Why 30% Recession Odds Are Harder to Trade Than 60%

6 mins ago

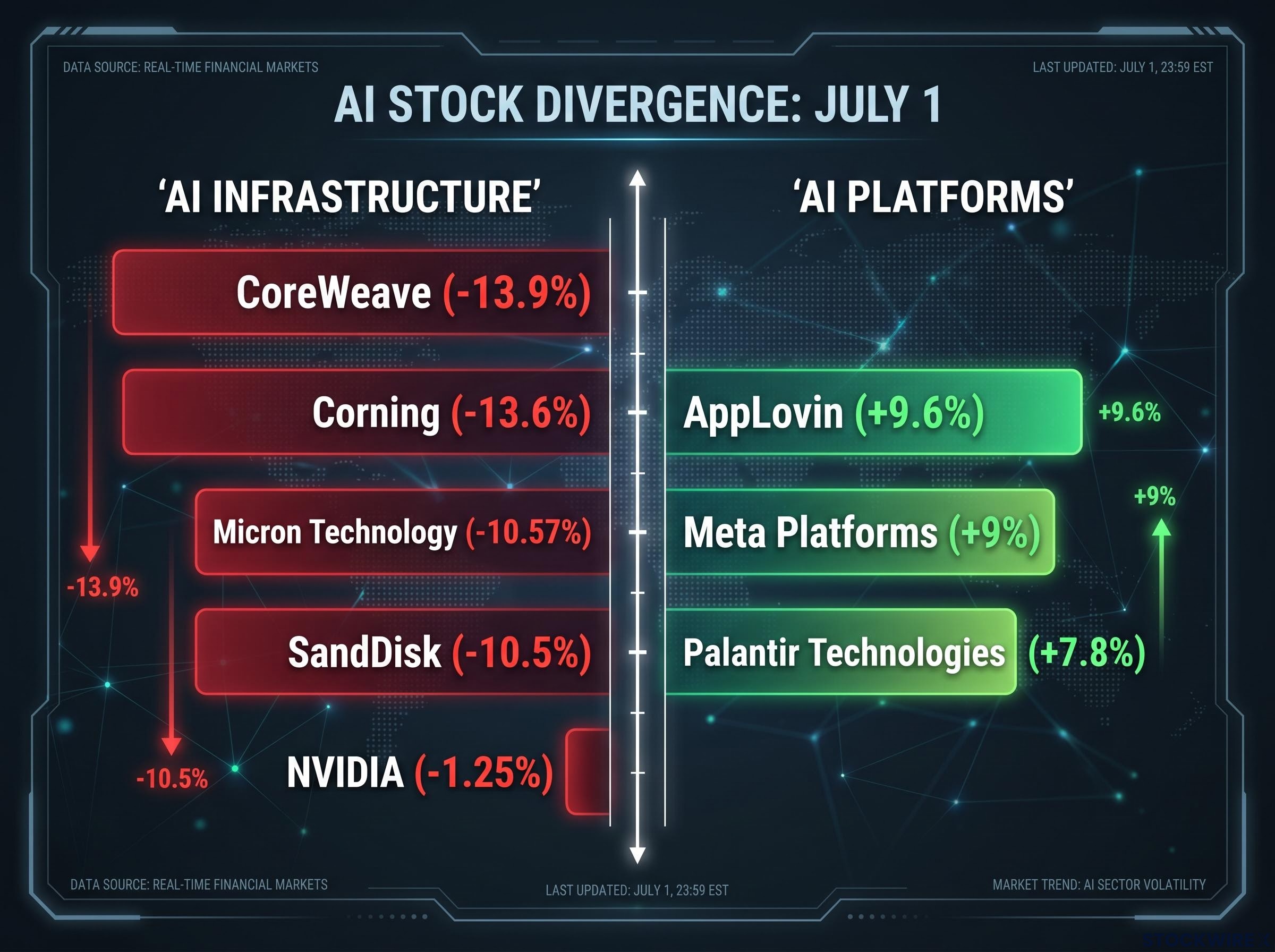

CoreWeave fell nearly 14% on Tuesday. Meta Platforms surged nearly 9%. Both moves happened in the same session, within the same sector, driven by the same theme: artificial intelligence.

That contradiction defined the first trading day of Q3 2026. Investors entered 1 July at historically elevated valuations, coming off Wall Street’s strongest quarter in six years. Positioning in AI hardware names was stretched after multi-hundred-percent appreciation over the prior twelve months. The conditions were set for something to break, and on Tuesday, it did.

Here is what the split between winners and losers tells you about how the AI and semiconductor stocks trade is changing, and which side of that fault line matters more as the new quarter begins.

The scorecard from 1 July tells the story faster than any index number can.

| Stock | Category | 1 July Move |

|---|---|---|

| CoreWeave | AI Infrastructure / GPU Cloud | -13.9% |

| Corning | AI Infrastructure / Optical | -13.6% |

| SandDisk | AI Infrastructure / Storage | -10.5% |

| Micron Technology | AI Infrastructure / Memory | -10.57% |

| NVIDIA | AI Infrastructure / GPU | -1.25% |

| AppLovin | AI Platform / Ad-Tech | +9.6% |

| Meta Platforms | AI Platform / Advertising | +9% |

| Palantir Technologies | AI Platform / Enterprise | +7.8% |

The Nasdaq Composite fell just 0.7% on the session. CoreWeave fell 13.9%. The index barely moved; individual names moved violently. This was not broad selling. It was targeted repricing.

The broader indices held far steadier, with the S&P 500 shedding 0.2% and the Dow closing only marginally lower. Against that backdrop, double-digit moves in opposite directions within the same sector tell you the market is no longer buying “AI exposure” as a single trade. It is now asking a sharper question: which AI companies actually convert infrastructure spending into durable earnings, and which ones simply depend on it?

Low index-level volatility across AI-heavy benchmarks had been masking precisely this type of distributional divergence for months, as large opposing moves by individual winners and losers cancel each other out, leaving investors exposed to single-stock risk they believed they had diversified away.

The divergence was not random. It ran along a structural fault line that has been building for months, and it comes down to how these businesses generate revenue.

AI hardware and infrastructure companies share vulnerabilities that the session made visible:

Hyperscaler capex commitments for 2026 sit in the $600-$805 billion range, a scale that has made infrastructure suppliers’ revenue narratives almost entirely dependent on continued data centre build-out, and that dependency is exactly what the market began repricing on 1 July.

Meta, AppLovin, and Palantir represent structurally different AI exposure:

The question to ask of any AI holding is not “does this company use AI” but “does this company have a revenue engine that AI makes better, or is AI the entire revenue thesis?” Tuesday’s session answered that question with price.

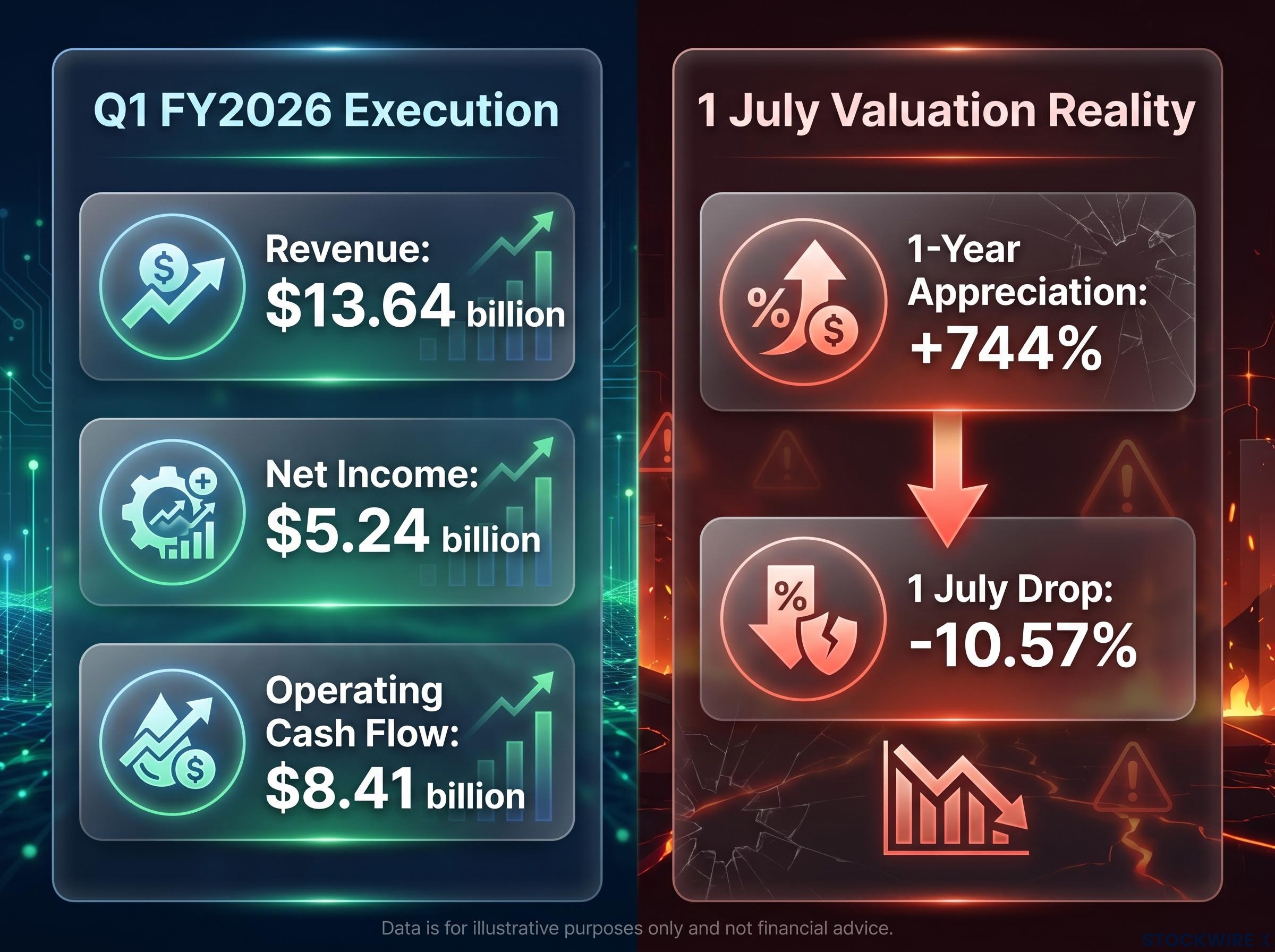

Micron Technology closed at $1,032.28 on 1 July, down 10.57% from its 30 June close of $1,154.29. The decline was the session’s clearest example of what happens when extraordinary appreciation meets even minor positioning shifts.

Micron had appreciated approximately +744% over the prior twelve months and +262% year-to-date as of 1 July. Its 52-week range stretched from $103.38 to $1,255.00. A 10.57% single-day decline, against that backdrop, is arithmetic, not panic.

The business itself was not the problem. Micron’s most recent quarterly results confirmed strong execution:

Revenue, earnings, and cash flow were all growing sequentially and year-over-year. The fundamentals were not the trigger. The trigger was starting valuation.

Micron’s forward earnings multiple, at approximately 7.58x-8.9x despite posting record quarterly revenue, placed it far below historical memory-sector valuation peaks, meaning the 10.57% single-day decline was driven by positioning and momentum rather than a genuine fundamental rerating of the business.

When a stock has appreciated +744% in a year, even excellent delivery leaves almost no margin for error. Positioning becomes extended, and any catalyst for profit-taking, however modest, produces outsized moves. That dynamic applies to every AI hardware name that experienced similar multi-hundred-percent appreciation over the past year.

The timing was not coincidental. 1 July was the first session of Q3 2026, arriving immediately after what market data characterised as Wall Street’s strongest quarter in six years. That calendar fact matters.

Three specific repositioning dynamics converged at the quarter boundary:

After-hours futures on 1 July told a consistent story. S&P 500 futures settled roughly 0.1% lower at 7,536.0. Nasdaq 100 futures lost around 0.1% to close at 30,068.75. Dow futures fell a similarly modest 0.1% to 52,600.0. The stability in broad futures, even as individual AI names moved 10-14%, is consistent with rotation within the AI complex rather than a retreat from the theme entirely.

Understanding this timing distinction matters. What happened on 1 July was an institutionally rational repositioning that the calendar made predictable. That context should shape how you interpret the sessions that follow.

The prior regime in AI investing was straightforward: anything with GPU exposure or an AI story attracted capital at almost any price. That regime ended on 1 July.

The old regime: AI exposure at any price. The new regime: show demonstrated monetisation and durable cash flow, or face de-rating.

Infrastructure names, the memory makers, GPU cloud providers, and optical connectivity suppliers, are now more likely to trade as what they structurally are: cyclical hardware plays sensitive to hyperscaler capex cycles. The market is no longer granting them permanent AI premium multiples without corresponding earnings visibility. Micron’s +744% one-year appreciation followed by a 10.57% single-day decline on no fundamental deterioration is the anchor example.

The monetisation vs. dependency distinction the market enforced on 1 July echoes BCA Research’s airline analogy for foundation model providers: companies bearing massive capital intensity for interchangeable, commoditised output face structural margin compression regardless of how strong the underlying technology becomes.

Platform names with existing monetisation engines may sustain more stable multiples, provided they continue delivering visible AI-driven revenue and margin gains. Meta’s +9% gain on cloud expansion news is the contrasting anchor.

Three variables will determine whether this shift holds or reverses in Q3:

The question you now need to answer for every AI holding is whether the company monetises AI or merely depends on others spending on AI. That distinction is where the next quarter’s returns will separate.

The AI growth narrative remains intact. Hyperscaler spending is elevated. Enterprise AI adoption is accelerating. The demand signal has not reversed.

What has changed is investor tolerance. Undifferentiated AI exposure at any valuation is no longer being rewarded. Tuesday’s session gave the market two possible interpretations to track through Q3: either this was temporary positioning-driven volatility that reverses if capex stays elevated and supply stays tight, or it was an early signal of a broader de-rating of AI infrastructure valuations as the market begins discriminating between monetisation and dependency.

The data over the coming weeks will determine which reading proves correct. What investors can act on now is the framework the session made visible: the companies that use AI to enhance proven revenue engines and the companies whose revenue depends entirely on others building AI infrastructure are no longer trading as the same bet.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

The selloff in infrastructure names like CoreWeave and Micron was driven by institutional profit-taking and quarter-boundary rebalancing after multi-hundred-percent appreciation, not a deterioration in fundamentals; the timing at the start of Q3, following Wall Street's strongest quarter in six years, made repositioning an institutionally rational move.

Meta, AppLovin, and Palantir have existing revenue engines that AI enhances rather than entire revenue theses that depend on AI infrastructure spending, giving them clearer near-term earnings visibility; Meta's cloud expansion announcements on 1 July directly reinforced that narrative and drove its 9% gain.

AI monetisation means a company uses AI to improve a revenue engine it already has, such as Meta applying AI to its advertising platform; AI dependency means a company's growth narrative relies almost entirely on continued hyperscaler data centre spending, which exposes it to cyclical capex risk and makes it vulnerable to de-rating when that spending moderates.

Micron had appreciated approximately 744% over the prior twelve months and 262% year-to-date before the session, with its 52-week range stretching from $103.38 to $1,255.00; despite posting record quarterly revenue of $13.64 billion, its forward earnings multiple of roughly 7.58x-8.9x meant the 10.57% decline was a positioning-driven move rather than a fundamental rerating.

No. Hyperscaler spending remains elevated and enterprise AI adoption is accelerating; what changed is investor tolerance for undifferentiated AI exposure at any valuation, with the market now separating companies that demonstrate durable monetisation from those that merely depend on others building AI infrastructure.