OpenAI closed a funding round on 31 March 2026 valuing the company at $852 billion. It is now preparing a confidential S-1 filing with Goldman Sachs and Morgan Stanley as lead underwriters, targeting a market debut as early as September 2026. The number is extraordinary. The question finance-educated investors need answered is whether the story behind the number holds together under scrutiny.

Three distinct risk clusters are converging as OpenAI approaches public markets: a pending Elon Musk appellate case that keeps the company’s foundational governance in legal limbo; a unit-economics structure where infrastructure costs compress margins in ways atypical of software peers; and an increasingly competitive enterprise environment where Anthropic has been winning net-new Fortune 500 deals at a faster rate. None of these risks is individually fatal. Together, they shape the discount investors should demand.

What follows works through each risk systematically, examines what the available data actually shows, and offers a framework for how investors should weigh these headwinds against the $852 billion valuation benchmark.

What the Musk verdict actually settled (and what it left open)

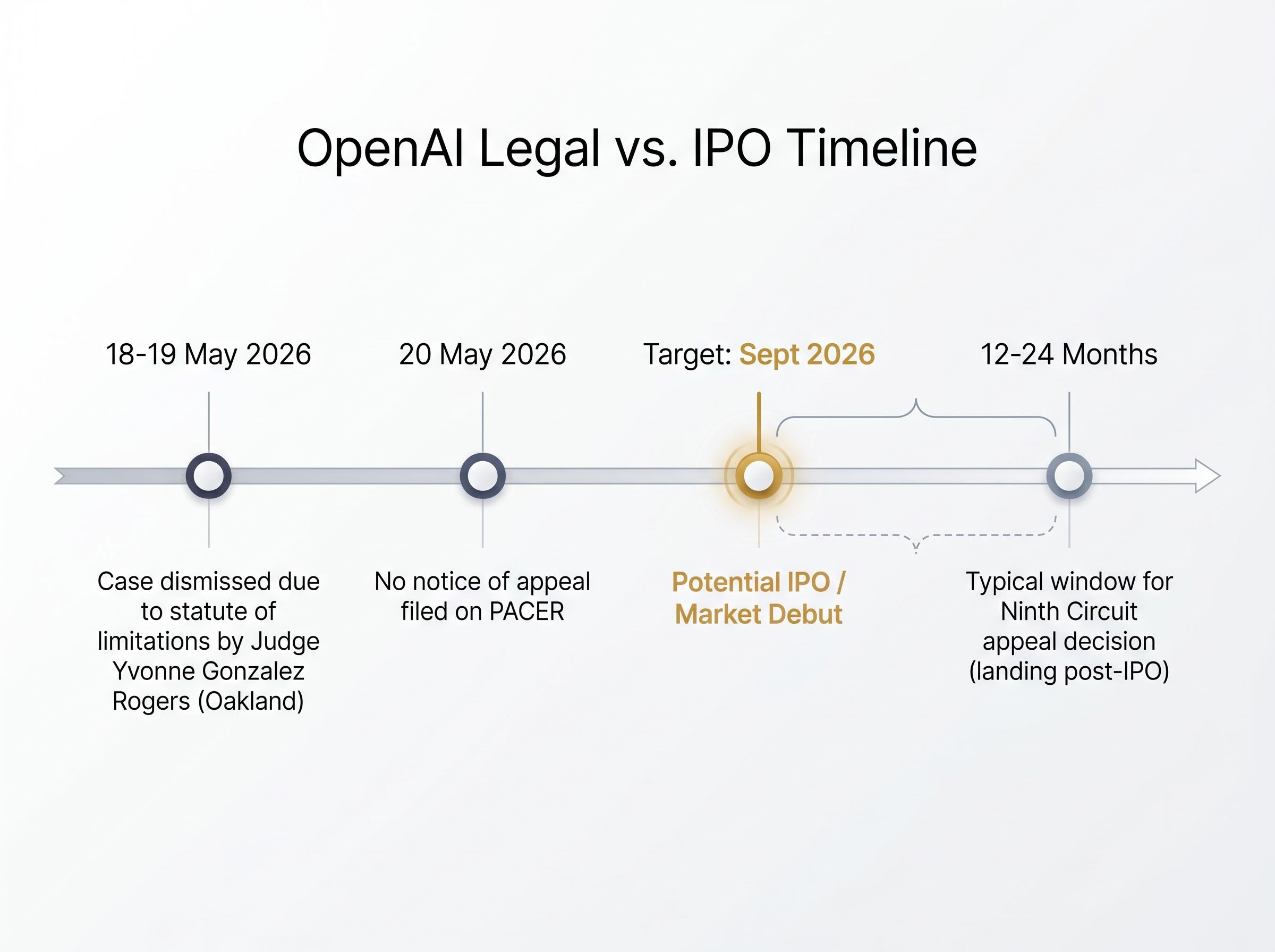

The verdict arrived on 18-19 May 2026, and for OpenAI, it looked like a clean win. A unanimous jury in the U.S. District Court, Northern District of California, Oakland, before Judge Yvonne Gonzalez Rogers, found that Elon Musk had exceeded the statute of limitations in bringing his claims. The case was dismissed.

Then the fine print mattered. The jury’s finding was procedural. It determined that Musk waited too long to sue. It did not rule on the substance of his allegations: that OpenAI violated a founding agreement to remain a nonprofit and to open-source its technology. Those claims were never adjudicated on their merits.

Three distinct legal layers sit underneath that headline verdict:

- What the trial resolved: Musk’s claims were time-barred. The statute of limitations had expired.

- What it left open: Whether a binding agreement to remain nonprofit ever existed, and whether OpenAI breached fiduciary duties, remains unanswered by any court.

- What an appeal could theoretically reopen: If the Ninth Circuit reverses the limitations finding, the substantive contract and fiduciary-duty claims could return to trial, raising questions about OpenAI’s ability to operate as a for-profit entity.

Musk has signalled intent to appeal. As of 20 May 2026, no notice of appeal or briefing schedule has appeared on PACER. Ninth Circuit civil appeals typically take 12-24 months from docketing to decision, placing a potential ruling well after any September 2026 IPO.

A securities-litigation attorney, quoted by The Information, characterised the case as “headline risk and distraction rather than existential legal risk” to the IPO, noting that the probability of the appeal materially altering OpenAI’s structure is low given the procedural defeat at trial.

The appeal is unlikely to block the offering. But it does mean the S-1 risk-factor section will carry an active litigation disclosure that investors have no choice but to price.

The Musk appeal is not the only active governance cloud over the offering; the Altman conflict-of-interest investigation launched by the House Oversight Committee in May 2026 examines whether OpenAI resources were directed toward companies in which the CEO holds personal financial stakes, adding a second unresolved disclosure risk that will need to appear alongside the Musk litigation in the S-1 risk-factor section.

When big ASX news breaks, our subscribers know first

Why Anthropic winning more Fortune 500 deals matters to the OpenAI IPO story

OpenAI still leads. It leads on total revenue. It leads on total user count. It leads on brand recognition. Those facts are not in dispute.

The pattern underneath those facts is what complicates the IPO narrative. Anthropic was on a more than $1 billion annualised revenue run-rate by early 2026, with revenue more than tripling year-on-year in 2025. Most of that growth came from enterprise contracts delivered through AWS Bedrock and Google Vertex AI.

Among new Fortune 500 AI platform deals signed in 2025, Anthropic won more net-new enterprise platform standards than OpenAI, according to analyst-cited data reported by The Information. The reasons are structural rather than accidental:

- A major U.S. bank selected Anthropic via AWS Bedrock for risk-model documentation and compliance, a multi-million-dollar annual contract where cloud neutrality and data-governance flexibility drove the decision

- A global consulting firm standardised on Claude for client-facing knowledge workers, again through a cloud-marketplace channel independent of Azure

- OpenAI’s flagship enterprise positioning centres on enterprise ChatGPT agreements and co-selling through Microsoft’s Azure OpenAI Service, tying its distribution to a single cloud provider

Bain and Company’s Technology Report 2025 observes that “Anthropic has emerged as the preferred second-source or even primary model in a growing subset of large enterprises, particularly those already committed to AWS or Google.”

Anthropic’s defence AI exclusion, which followed a supply chain risk designation after the company refused to permit use cases involving autonomous lethal weapons and mass domestic surveillance, effectively removed it from a defence spending supercycle that now routes through a seven-vendor Pentagon coalition including OpenAI, Nvidia, Microsoft, and Google, complicating any simple narrative that Anthropic’s enterprise momentum threatens OpenAI across all verticals.

The Azure dependency as a double-edged asset

Microsoft’s infrastructure partnership provides scale, credibility, and distribution. It also creates concentration risk. Enterprises committed to other clouds, or pursuing hybrid and multi-cloud strategies, face friction adopting OpenAI models in ways they do not face with Anthropic or open-source alternatives.

Analysts characterise this as a factor actively driving cloud-neutral enterprises toward competitors, according to both Bain’s Technology Report and reporting by The Information. The friction compounds as Microsoft advances its own first-party Copilot models, introducing potential channel conflict with the very partner OpenAI depends on for distribution.

The structure that makes OpenAI unlike any company public investors have priced before

Start with what is familiar. A company generates revenue, scales operations, and files to go public. Investors buy equity expecting a share of future profits, governed by a board accountable to shareholders.

Now adjust. OpenAI operates as a capped-profit company, a subsidiary of a nonprofit parent. Investor returns are explicitly capped, with surplus flowing to the nonprofit. The nonprofit board retains authority to prioritise AI safety over profit maximisation. Public shareholders would, in effect, own equity in an entity whose governing body can override their financial interests in service of a broader mission.

No publicly traded company carries this structure. Securities lawyers quoted by The Information characterised the hybrid model as something that “will be a central risk factor in the S-1,” because the governance mechanics that determine how this tension resolves are not yet disclosed.

How the nonprofit-for-profit split works in practice

The mechanics are where the ambiguity concentrates. Three items remain undisclosed and will be among the most closely watched sections of the filing:

- Microsoft’s equity stake: the exact ownership percentage has not been publicly confirmed

- Conversion mechanics: the terms under which the capped-profit structure converts, including what triggers apply and what limits remain

- Governance authority distribution: how nonprofit board decisions interact with public shareholder fiduciary rights, and what recourse shareholders have if the two conflict

The 2023 governance crisis, when the board briefly removed CEO Sam Altman before reinstating him, remains institutional memory for investors evaluating how decision-making authority is actually distributed. The S-1 will need to answer whether the structure has been clarified since then, or whether the same fault lines persist.

Reading OpenAI’s unit economics without the hype filter

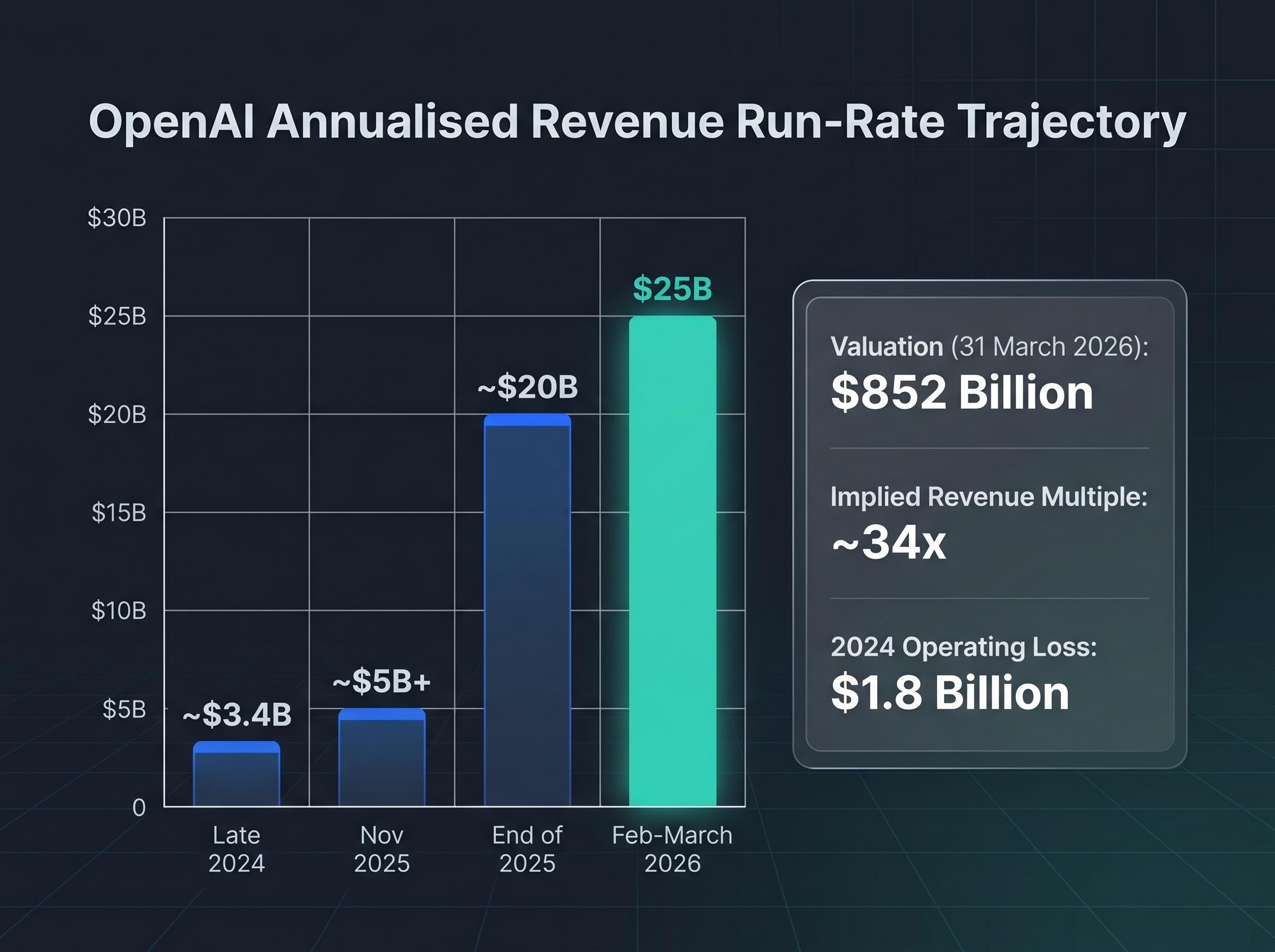

The revenue trajectory speaks first, and it speaks loudly. OpenAI scaled from approximately $3.4 billion annualised in late 2024 to $25 billion annualised by February-March 2026, roughly $2 billion per month. That pace of growth is striking by any measure.

| Period | Annualised Run-Rate | Key Context |

|---|---|---|

| Late 2024 | ~$3.4 billion | $1.8 billion operating loss for 2024 |

| November 2025 | ~$5 billion+ | Losses projected to continue through at least 2026 |

| End of 2025 | ~$20 billion | Multi-year compute reservations compressing gross margins |

| Feb-March 2026 | $25 billion | $852 billion valuation implies ~34x revenue multiple |

The cost structure changes the picture. OpenAI lost approximately $1.8 billion in 2024 and has indicated to investors that it expects to remain loss-making through at least 2026. Capital commitments for compute, largely via Microsoft, are described as tens of billions of dollars over the coming years. Microsoft’s AI capex guidance alone exceeds $50 billion annually. Analysts believe OpenAI’s minimum-spend commitments exceed near-term revenue, contributing to negative free cash flow even as the top line scales.

Hyperscaler capital expenditure trajectories provide the most direct external calibration point for OpenAI’s compute cost structure: Amazon, Microsoft, Alphabet, and Meta collectively spent $130 billion in Q1 2026 alone, with full-year 2026 guidance reaching approximately $725 billion, a spending scale that sets the benchmark against which OpenAI’s minimum-commit obligations and negative free cash flow projection should be evaluated.

Bain and Company’s Technology Report 2025 notes that foundation-model providers face “capex-intensive economics more akin to hyperscale cloud than classic SaaS,” warning that investors should adjust multiples accordingly.

At an $852 billion post-money valuation against $25 billion annualised revenue, the implied multiple is approximately 34x. That expectation requires sustained dominance and significant margin expansion in a business where training and inference costs scale with usage rather than declining smoothly. The Financial Times observed in November 2025 that OpenAI “has not yet demonstrated the operating leverage public investors expect.” Seven months later, the revenue has grown dramatically. The margin question has not been answered.

What “AI company” means when you price it against software comparables

Investors approaching the OpenAI IPO with a Software-as-a-Service (SaaS) valuation framework, where companies typically exhibit high gross margins, low marginal cost per additional customer, and operating leverage at scale, are applying a model that does not transfer cleanly to a foundation-model provider.

The divergence is structural. Training and inference costs for large language models scale with usage rather than declining smoothly with volume. Multi-year compute reservations with Microsoft lock in front-loaded capital expenditure that compresses gross margins relative to software peers. Deloitte’s Tech Trends 2026 frames this as “AI infra lock-in risk”: large, front-loaded training and deployment spend that may not be fully recoverable if enterprise buyers shift to open-source or cheaper competitors.

Comparative analysis of AI versus SaaS valuation multiples shows that foundation-model and AI infrastructure companies have commanded average revenue multiples of approximately 37.5x, versus 7.6x for traditional SaaS, reflecting speculative premium rather than demonstrated operating leverage.

The Financial Times noted in November 2025 that OpenAI “has not yet demonstrated the operating leverage public investors expect,” given dependence on costly training cycles and revenue-sharing arrangements with partners.

Bain and Company’s Technology Report 2025 identifies three conditions that would need to hold for a foundation-model provider at this scale to reach breakeven:

- Sustained price increases combined with upselling into higher-margin enterprise features

- Significant cost reductions from hardware advances and model optimisation

- A material shift in revenue mix toward higher-margin enterprise workflows

All three must move in the right direction simultaneously. Deloitte warns that investors may apply a structural discount to foundation-model providers whose economics are tightly bound to escalating compute spend and partner revenue-shares. At approximately 34x revenue, the $852 billion valuation assumes those conditions will be met. The category is new enough that no public-market comparable exists to test that assumption against.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The honest investor calculus as OpenAI approaches its S-1

The three risks examined above do not operate independently. The Musk appeal raises governance uncertainty. The nonprofit-capped-profit hybrid structure amplifies that uncertainty for public shareholders who lack a precedent for how such conflicts resolve. The capex-intensive economics limit the financial runway for addressing governance and competitive headwinds. And Anthropic’s growth in the enterprise segments that matter most narrows the margin for error on all three fronts.

The $852 billion valuation, set in the 31 March 2026 funding round, is defensible only if three conditions hold:

- Revenue growth sustained at or near current trajectory

- Margin expansion materialises as compute costs decline with next-generation hardware

- The enterprise channel broadens meaningfully beyond Azure to capture cloud-neutral and multi-cloud buyers

Investors underwriting all three simultaneously at IPO pricing are accepting substantial compounded uncertainty. Goldman Sachs and Morgan Stanley, as lead underwriters, will need to price that uncertainty into the offering range.

For investors wanting to situate the OpenAI pricing discussion within the broader AI equity environment, our deep-dive into AI stock valuation risk examines how Goldman Sachs’ May 2026 assessment found that AI-related technology spending as a share of US GDP has surpassed the dot-com peak, how index-level calm is masking dangerous distributional divergence at the single-stock level, and why passive investors may be carrying more AI-specific concentration exposure than standard portfolio metrics suggest.

The two S-1 sections that will tell investors the most

When the filing arrives, two sections will carry the most signal for investors evaluating the risk-reward balance:

- Governance disclosure: Specificity on how nonprofit board authority interacts with public shareholder fiduciary rights, and whether the capped-profit structure is clearly defined with disclosed conversion mechanics, will determine whether the governance risk is quantifiable or open-ended

- Path-to-profitability narrative: The explicit assumptions underlying the free-cash-flow timeline, including compute cost trajectory, Microsoft contract terms, and enterprise revenue-mix targets, will reveal whether the margin expansion thesis rests on concrete operational plans or market-condition assumptions outside management’s control

Financial projections referenced in this analysis are subject to market conditions and various risk factors. Past performance does not guarantee future results.

The S-1 will not resolve every question. But it will tell investors whether OpenAI is asking the public market to underwrite a specific plan or a general belief.