Why a 57,000 Jobs Miss Sent Equity Futures Higher

52 mins ago

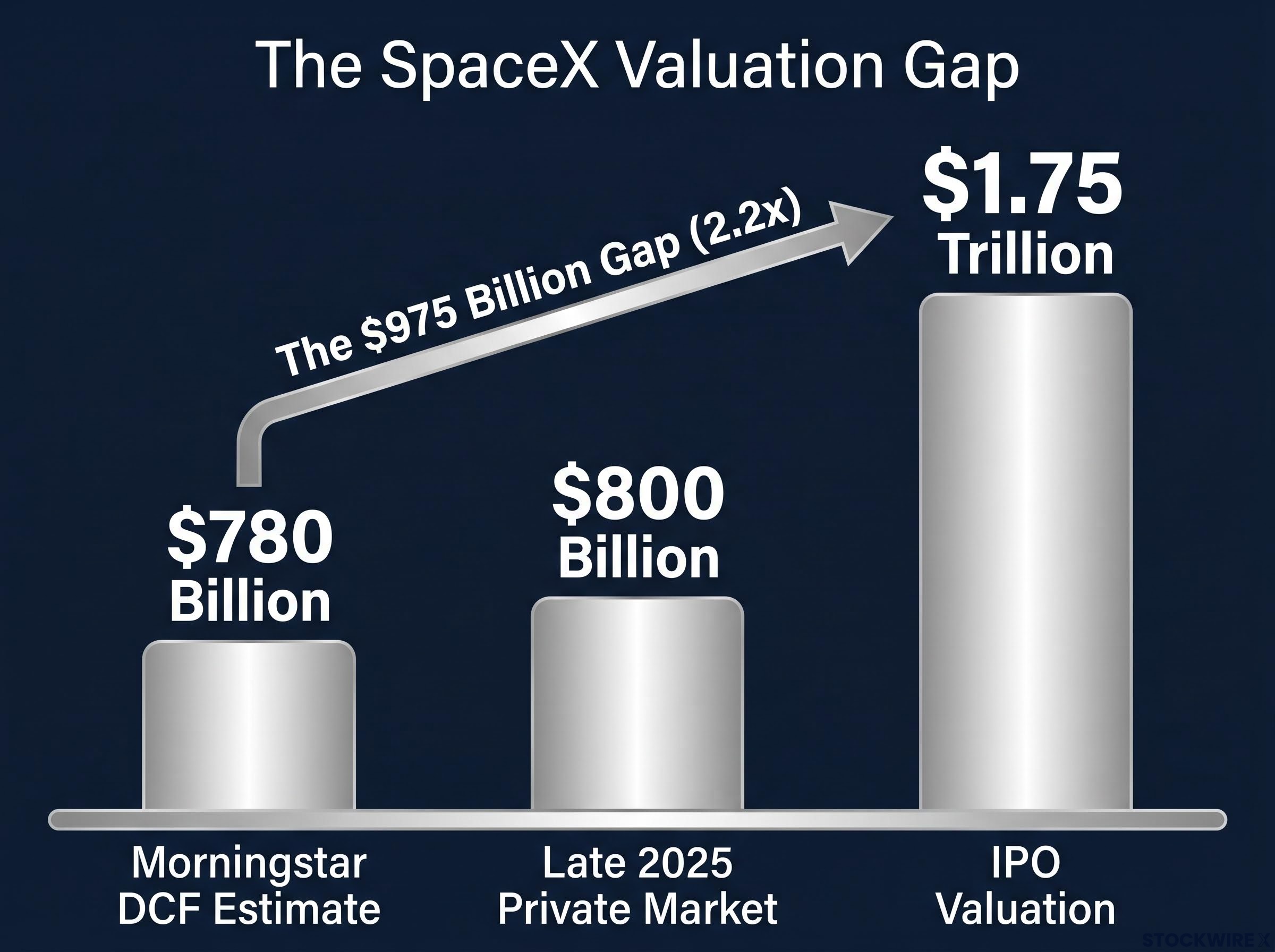

Public investors are being asked to pay $1.75 trillion for a company that a leading equity research house values at $780 billion. That is not a rounding error. It is a $975 billion gap between what the market wants to charge and what a discounted cash flow model says the business is worth.

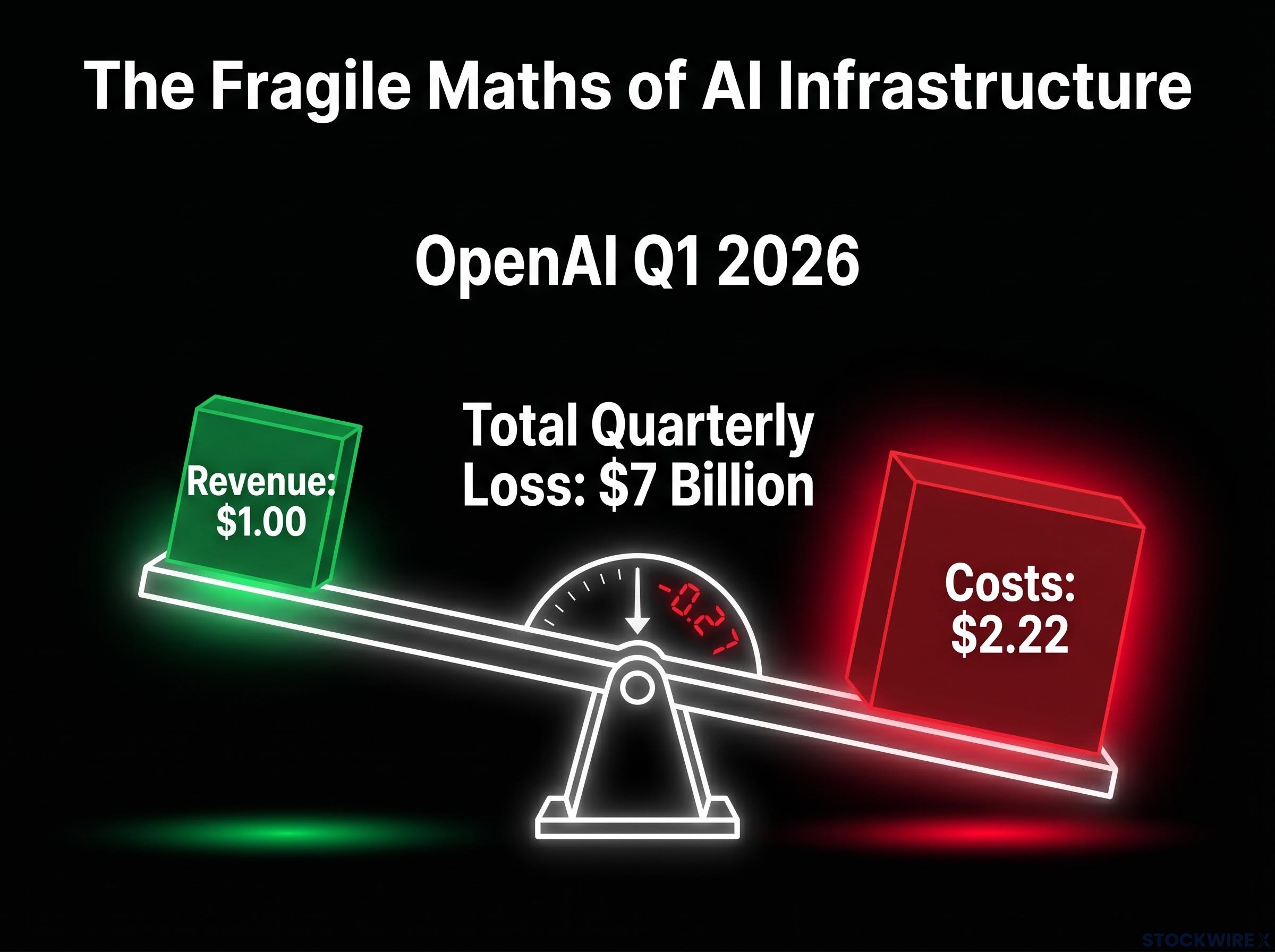

SpaceX‘s record-setting IPO is the most numerically legible data point in a pattern spreading across AI-linked assets: prices are disconnecting from the cash flows needed to justify them. OpenAI lost $7 billion in a single quarter. Frontier AI companies are spending more than twice what they earn. And the companies attracting the largest valuations are being priced not on what they produce today, but on an AI infrastructure future that has not yet demonstrated sustainable economics.

Here is the framework for separating a technology that is genuinely rewiring the economy from a market that has overshot the value of that technology. The numbers that follow tell you which side of that line the evidence currently favours, and what would need to change for the current prices to be right.

The core facts are straightforward, and they are worth isolating before any interpretation:

Morningstar‘s equity analysts ran a discounted cash flow (DCF) analysis on SpaceX. A DCF values a company by estimating all the cash it will generate in the future and discounting those amounts back to today’s dollars; it measures what a business is worth based on its projected earnings, not on what the market is willing to pay for it right now. Their estimate: approximately $780 billion.

That puts the price-to-intrinsic-value gap at roughly 2.2x. Private market transactions had marked SpaceX at approximately $800 billion at the end of 2025. Within six months, the IPO asks public investors to pay more than double that figure.

The SpaceX IPO mechanics also carry a structural wrinkle that complicates standard price discovery: the company bypassed the traditional institutional roadshow, meaning no institutional order book existed to signal demand levels before the $135 price was set and shares began trading.

Morningstar’s explicit assessment: SpaceX is “substantially overvalued” at the IPO price, and investors are likely to find better entry points after listing.

A 4% float means 96% of SpaceX shares have not been priced by an open market transaction. The headline valuation of $1.75 trillion is extrapolated from a thin slice of actual trading.

That matters for a specific reason. Near-term demand for the stock will be driven significantly by index inclusion mechanics, where passive funds are compelled to buy because of SpaceX’s market capitalisation, not by active fundamental buying decisions. What this tells you is that the price discovery happening at IPO reflects a structurally thin market. Public investors buying today are underwriting a number that very few transactions have actually stress-tested.

SpaceX operates across three revenue segments, and the gap between their profitability profiles and their respective roles in the valuation story is where the analytical tension sits.

| Segment | Profitability status | Role in valuation narrative |

|---|---|---|

| Launch operations | Loss-making | Foundational capability; priced for scale |

| Starlink (satellite broadband) | Profitable (only profitable segment) | Revenue anchor; connectivity moat |

| xAI / AI infrastructure | Loss-making; uncertain moat | Primary driver of valuation premium |

Starlink is the only segment generating profit. Launch operations remain loss-making. xAI, acquired by SpaceX in February 2026, is the segment investors are most excited about, and the one Morningstar is most cautious on.

Morningstar on xAI: The segment carries a “material threat of value destruction” and an uncertain economic moat.

The revenue multiples make the pricing story explicit. SpaceX trades at approximately 67-90x trailing sales depending on the revenue base used, roughly 3x Nvidia’s sales multiple. Analysts have attributed near-term price momentum primarily to elevated investor appetite for AI infrastructure exposure.

When the only profitable segment is satellite broadband and investors are assigning a $1.75 trillion valuation largely on the strength of AI infrastructure ambitions that do not yet generate positive returns, the company is priced for a future that has not yet arrived. That is not necessarily wrong. But it is a bet, not a valuation.

SpaceX is the most visible case study, but the unit economics of the broader AI sector tell the same story from a different angle. OpenAI‘s Q1 2026 financials provide the cleanest available window into what frontier AI economics actually look like at scale.

The number that anchors this section: OpenAI spent $2.22 for every $1.00 it earned in Q1 2026.

That ratio is not a startup-phase anomaly specific to one company. It reflects the structural cost burden of running frontier AI infrastructure at scale: massive compute requirements for model training and inference, energy costs, and hardware depreciation that currently outpace what customers are willing to pay.

The question facing the sector is not whether AI is useful. It plainly is. The question is whether the companies building it can achieve sustainable margins before capital markets reduce their appetite for funding losses. OpenAI’s numbers and SpaceX’s valuation are not separate stories. They are both expressions of the same investor thesis about AI infrastructure, and OpenAI’s cost ratio provides the closest available data on whether that thesis has found its financial footing yet. So far, it has not.

The OpenAI governance structure adds a layer of uncertainty that the cost-to-revenue ratio alone does not capture: a capped-profit nonprofit hybrid with board authority over commercial decisions has no public-market precedent, and three critical disclosures including Microsoft’s equity stake and conversion mechanics remain undisclosed ahead of any filing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The pattern has a name, and it has happened before. During the late 1990s, companies appended “.com” to their names to attract speculative capital regardless of underlying business fundamentals. Share prices responded to the label, not the balance sheet.

The AI era has its own version. Reports have cited shoe company Allbirds rebranding to “Smartbird” after a stated pivot to AI infrastructure as one example of this phenomenon (though this specific rebrand has not been independently verified against primary sources and should be confirmed before being treated as established fact). Whether that particular case holds up, the behaviour it represents, companies adopting the dominant speculative theme as a corporate identity, is consistent with late-cycle patterns that financial historians have documented across multiple eras.

The more important historical lesson is not about names. It is about returns. Technologies that proved genuinely world-changing still produced poor investor returns during their speculative expansion phases:

The technology being real and the prices being wrong are not contradictory positions. They have coexisted in every major technology cycle.

The BIS analysis of historical investment booms draws explicit parallels between the current AI investment cycle and past speculative waves, including canal mania, British railway mania, and the dot-com era, each of which involved a genuine technological breakthrough that attracted capital exceeding what commercial returns could ultimately justify.

When Chinese AI model DeepSeek arrived in January 2025, U.S. technology stocks sold off sharply in response. The reaction was a concrete reminder that competitive shocks can puncture AI-linked valuations quickly, even when the broader technology thesis remains intact.

The enterprise side has already started behaving accordingly. Uber burnt through its entire 2026 AI budget by the close of Q1 2026 and then shifted its workloads to lower-cost model providers. That is not a hypothetical scenario about future cost sensitivity. It is a real-world data point showing enterprises shopping across providers the moment cheaper options appear, the kind of substitution behaviour that typically erodes pricing power in maturing technology markets.

The gap between SpaceX’s IPO price and Morningstar’s intrinsic value estimate closes one of two ways. Both deserve serious analytical attention.

| Scenario | What it requires | Historical frequency |

|---|---|---|

| Fundamentals catch up | Cash flows and profitability grow far beyond current conservative forecasts | Rare when premium is this large and generalised across a theme |

| Price corrects down | Sustained period of underperformance or sharp correction | More common historically in generalised speculative themes |

The bull case is not irrational on its face. AI is genuinely reshaping industries. SpaceX has competitive advantages in reusable launch technology and satellite broadband that are difficult to replicate. The question is whether those advantages, combined with nascent AI infrastructure ambitions, justify the specific price.

The quantitative requirement: Models assume approximately 40% annualised revenue growth for roughly a decade to justify current multiples.

That is not impossible. But it requires SpaceX to execute on AI infrastructure, global Starlink scaling, and launch dominance simultaneously and continuously, with no major competitive displacement, regulatory setback, or technology disruption. At projected 2026 combined revenue of approximately $28.5 billion (a figure that has not been independently verified), the forward revenue multiple sits at approximately 61x. The trailing multiple, depending on base used, ranges from 67x to north of 90x, roughly 3x what investors pay for Nvidia.

Index concentration risk compounds this dynamic in a way that headline volatility figures obscure: low index-level volatility across AI-heavy benchmarks is masking large opposing moves by individual winners and losers that cancel each other out, leaving investors exposed to single-stock risk they may believe they have already diversified away.

What you are evaluating when you look at these numbers is not whether AI will matter. It is whether the specific growth trajectory being priced in today will materialise on the assumed timeline. That is a narrower and harder question.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The evidence assembles into a picture that is specific enough to be useful and honest enough to acknowledge its limits.

SpaceX’s 2.2x price-to-intrinsic-value gap. OpenAI’s $7 billion quarterly loss and $2.22 cost-per-revenue-dollar. The DeepSeek competitive shock. Uber’s enterprise substitution behaviour. Together, these data points constitute speculative pricing characteristics consistent with conditions that have preceded past bubble formations. They do not constitute proof of an imminent sector-wide collapse, and the difference between those two statements matters.

The calibrated read: The AI sector is exhibiting speculative pricing characteristics, not a confirmed bubble with a defined crash timeline. The distinction is analytically significant.

Three variables will determine which gap-closing mechanism plays out:

“AI is real” and “AI stocks are overpriced” are not contradictory positions. The evidence supports holding both simultaneously. The railroads were real. Electrification was real. The internet was real. In each case, the technology rewired the economy and a significant share of the investors who funded the speculative expansion phase lost money. The ability to hold both of those ideas at once, without either uncritical enthusiasm or reflexive dismissal, is what separates a calibrated view of today’s market from one that is simply hoping the music keeps playing.

For investors wanting to stress-test the speculative pricing thesis with formal analytical tools, our dedicated guide to AI bubble frameworks applies the Shiller CAPE ratio, Minsky financing stages, and Kindleberger’s crisis model to the current AI cycle, with specific portfolio actions for each scenario.

These statements are speculative and subject to change based on market developments and company performance.

An AI bubble refers to a period when AI-linked asset prices disconnect from the cash flows needed to justify them; analysts identify one by comparing market valuations to discounted cash flow estimates, cost-to-revenue ratios, and historical speculative cycles such as the dot-com era and railway mania.

Morningstar's DCF analysis puts SpaceX's intrinsic value at approximately $780 billion, while the IPO priced the company at roughly $1.75 trillion, a gap of about $975 billion, and the firm explicitly described the stock as substantially overvalued at the $135 per share offering price.

OpenAI's Q1 2026 results show a $7 billion quarterly loss and a cost-to-revenue ratio of $2.22 spent for every $1.00 earned, indicating that frontier AI infrastructure spending currently outpaces what customers are paying by a wide margin.

When DeepSeek launched in January 2025, U.S. technology stocks sold off sharply, demonstrating that cheaper competitive models can rapidly compress the pricing power of incumbent AI infrastructure providers and puncture associated valuations even when the broader AI thesis remains intact.

The BIS has drawn explicit parallels between the current AI cycle and canal mania, British railway mania, and the dot-com era; in each case a genuine technological breakthrough attracted capital that exceeded what commercial returns could justify, with the Nasdaq falling 78% from its 2000 peak before recovering.