Why SMSF Trustees Hold Twice the Cash of Professional Funds

3 mins ago

Australian retail investors are not making random mistakes. They are making the same four mistakes, in the same order, for structural reasons that are unique to this market.

No other developed equity market combines the ASX’s bank and resource concentration with a government-designed dividend incentive system that shapes investor behaviour the way franking credits do. The mistakes feel rational here because the market is designed in a way that makes them feel rational.

Here is how to identify which of these four traps you are currently sitting inside, what the disciplined alternative looks like in practice, and how to build the structural habits that stop the pattern from repeating. Think of this as a diagnostic, not a lecture.

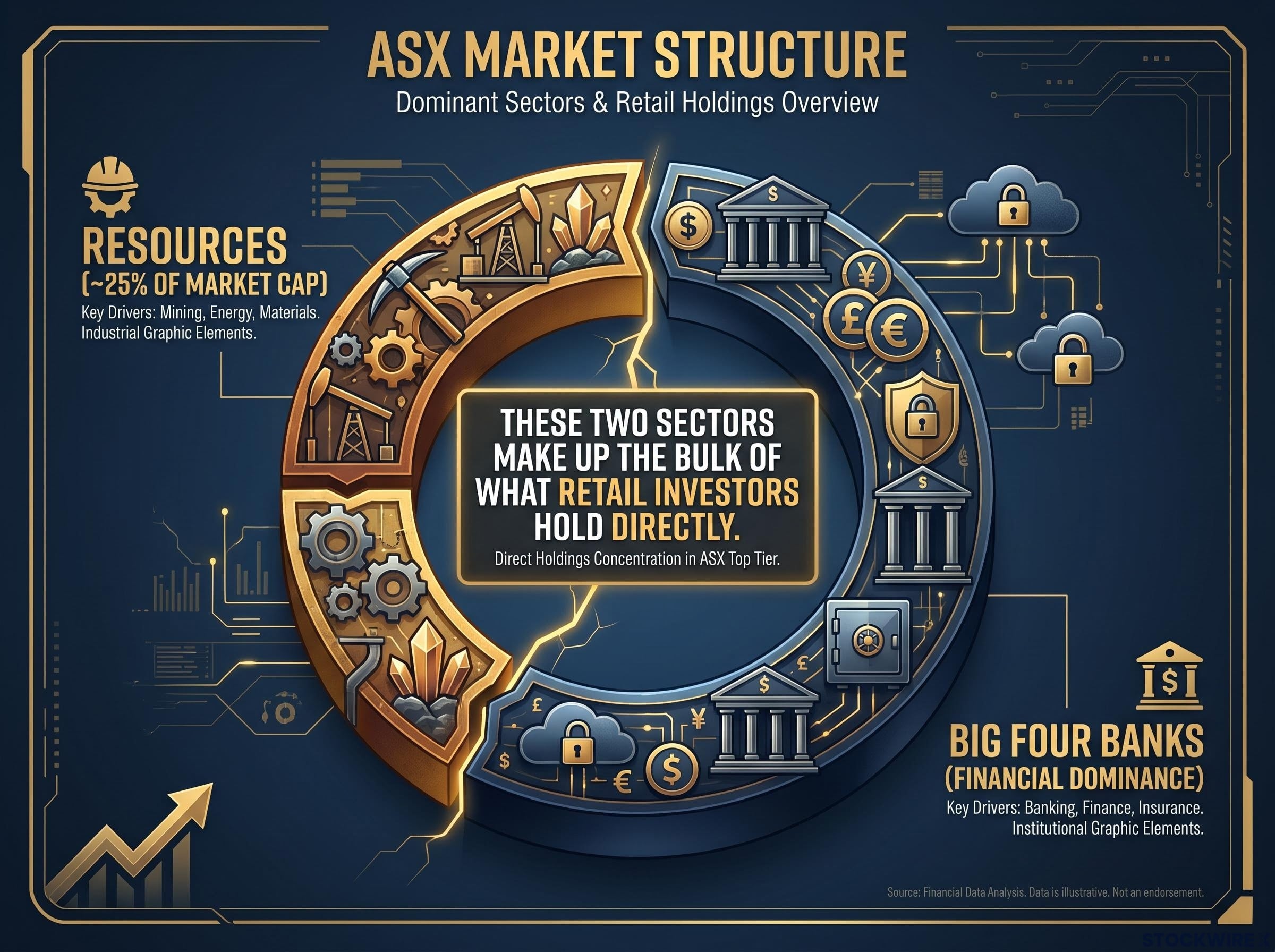

The ASX is not shaped like most developed equity markets. Resources account for approximately 25% of market capitalisation. The big four banks dominate the financial sector. Together, these two sectors make up the bulk of what retail investors hold directly.

That concentration creates a portfolio shape that pushes investors toward specific behavioural patterns:

These two structural conditions set up the four traps that follow. They are not personal failures. They are predictable outcomes of investing in a market designed the way the ASX is. Understanding that distinction is the first step to resisting them, because an investor who sees the market design behind their own behaviour is far better positioned to change it than one who is simply told they are wrong.

Franking credits deliver genuine after-tax value to investors who can fully utilise them: retirees in pension phase, those in lower tax brackets, and anyone whose tax position turns a franked dividend into a materially better return than the headline yield suggests. That advantage is real.

The PBO dividend imputation explainer confirms that the cash refund mechanism is most valuable to investors whose franking credits exceed their total tax liability, a category that disproportionately includes retirees in pension phase rather than working-age accumulators building wealth over a long time horizon.

The problem is cultural spillover. Investors across all life stages and tax situations now treat high-yield, high-franking stocks as inherently superior holdings, regardless of whether their personal tax position benefits from the structure. Yield has become cultural gospel in a way that no other developed market replicates.

The misapplication starts with a misunderstanding of franking credit mechanics: zero-tax investors and SMSFs in pension phase receive the full credit as a cash refund from the ATO, while investors at the top marginal rate extract far less value from the same dividend, meaning the same holding produces materially different after-tax outcomes depending entirely on the holder’s tax position.

“High yield is not the same as high return.”

Stocks advertising unusually elevated yields frequently fail to deliver. A high yield often reflects a falling share price rather than a rising or sustainable dividend. On the ex-dividend date, the share price routinely drops by an amount that erodes or eliminates the income received, because holders who bought purely for the payout exit once it is captured. The net result is income received alongside a capital loss that offsets it. Yields above 10% warrant serious scepticism: either the forecast payout will not be delivered, or the price has already fallen far enough to create the appearance of yield without the substance of return.

High payouts also reflect limited reinvestment opportunity. Companies returning the bulk of their earnings to shareholders have less capital available to compound internally. For investors still building wealth, this is a direct drag on long-term outcomes.

The distinction between income strategy and growth strategy is the foundational decision you need to make before selecting any individual holding. Blending them without intention is where portfolio damage begins.

If you are still in the accumulation phase and hold several high-yield ASX names “for the income,” that strategy deserves interrogation. The question is whether you are optimising for your actual tax position and life stage, or following a cultural assumption that was never designed for your situation.

The ASX’s concentration in both banks and resources creates a deceptive symmetry. Investors who understand, correctly, that they can hold the major banks through cycles then apply the same logic to resource companies. This is a category error, and it is the single most common misapplication of investment strategy among Australian retail investors.

| Attribute | Banks | Resource companies |

|---|---|---|

| Earnings driver | Regulated lending margins, structural demand | Commodity prices, global supply and demand |

| Dividend predictability | Relatively stable, supported by earnings | Variable, disappears in commodity down-cycles |

| Competitive moat | Regulatory barriers, oligopoly structure | No moat against commodity price declines |

| Appropriate strategy | Buy-and-hold is defensible | Requires entry timing and exit discipline |

The lithium sector is the most recent illustration. The structural narrative of electric vehicle demand was real. What investors treated as a permanent structural investment was a cyclical bet on lithium prices. The subsequent severe price decline destroyed large portions of retail portfolios that were held passively on the assumption that the long-term thesis made exit unnecessary.

“Resource stocks move with the commodity cycle and must be managed accordingly, not held as permanent positions.”

Significant wealth creation is possible in the resources sector, but it requires two capabilities that passive buy-and-hold does not provide: the ability to time entry relative to the commodity cycle, and the discipline to exit when the cycle turns rather than holding through the down-cycle waiting for recovery. If you are currently holding resource stocks with a “long-term thesis” but no exit framework, you are carrying an unmanaged cyclical bet. That is not a conservative strategy. It is a passive position that transfers the full downside of a commodity cycle onto you with no mechanism for protection.

You have heard this one. Someone at a social gathering mentions a stock, says they are already up, and delivers the name with the confidence of someone sharing privileged information. There is the lowered voice, the significant look, the performance of someone passing on something exclusive.

The problem is structural, not social. When someone shares a stock tip in a social setting, they are almost always describing a position they already hold and have already profited from. The story being told is about their past return, not your future one. Professional practitioners in Australia explicitly identify “buying relatives’ hot tips” as one of the most common retail investor traps.

“By the time an idea surfaces at a barbecue, the easy money is usually gone.”

The social dynamics are precisely the conditions under which decisions are made on emotion rather than analysis: authority implied by confident delivery, fear of missing out, and social proof from someone having already profited. All three override the analytical process you would normally apply.

The disciplined alternative is not to dismiss tips entirely. A tip can be a useful research lead. The discipline is in separating the lead from the decision:

Building an independent investment thesis from primary sources, including ASX announcements, filed financial statements, and management track records, is precisely the process that separates a tip that becomes a research lead from a tip that becomes a position, because the analytical work either confirms or kills the idea on its own merits before money is committed.

The source of the idea is irrelevant to whether the investment makes sense at today’s price.

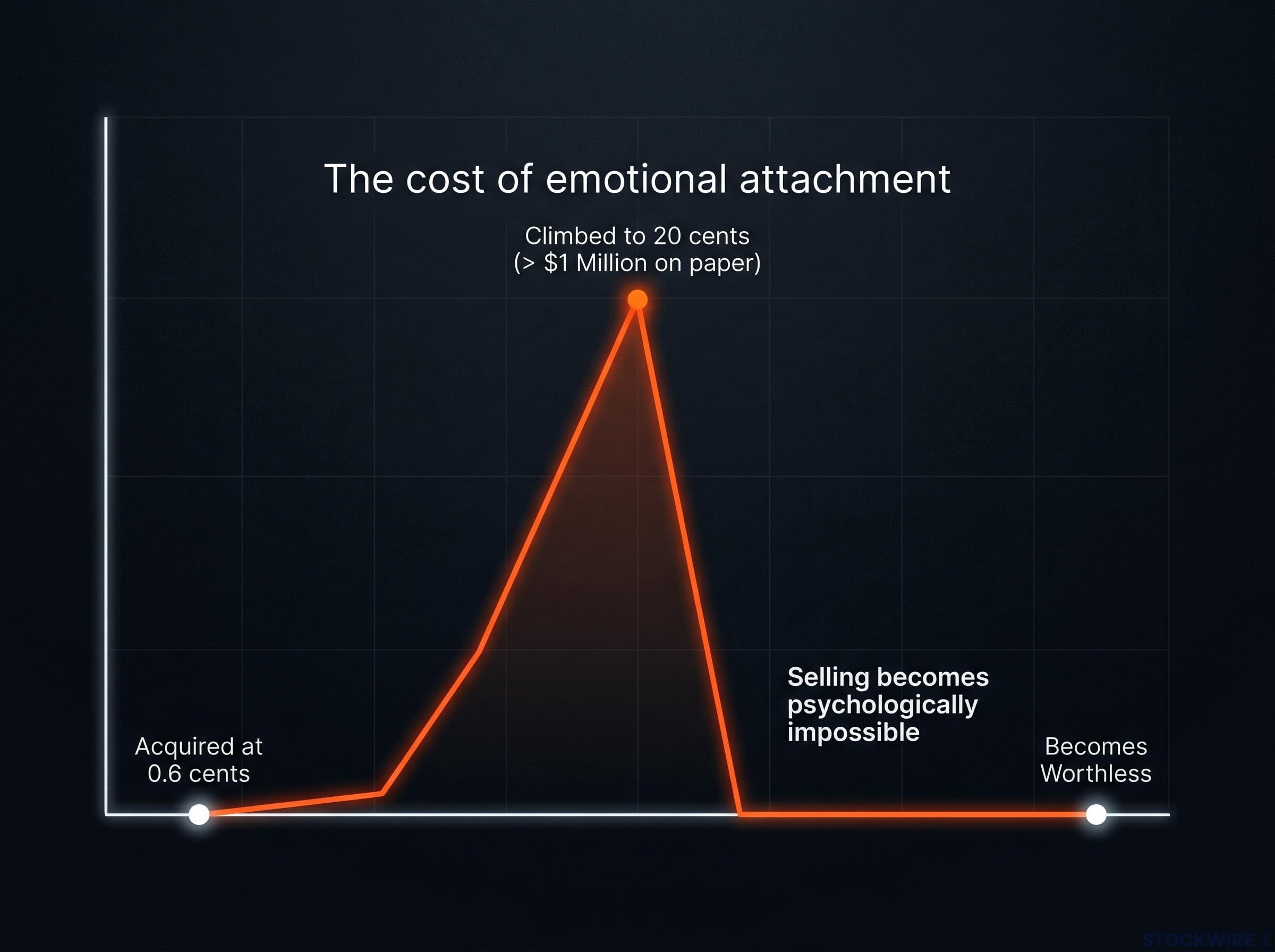

Consider a stock acquired at 0.6 cents per share that climbed to around 20 cents, turning a modest initial sum into more than one million dollars on paper. The holder had spoken about the position at every opportunity, family gatherings, professional events, social occasions, and had staked their reputation on it. When the price began to fall, they held on. Then it continued to fall. The stock eventually became worthless. The million dollars in paper gains disappeared entirely, not because the outcome was unforeseeable, but because selling had become psychologically impossible once identity and investment had fused into the same thing.

Two reinforcing psychological failures explain this pattern. The first is the disposition effect, which is the tendency for investors to hold losing positions too long and sell winning ones too early. Selling a large winner feels like closing the chapter on something meaningful. The second is identity attachment: having promoted the stock to others, selling feels like admitting failure rather than executing the rational decision.

The disposition effect, formally documented as a tendency to hold losers too long and sell winners too early, is not an isolated quirk; University of Chicago research found it contributes to sell-side decision quality so poor that randomly selected exits outperformed professional managers by up to 150 basis points annually, which suggests the psychological cost of emotional attachment extends well beyond any single position.

In volatile markets, this paralysis is amplified. The ASX notes that in volatile conditions, investors make decisions based on fear rather than plan. Emotional attachment adds a second layer: fear of “being wrong to sell” or “missing the recovery” keeps investors in deteriorating positions even as the rational case for holding evaporates.

“If you wouldn’t buy it today with fresh cash, you need a documented reason to still own it.”

The fresh-capital test is the primary cognitive check. If you would not buy this stock today at today’s price with fresh cash, that is the question you need to answer honestly before deciding whether to keep holding. Past gains do not change the forward-looking case.

The solution is not willpower. It is structural habits that operate automatically, before emotion enters the room:

These are structural habits, not one-off decisions. Their value is in automatic application rather than case-by-case judgement under pressure. Emotional attachment does not just damage one position. It distorts every decision made while you are inside it, including how much of the portfolio you allow it to consume.

Understanding these four traps intellectually is not enough. Awareness alone does not change behaviour. Scheduled habit structures do. Here is the minimum viable framework.

Before buying any stock:

Every 6-12 months per holding:

“The returns are in the habits.”

A reader who adopts even two of these checklist items as a consistent practice will make meaningfully better decisions than one who understands all four traps intellectually but has no structural habit to interrupt the behavioural pattern when it activates. Disciplined investing is not primarily about clever single decisions. It is about consistent habits over time: scheduled portfolio reviews, written investment rules, and predefined position limits that operate automatically.

The ASX’s structural shape, bank and resource concentration combined with the franking credit incentive, created the conditions for these four errors to feel rational. Understanding that structure is the foundation of resisting it.

International equity allocation is the structural corrective that addresses the bank and resource concentration directly: Australia represents approximately 2% of global market capitalisation, meaning a portfolio that holds only ASX names is ignoring 98% of the world’s listed companies and concentrating entirely in the sectors that drive the four traps described above.

If you have diagnosed which of the four traps you are currently sitting inside, you have already done the hardest part. The decision-making framework above provides the tools to act on that diagnosis. The traps are not random. They are structural. And the corrective is not extraordinary intelligence or market-beating insight.

It is process. It is consistency. It is the willingness to apply an objective test to decisions that feel personal. The returns are in the habits, and the habits are specific: scheduled reviews, written rules, predefined limits. Start with the one that addresses whichever trap you recognised yourself in first.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The four most common mistakes are chasing high-yield franked dividends regardless of personal tax position, applying buy-and-hold strategy to cyclical resource stocks, acting on unverified social tips, and developing emotional attachment to winning positions that prevents rational selling.

Franking credits are most valuable to investors whose credits exceed their total tax liability, primarily retirees in pension phase and those in lower tax brackets; working-age accumulators at higher marginal rates extract far less value from the same franked dividend, making a dividend-first strategy potentially costly for that group.

Resource company earnings are driven by commodity prices rather than structural demand, meaning dividends disappear in down-cycles and there is no competitive moat against price declines; the lithium sector collapse is a recent example where passive holders who lacked an exit framework lost large portions of their portfolios.

The fresh-capital test asks whether you would buy a stock today at its current price with fresh cash; if the answer is no but you are still holding, that gap reveals emotional attachment rather than a forward-looking investment thesis, and requires a documented reason to justify continued ownership.

A social tip should be treated as a research prompt, not a buy signal; the disciplined approach is to verify business quality and valuation independently from primary sources, and only act if the investment thesis stands entirely on its own merits without reference to who mentioned it.