ASX Healthcare’s 50-Day Break: Recovery Signal or Bear Bounce?

25 mins ago

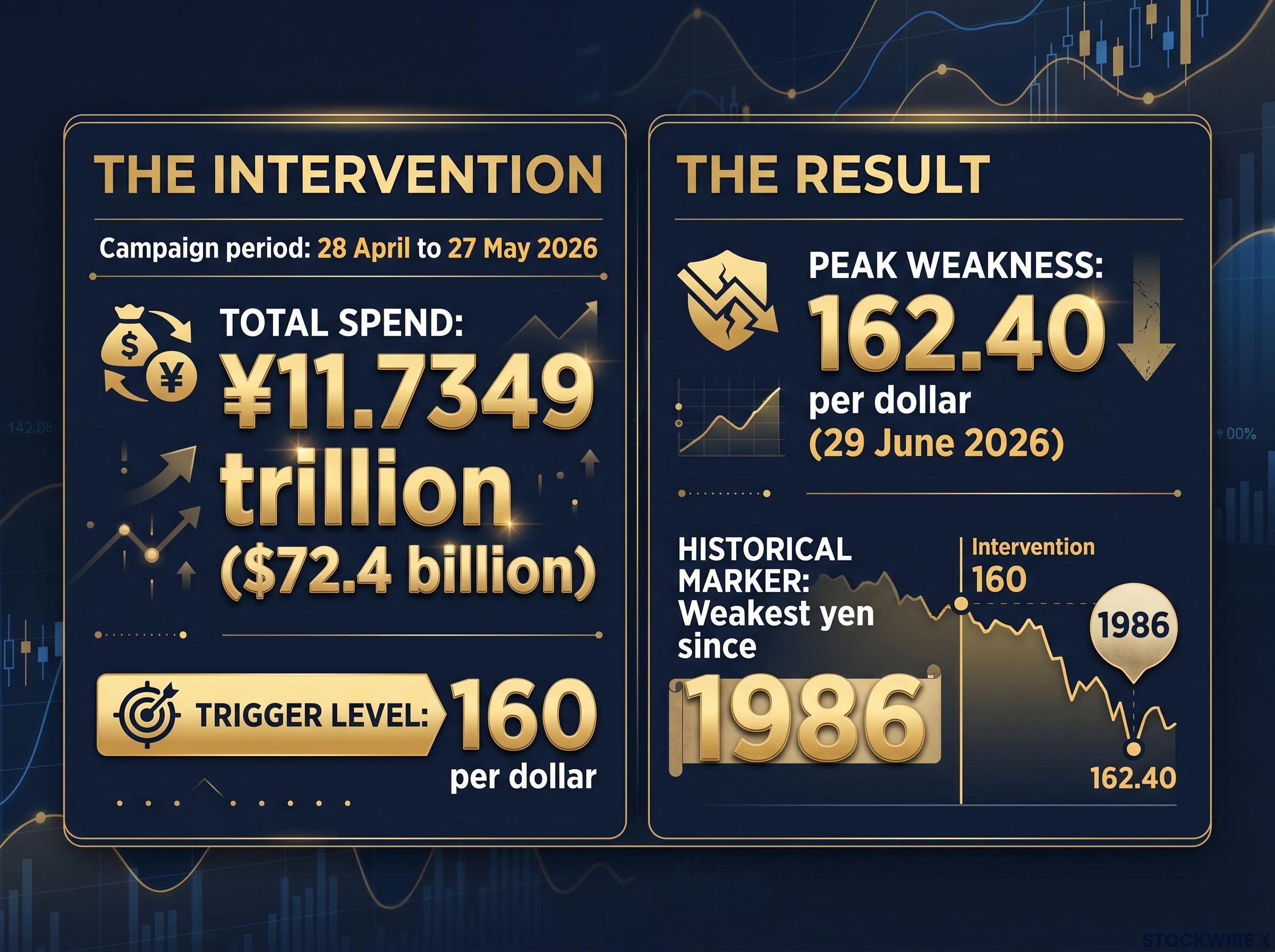

Tokyo deployed ¥11.7349 trillion, approximately $72.4 billion, in a currency market defence operation running from late April through late May. It was the largest foreign exchange intervention campaign in the country’s history. By 29 June 2026, the yen had depreciated to 162.40 per dollar during the Asian session, a level not seen since 1986.

That sequence is the story. Record spending produced a record failure. The question is no longer whether Tokyo is willing to defend its currency; the question is whether the tools it is using can work at all when the structural forces pushing the yen lower remain firmly in place.

Here is the framework for understanding why intervention keeps failing, what the political constraints actually are, and precisely which conditions would need to change before Tokyo’s next move carries any lasting weight.

The yen’s slide did not happen in a single session. It accumulated across weeks, each new low arriving after the previous one had already forced a response.

The Ministry of Finance moved into currency markets on 28 April 2026, after USD/JPY broke through the 160-per-dollar level. In the month that followed, Tokyo committed a record ¥11.7349 trillion (roughly $72.4-$73 billion) to yen-buying operations, a total that exceeded any prior single intervention campaign in Japan’s history.

The Golden Week intervention, estimated at 8-9 trillion yen across a compressed holiday window, also carried a secondary consequence: funding those operations likely required liquidating $40-50 billion in U.S. Treasury holdings, adding a cross-asset dimension that bond investors were slow to price.

By late June, the yen was trading in the 161.8-162.3 range. On 29 June, it reached 162.40, breaching the floor established in July 2024 and printing the currency’s lowest value against the dollar since 1986.

The key intervention statistics tell the story of the gap between effort and result:

Tokyo’s defensive line did not hold. $72 billion was not sufficient to alter the market’s direction. For anyone assessing whether further intervention is worth pricing in, that is the single most important data point.

The interest rate gap between Japan and the United States sits at the centre of the yen’s weakness. The Bank of Japan’s (BOJ) policy rate stood at 1.0% as of June 2026, following a 25 basis point hike. U.S. rates remain significantly higher. That differential makes the yen the world’s preferred cheap funding currency.

The BOJ rate decision on 16 June 2026 delivered a 25-basis-point hike to 1.0% via a 7-1 board vote and paired it with a structured JGB tapering schedule reducing monthly bond purchases by approximately 200 billion yen per quarter, a combination designed to compress the carry spread from both sides simultaneously.

The mechanism is straightforward. Investors borrow in yen at low rates, convert those yen into dollars or other higher-yielding currencies, and pocket the interest rate spread. This is the carry trade, and it creates persistent, structural selling pressure on the yen that operates every day, not just when Japan intervenes.

Scale compounds the problem. Global foreign exchange markets turn over trillions of dollars daily. Even a record ¥11.7 trillion intervention can be absorbed by the market when the underlying flow of capital favours the dollar. The intervention becomes a speed bump, not a roadblock.

Japan is also operating alone. No coordinated intervention involving the U.S. Federal Reserve or the European Central Bank (ECB) has occurred as of 30 June 2026. Unilateral operations carry less signal value because they suggest a local attempt to resist global capital flows rather than a policy consensus.

| Factor | Japan position | U.S. position | Market effect |

|---|---|---|---|

| Policy rate | 1.0% | Significantly higher | Capital flows toward higher-yielding dollar assets |

| 10-year sovereign yield | ~2.6-2.7% | Higher | Bond investors favour U.S. Treasuries over JGBs |

| Carry trade role | Funding currency (borrowed) | Target currency (invested into) | Persistent yen selling pressure |

| FX intervention status | Unilateral, record spend | No participation | Limited credibility signal from Japan acting alone |

Nomura analysts assessed that the Finance Ministry is unlikely to pursue more aggressive intervention while the Takaichi administration continues to lag behind the situation.

For anyone sizing positions around yen exposure, the carry trade arithmetic means that until the rate gap narrows materially, every yen-support operation is a temporary headwind, not a reversal signal.

The carry trade is not a speculative bet. It is a mechanically rational position grounded in a real yield advantage. Understanding why it persists explains why government intervention has structural limits.

The decision process works in four steps:

Japan’s yen is uniquely suited as a carry funding currency because of decades of near-zero rates, deep liquidity, and reliable cheapness relative to alternatives. Even with the BOJ at 1.0%, the rate remains far below a level that would make yen borrowing unattractive.

The risk for carry traders is a rapid unwind. When risk sentiment turns sharply negative or yield differentials compress suddenly, carry positions get closed in a rush, producing violent yen appreciation. That is exactly what happened briefly in August 2024, when a sudden reversal sent the yen sharply higher in days.

The carry trade warning signals that preceded the August 2024 unwind are already partially reconstructed in mid-2026: JGB yields near 2.65% and U.S. 10-year Treasuries at approximately 4.46-4.49% mean the compressed spread is doing structural work, with a USD/JPY breakdown below 160 identified as the remaining trigger for a forced deleveraging cascade.

But verbal warnings and FX operations do not change the yield calculation. They cannot structurally deter carry accumulation. The carry trade will only be unwound when the maths of yield differentials shifts, which means government rhetoric alone is not a market-moving force.

Prime Minister Sanae Takaichi has held office since October 2025, and her administration’s intellectual inheritance is the problem as much as it is the platform. The Abenomics tradition of loose monetary conditions, which she has broadly continued, is the same policy framework that contributed to the yen’s structural weakness.

The political contradiction sits at the centre of the crisis. Advocating decisively for tighter BOJ policy would amount to publicly conceding that prior loose frameworks contributed to the currency’s collapse. For a government still associated with those frameworks, that is a significant political cost.

From the other direction, the pressure is equally intense. A weak yen raises import prices for energy and food, squeezing households and small businesses. The economic pain is visible and growing, making inaction its own form of political risk.

Senior officials have followed the verbal warning playbook. Chief Cabinet Secretary Minoru Kihara and Finance Minister Satsuki Katayama have both issued statements emphasising vigilance and readiness to act. Markets now treat this rhetoric as a predictable cycle rather than a signal of regime change. The warnings come, the intervention follows, the yen weakens further, and the cycle repeats.

The most effective policy response, decisive BOJ tightening backed by credible fiscal communication, is also the one that carries the highest political cost for this specific administration. That is why the market is not pricing in a turnaround.

The diagnosis is clear. The question is what would alter it. Four conditions, ordered by structural importance, define the path from failed intervention to durable recovery:

The BOJ monetary policy decisions for 2026 confirm the June rate move to 1.0%, a level that still leaves yen borrowing costs far below what would be required to meaningfully deter carry trade accumulation against higher-yielding dollar assets.

Each of these conditions is achievable in principle. None is imminent. That is why the current yen level is likely to persist unless a specific catalyst materialises.

Intervention buys time. It does not buy reversal. Each new record spend that fails to hold reinforces market confidence in testing lower levels.

The credibility erosion is specific and measurable. The 160-per-dollar level was defended at historic cost. It was then breached within weeks. When a “line in the sand” falls that visibly, the market signal is that authorities’ tolerance is finite and their ammunition is not unlimited. Traders read that as permission to press further.

USD/JPY is trading in the 161.8-162.3 zone, the weakest since 1986. A further slide toward 165 or beyond is the market’s current default expectation unless a specific catalyst changes the calculus. Waiting for the next intervention to hold is not a reliable strategy.

What to watch from here:

Japan’s intervention failure is not a failure of will or resources. It is a failure of the policy mix to address the profit motive behind yen selling. The Ministry of Finance can execute FX operations, shape fiscal communication, and apply pressure on the BOJ. It cannot set U.S. rate policy, control global dollar dynamics, or compel G7 partners to coordinate.

The most plausible near-term catalyst for a shift remains a change in Federal Reserve guidance that compresses the rate differential, even partially. A Fed signal toward easing would weaken the carry trade’s arithmetic and give intervention operations a tailwind they have not had.

As of late June 2026, those conditions are not in place. The market is pricing that assessment correctly.

Intervention is failing not because authorities lack money or will, but because they have not changed the underlying incentives that make selling yen profitable.

The yen’s trajectory is a policy choice problem, not a market accident. The variables within Tokyo’s control are narrower than the scale of intervention spending implies. That distinction, between what a government can spend and what it can actually change, is the analytical lens that applies not just to this episode but to every currency crisis where intervention confronts structural forces.

For readers wanting to understand the geopolitical layer compounding Japan’s structural position, our deep-dive into how the Hormuz crisis reshaped forex valuation explains why Japan’s near-total energy import dependence has made the yen uniquely vulnerable to supply-side shocks that do not affect energy-producing currencies in the same way.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The yen carry trade involves borrowing in yen at low interest rates, converting those yen into higher-yielding currencies like the dollar, and pocketing the interest rate differential. With the Bank of Japan's policy rate at just 1.0% in June 2026, this creates persistent, structural selling pressure on the yen every day, not just during market events.

Japan spent a record ¥11.7349 trillion (roughly $72.4 billion) buying yen between late April and late May 2026, yet the currency still fell to 162.40 per dollar, its weakest since 1986. The intervention cannot change the underlying carry trade arithmetic: as long as U.S. rates sit significantly above Japan's 1.0% policy rate, capital flows will favour the dollar over the yen.

USD/JPY hit 162.40 during the Asian session on 29 June 2026, surpassing the July 2024 low and marking the weakest yen reading against the dollar since 1986. That breach came despite Japan's largest-ever FX intervention campaign.

Four conditions matter most: a material narrowing of the U.S.-Japan interest rate differential, coordinated G7 intervention involving the Fed and ECB, a credible domestic policy normalisation package aligning the Ministry of Finance and the BOJ, and a shift in global dollar dynamics such as a Fed easing cycle. None of these conditions were in place as of late June 2026.

Japan committed ¥11.7349 trillion (approximately $72.4-$73 billion) across the period from 28 April to 27 May 2026, the largest single FX intervention campaign in the country's history. It bought a temporary slowdown in the yen's decline but failed to prevent USD/JPY from breaching 160 and ultimately trading above 162.