Why Australian Investors Keep Repeating the Same 4 Mistakes

3 mins ago

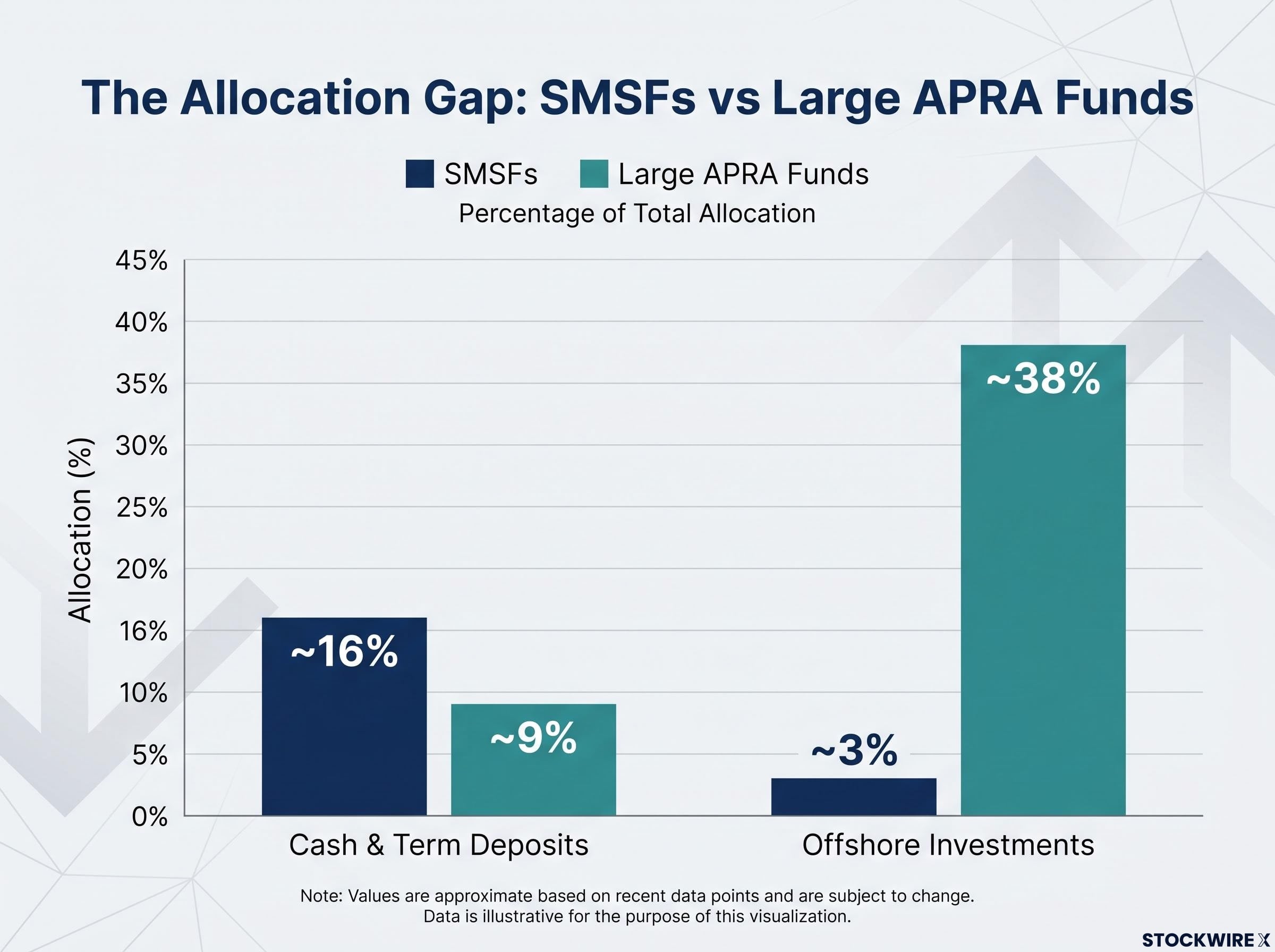

Most SMSF trustees believe their allocation is prudent. The ATO’s own data tells a different story. The average self-managed super fund holds roughly 16% of its assets in cash and term deposits, nearly double the rate of large professionally managed funds, and just 3% in offshore investments, compared with 38% for those same large funds.

The SMSF sector holds $1.06 trillion in assets. With median balances close to $1 million per fund, these are not abstract portfolio theory questions. They are retirement outcome questions measured in hundreds of thousands of dollars. The two structural gaps, excess cash and near-zero global exposure, compound over time and pull in the same direction: away from long-run returns.

Here is what the data actually shows, why both gaps persist despite having no remaining structural justification, and what a better-calibrated allocation path looks like for trustees willing to examine the evidence.

Start with the baseline. ATO quarterly data from December 2025 shows SMSFs holding approximately 16% of total assets in cash and term deposits, and roughly 27-28% in Australian listed shares. The total asset base sits at $1.06 trillion. Those numbers, on their own, look unremarkable.

The comparison makes them meaningful. Morningstar analysis of APRA data, published in July 2025, found that large APRA-regulated super funds hold approximately 9% in cash and roughly 38% offshore. SMSFs hold almost twice the cash and one-tenth the global exposure.

| Metric | SMSFs | Large APRA-Regulated Funds |

|---|---|---|

| Cash and term deposits | ~16% | ~9% |

| Offshore investments | ~3% | ~38% |

| Australian listed shares | ~27-28% | Not separately specified |

The 16% sector average likely understates the problem for a significant cohort. Many trustees hold 30-50% in cash, a range that is above average but far from uncommon. For those funds, the opportunity cost is materially more severe.

The gap between 3% and 38% offshore exposure is not a stylistic difference in portfolio construction. It tells you that SMSF trustees and professional fund managers have made fundamentally different bets about where global growth is coming from, and the professional managers’ bet has considerably more structural support.

Cash does not underperform equities once. It underperforms every year. And that gap compounds over five, ten, and fifteen-year horizons in ways that are not intuitively obvious.

The Vanguard 2025 Index Chart puts concrete numbers on that divergence: shares vs cash returns over 30 years show $10,000 in Australian equities growing to $143,786 versus $33,677 in cash, a verified historical outcome that makes the opportunity cost of excess cash holdings measurable rather than theoretical.

The mechanics work in three stages:

To illustrate the arithmetic: take a $1 million fund where half the capital sits in cash and the trustee targets a 10% overall return. The deployed half must generate roughly 20% annually to deliver the same dollar outcome as a fully invested fund earning 10% across the whole balance. That scenario is not typical, but it accurately represents what deeply cautious trustees are doing to their own retirement trajectory. The allocation feels like prudence; in practice it operates as a structural headwind against long-run accumulation.

Even at the 16% sector average, the opportunity cost over a long horizon is material, particularly for trustees who still have a decade or more before drawing down.

Professionally managed funds typically target a cash position of around 5% in ordinary market conditions, with that figure climbing toward 20% only in genuinely exceptional circumstances.

Hostplus explicitly warns SMSF trustees that excess cash holdings mean “missing out on long-term growth.” The gap between professional practice at 5% and the SMSF average at 16% tells you something about how the market’s best-resourced investors think about cash as a position: it has a measurable cost, not a neutral default.

The case for global exposure is not about diversification as an abstract virtue. It is about what is structurally absent from the ASX.

Several sectors that generated significant returns in globally diversified portfolios across the prior 18 months have little or no meaningful representation in the Australian market:

Treasury documentation notes that SMSFs remain concentrated in cash, term deposits, and Australian listed shares, with “little direct overseas investments.” That concentration is not cautious. It is a sector bet.

An ASX-only portfolio is not a neutral allocation. It is implicitly overweight in Australian financials, materials, and resources relative to the global benchmark. A fund with 3% offshore and 27-28% in Australian listed shares has not avoided risk through caution; it has exchanged global growth risk for domestic concentration risk.

Investing in international shares from Australia now requires only two ETFs covering developed and emerging markets, according to a framework built around the structural reality that the ASX represents approximately 2% of global market capitalisation and is heavily concentrated in financials and materials.

Franking credits and income from Australian equities are genuinely valuable. They do not, however, compensate for the complete absence of the high-growth global sectors that have driven returns in recent years. The question for trustees is which tradeoff better serves a multi-decade retirement portfolio.

The home bias had a legitimate historical justification. Direct offshore investing once required foreign brokerage accounts, foreign exchange management, and additional fund administration complexity. For self-directed trustees already managing compliance obligations, that was a genuine deterrent.

Those barriers no longer exist. ASX-listed exchange-traded funds (ETFs), which are investment funds that trade on the stock exchange like ordinary shares and track a specific index or theme, now provide straightforward access to:

These ETFs settle in Australian dollars through the same brokerage and custodial platforms SMSF trustees already use for domestic shares. No foreign brokerage account. No foreign exchange management. No additional compliance complexity.

The compliance and operational profile of adding a global ETF to an SMSF is now identical to adding another Australian equity holding.

The practical implication is direct. Any SMSF still holding 3% offshore is not doing so because global investing is technically difficult. The access barrier expired. What remains is either a deliberate investment view or inertia, and the distinction matters, because one can be evaluated on its merits and the other cannot.

The direction the data supports is straightforward: less cash, more global equity exposure. The specifics require individual calibration.

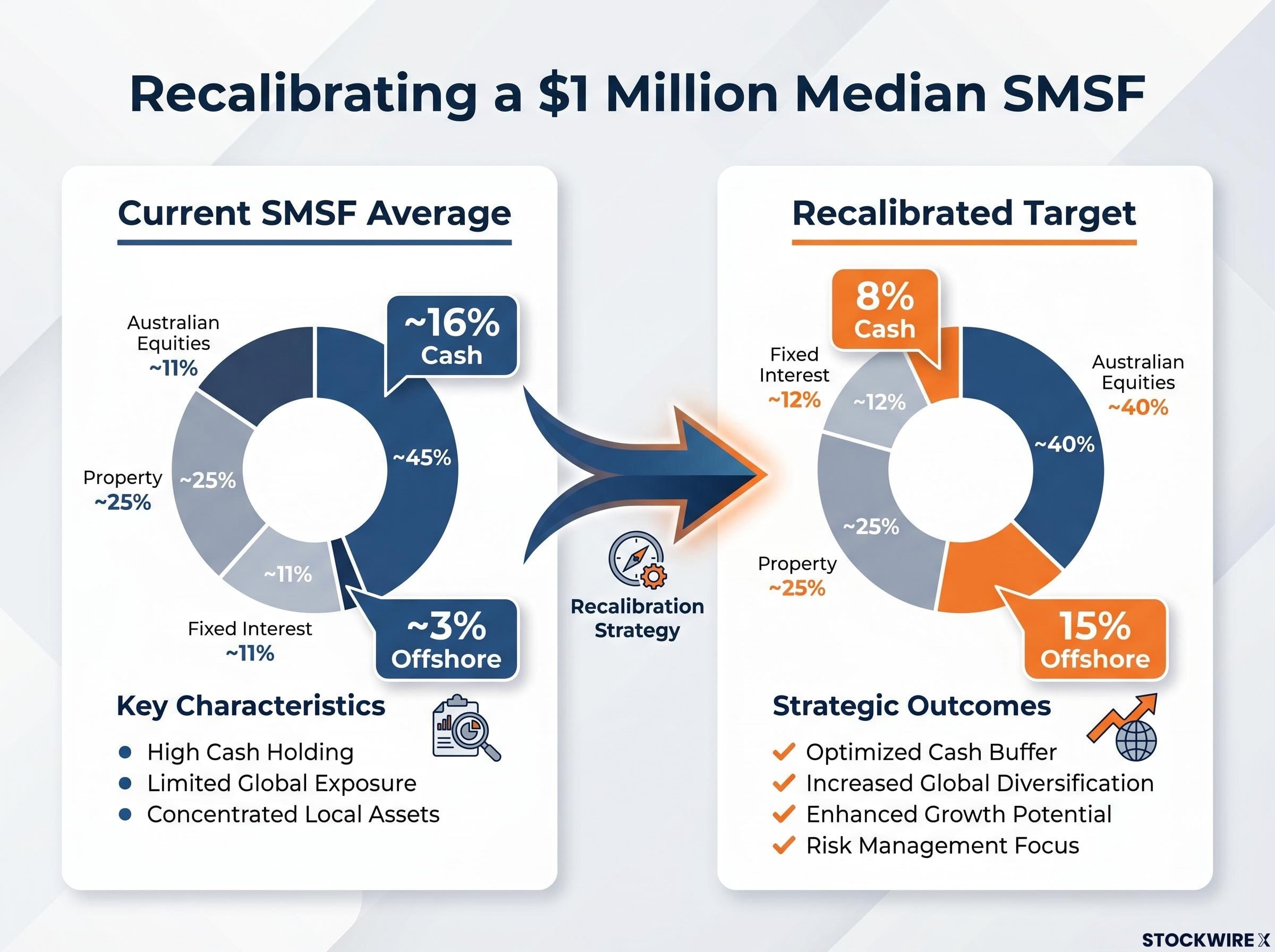

On cash, moving from 16% (the sector average) or higher toward a single-digit range of 5-10% aligns the fund more closely with professional practice without eliminating defensive positioning entirely. On global exposure, progressively building an international sleeve via ASX-listed ETFs preserves Australian equity income, including franking credits, while addressing the structural gap the data identifies.

| Metric | Current SMSF average | Large fund benchmark | Direction of travel |

|---|---|---|---|

| Cash and term deposits | ~16% | ~9% | Single-digit cash range (5-10%) |

| Offshore investments | ~3% | ~38% | Progressively building international sleeve |

| Australian listed shares | ~27-28% | Varies | Maintain for income and franking benefits |

At median balances close to $1 million, a shift from 16% cash to 8% and from 3% offshore to 15% is not a minor portfolio adjustment. It is a structural reallocation worth hundreds of thousands of dollars in expected long-run outcome, as ASIC’s Moneysmart guidance notes, investment returns in SMSFs depend entirely on trustee decisions.

Allocation changes in SMSFs interact with pension phase rules, transfer balance cap (TBC) limits, which cap the total amount a member can transfer into the tax-free retirement phase, and trust deed specifics in ways that make generic financial advice insufficient. A seemingly simple change, reducing cash and adding a global ETF, can trigger tax consequences, affect pension payment obligations, and require trust deed amendments.

At median balances close to $1 million, the cost of specialist SMSF advice is proportionate to the dollar value of the decisions it supports. This is not a disclaimer. It is a functional requirement of getting the execution right.

ASIC Moneysmart SMSF guidance establishes that trustees bear full responsibility for investment decisions within their fund, with no external manager accountability and no government compensation scheme if those decisions produce poor outcomes.

The two structural gaps, excess cash and near-zero global exposure, persist despite the technical barriers having been removed. The remaining barrier is behavioural, and it operates through three recognisable mechanisms:

Reactive cash switching in superannuation carries a documented asymmetry: members who moved to cash during the April 2025 sell-off were positioned to miss a roughly 5.8% single-month recovery, a pattern that illustrates why the instinct to hold cash during uncertainty has measurable costs that compound over accumulation-phase timelines.

An overweight cash position, viewed through this lens, is not a defensive investment posture. It reflects the absence of an active allocation decision. That distinction carries real weight: a genuine strategy can be tested against evidence and outcomes; a position that persists through inertia has no investment rationale to examine or defend.

Hostplus guidance encourages trustees to review their allocation against ATO averages, an implicit acknowledgment that many are defaulting rather than actively choosing. The 3% offshore allocation has persisted despite ASX-listed ETFs being readily available for years. That persistence is the evidence that the remaining barrier is inside the trustee’s frame of reference, not in the market infrastructure.

If your current allocation has not been actively reviewed against ATO benchmarks and the professional standard, the most likely explanation is not that you have made a deliberate choice to hold more cash and fewer global assets than professional managers. It is that the portfolio reflects inertia, and that is the thing worth examining.

The two structural gaps compound in the same direction. Excess cash and near-zero global exposure are not separate problems; they interact. The capital sitting idle in cash is also the capital not working in global growth assets. At a sector-wide scale of $1.06 trillion, the aggregate opportunity cost is substantial. At the individual fund level, with median balances close to $1 million, it is the difference between a retirement outcome that reflects the global opportunity set and one that reflects domestic inertia.

Australian equities do important work: franking credits, income generation, and exposure to sectors where Australia has genuine global strength. The case is not to replace the domestic sleeve. It is to supplement it with the global exposure that professional managers consider standard practice, funded in part by reducing a cash position that exceeds what any professionally managed fund would hold under normal conditions.

Tax-efficient rebalancing inside a superannuation or SMSF structure is the preferred execution pathway for allocation shifts of this kind, as earnings are taxed at the concessional 15% rate rather than the investor’s full marginal rate, materially changing the net cost of moving capital from cash into growth assets.

The question is no longer whether the case for recalibration is sound. It is whether individual trustees are willing to examine their allocation against the evidence.

The data is publicly available. The technical barriers have been removed. The directional path, single-digit cash, progressive international sleeve via ASX-listed ETFs, aligns with professional practice and regulatory guidance from ASIC. What remains is the decision to look.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

ATO quarterly data from December 2025 shows the average SMSF holds approximately 16% of assets in cash and term deposits, 27-28% in Australian listed shares, and just 3% in offshore investments.

Large APRA-regulated funds hold around 9% in cash and 38% offshore, meaning the average SMSF holds nearly double the cash and one-tenth the global equity exposure of professionally managed funds.

ASX-listed ETFs tracking global equity indices settle in Australian dollars through standard brokerage platforms, giving SMSF trustees straightforward access to developed markets, emerging markets, and sector themes like global technology with no foreign exchange management required.

Vanguard's 2025 Index Chart shows $10,000 in Australian equities grew to $143,786 over 30 years versus $33,677 in cash; in a $1 million fund with half the capital sitting idle, the deployed half must generate roughly 20% annually to match the outcome of a fully invested fund earning 10% across the whole balance.

The home bias once had a legitimate basis in the operational complexity of direct offshore investing, but those barriers no longer exist; what persists is largely familiarity bias and inertia rather than a deliberate investment view supported by evidence.