Who Really Runs a Public Company: Shareholders, Board or CEO?

18 mins ago

When a CEO walks out the door with a $20 million exit package, the instinctive reaction is outrage. Nine figures. Failure rewarded. Shareholders robbed. But here is the part that rarely makes the headline: most of that $20 million was equity the executive had already earned over years of employment, not cash invented by the board on the way out.

Golden parachutes are among the most misunderstood instruments in corporate finance. The gap between the public perception (a parting gift for incompetence) and the financial reality (a pre-negotiated contractual obligation) has direct consequences for you as a retail investor. When a CEO departure hits the news, the question is not whether the number sounds large. The question is whether it signals a governance problem or a manageable leadership transition.

Here is the framework for knowing the difference. After this, you will know exactly what questions to ask when a CEO departure is announced, where to find the actual contractual terms, and what those terms reveal about whether a company’s board is protecting shareholders or enriching executives.

The terms governing a CEO’s departure are established at the beginning of the employment relationship, not at its end. A golden parachute is a specific clause within an executive’s employment contract, agreed upon during the hiring process, that defines what happens financially if the board terminates the arrangement. By the time a payout makes headlines, the underlying agreement is typically years old.

The contract covers multiple components as a single integrated package:

Most CEO severance arrangements at large-cap companies are structured as 2-3 times base salary plus bonus for the cash component. For companies valued in the hundreds of billions, the cost of even a generous severance payment is typically lower than the financial harm from a protracted executive dispute that plays out in court filings and press coverage. Settling terms in advance also limits the risk that internal board deliberations surface through litigation, protecting the company’s reputation at a moment when it can least afford the distraction.

What this means for you: the board that approved the headline-grabbing payout was likely not the board that negotiated it. The governance accountability traces back to the compensation committee that set the original terms, sometimes years earlier. That is where your scrutiny belongs.

The headline number obscures the composition. When you break a golden parachute into its components and rank them by dollar size, the picture changes considerably.

Cash severance is the most visible component but rarely the largest. It is a multiple of base salary plus bonus. Accelerated equity vesting is where the real money sits. Stock awards granted over prior years, sometimes three to five years of accumulated grants, vest immediately upon the triggering event. Pro-rated bonuses cover the current-year bonus calculated through the departure date. Benefits continuation extends health and insurance coverage for a defined period. Consulting arrangements keep the departing executive engaged for a transition window. And restrictive covenants, specifically non-compete and non-solicitation clauses, represent what the company receives in exchange for the severance payment.

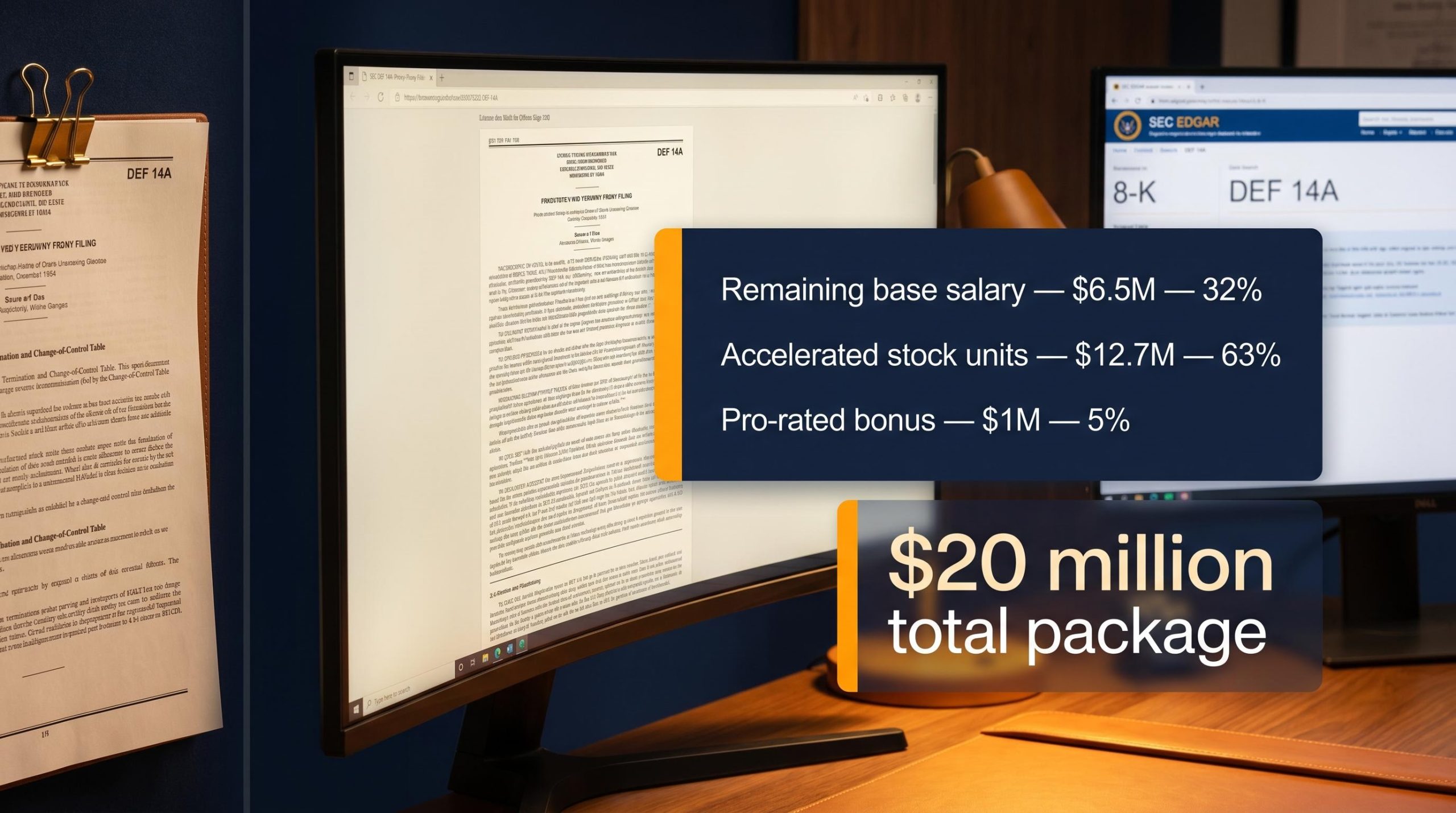

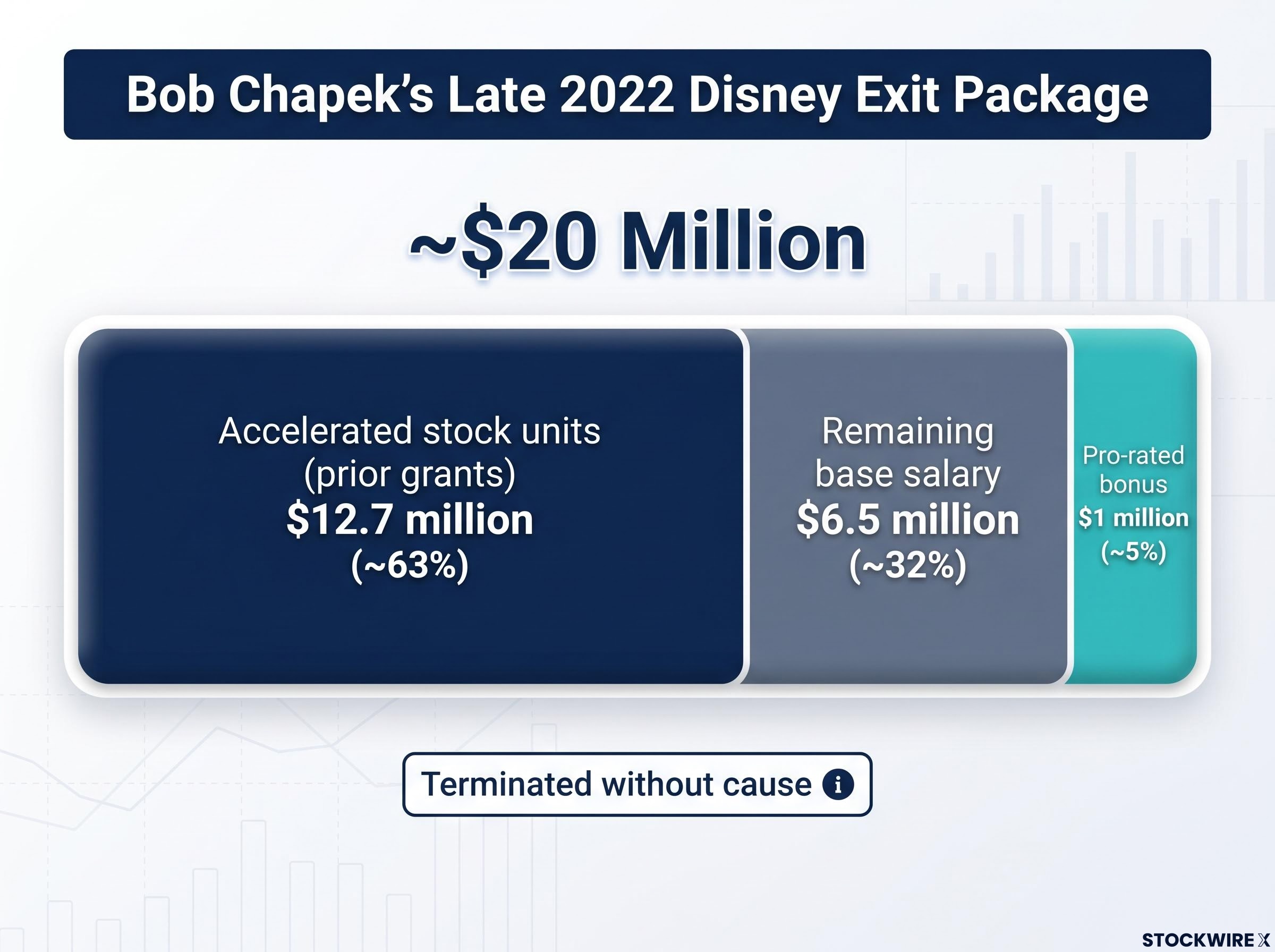

Bob Chapek’s exit from Disney in late 2022 is a useful illustration. His separation package totalled approximately $20 million.

| Component | Approximate Amount | Share of Total Package |

|---|---|---|

| Remaining base salary | $6.5 million | ~32% |

| Pro-rated bonus | $1 million | ~5% |

| Accelerated stock units (prior grants) | $12.7 million | ~63% |

Chapek was terminated without cause, which activated full severance benefits including equity vesting. The $12.7 million equity component, roughly 63% of the total package, was compensation already granted over prior years. It was not new money approved at the moment of his departure.

The compensation structures that produce large equity grant pools in the first place are themselves a product of the shareholder primacy doctrine, the framework that embedded stock-based pay as the dominant mechanism for aligning executive incentives with share price performance from the early 1990s onward.

When the bulk of a golden parachute’s headline figure represents equity that accumulated over multiple years of employment, it is a fundamentally different event from a board writing a large discretionary cheque on the way out. The key analytical question is always: what share of that total was already earned, and what share is genuinely new?

A $20 million package is very different analytically when $13 million of it is equity earned over five years than when $13 million is new cash approved by the board after a poor tenure. Decomposing the structure removes the emotional distortion of the headline.

There is a genuine shareholder-alignment case for golden parachutes, and understanding it gives you a more analytically complete picture than the “pay for failure” narrative alone.

The most important function is the change-of-control provision. A CEO whose employment would end the moment an acquisition closed has a direct personal incentive to oppose or delay that transaction, regardless of its merits for shareholders. Severance protection neutralises that incentive by decoupling the CEO’s financial outcome from the deal’s outcome. With their own position secured contractually, they can assess a takeover offer on what it actually delivers for the company’s owners rather than on what it costs them personally.

The “without cause” and “change of control” categories drive the largest and most visible payouts. Understanding the four main termination categories tells you what triggers payment and what does not:

The alignment logic has a well-documented counterpart. CEOs with excessively rich change-of-control provisions can become too deal-friendly, supporting acquisitions that are only marginally value-creating because the transaction triggers their severance windfall. This is a known misalignment pattern actively monitored by governance analysts and proxy advisory firms including ISS and Glass Lewis.

The primary lever for avoiding this outcome is compensation committee discipline in setting the original terms. When you see a change-of-control provision in a CEO’s contract, its existence is not inherently problematic. But its size and structure relative to the company’s deal-making history tells you something important about whether the board has balanced shareholder protection against executive enrichment.

Proxy advisory firms including ISS and Glass Lewis have made board alignment signals a standard part of their annual governance reviews, assessing not just whether directors hold equity but whether that equity was purchased with personal capital or simply received as compensation.

Golden parachutes operate within a system of imperfect but real constraints. Significant checks exist, and the full contractual terms are accessible to any investor willing to look for them.

Internal Revenue Code Section 280G creates a structural financial disincentive for excessive packages. Payments exceeding three times an executive’s average annual compensation over the preceding five years trigger two consequences: an excise tax on the executive and a loss of tax deductibility for the company. Many packages are deliberately structured to avoid crossing this threshold.

The IRC Section 280G excise tax threshold operates as a structural cap: payments exceeding three times an executive’s five-year average compensation trigger both an excise tax on the executive and a loss of corporate tax deductibility, which is why compensation committees engineer packages to land just below that boundary.

The IRS built a financial disincentive for excessive parachute payments directly into the tax code. That is why many packages are carefully structured just below the 280G threshold, and it is why a package that appears to approach or cross it is a governance signal worth investigating.

The Dodd-Frank Act introduced mandatory shareholder advisory votes on executive compensation (“say-on-pay”) and requires disclosure of golden parachute arrangements in merger proxy filings. These votes are non-binding but create reputational pressure on boards and compensation committees. Significant opposition votes have historically prompted boards to revise compensation structures.

If you want to find the full terms yourself, the path is straightforward:

Knowing these specific filing types and where to find them converts passive headline consumption into active research capability.

CEO departures at large public companies are not the crises they appear to be in news coverage. They are pre-rehearsed sequences with multiple internal teams coordinating before the announcement reaches the public.

Key internal stakeholders across legal, communications, and investor relations functions are brought into the process well before the CEO’s departure is formally communicated. Announcements are timed for outside market trading hours so that all investors receive the news at the same moment, reducing the scope for information asymmetry to drive volatility. A named successor, whether permanent or serving in an interim capacity, is typically included in the same announcement to reinforce business continuity. When Chapek departed Disney, Bob Iger was confirmed as his replacement within the same public statement.

Once access protocols are activated, the outgoing executive is cut off from sensitive internal systems and forward-looking strategic information. For the wider workforce, the experience is largely unremarkable: an internal communication from the board, a name change at the top of the organisation chart, and then the ordinary rhythm of the working day resumes. The impact on customers is typically even smaller. Companies including Apple, Microsoft, Starbucks, Disney, Nike, and Intel have each navigated CEO transitions while their operations continued without interruption.

The degree of operational preparation visible in a departure announcement is itself a governance signal. Companies that have clearly planned for the contingency are demonstrating the kind of board-level foresight that should reassure, not alarm, investors.

A well-managed transition looks like paired successor identification, off-hours timing, and coordinated stakeholder communications. The warning signs of a poorly managed one are different:

These are the signals you should treat as genuinely concerning, independent of the severance dollar amount.

The severance number is the least predictive variable in a CEO departure for subsequent stock performance. The investor who asks the right questions is operating with a materially more complete picture than the one who stops at the headline.

Here are the six questions to apply the next time a CEO departure appears in your portfolio holdings:

Proportionality changes everything about how a number reads:

| Package Size | Company Market Cap | Proportion of Market Value |

|---|---|---|

| $20 million | $200 billion | 0.01% |

| $20 million | $10 billion | 0.2% |

| $20 million | $500 million | 4.0% |

A $20 million package is a rounding error at a $200 billion company and a material event at a $500 million company. Governance analysts assess small-cap and large-cap norms differently for exactly this reason. The raw dollar figure without context is not analytically meaningful.

Succession quality is the variable that drives post-transition stock performance. The severance cheque tells you about the contract, not the company’s future.

Succession quality at Berkshire is visible in the structured handover Greg Abel received, with capital allocation continuity clearly communicated and nearly $400 billion in reserves positioned as a deployment mandate rather than a management uncertainty, a contrast to transitions where successor strategy is left ambiguous at the moment of announcement.

This framework converts an emotionally loaded corporate event into a structured analysis. That is the difference between a reactive decision and an informed one.

Golden parachutes are contractual instruments whose primary purpose is to maintain organisational stability through leadership transitions. The dollar amounts attached to them reflect prevailing market norms for executive compensation at a company of a given scale, not a board’s assessment of the departing CEO’s performance. The agreement was drafted and signed long before any departure was contemplated. The equity component had been accumulating through regular grant cycles. The compensation committee responsible for the original terms may itself have been replaced several times over by the time the exit became public news.

The governance signals that carry genuine predictive weight are compensation committee discipline, prior say-on-pay vote results, tightness of “for cause” definitions, and succession planning quality. Those are the variables worth your time. The headline dollar figure is context about the employment contract, not a signal about where the stock goes next.

For investors wanting to understand how board quality affects long-run share price outcomes beyond the departure event itself, our full explainer on governance and post-transition valuation examines the specific mechanisms through which compensation committee discipline and management communication shape how markets price a company across its first several years of scrutiny.

Retail investors who understand the mechanics of executive departures are better positioned to assess risk at the moment the market is most likely to overreact to a number. Most public reaction focuses on the payout. You now have the framework, the filing locations, and the six questions that separate an informed assessment from a headline-driven one.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

—

A golden parachute is a clause in a CEO's employment contract, negotiated at the start of the relationship, that defines the financial terms if the board terminates the arrangement. It typically includes cash severance, accelerated equity vesting, and benefits continuation, with the equity component often representing the largest share of the total package.

The two triggers that produce the largest payouts are termination without cause and change of control. Voluntary resignation or termination for cause (such as misconduct or fraud) results in reduced or eliminated severance benefits, while a without-cause termination or acquisition activates full severance including accelerated equity vesting.

Search the SEC's EDGAR database for the company's most recent 8-K filing around the departure date for initial disclosure, then locate the DEF 14A proxy statement for the full termination and change-of-control tables, which itemise every component including equity vesting schedules and restrictive covenants.

IRC Section 280G penalises excessive parachute payments by imposing an excise tax on the executive and removing corporate tax deductibility when total payments exceed three times the executive's average annual compensation over the preceding five years. Compensation committees routinely structure packages to land just below this threshold to avoid triggering both penalties.

The warning signs of a poorly managed transition are: no successor named at announcement, disclosure during a live trading session, conflicting board statements in subsequent days, and unexplained shifts in how the departure is characterised. These operational signals carry more predictive weight for stock performance than the dollar size of the severance package.