Goldman Stress Test: KOSPI Already Priced for Worse Than GFC

4 mins ago

Overseas investors have now offloaded a cumulative 157.50 billion won in KOSPI shares this year, yet Goldman Sachs is reading that same selling pressure as a reason to look at South Korean stocks more closely, not less.

Goldman’s Korea Equity Risk Barometer (GSSRKERB) registered -1.5 for the week ending 3 July 2026, a level the bank places firmly in what it calls risk-averse territory, and one it treats as a contrarian indicator pointing toward better prospective returns. The barometer is designed to flag moments when sentiment and positioning have become so depressed that the marginal seller has likely already acted, shifting the asymmetry of outcomes toward the upside. That reading lands against a backdrop of rising bond yields, a modestly firmer won, and domestic investors partially absorbing what foreign hands are selling.

Here is what the signal actually claims, what it does not, and how the macro and flow picture around it should shape the way different types of investors approach Korea right now.

The GSSRKERB is a contrarian sentiment and positioning indicator, not a price target or a timing tool. A reading of -1.5 reflects a market state where risk-averse positioning is so entrenched that further bad news has a diminishing incremental impact on prices. Goldman itself stresses that contrarian tools are most useful “when meaningful market moves have already occurred.”

“More constructive equity market returns on a prospective basis.” — Goldman Sachs characterisation of the GSSRKERB signal

That language is precise. “More constructive” and “prospective” signal improved probability, not certainty. The -1.5 reading tells you the asymmetry has shifted: a positive surprise could move the market more than an equivalent negative one would, because much of the bad news is likely already reflected in prices.

Goldman sentiment indicators across different markets operate on the same underlying logic: when positioning becomes stretched enough that further bad news produces diminishing price impact, the asymmetry of prospective returns shifts, a principle Goldman applied to the US Equity Sentiment Indicator reaching 1.7 and now applies through the GSSRKERB to Korean equities.

What the barometer does say:

What it does not say:

Understanding the barometer’s logic is the prerequisite for deciding whether it changes your Korea positioning at all. Treat it as a probabilistic edge, not a green light.

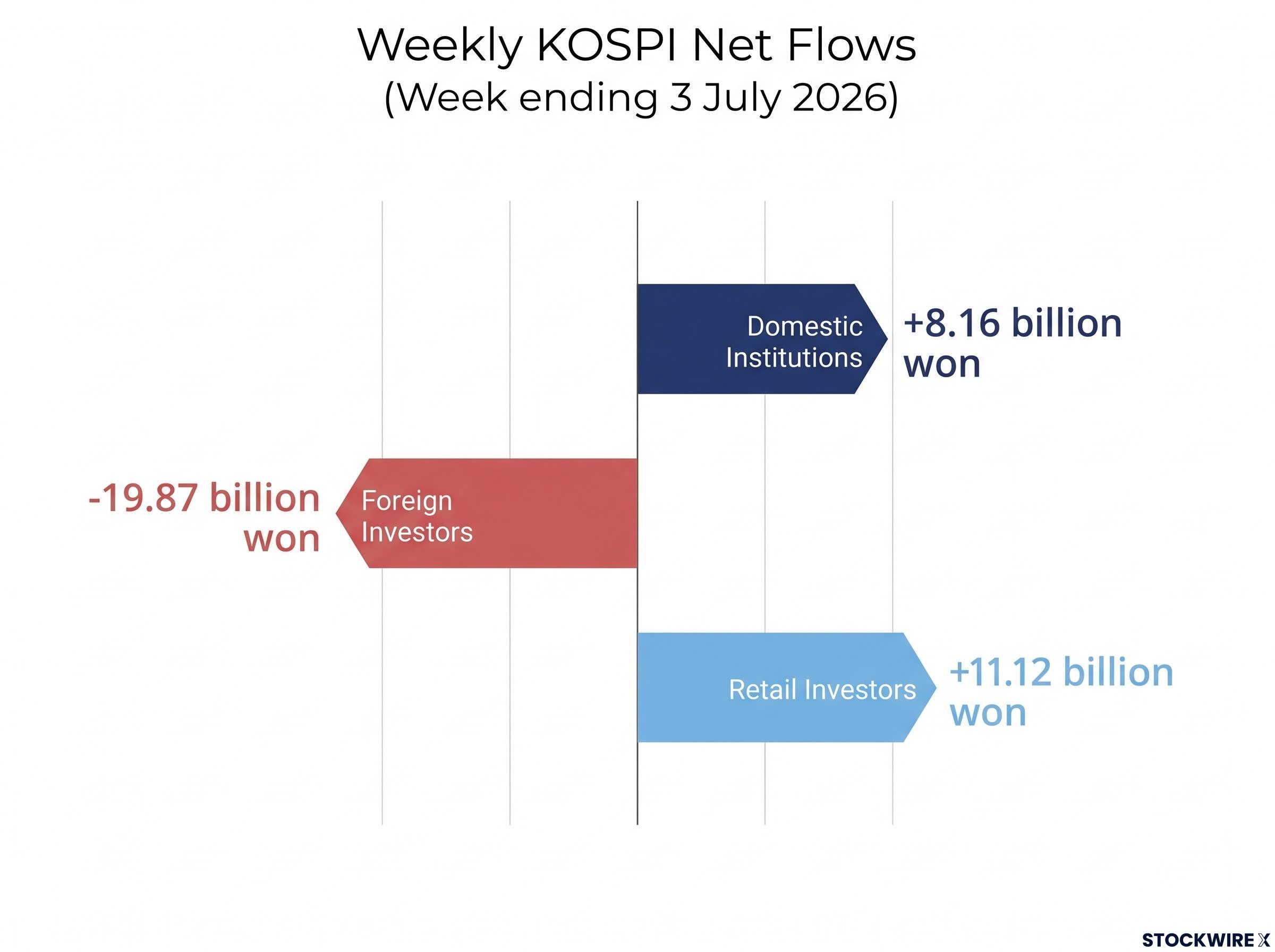

Year-to-date foreign net selling on the KOSPI has accumulated to 157.50 billion won, of which roughly 19.87 billion won landed in the single week ending 3 July 2026. Outflows during that week were skewed heavily toward technology, reflecting the concentration risk embedded in the index through heavyweights such as Samsung Electronics and SK Hynix.

| Investor Category | Weekly Net Flow (billion won) | Direction |

|---|---|---|

| Foreign Investors | -19.87 | Net Seller |

| Domestic Institutions | +8.16 | Net Buyer |

| Retail Investors | +11.12 | Net Buyer |

The selling is concentrated and flow-driven. That distinction matters because it suggests a market in transition rather than freefall.

For the week, domestic institutions added 8.16 billion won on a net basis, while retail participants contributed a further 11.12 billion won in net purchases. Combined, those two groups provided a meaningful counterweight to foreign outflows, though the offset remains partial rather than complete. The gap between foreign selling and domestic buying is where the barometer’s risk-averse reading originates: positioning remains stretched, but not unopposed.

Korea has cycled through this pattern before. In 2024-2025, foreign institutions sold roughly $28 billion of Korean stocks during a period of political uncertainty, then became net buyers of approximately $6 billion over three months as reform expectations improved. The reversal was sharp, but it did not happen on sentiment alone.

Three conditions preceded that recovery, and each is worth checking against the current environment:

Korea’s structural valuation discount, driven by chaebol governance structures, weak payout culture, and a persistent geopolitical risk premium, has historically been one of the primary reasons foreign capital demanded a higher return hurdle before committing to the market, and governance reform progress under the Corporate Value-Up programme represents the most direct policy lever for compressing it.

The AI trade meltdown offers a more granular precedent. A near-10% KOSPI drop was amplified by dealer hedging, leveraged ETF rebalancing, and margin liquidation.

The forced selling mechanics that amplified the AI trade meltdown, including margin call liquidations, daily-rebalancing leveraged ETF selling, and passive index-tracker redemptions, followed the same self-reinforcing pattern that Goldman estimated could push hedging and rebalancing flows in Samsung and SK Hynix above 20% of average daily volume during stress periods.

Goldman estimated that hedging and rebalancing flows in Samsung and SK Hynix could exceed 20% of average daily volume during stress periods.

Margin loans reached approximately $26 billion during that episode, with forced liquidations hitting 4-5% of brokerage receivables. Once that mechanical selling exhausted itself, the market found a new equilibrium with lighter positioning and lower expectations. History tells you that flow-driven dislocations in Korea have repeatedly created recoverable entry points, but only when fundamentals eventually cooperated. The precedent is useful, not automatic.

The barometer flashes opportunity, but it does so in a more expensive cost-of-capital environment than prior Korean recovery phases. That is why Goldman’s own language reads as constructive but cautious rather than outright bullish.

Three macro variables frame the complication:

| Bond Maturity | Yield | Equity Implication |

|---|---|---|

| Three-year | 3.75% | Raises near-term discount rates for growth equities |

| Ten-year | 4.20% | Creates a competing asset for domestic institutional capital |

The macro backdrop means the barometer’s probabilistic edge operates against a higher cost-of-capital baseline than investors saw in previous Korean recoveries, which changes the risk-reward calculus depending on base currency and time horizon.

The barometer makes a probabilistic claim. The data arriving over the next several weeks will either confirm or undermine it. Four domains are worth monitoring:

The FSC regulatory reforms for foreign investment, including the phased removal of Korea’s investment registration requirement and expanded English disclosure obligations for KRX-listed securities, form part of the structural backdrop against which governance progress is now being assessed by foreign allocators.

If foreign flows begin to moderate while yields stabilise and earnings hold, the barometer’s probabilistic edge starts to look like a genuine setup rather than a premature call.

The GSSRKERB at -1.5, set against 157.50 billion won in year-to-date foreign selling and a ten-year yield at 4.20%, does not produce a single answer for every investor. It produces a probability shift that different investor types should weight differently:

Institutional position management on the KOSPI during 2026 has involved competing signals from major banks, with JPMorgan and Goldman Sachs raising targets to 9,000 while Citigroup cut half its long position in May, citing overbought signals and elevated global rate risks, a split that illustrates why the contrarian barometer reading does not resolve to a single institutional view.

The signal is real. How much it changes your positioning depends entirely on your base currency, time horizon, and tolerance for continued volatility.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Goldman Sachs Korea Equity Risk Barometer (GSSRKERB) is a contrarian sentiment and positioning indicator that flags when risk-averse positioning in South Korean stocks has become so entrenched that the marginal seller has likely already acted, shifting the asymmetry of prospective returns toward the upside. It is not a price target or a precise timing tool.

A reading of -1.5 places the KOSPI firmly in Goldman's risk-averse territory, meaning much of the bad news is likely already reflected in prices and a positive surprise could move the market more than an equivalent negative one would. Goldman characterises this as pointing toward more constructive equity market returns on a prospective basis, though the signal is probabilistic rather than a guarantee of near-term gains.

Foreign investors have accumulated net selling of 157.50 billion won on the KOSPI year-to-date as of the week ending 3 July 2026, with roughly 19.87 billion won of that total occurring in that single week, skewed heavily toward technology names such as Samsung Electronics and SK Hynix.

The four key indicators to watch are: a moderation or reversal in cumulative foreign net selling from 157.50 billion won, a subsiding of forced liquidations and leveraged ETF rebalancing, stabilisation of the ten-year Korean government bond yield around 4.20%, and earnings stability in the semiconductor and export sectors that historically converts a sentiment washout into sustained foreign re-engagement.

Korea's ten-year government bond yield at 4.20% creates a credible competing asset for domestic institutional capital and raises the discount rate on growth-oriented tech stocks, meaning the barometer's probabilistic edge operates against a higher cost-of-capital baseline than investors faced in previous Korean recovery phases.