Why Off-the-Shelf CAR-T Has an Edge After BTKi Failure

38 mins ago

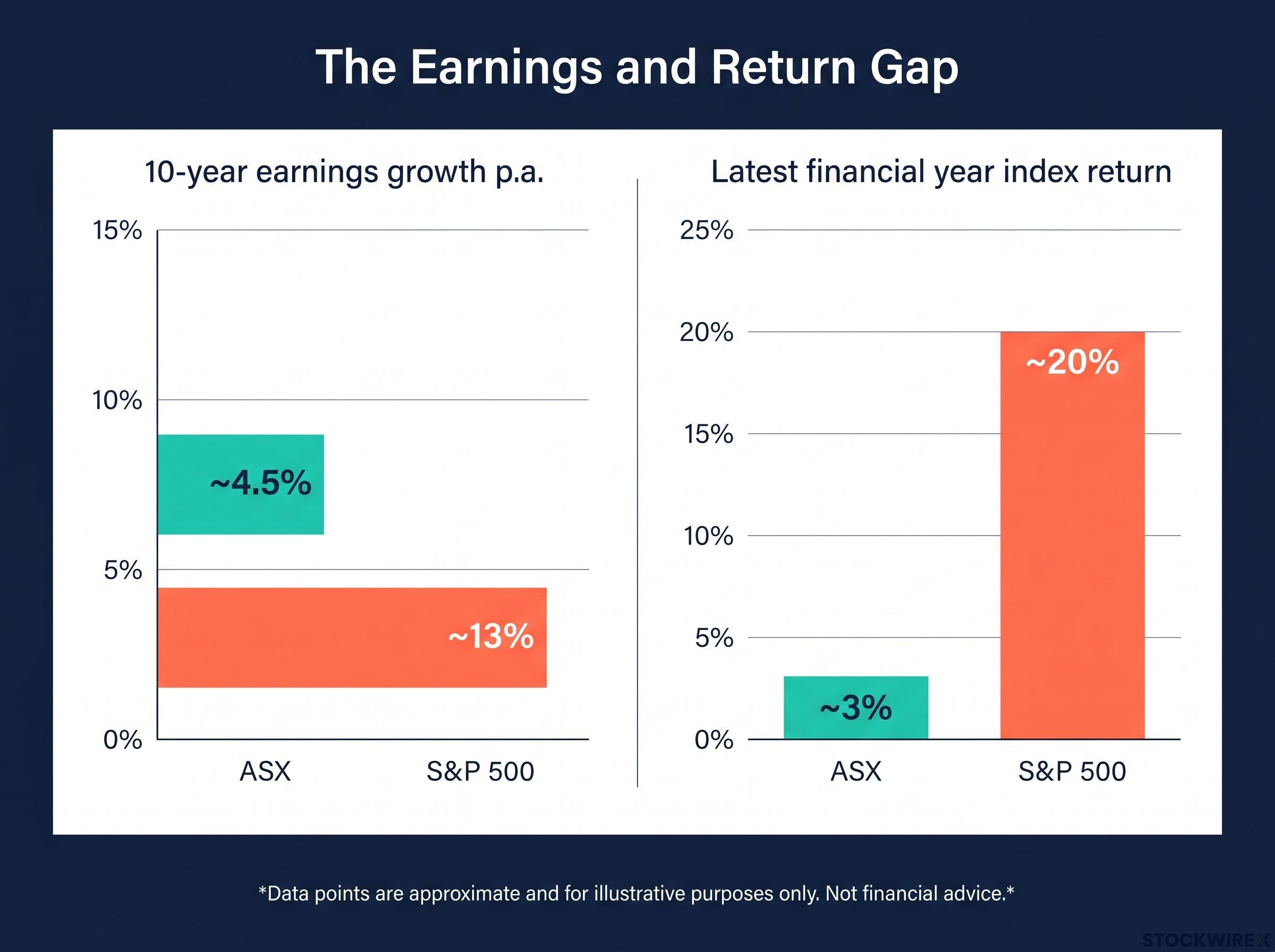

Over the past decade, Australian blue-chip companies grew earnings at roughly 4.5% per year. Their U.S. counterparts compounded at 13%. If you hold ASX blue chips for growth, that gap raises an uncomfortable question: what exactly have you been compounding?

This is not a short-term wobble. The ASX delivered roughly 3% over the latest financial year versus roughly 20% for the S&P 500, and the pattern has repeated across multiple timeframes. Australia holds a remarkable historical record: the 2023 Credit Suisse Global Investment Returns Yearbook ranked it first globally for equity returns across 123 years of data in USD terms. The recent divergence is not inevitable. It is structural, and it is explicable.

Here is the framework for understanding the three forces behind the gap, and for deciding what role, if any, ASX blue chips should play in a growth-oriented portfolio. The diagnosis is specific enough to apply to your own holdings.

Analysis by Mark LaMonica, CFA, published via Morningstar Australia on 19 June 2026, puts the divergence in sharp relief. Over the past decade, the All Ordinaries Index produced estimated earnings growth of around 4.5% per year, while the S&P 500 delivered approximately 13% annual earnings growth across the same period.

That gap is not narrowing. ASX aggregate earnings declined for three consecutive years before a tentative FY26 recovery, while S&P 500 consensus earnings per share (EPS) growth for 2026 sits in the 12.5-15% range.

| Metric | ASX | S&P 500 |

|---|---|---|

| 10-year earnings growth p.a. | ~4.5% | ~13% |

| Latest financial year index return | ~3% | ~20% |

| 2026 consensus EPS growth | Tentative recovery | 12.5-15% |

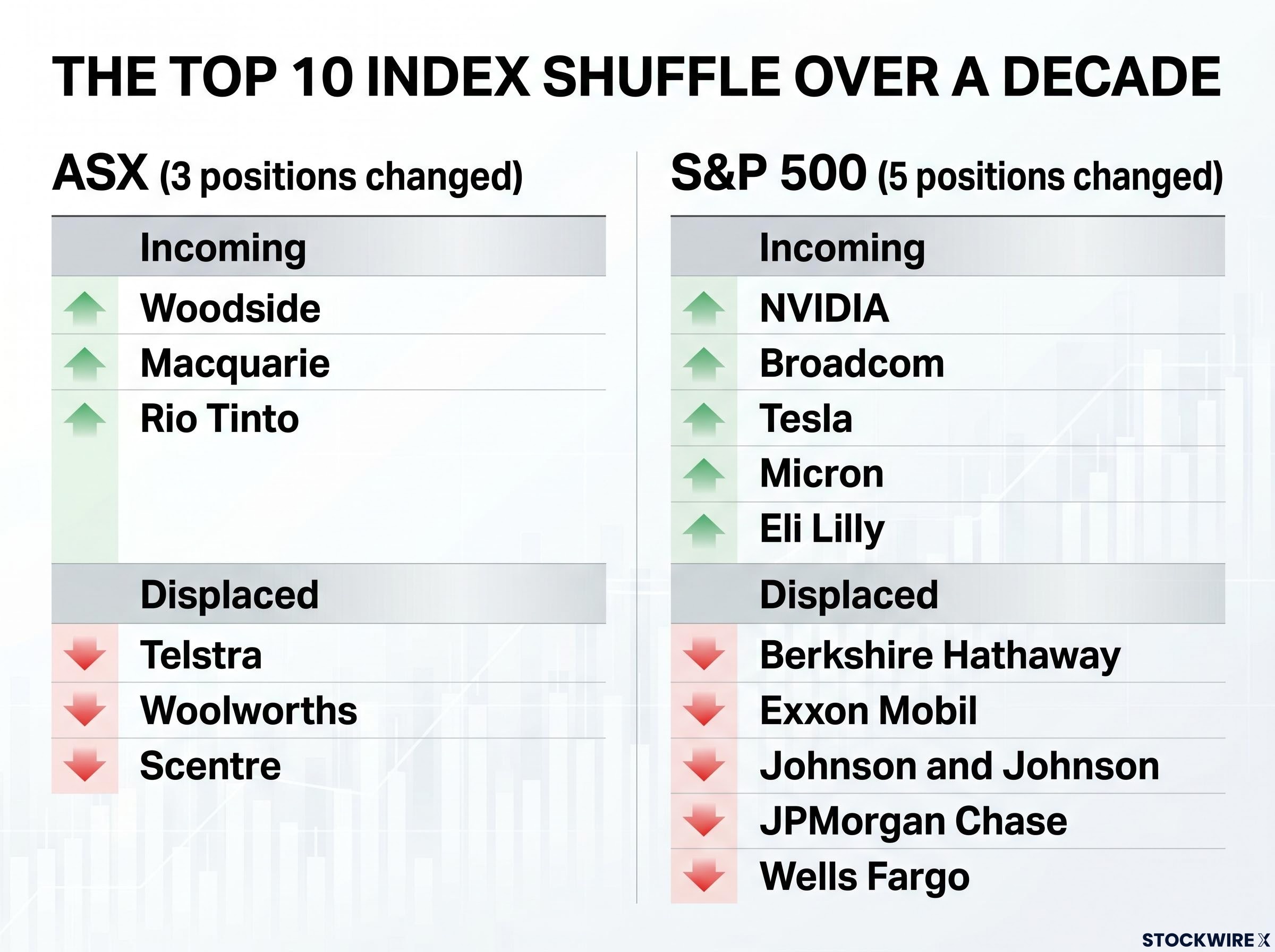

The index-level data becomes even starker at the company level. Of the ten largest ASX-listed companies a decade ago, only two grew net income above the rate of inflation over the subsequent ten years. Four delivered negative total returns.

Among the ten biggest ASX companies by market cap in 2016, just two managed net income growth that kept pace with inflation over the decade that followed, while four produced negative annual total returns across the same period.

The 4.5% versus 13% earnings gap is not a market anomaly to wait out. It tells you that the composition of what you own when you buy an ASX blue-chip fund is fundamentally different from what you own in a U.S. large-cap exposure. The numbers are the opening evidence of that structural difference.

Australia’s franking credit system is the first structural force. It works like this: when an Australian company pays corporate tax and then distributes a dividend, it can attach a franking credit to that dividend. Resident investors, especially retirees and self-managed superannuation funds (SMSFs) in pension phase, can use that credit to offset their own tax liability, sometimes receiving a cash refund. The effect is that franked dividend income is worth materially more on an after-tax basis than an equivalent pre-tax return from other sources.

The franking credit mechanics that drive this payout behaviour are straightforward in principle: when an Australian company pays corporate tax before distributing a dividend, eligible shareholders receive a credit that offsets their own tax liability, and pension-phase SMSFs receive it as a direct ATO cash refund rather than a reduction in tax owed.

According to historical estimates from Australian equity specialists, franking credits have added in the order of 2% per year to total returns for Australian investors able to fully utilise them. That is a genuine benefit. It can close the performance gap against some lower-growth international markets. It does not close the much larger recent gap against U.S. large-cap growth.

The mechanism produces a predictable chain of consequences:

Grossed-up dividend yields across top ASX dividend stocks for 2026 frequently appear in the 6-15% range across utilities, energy, real estate investment trusts (REITs), and smaller industrials. The market is pricing what it values: income, not reinvestment.

U.S. companies face a different set of incentives. Dividends are not especially tax-favoured relative to capital gains. Buybacks are the preferred capital return mechanism, and growth investors actively reward companies that retain earnings and reinvest at high returns. This has supported higher reinvestment rates in U.S. growth sectors, reinforcing the EPS growth differential over time.

For a growth-oriented investor, the franking system’s real effect is to make it economically rational for ASX companies to distribute cash rather than reinvest it. That is not a management failure. It is a structural incentive embedded in the tax code.

The second structural force is what the index actually contains. ASX earnings are dominated by a small cluster of slower-growing, cyclical sectors: the four major banks, plus materials and energy producers concentrated in iron ore, copper, lithium, and gold. Their earnings are driven by credit conditions and commodity price cycles, not by compounding reinvestment.

ASX sector concentration is more severe at the individual stock level than the broad sector percentages imply: VanEck research has shown that two stocks alone have historically represented approximately 22% of a typical cap-weighted Australian equity portfolio, meaning a single large-cap earnings miss can produce a portfolio-wide drag before any other holding moves.

The S&P 500’s dominant weight sits in technology, semiconductors, software, and advanced healthcare, sectors characterised by high-margin recurring revenue with strong returns on reinvestment. Current S&P 500 earnings expectations for 2026 are driven disproportionately by megacap technology and communications stocks.

| Market | Dominant sectors | Earnings drivers |

|---|---|---|

| ASX | Mature banks, commodity producers | Credit growth, net interest margins, global resource cycles |

| S&P 500 | Cloud, AI, semiconductors, platform software, biopharma | High-margin recurring revenue, reinvestment at high returns |

The February 2026 earnings season illustrated a “two-speed economy” within the ASX: banks and insurers benefiting from technology adoption including AI, while discretionary retailers faced cost-of-living pressure. Resources were recovering, but on commodity price strength, not structural business model improvement. Gold was near record highs, copper near record highs, and lithium had more than doubled from its trough.

The composition of the top ten tells the deeper story. Over the decade, three positions in the ASX’s top ten changed hands, with Woodside, Macquarie, and Rio Tinto taking the spots vacated by Telstra, Woolworths, and Scentre. In the U.S., the equivalent reshuffle was far more dramatic: five of the S&P 500’s ten largest positions turned over, as NVIDIA, Broadcom, Tesla, Micron, and Eli Lilly displaced Berkshire Hathaway, Exxon Mobil, Johnson and Johnson, JPMorgan Chase, and Wells Fargo.

Five of the ten largest S&P 500 companies were replaced over the decade by names from high-growth sectors, reflecting genuine structural transformation in the U.S. economy.

The S&P 500’s top-ten transformation reflects structural economic change. The ASX’s modest shuffle reflects continuity. Owning the ASX index is a bet on credit growth and commodity cycles, whether or not you have framed it that way.

There is a genuine cyclical positive to acknowledge. Resources earnings have improved as gold, copper, and lithium prices rebounded. FY26 is expected to mark the end of three consecutive years of declining ASX aggregate earnings. The ASX even outperformed the U.S. on a monthly basis in June 2026, as Wall Street dipped while resources and selected domestic sectors held up.

Those are real data points. They do not resolve the structural question.

The return gap between ASX and international markets in 2026 extends well beyond the US comparison: Taiwan’s TAIEX gained 57% and the Nikkei surged over 40% over the same period that the ASX 200 returned roughly 1.3% year-to-date, a divergence driven by identical structural forces, no large-cap technology, no semiconductor exposure, and no stimulus narrative, rather than by short-term currency or commodity movements.

Cyclical tailwinds (current, time-limited):

Structural headwinds (persistent, slow-moving):

The ASX’s 3% full-year return versus the S&P 500’s roughly 20% shows that even a commodity recovery did not close the gap. Analysts warn the FY26 recovery remains vulnerable to runaway inflation, labour market deterioration, or a global growth shock, all of which would disproportionately affect the domestic banks and retailers that anchor the index.

For the index-level earnings trajectory to shift meaningfully, three things would need to happen: a meaningful multifactor productivity uplift across the domestic economy; the emergence of globally scaled Australian technology or biotech companies that shift index sector weights; or a sustained new commodity supercycle of the kind not seen since the China-led surge of the 2000s. Each is a genuine possibility worth monitoring. None is currently underway.

The current commodity-driven recovery tells you the ASX can outperform in specific windows. It does not change the structural architecture of the index, and that distinction is the most important one a growth investor can draw from the data.

The structural diagnosis splits cleanly by investor type.

If your priority is income and tax efficiency:

If your priority is real earnings growth:

Three questions to ask about any individual ASX holding:

1. What is this company’s reinvestment rate? 2. Is it delivering real, inflation-adjusted earnings growth? 3. What would need to change structurally for it to grow faster?

The income-versus-growth split is not a judgment about which approach is better. It is a clarity tool that allows you to assign ASX blue chips the correct portfolio role rather than expecting them to serve both functions simultaneously.

Three structural forces operate as a coherent system. Sector composition concentrates ASX earnings in cyclical industries. The franking incentive diverts capital from reinvestment to distribution. Weak domestic productivity limits what remains.

Australia’s extraordinary historical record, first globally for equity returns across 123 years in USD terms per the 2023 Credit Suisse Global Investment Returns Yearbook, is not negated by recent underperformance. But it was built in a different structural environment, and it does not guarantee forward-looking replication.

The three structural forces in summary:

Using ASX blue chips as an income engine while accessing growth through international exposure is not a concession to underperformance. It is the rational response to the structural evidence. Investors who understand the architecture of the index they own can deploy it deliberately, calibrating domestic holdings for income and international holdings for growth, rather than expecting a single allocation to deliver both.

For investors wanting to translate the domestic income and international growth split into a concrete fund structure, our comprehensive walkthrough of ETF portfolio construction covers asset allocation methodology, the trade-off between equal-weighted and cap-weighted funds, and the fee-compounding arithmetic that makes fund selection one of the highest-leverage decisions available.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

—

The ASX is structurally concentrated in slow-growing, cyclical sectors like the four major banks and commodity producers, while the S&P 500 is dominated by high-margin technology, semiconductors, and platform software companies that reinvest at high returns. Over the past decade, ASX blue chips compounded earnings at roughly 4.5% per year versus approximately 13% for the S&P 500.

Franking credits make dividend distributions worth materially more on an after-tax basis for resident investors and SMSFs, which pressures ASX boards to maintain high payout ratios. Higher payouts reduce retained earnings available for reinvestment, and lower reinvestment produces slower earnings growth over time, a structural incentive embedded in the tax code rather than a management failure.

The ASX is dominated by mature banks and commodity producers whose earnings are driven by credit conditions and global resource price cycles, not by compounding reinvestment. VanEck research has shown that two stocks alone have historically represented approximately 22% of a typical cap-weighted Australian equity portfolio, meaning buying the ASX index is largely a bet on credit growth and commodity cycles.

FY26 is expected to break three consecutive years of declining ASX aggregate earnings, partly driven by a commodity price recovery in gold, copper, and lithium. However, the structural headwinds, including China's property slowdown suppressing iron ore demand, highly indebted Australian households constraining credit growth, and flat domestic productivity, remain in place and are not resolved by a cyclical commodities rebound.

ASX blue chips are most rationally deployed as an income engine, where franking credits add roughly 2% per year to after-tax returns for eligible investors and grossed-up yields sit in the 6-15% range across top dividend stocks. Growth compounding is better accessed through international exposure, particularly U.S. and selected Asian markets where high-growth sectors like AI infrastructure, semiconductors, and cloud software are concentrated.