In 1970, Milton Friedman published a newspaper op-ed arguing that a corporation has no social responsibility beyond one obligation: making money for its shareholders. That single argument, dressed up as economic common sense, went on to rewire how American businesses are run, how executives are paid, and who gets to benefit when a company succeeds.

Shareholder primacy is not a law. It is not enshrined in the U.S. corporate code. It is a doctrine, a set of ideas that became institutional habits, and those habits now shape decisions from the boardroom to the factory floor. With the Business Roundtable’s 2019 stakeholder pledge still debated and S&P 500 buybacks hitting $942.5 billion in 2024, the doctrine’s grip on American corporate behaviour is as relevant as ever for investors, analysts, and anyone trying to read a company’s true priorities.

This explainer traces how shareholder primacy took hold, what mechanisms it operates through, what it costs workers and communities in concrete terms, and what the current governance landscape actually looks like for long-term investors assessing corporate health.

The idea that changed corporate America: Friedman’s 1970 doctrine

What executives believed before Friedman

Before the doctrine arrived, the postwar American corporation operated under a different theory of legitimacy. Executives saw themselves as trustees of institutions that owed obligations to employees, suppliers, communities, and shareholders alike. This was not altruism. It was a model built on the premise that long-term corporate durability depended on balancing multiple constituencies, and that a company which neglected its workers or its town would eventually lose its capacity to generate returns at all.

The argument that displaced it

Then came Friedman’s 1970 New York Times op-ed. Its claim was blunt: a corporation’s sole social responsibility is to increase profits for its owners, and any executive who diverts resources to social goals is spending someone else’s money.

“There is one and only one social responsibility of business: to use its resources and engage in activities designed to increase its profits so long as it stays within the rules of the game.” — Milton Friedman, The New York Times, 1970

This was a normative argument, not a legal mandate. No statute required companies to maximise shareholder value above all other considerations. The doctrine’s power came from adoption, not legislation. Over the following two decades, business schools taught it as orthodoxy, compensation consultants built pay packages around it, and institutional investors demanded it. Legal scholar Lynn Stout later argued that the doctrine rested on assumptions about corporate purpose that were never tested against legal reality, yet by the time that critique gained traction, the habits were already embedded.

When big ASX news breaks, our subscribers know first

How stock-based pay turned doctrine into daily behaviour

An idea published in a newspaper does not, on its own, change how companies operate. The transmission mechanism was compensation. Tying executive pay predominantly to share price performance converted Friedman’s intellectual argument into a personal financial incentive sitting on every CEO’s desk.

Stock options and equity grants create a direct link: when the share price rises, executives’ personal wealth increases. That structure makes workforce reductions, factory closures, and wage suppression rational choices under the doctrine’s logic, because each reduces short-term costs and lifts near-term profitability metrics. Lynn Stout described this short-termism as a structural outcome of the incentive design itself, not an aberration.

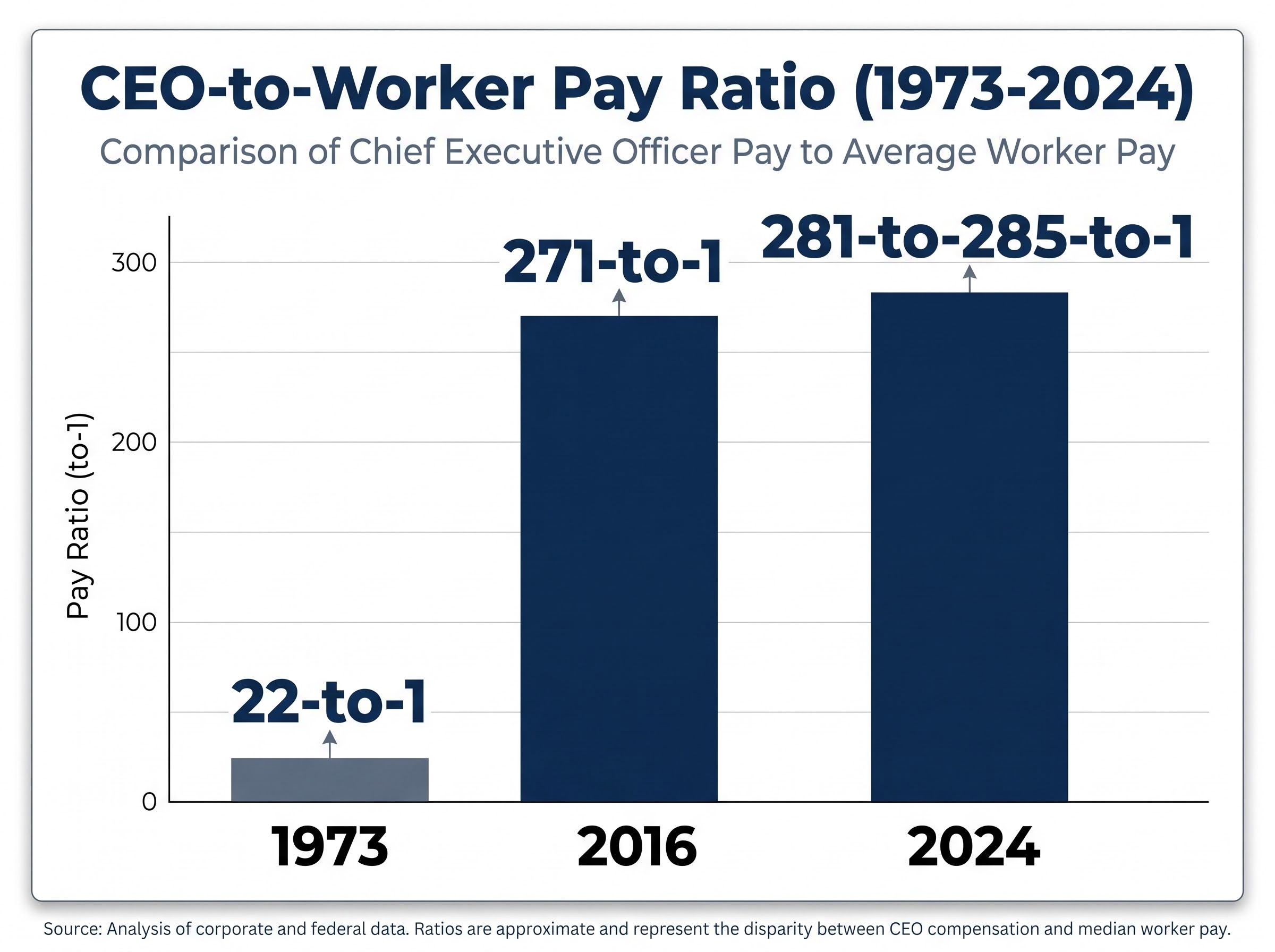

The pay ratio tells the story in a single number.

| Year | CEO-to-Worker Pay Ratio | Source |

|---|---|---|

| 1973 | 22-to-1 | Historical benchmark |

| 2016 | 271-to-1 | EPI / AFL-CIO data |

| 2024 | 281-to-285-to-1 | EPI (281-to-1); AFL-CIO Executive Paywatch (285-to-1) |

That ratio is not just a political talking point. For long-term investors reading compensation disclosures, it serves as a proxy for how aggressively a company distributes productivity gains upward rather than reinvesting them. A ratio that has climbed from 22-to-1 in 1973 to 281-to-285-to-1 in 2024 reflects a capital allocation philosophy, one that stock-based pay structurally reinforces every quarter.

EPI CEO pay research places the 2024 ratio at 281-to-1, part of a long-run dataset showing the figure stood at just 21-to-1 in 1965, giving investors a five-decade baseline against which to assess whether any given company’s compensation structure sits at the aggressive or restrained end of the spectrum.

The Wausau Paper closure: shareholder primacy with a human address

The doctrine becomes harder to treat as an abstraction once it has an address. In 2012, the Wausau Paper Company Brokaw Mill in Wisconsin provided one.

The mill’s management had a long-term plan: convert the facility from printing paper production to tissue paper manufacturing, a strategic pivot designed to keep the operation viable as demand for printing paper declined. Then a hedge fund acquired a significant stake in the company and pressured management to prioritise dividend increases instead. The conversion was abandoned. The mill was closed. Approximately 450 workers lost their jobs, with the closure announced for 31 March 2012. The surrounding communities that depended on the facility absorbed the impact alongside them.

Hank Newell, an executive at Wausau Paper, described the conflict directly: the tension between stakeholder-oriented long-term planning and shareholder-driven short-term demands was not theoretical. It was the daily operating reality of managing a company whose strategic direction had been overridden by capital return pressure.

Workers affected by the closure described the personal toll in concrete terms: lost wages, disrupted families, and a community that lost its largest employer in a single board decision.

For investors, the Wausau Paper case is a template. The pattern of stake acquisition, dividend or buyback pressure, and strategic plan reversal repeats across industries. Recognising that pattern early is a meaningful edge in evaluating activist targets.

The Lululemon governance conflict illustrates the same pattern with a more recent timestamp: activist fund intervention, in this case Elliott Management using a universal proxy card to target specific board seats, followed by a violent market reaction to a leadership decision made without apparent investor buy-in, producing a 12% single-session drop that reflected structural loss of confidence rather than any single operational miss.

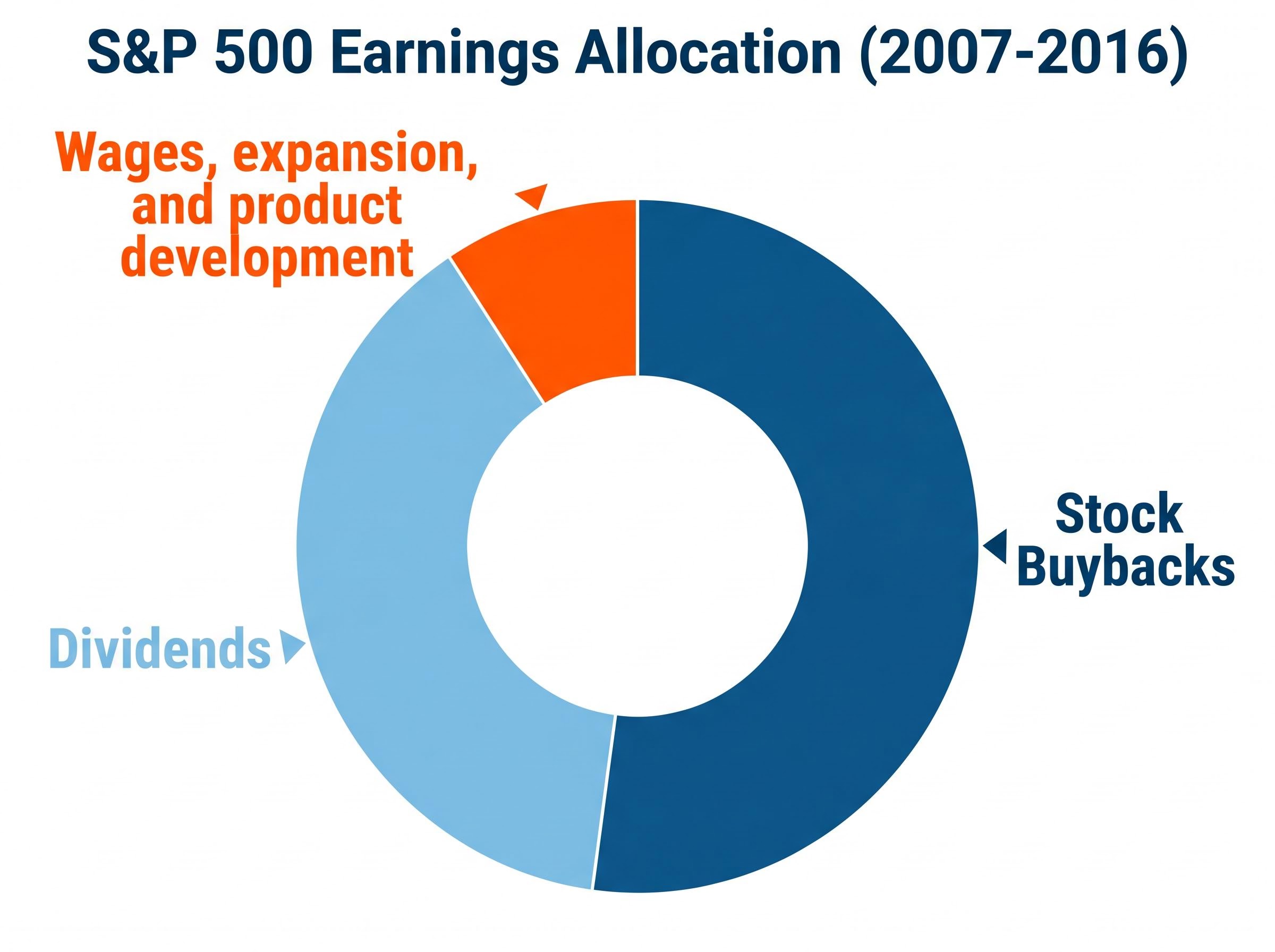

Where the money actually goes: buybacks, dividends, and the capital allocation ledger

Between 2007 and 2016, S&P 500 companies directed their earnings according to a pattern that reveals the doctrine’s priorities more clearly than any corporate mission statement:

- Stock buybacks: More than 50% of total earnings

- Dividends: Approximately 39% of total earnings

- Wages, expansion, and product development: Less than 10% of total earnings

Stock buybacks work by reducing the number of shares outstanding, which inflates earnings per share and pushes up the share price without any underlying improvement in the business. This is precisely why they are the preferred shareholder-value tool: they deliver the metric that stock-based compensation rewards.

The distinction between buybacks and dividends matters less than it might appear at the capital allocation level: both are mechanisms for returning cash to shareholders rather than reinvesting it, and the case for treating dividends and total return as the correct unit of analysis, rather than yield alone, has significant implications for how investors read a company’s actual growth ambitions.

S&P 500 companies repurchased $942.5 billion in shares during 2024, according to S&P Dow Jones Indices data published in March 2025, a figure confirmed by the Wall Street Journal as a record-high annual pace.

Why the 1% excise tax did not change the math

The Inflation Reduction Act’s 1% excise tax on corporate share repurchases has been in effect since 2023. At 1%, the tax is small relative to the earnings-per-share boost, the signalling value, and the capital-return benefits companies associate with buybacks. S&P Dow Jones Indices and Reuters analysis both confirmed no material decline in repurchase activity after the tax took effect. The 2024 total of $942.5 billion speaks for itself.

One further dimension sharpens the picture: fewer Americans hold stock market investments than at any point in the prior two decades. That concentration means buyback-driven market gains flow to a narrower share of the population, widening the gap between the doctrine’s beneficiaries and everyone else.

That concentration dynamic compounds at the macro level: buyback-driven index returns flow primarily to existing asset holders, and the feedback loop between wealth concentration and asset price inflation has been documented as self-reinforcing, with the top 10% capturing roughly 88% of total U.S. wealth growth between 2020 and 2024 according to Federal Reserve data.

The Business Roundtable’s stakeholder pledge and why it changed less than it promised

In August 2019, the Business Roundtable issued its Statement on the Purpose of a Corporation, formally committing 181 major U.S. company CEOs to serving all stakeholders, not shareholders alone. The announcement was treated as a genuine inflection point. Headlines framed it as the end of the Friedman era.

What the governance landscape actually looks like in 2025

The statement remains formally in place. What it has not produced is a binding governance framework to replace shareholder primacy in practice. The Harvard Law School Forum on Corporate Governance, in 2024-2025 commentary, characterised the statement as increasingly a symbolic benchmark rather than a live constraint on corporate decision-making.

The Harvard Law School Forum on Corporate Governance has documented how the 2019 statement produced no binding enforcement architecture, leaving individual boards free to continue prioritising capital return to shareholders whenever financial pressure or activist positioning made that the path of least resistance.

Three structural factors explain why the pledge has not displaced the doctrine:

- No binding governance mechanism. The statement committed signatories to a purpose, not to a set of enforceable rules. Boards retained full discretion over capital allocation, and that discretion continued to flow toward buybacks and cost restructuring when financial pressure arose.

- Activist hedge fund pressure. Reuters reported in 2024-2025 that activist funds continued to push boards toward buybacks, cost cuts, and asset sales, reinforcing shareholder primacy in the same boardrooms where the pledge was signed.

- Anti-ESG political backlash. The Brookings Institution described the U.S. governance environment as one in which ESG had become more contested, with shareholder-value arguments regaining force amid higher interest rates, index-fund voting debates, and corporate pullback from public ESG commitments.

ESG language persists in disclosures. Shareholder primacy persists in practice. The gap between the two is where the current governance equilibrium sits.

What shareholder primacy means for how you read a company

The doctrine is not a villain in a story. It is a structural feature of American corporate governance, and understanding it gives investors a more accurate model for reading company behaviour.

A company’s capital allocation pattern reveals more about its actual governance priorities than its stated values or ESG disclosures. Three diagnostic questions sharpen the picture:

- What share of free cash flow goes to buybacks versus capital expenditure? A company directing the majority of free cash flow to repurchases is making a bet that there are no better internal uses of that capital. That is sometimes the right call. It is also sometimes a signal that management has run out of growth ideas.

- How is CEO pay structured relative to long-term performance metrics? A compensation package tied overwhelmingly to short-term share price targets tells investors exactly which time horizon the executive is optimising for.

- Is an activist fund holding a significant stake? Activist positioning is one of the most reliable leading indicators of near-term capital allocation shifts toward buybacks, dividend increases, or asset sales.

The CEO pay ratio, from 22-to-1 in 1973 to 281-to-285-to-1 in 2024, is a single-number diagnostic for how the doctrine has shaped capital flows over five decades. The $942.5 billion in 2024 buybacks is the scale at which those flows operate today.

The debate between shareholder primacy and stakeholder governance is not resolved. Its outcome is a live governance risk factor for long-term investors, because the model a company operates under shapes its capacity to sustain competitive advantage, retain talent, and absorb disruption.

The doctrine survives its critics, and what that tells investors

Shareholder primacy has survived Friedman’s academic critics, the 2008 financial crisis, the 2019 Business Roundtable statement, the ESG wave, and a federal excise tax. It endures not because it is legally mandated, but because the incentive structures that embed it, stock-based pay, activist fund pressure, and buyback-driven earnings management, remain largely unchanged.

The current regulatory debate over the quarterly reporting cadence adds a further layer: the SEC’s 2026 proposal to let eligible companies switch to semiannual filings would extend the information gap between insiders and outside investors, a change critics argue would make it harder to detect the kind of short-termism that stock-based compensation already incentivises.

The stakeholder model raises legitimate questions about long-term corporate resilience. It has not yet produced the governance mechanisms needed to displace buyback-driven capital allocation in practice. That gap between rhetoric and structure is itself the most important thing for investors to understand.

In the current environment, reading corporate governance accurately means understanding the doctrine first, then evaluating how any given company operates within or against it. The balance sheet will tell investors more than the mission statement.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.