Morgan Stanley Rules Out Fed Hikes, Names Two Numbers to Watch

18 mins ago

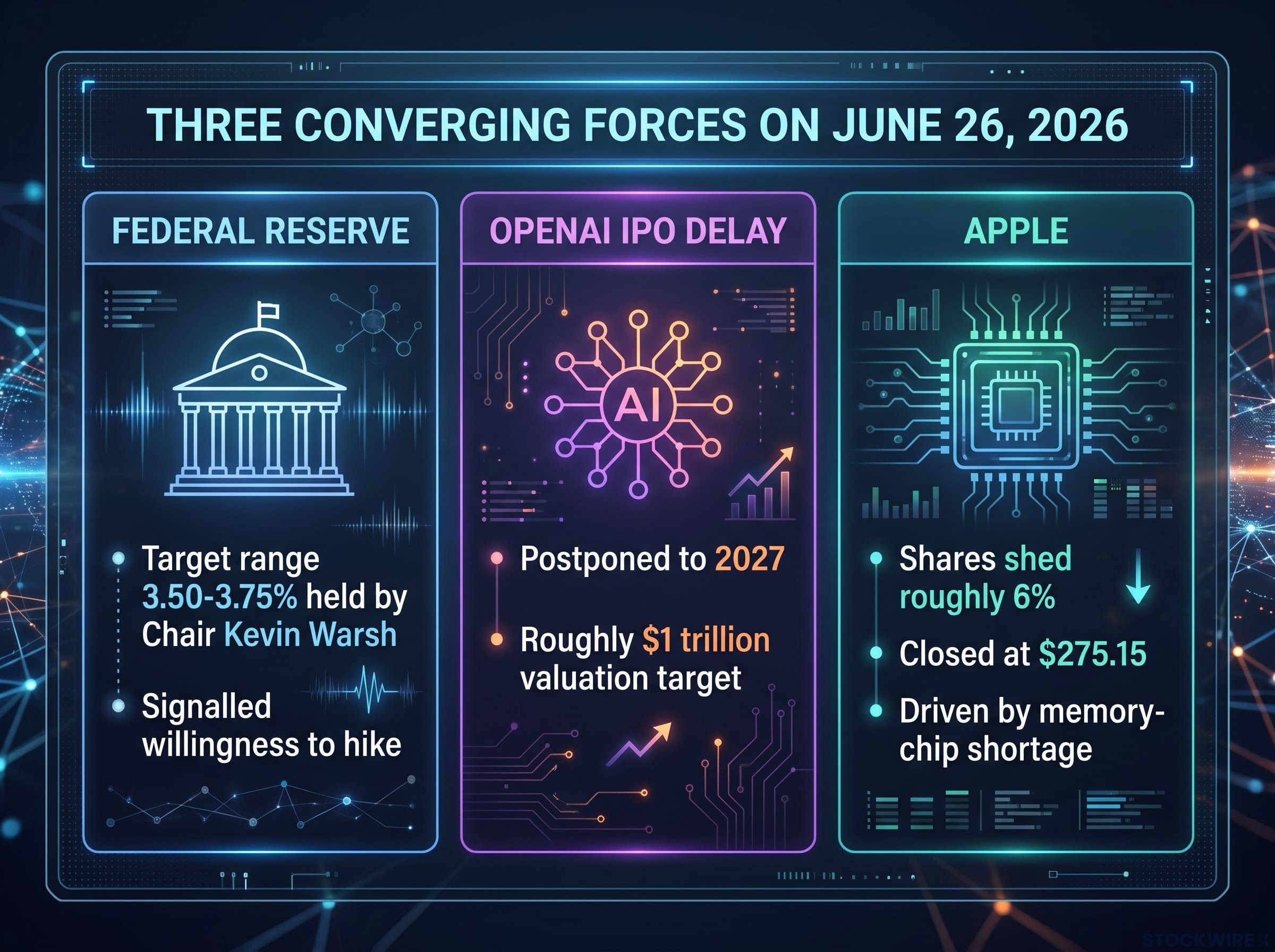

Three separate forces converged on AI-linked technology equities on 26 June 2026, and they arrived in a single session. The Federal Reserve signalled it may raise rates before year-end. According to reports, OpenAI is weighing a postponement of its IPO until 2027. And Apple shed roughly 6% after executives pointed to a global memory-chip shortage, fuelled by AI infrastructure demand, as the driver of product price increases.

For investors who had been riding the AI trade through a prolonged rally, this confluence exposed a structural vulnerability. The same narrative enthusiasm that drove valuations higher left high-multiple tech names with almost no cushion when macro conditions shifted. The session crystallised how fragile sentiment-driven valuations can be when two of the AI cycle’s most anticipated milestones, cheap capital and a landmark IPO, recede at the same moment.

Here is the framework for understanding what just happened, which part of your AI exposure it puts most at risk, and the specific signals to watch before making any portfolio decision.

The Federal Reserve held its target range at 3.50-3.75% at its most recent meeting. But three actions taken alongside that hold changed the landscape:

Fed chair Kevin Warsh led this shift, and major bank analysts have characterised it not as a slower-cut trajectory but as something qualitatively different.

The FOMC April 2026 policy statement confirmed the target range at 3.50-3.75% while noting the Committee’s explicit consideration of the extent and timing of additional adjustments, language that major bank analysts read as opening the door to further hikes rather than signalling a pause.

Analysts at major banks warned that this meeting marked a clear shift toward a possible rate-hike path, not merely a pause or a slower timeline for cuts.

A Fed willing to hike is a different regime from a Fed simply pausing. The distinction matters because AI stocks are long-duration assets, meaning their valuations depend predominantly on cash flows expected years or decades into the future. When the rate used to discount those distant cash flows rises, their present value compresses sharply. A company generating substantial near-term earnings absorbs that compression with less damage. A company valued almost entirely on future promise does not.

For investors wanting historical context on how equity markets have actually performed across prior tightening cycles, our full explainer on rate hikes and stock returns examines RBC Capital Markets data showing the S&P 500 averaged roughly 13.7% during modest hike windows, and maps where AI-heavy growth names diverge from that historical average.

The rate signal that matters most here is not just the policy rate itself but the behaviour of the 10-30 year Treasury curve. That is the part of the yield curve equity analysts actually use when discounting future cash flows. If the long end moves higher independently of short-term expectations, it signals a repricing of the term premium, and that repricing hits high-multiple AI names hardest.

The AI investment cycle has not progressed as a smooth trend. It has moved in a sequence of narrative-validation events, each one ratifying the speculation that preceded it:

That fourth milestone has now been delayed. The New York Times reported in June 2026 that OpenAI is weighing a push of its public listing back to 2027, with advisers indicating that a valuation target of roughly $1 trillion is better suited to a longer runway.

The appropriate framing here is that this is a sentiment shock first, not a fundamental verdict on OpenAI’s business. But it removes one of the clearest near-term catalysts for an AI sector re-rating. Without that validation event on the horizon, speculative positions are left exposed to macro headwinds with no sentiment anchor to absorb them.

The longer the delay persists, the more it risks becoming something more than a timing question in market perception. OpenAI’s business model, built on enterprise licensing, API usage, and partnerships, is still evolving. Translating frontier models into durable, margin-rich revenue at scale remains an open question rather than a solved problem. That uncertainty was easier to carry when the IPO was expected to arrive as a confidence event. Without it, the uncertainty sits more heavily on the trade.

Apple raised prices on multiple product lines on 26 June 2026, and the company’s executives were explicit about why: elevated memory and storage costs driven by the global AI-demand crunch, not discretionary margin expansion.

Apple characterised the price increases as “unavoidable,” tying them directly to a global memory-chip crunch fuelled by AI infrastructure demand.

On the day, Apple shares closed at $275.15, a decline of approximately 6%. The decline matters on two levels. First, Apple’s index weight means a 6% fall carries outsized impact on broad market benchmarks. Second, Apple sits at the intersection of the hardware stack and AI-enabled consumer devices. When its executives describe memory cost increases as unavoidable and attribute them to AI demand, the supply chain is communicating something concrete: AI infrastructure build-out is creating real, measurable cost pressure now visible in consumer-facing product prices.

Index concentration risk compounds this dynamic: the top five US companies now control roughly 30% of total market capitalisation, meaning Apple’s 6% decline carries a mechanical transmission effect on benchmark returns that is structurally larger than the weight of its fundamentals alone would justify.

| Company/Market | Event on 26 June | Transmission Mechanism |

|---|---|---|

| Apple | Price hike announcement; shares fell ~6% | Index weight decline; consumer cost pass-through signal |

| South Korean memory producers | Added to existing equity weakness | DRAM/NAND proxy for U.S. device-maker demand tightness |

| Broader AI hardware names | Sentiment contagion across the sector | Supply chain cost exposure to memory-chip crunch |

The geographic transmission was immediate. Apple’s Wall Street decline fed through to South Korean and other Asian memory-producer equities, which trade as proxies for DRAM/NAND market tightness. When the world’s biggest consumer electronics firm declares that memory costs cannot be absorbed, that message carries upstream through the entire supply chain.

The session’s sell-off hit AI names broadly, but the damage is not distributed equally. The distinction that matters most from here sits between two categories of AI exposure:

| AI Exposure Type | Valuation Driver | Sensitivity to Current Shocks |

|---|---|---|

| Infrastructure leaders (chipmakers, hyperscalers) | Near-term cash flows; measurable AI revenue on income statements | Relatively lower |

| Narrative/platform names (revenue-light AI software) | Future optionality; story-driven multiples | High |

Cash-generating AI infrastructure leaders already show substantial AI-related revenue in their earnings reports. Their valuations rest on near-term fundamentals, which provides a degree of insulation from pure discount-rate compression. High-multiple, revenue-light AI software and platform names carry the full force of rate-driven present-value compression and sentiment shifts like the IPO delay.

For a reader with mixed AI exposure, this distinction is the difference between holding a position that can re-rate on earnings and holding one that requires a sentiment catalyst that has just been delayed.

The expectations gap concept, drawn from Howard Marks and Aswath Damodaran, frames this distinction precisely: investment returns are driven by the difference between what a price already implies and what actually occurs, which is why the infrastructure-versus-narrative dispersion thesis matters more as a return driver than the direction of AI sentiment alone.

The correction may flush out excess speculation in narrative-heavy names while leaving infrastructure leaders to re-rate on fundamentals. But that thesis requires confirmation. Three signals will tell you whether the market is genuinely differentiating:

The Fed signal and the OpenAI IPO delay are the headlines, but they are not the complete picture. Regulatory scrutiny on AI safety, data, and competition is active across multiple major jurisdictions, and geopolitical risk remains concentrated in advanced-node semiconductor manufacturing in a small number of countries. Neither of these factors has a near-term resolution.

OpenAI’s path to translating frontier models into durable, margin-rich revenue at scale remains an open question rather than a solved problem.

This matters because the timeline compression affecting AI valuations today is not purely a function of Fed policy or one company’s IPO schedule. It reflects a broader regime in which multiple structural uncertainties are converging on the same window. Investors who frame today’s decline as a simple rates story may be underestimating how durable these headwinds are.

For readers wanting to assess whether today’s convergence of shocks represents a valuation correction or something more structurally significant, our deep-dive into AI stock bubble frameworks applies Minsky, Kindleberger, Sharma, and Shiller CAPE analysis to the current cycle, including the finding that major AI infrastructure investors are currently classified in Minsky’s speculative financing stage.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Rather than reacting to today’s headlines, here is a structured monitoring framework. Each signal tells you something specific, and each has a reading that would point toward either stabilisation or further deterioration:

This framework gives you a basis for forming your own view on timing rather than reacting to daily price moves.

Three converging shocks arrived on the same day, and together they revealed something the AI trade’s momentum had been obscuring: the macro environment supporting narrative-driven valuations has tightened, and a near-term sentiment catalyst has been removed.

What has not changed is the underlying structural case for AI infrastructure investment. Leading chipmakers and hyperscalers with measurable AI revenue are still generating durable cash flows. The correction does not invalidate the AI investment thesis.

But it does make clear that not all AI exposure is equal. Macro conditions are no longer a tailwind for the parts of the trade built on future promise alone. The five-signal framework above gives you a set of observable conditions to monitor, whether the correction deepens or stabilises, without prescribing a trade. The session’s message was not that AI is over. It was that the market just started charging for the distinction between what is real and what is still a promise.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AI stocks are long-duration assets whose valuations depend heavily on cash flows expected years or decades into the future. When discount rates rise, those distant cash flows compress sharply in present value, meaning revenue-light AI names with story-driven multiples absorb far more damage than companies generating substantial near-term earnings.

The delay removes one of the clearest near-term catalysts for an AI sector re-rating, leaving speculative positions exposed to macro headwinds with no sentiment anchor. The longer the listing is postponed, the more market perception risks shifting from a timing question to a fundamental reassessment of whether frontier AI models can generate durable, margin-rich revenue at scale.

Apple raised prices across multiple product lines and explicitly attributed the increases to elevated memory and storage costs driven by the global AI infrastructure demand crunch. The stock closed at $275.15, and its heavy index weighting meant the decline carried an outsized mechanical impact on broad market benchmarks.

AI infrastructure leaders, such as leading chipmakers and hyperscalers, already show measurable AI revenue on their income statements and their valuations rest on near-term fundamentals, providing insulation from discount-rate compression. Revenue-light AI software and platform names carry the full force of rate-driven present-value compression because their valuations depend entirely on future optionality and sentiment catalysts.

The article identifies five key signals: whether the 10-30 year Treasury curve is moving independently of policy rate expectations, OpenAI secondary market valuations, DRAM and NAND spot pricing trends, earnings revision divergence between infrastructure leaders and narrative-heavy names, and the progress of AI regulatory proceedings across major jurisdictions.