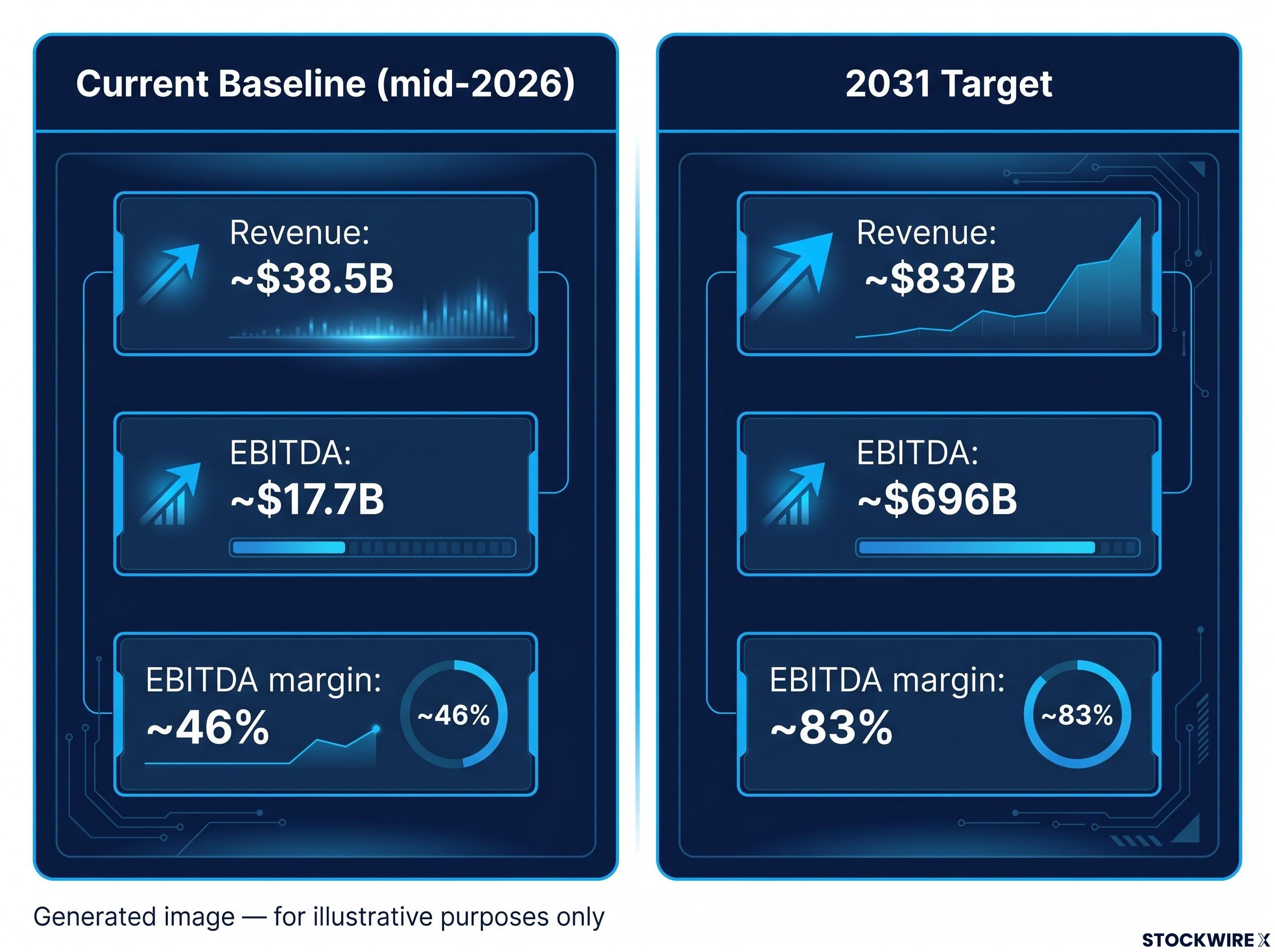

The financial architecture starts with a baseline: SpaceX today brings in roughly $38.5 billion in annual revenue and roughly $17.7 billion in EBITDA (earnings before interest, taxes, depreciation, and amortisation), putting its current EBITDA margin at roughly 46%.

By 2031, Gesuale’s model requires the business to have scaled to roughly $837 billion in revenue and roughly $696 billion in EBITDA, producing an implied EBITDA margin of roughly 83%. Applying a 27x exit multiple to that 2031 EBITDA figure produces an implied terminal enterprise value of roughly $18.8 trillion, which the model then discounts back to its present-day equivalent of $800 per share.

The CAGR mathematics behind SpaceX’s revenue targets reveal how extraordinary the growth burden actually is: reaching $1 trillion in revenue by 2030 from the 2025 base requires approximately 122% annual compound growth, roughly four times faster than the strongest sustained rate ever recorded by any mega-cap company.

| Metric | Current baseline (mid-2026) | 2031 target |

|---|---|---|

| Revenue | ~$38.5B | ~$837B |

| EBITDA | ~$17.7B | ~$696B |

| EBITDA margin | ~46% | ~83% |

Raymond James describes the 27x multiple as modest when set against a comparable peer group whose valuations cluster around 60.7x on 2028 estimates. That gap between 27x and 60.7x is not modesty. It is the mechanism through which the model internalises execution risk. Understanding the size of that built-in discount tells you how much probability adjustment is already embedded before you layer on your own.

The $30 trillion total addressable market (TAM), the total theoretical revenue pool a company could pursue, underpinning the thesis is not a revenue projection. It is a constructed estimate of the sectors that cheap orbital infrastructure could restructure: transportation, communications, compute, manufacturing, and energy.

Gesuale frames SpaceX as analogous to the railroads, arguing that the value was never in the rails themselves but in the industries, settlements, and supply chains they made possible. The same logic applies: the value of cheap launch is not in the rocket but in what becomes economically viable once a kilogram reaches orbit for tens of dollars rather than thousands.

The comparisons to electrification, containerisation, and the early internet follow the same structure. Each was a general-purpose enabling technology whose economic impact was realised not by the infrastructure builder alone, but across entire economies.

What each TAM sector represents:

Independent analyses from Citi and Bain confirm that cheap launch could expand the space economy dramatically, but their largest-impact scenarios sit in the 2035-2040 window, not 2031. The $30 trillion figure tells you the ceiling of what orbital access could theoretically open up, not what SpaceX will collect, and the distance between those two figures is where most of the investor risk lives.

Everything downstream in the model, the margin expansion, the TAM capture, the terminal value, depends on Starship achieving near-best-case cost-per-kilogram economics by 2031. This is the load-bearing assumption.

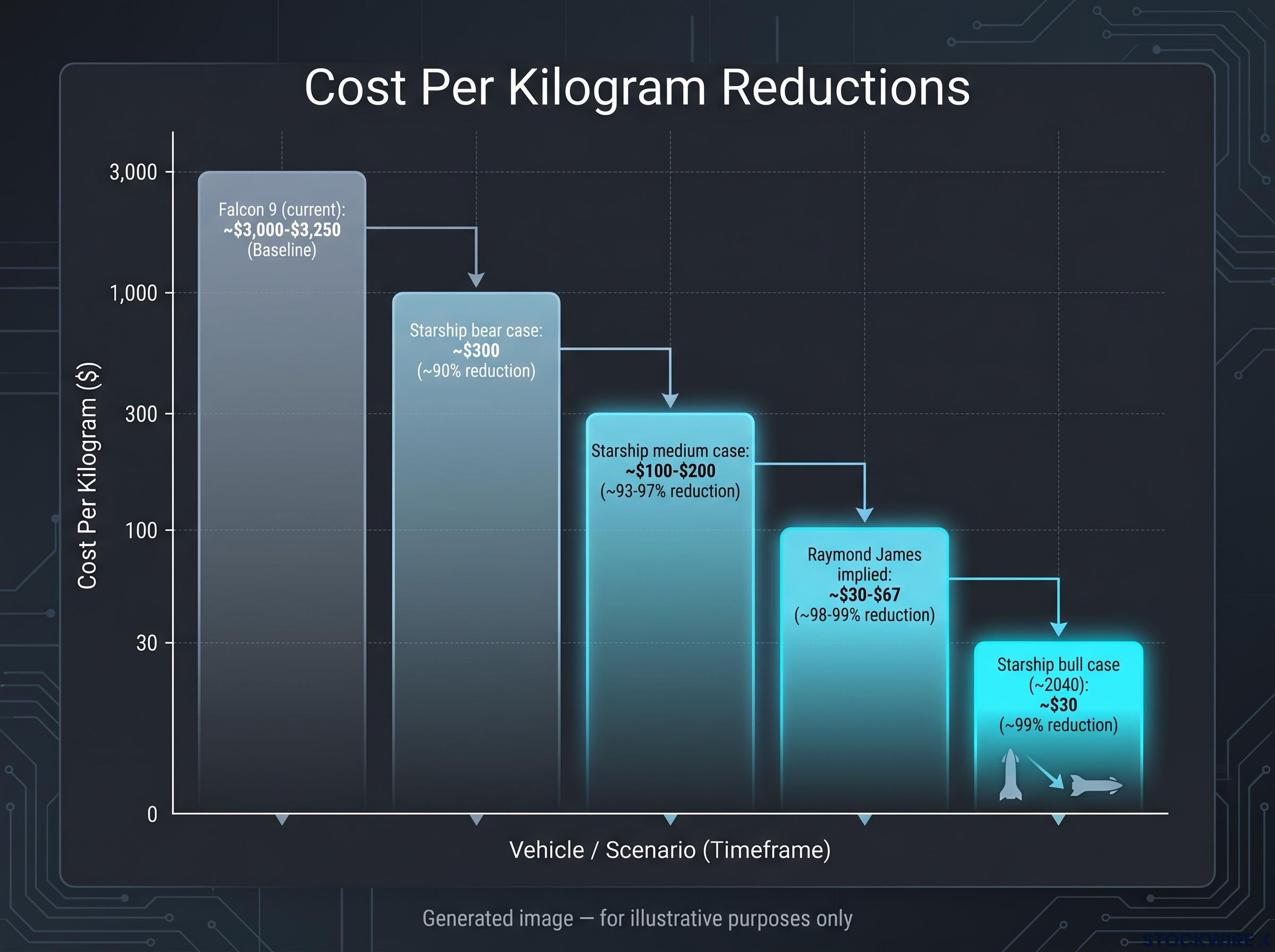

Falcon 9 currently delivers payload to low Earth orbit at approximately $3,000-$3,250 per kilogram at dedicated launch pricing. SpaceX’s aspirational target for a fully reusable Starship is approximately $10 million per flight at 150 tonnes of payload, which implies approximately $67 per kilogram. That would represent a reduction of roughly 98% from current Falcon 9 pricing.

The $30 per kilogram figure is the threshold that gets you to the 99% reduction the model implicitly requires. External banks treat that number as a bull-case outcome achievable by approximately 2040, not an early-2030s base case.

Independent modelling from Citi, Bain, and the American Enterprise Institute converges on a medium-term range of approximately $100-$200 per kilogram, with bear-case scenarios around $300 per kilogram if reuse cadence disappoints.

| Scenario | Cost per kg | Reduction from Falcon 9 |

|---|---|---|

| Falcon 9 (current) | ~$3,000-$3,250 | Baseline |

| Starship bear case | ~$300 | ~90% |

| Starship medium case | ~$100-$200 | ~93-97% |

| Starship bull case (~2040) | ~$30 | ~99% |

| Raymond James implied | ~$30-$67 | ~98-99% |

If Starship stabilises in the $100-$200 per kilogram range rather than approaching $30, the model’s EBITDA margin and TAM assumptions face direct downward pressure. The $800 target compresses significantly even before you touch the multiple.

The margin expansion from approximately 46% to approximately 83% is the most aggressive single assumption in the model. It rests on two drivers operating simultaneously.

The first driver is mechanical. If Starship radically reduces the marginal cost of each launch, the variable cost base of the entire operation compresses. Lower cost per kilogram means higher gross margin on every payload delivered, every satellite deployed, and every government contract fulfilled.

The second driver is structural. As revenue mix shifts from launch services toward recurring, high-margin businesses, the overall margin profile changes character. The businesses contributing to this shift include:

Each of these carries different capital intensity. Starlink connectivity requires ongoing satellite replenishment and a global ground station network. Data platforms are lighter. Compute services are somewhere in between. Point-to-point transport is capital-heavy and regulatory-heavy.

The industrial finance counterargument is straightforward: businesses that manufacture rockets, operate global ground station networks, and build entirely new orbital markets carry capital expenditure that typically prevents pure-software margin profiles. Integrated operations reaching 83% EBITDA margins would require the revenue mix to shift so completely toward recurring, infrastructure-light sources that the manufacturing and operations base becomes a rounding error on the income statement.

The 83% margin assumption is asking you to believe SpaceX behaves more like a software platform by 2031 than like an aerospace manufacturer. Whether you accept that depends on how quickly and completely the revenue mix shifts, and small margin misses create outsized impacts on the final price target because margin drives EBITDA, EBITDA drives terminal value, and terminal value drives $800.

Each programme in SpaceX’s portfolio has been structured to generate the capital that underwrites the next stage of development. The sequencing is deliberate and mutually reinforcing:

Starlink’s two franchises, rural broadband subscriptions and wholesale Direct-to-Cell infrastructure distributed through carriers including T-Mobile, operate off the same constellation with meaningfully different capital intensity profiles, a structural feature that directly shapes how much of Starlink’s revenue growth translates into incremental margin.

This structure gives SpaceX unusual strategic autonomy. It limits dilution, reduces interest-rate sensitivity, and creates a self-reinforcing infrastructure cycle that most competitors cannot replicate because they lack the upstream revenue to fund the downstream ambition.

Each link is load-bearing. If Starlink’s subscriber growth, pricing power, or regulatory access underperforms for any sustained period, the cascade loses pressure at precisely the moment when Starship needs maximum capital to achieve the cost targets the rest of the model depends on.

Starship delays or cost overruns, in turn, reduce the probability that speculative downstream platforms receive funding on the timeline the model assumes. The self-financing structure is simultaneously SpaceX’s most distinctive competitive advantage and the architectural feature that concentrates execution risk into a single sequential chain. One weak link does not just slow progress; it constrains capital for everything downstream.

The useful question is not whether Raymond James is right. It is how much probability mass you personally assign to something approximating the trajectory the model assumes. Six conditions must hold near their optimistic ends simultaneously:

SpaceX remains private as of July 2026. This coverage primarily informs secondary-market positioning and institutional calibration ahead of a potential IPO rather than direct retail investment decisions.

Most of SpaceX’s current valuation rests on priced-in optionality rather than current fundamentals: Q1 2026 financials showed a $4.28 billion net loss on $4.69 billion in revenue, with Starlink the only profitable segment, while orbital compute and AI infrastructure remained cash-flow negative.

A shift from 27x to 20x on the same EBITDA base, or a modest change in the discount rate, can move the per-share target by hundreds of dollars. The precise $800 figure is extremely sensitive to valuation inputs that cannot be known with precision years in advance.

Each of those six conditions is individually plausible. The compound probability of all six landing near their optimistic ends simultaneously is where your own analysis matters more than any single price target.

The directional case has strong independent support. Cheap, reusable launch can transform multiple industries. Citi, Bain, and AEI modelling all confirm dramatic long-run space economy expansion driven by Starship-class cost reductions. On the direction of travel, Raymond James is not an outlier.

The specific question is timing. Independent analyses place the largest economic impacts of sub-$100 per kilogram launch in the 2035-2040 window, with value creation spread across multiple companies and decades rather than concentrated in SpaceX by 2031. The Raymond James model pulls a very optimistic slice of that long-run potential into a five-year horizon and assumes SpaceX captures a disproportionately large share.

Multiple assumptions must simultaneously hit their optimistic ends. Each one being individually achievable does not make the combination likely on the compressed timeline. Getting the direction right on SpaceX but wrong on the timeline by even a few years can mean holding a position that is correct over a decade but deeply underwater over a five-year horizon.

The $800 target is a coherent, internally defensible bull case. It asks you to hold a strong view on timing rather than direction, and to be comfortable with the specific compound probability that six optimistic conditions converge within five years. The thesis is serious. The assumptions are transparent. The risk is that the future arrives on a different schedule than the model requires.

For investors ready to move beyond the valuation model and assess what early market participants actually priced in, our deep-dive into SPCX’s debut-day trading covers the 28% intraday surge, the cross-asset rotation out of Tesla, and the concurrent selling pressure on smaller space-sector stocks.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections are subject to market conditions and various risk factors. Forward-looking statements regarding SpaceX’s cost targets, revenue, and margin projections are speculative and subject to change based on technical development, market conditions, and company performance.

Raymond James analyst Brian Gesuale initiated coverage of SpaceX with an $800 per share price target and a Strong Buy rating, making it the highest published price target on Wall Street as of mid-2026.

The model projects SpaceX reaching approximately $837 billion in revenue and $696 billion in EBITDA by 2031, applies a 27x exit multiple to produce an implied terminal enterprise value of roughly $18.8 trillion, and then discounts that figure back to a present-day equivalent of $800 per share.

The model implicitly requires Starship to achieve approximately $30 to $67 per kilogram of payload to orbit by 2031, a 98-99% reduction from current Falcon 9 pricing; independent analysts at Citi, Bain, and AEI treat the $30 per kilogram figure as a bull-case outcome achievable around 2040, not an early-2030s base case.

Raymond James deliberately applied a 27x exit multiple against a comparable peer group trading around 60.7x on 2028 estimates; that discount is the mechanism through which execution risk is built into the model before any additional probability adjustment by investors.

SpaceX remains a private company as of July 2026, so this coverage primarily informs secondary-market positioning and institutional calibration ahead of a potential IPO rather than direct retail investment decisions.